How does the portfolio possibility curve look like if you have a portfolio consisting of asset...

How does the portfolio possibility curve look like if you have a portfolio consisting of asset A (a share with a volatility of 10% and an expected return of 8%) and asset B which is risk-free (rf 1%)?

Please sketch the curve and indicate clearly the min. variance and the max. sharpe point.

Another question from me relating this question: what would the sigma (variance) of a risk-free asset be?

Homework Answers

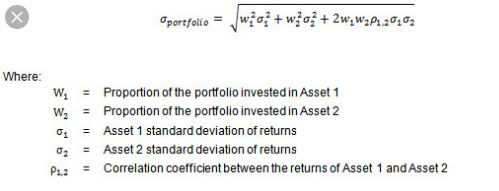

Portfolio Possibility Curve is also known as Efficient frontier curve which tells us set of optimal portfolios (share of two assets in a portfolio) that offer highest expected return over a given risk level (standard deviation/variance) or lowest risk at a specified return.

As per the figures provided in question,

Asset A: Return = 8% Risk = 10%

Asset B: Return = 1% Risk = 0% (since, it's risk free)

The portfolio possibility curve would look like as below,

The curve has been made with following weights of each asset. At each point, variance of the portfolio is calculated by using below formula and expected return is calculated using weighted average method.

| Weight | Weight | Standard | Expected |

| Security 1 | Security 2 | Deviation | Return |

| 1.0 | 0.0 | 0.10000 | 0.08000 |

| 0.9 | 0.1 | 0.09000 | 0.07300 |

| 0.8 | 0.2 | 0.08200 | 0.06740 |

| 0.7 | 0.3 | 0.07000 | 0.05900 |

| 0.6 | 0.4 | 0.06000 | 0.05200 |

| 0.5 | 0.5 | 0.05000 | 0.04500 |

| 0.4 | 0.6 | 0.04000 | 0.03800 |

| 0.3 | 0.7 | 0.03000 | 0.03100 |

| 0.1 | 0.9 | 0.01236 | 0.01865 |

| 0.1 | 0.9 | 0.01000 | 0.01700 |

| 0.0 | 1.0 | 0.00000 | 0.01000 |

The Minimum Variance Portfolio is when the risk is minimum. In this case, asset A (share = 0%) and asset B (share = 100%) will be Min Variance portfolio as the risk will be 0% and the return will be 1%.

The max Sharpe ratio point will be all the points on the curve except when the return and risk both are zero. Sharpe ratio is 0.7 in each case. It is calculated by using formula (Rp-Rf)/SigmaP.

The sigma of risk free asset would be 0 because it provides constant return without any volatility.

Add Answer to:

How does the portfolio possibility curve look like if you have a

portfolio consisting of asset...

The risk-free rate is 0%. The market portfolio has an expected return of 20% and a volatility of 20%. You have $100 to invest. You decide to build a portfolio P which invests in both the risk-free investment and the market portfolio.

The risk-free rate is 0%. The market portfolio has an expected return of 20% and a volatility of 20%. You have $100 to invest. You decide to build a portfolio P which invests in both the risk-free investment and the market portfolio.a. How much should you invest in the market portfolio and the risk-free investment if you want portfolio P to have an expected return of 40%?b. How much should you invest in the market portfolio and the risk-free investment...

I would like part d and e answered please 2. Consider the information in Table 1...

I would like part d and e answered please

2. Consider the information in Table 1 Table 1 Correlation with market portfolio 0.20 0.80 1.00 0.00 Standard deviation Return Beta Stock 1 Stock 2 Market portfolio 6% 12% 8% 0% 16% 2% Risk-free asset 0 (a) Consider Table 1. Calculate betas for stock 1 and stock 2. (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for stocks 1 and 2. (c) Consider Table 1 and...

I would like part d and e answered please

2. Consider the information in Table 1 Table 1 Correlation with market portfolio 0.20 0.80 1.00 0.00 Standard deviation Return Beta Stock 1 Stock 2 Market portfolio 6% 12% 8% 0% 16% 2% Risk-free asset 0 (a) Consider Table 1. Calculate betas for stock 1 and stock 2. (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for stocks 1 and 2. (c) Consider Table 1 and...

Investment Portfolio You are an investment manager for Simple Asset Management, a company that specializes in...

Investment Portfolio You are an investment manager for Simple Asset Management, a company that specializes in developing simple investment portfolios consisting of no more than three assets such as stocks, bonds, etc., for investors who like to keep things simple. One of your more popular investments is called the All World Fund and is composed of global stocks with good dividend yields. A client is interested in constructing a portfolio that consists of the All World Fund and the Treasury...

Sample Test Problem 7.03 You have just invested in a portfolio of three stocks. The amount...

Sample Test Problem 7.03 You have just invested in a portfolio of three stocks. The amount of money that you invested in each stock and its beta are summarized below Stock Investment Beta $188,000 1.51 А 282,000 0.52 В 470,000 1.35 с Calculate the beta of the portfolio and use the Capital Asset Pricing Model (CAPM) to compute the expected rate of return for the portfolio. Assume that the expected rate of return on the market is 18 percent and...

Sample Test Problem 7.03 You have just invested in a portfolio of three stocks. The amount of money that you invested in each stock and its beta are summarized below Stock Investment Beta $188,000 1.51 А 282,000 0.52 В 470,000 1.35 с Calculate the beta of the portfolio and use the Capital Asset Pricing Model (CAPM) to compute the expected rate of return for the portfolio. Assume that the expected rate of return on the market is 18 percent and...

Your answer is incorrect. Try again. You have just invested in a portfolio of three stocks....

Your answer is incorrect. Try again. You have just invested in a portfolio of three stocks. The amount of money that you invested in each stock and its beta are summarized below. Stock А Beta 1.52 Investment $196,000 294,000 490,000 0.55 1.34 Calculate the beta of the portfolio and use the Capital Asset Pricing Model (CAPM) to compute the expected rate of return for the portfolio. Assume that the expected rate of return on the market is 18 percent and...

Your answer is incorrect. Try again. You have just invested in a portfolio of three stocks. The amount of money that you invested in each stock and its beta are summarized below. Stock А Beta 1.52 Investment $196,000 294,000 490,000 0.55 1.34 Calculate the beta of the portfolio and use the Capital Asset Pricing Model (CAPM) to compute the expected rate of return for the portfolio. Assume that the expected rate of return on the market is 18 percent and...

please answer question 4 Examples on Asset Pricing Models 1. You are given the following equilibrium...

please answer question 4

Examples on Asset Pricing Models 1. You are given the following equilibrium expected returns and risks -07: 12 ke (RA) - 12.296; E(R) -15.556; No. 0. 015 a. What is the equation of the Security Market Line? b. A portfolio, made up of A (above) and another security, has a beta of 1.10 and expected return of 1396Which one would you rather buy - A alone or the portfolio? Why? ES 1.6 I OVAL B A...

please answer question 4

Examples on Asset Pricing Models 1. You are given the following equilibrium expected returns and risks -07: 12 ke (RA) - 12.296; E(R) -15.556; No. 0. 015 a. What is the equation of the Security Market Line? b. A portfolio, made up of A (above) and another security, has a beta of 1.10 and expected return of 1396Which one would you rather buy - A alone or the portfolio? Why? ES 1.6 I OVAL B A...

question 2 Examples on Asset Pricing Mode 1. You are given the following equilibrium expected returns...

question 2

Examples on Asset Pricing Mode 1. You are given the following equilibrium expected returns and risks 7 (R- es-2 E(RA)- 12.2 % ; E(Ra)-15.5 % ; Ba-1.25 BA-0.7; .£{{¢*6,4 *రి 6 a What is the equation of the Security Market Line? b. A portfolio, made up of A (above) and another security, has a beta of 1.10 and expected return of 13 %. Which one would you rather buy- A alone or the portfolio? Why? (R) 4-6 7...

question 2

Examples on Asset Pricing Mode 1. You are given the following equilibrium expected returns and risks 7 (R- es-2 E(RA)- 12.2 % ; E(Ra)-15.5 % ; Ba-1.25 BA-0.7; .£{{¢*6,4 *రి 6 a What is the equation of the Security Market Line? b. A portfolio, made up of A (above) and another security, has a beta of 1.10 and expected return of 13 %. Which one would you rather buy- A alone or the portfolio? Why? (R) 4-6 7...

please answer question #1 7 1. You are given the following equilibrium expected returns and risks...

please answer question #1

7 1. You are given the following equilibrium expected returns and risks E(R) - 12.2%; E(Re) - 15.5% BA -0.7; Be-1.25. c( 0.460.0615 a. What is the equation of the Security Market Line? b. A portfolio, made up of A (above) and another security, has a beta of 1.10 and expected return of 13%. Which one would you rather buy - A alone or the portfolio? Why? Ee19. 6 - OVAL BYA c. Given the SML...

please answer question #1

7 1. You are given the following equilibrium expected returns and risks E(R) - 12.2%; E(Re) - 15.5% BA -0.7; Be-1.25. c( 0.460.0615 a. What is the equation of the Security Market Line? b. A portfolio, made up of A (above) and another security, has a beta of 1.10 and expected return of 13%. Which one would you rather buy - A alone or the portfolio? Why? Ee19. 6 - OVAL BYA c. Given the SML...

Date: Names Directions: You must work with one or two other students on this take-home exam and you may use your textbo...

Date: Names Directions: You must work with one or two other students on this take-home exam and you may use your textbook. Your work answering Questions 1 and 2 can be shared, but each of you must do your own Question 3, where each of you will pose your own question based on the data. Only one project will be turned for each team, consisting of joint answers for Questions 1 and 2, and as many Questions 3 answers are...

Date: Names Directions: You must work with one or two other students on this take-home exam and you may use your textbook. Your work answering Questions 1 and 2 can be shared, but each of you must do your own Question 3, where each of you will pose your own question based on the data. Only one project will be turned for each team, consisting of joint answers for Questions 1 and 2, and as many Questions 3 answers are...

How can we assess whether a project is a success or a failure? This case presents...

How can we assess whether a project is a success or a

failure?

This case presents two phases of a large business transformation project involving the implementation of an ERP system with the aim of creating an integrated company. The case illustrates some of the challenges associated with integration. It also presents the obstacles facing companies that undertake projects involving large information technology projects. Bombardier and Its Environment Joseph-Armand Bombardier was 15 years old when he built his first snowmobile...

How can we assess whether a project is a success or a

failure?

This case presents two phases of a large business transformation project involving the implementation of an ERP system with the aim of creating an integrated company. The case illustrates some of the challenges associated with integration. It also presents the obstacles facing companies that undertake projects involving large information technology projects. Bombardier and Its Environment Joseph-Armand Bombardier was 15 years old when he built his first snowmobile...

I would like part d and e answered please

2. Consider the information in Table 1 Table 1 Correlation with market portfolio 0.20 0.80 1.00 0.00 Standard deviation Return Beta Stock 1 Stock 2 Market portfolio 6% 12% 8% 0% 16% 2% Risk-free asset 0 (a) Consider Table 1. Calculate betas for stock 1 and stock 2. (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for stocks 1 and 2. (c) Consider Table 1 and...

I would like part d and e answered please

2. Consider the information in Table 1 Table 1 Correlation with market portfolio 0.20 0.80 1.00 0.00 Standard deviation Return Beta Stock 1 Stock 2 Market portfolio 6% 12% 8% 0% 16% 2% Risk-free asset 0 (a) Consider Table 1. Calculate betas for stock 1 and stock 2. (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for stocks 1 and 2. (c) Consider Table 1 and...

Sample Test Problem 7.03 You have just invested in a portfolio of three stocks. The amount of money that you invested in each stock and its beta are summarized below Stock Investment Beta $188,000 1.51 А 282,000 0.52 В 470,000 1.35 с Calculate the beta of the portfolio and use the Capital Asset Pricing Model (CAPM) to compute the expected rate of return for the portfolio. Assume that the expected rate of return on the market is 18 percent and...

Sample Test Problem 7.03 You have just invested in a portfolio of three stocks. The amount of money that you invested in each stock and its beta are summarized below Stock Investment Beta $188,000 1.51 А 282,000 0.52 В 470,000 1.35 с Calculate the beta of the portfolio and use the Capital Asset Pricing Model (CAPM) to compute the expected rate of return for the portfolio. Assume that the expected rate of return on the market is 18 percent and...

Your answer is incorrect. Try again. You have just invested in a portfolio of three stocks. The amount of money that you invested in each stock and its beta are summarized below. Stock А Beta 1.52 Investment $196,000 294,000 490,000 0.55 1.34 Calculate the beta of the portfolio and use the Capital Asset Pricing Model (CAPM) to compute the expected rate of return for the portfolio. Assume that the expected rate of return on the market is 18 percent and...

Your answer is incorrect. Try again. You have just invested in a portfolio of three stocks. The amount of money that you invested in each stock and its beta are summarized below. Stock А Beta 1.52 Investment $196,000 294,000 490,000 0.55 1.34 Calculate the beta of the portfolio and use the Capital Asset Pricing Model (CAPM) to compute the expected rate of return for the portfolio. Assume that the expected rate of return on the market is 18 percent and...

please answer question 4

Examples on Asset Pricing Models 1. You are given the following equilibrium expected returns and risks -07: 12 ke (RA) - 12.296; E(R) -15.556; No. 0. 015 a. What is the equation of the Security Market Line? b. A portfolio, made up of A (above) and another security, has a beta of 1.10 and expected return of 1396Which one would you rather buy - A alone or the portfolio? Why? ES 1.6 I OVAL B A...

please answer question 4

Examples on Asset Pricing Models 1. You are given the following equilibrium expected returns and risks -07: 12 ke (RA) - 12.296; E(R) -15.556; No. 0. 015 a. What is the equation of the Security Market Line? b. A portfolio, made up of A (above) and another security, has a beta of 1.10 and expected return of 1396Which one would you rather buy - A alone or the portfolio? Why? ES 1.6 I OVAL B A...

question 2

Examples on Asset Pricing Mode 1. You are given the following equilibrium expected returns and risks 7 (R- es-2 E(RA)- 12.2 % ; E(Ra)-15.5 % ; Ba-1.25 BA-0.7; .£{{¢*6,4 *రి 6 a What is the equation of the Security Market Line? b. A portfolio, made up of A (above) and another security, has a beta of 1.10 and expected return of 13 %. Which one would you rather buy- A alone or the portfolio? Why? (R) 4-6 7...

question 2

Examples on Asset Pricing Mode 1. You are given the following equilibrium expected returns and risks 7 (R- es-2 E(RA)- 12.2 % ; E(Ra)-15.5 % ; Ba-1.25 BA-0.7; .£{{¢*6,4 *రి 6 a What is the equation of the Security Market Line? b. A portfolio, made up of A (above) and another security, has a beta of 1.10 and expected return of 13 %. Which one would you rather buy- A alone or the portfolio? Why? (R) 4-6 7...

please answer question #1

7 1. You are given the following equilibrium expected returns and risks E(R) - 12.2%; E(Re) - 15.5% BA -0.7; Be-1.25. c( 0.460.0615 a. What is the equation of the Security Market Line? b. A portfolio, made up of A (above) and another security, has a beta of 1.10 and expected return of 13%. Which one would you rather buy - A alone or the portfolio? Why? Ee19. 6 - OVAL BYA c. Given the SML...

please answer question #1

7 1. You are given the following equilibrium expected returns and risks E(R) - 12.2%; E(Re) - 15.5% BA -0.7; Be-1.25. c( 0.460.0615 a. What is the equation of the Security Market Line? b. A portfolio, made up of A (above) and another security, has a beta of 1.10 and expected return of 13%. Which one would you rather buy - A alone or the portfolio? Why? Ee19. 6 - OVAL BYA c. Given the SML...

Date: Names Directions: You must work with one or two other students on this take-home exam and you may use your textbook. Your work answering Questions 1 and 2 can be shared, but each of you must do your own Question 3, where each of you will pose your own question based on the data. Only one project will be turned for each team, consisting of joint answers for Questions 1 and 2, and as many Questions 3 answers are...

Date: Names Directions: You must work with one or two other students on this take-home exam and you may use your textbook. Your work answering Questions 1 and 2 can be shared, but each of you must do your own Question 3, where each of you will pose your own question based on the data. Only one project will be turned for each team, consisting of joint answers for Questions 1 and 2, and as many Questions 3 answers are...

How can we assess whether a project is a success or a

failure?

This case presents two phases of a large business transformation project involving the implementation of an ERP system with the aim of creating an integrated company. The case illustrates some of the challenges associated with integration. It also presents the obstacles facing companies that undertake projects involving large information technology projects. Bombardier and Its Environment Joseph-Armand Bombardier was 15 years old when he built his first snowmobile...

How can we assess whether a project is a success or a

failure?

This case presents two phases of a large business transformation project involving the implementation of an ERP system with the aim of creating an integrated company. The case illustrates some of the challenges associated with integration. It also presents the obstacles facing companies that undertake projects involving large information technology projects. Bombardier and Its Environment Joseph-Armand Bombardier was 15 years old when he built his first snowmobile...

Most questions answered within 3 hours.

-

Considering gravitational time dilation, calculate the time that

passes in Earth’s surface while 1 hour passes...

asked 12 minutes ago -

Minitab Problem: Take the Lake Hume June rainfall data and find

use the processes outlined in...

asked 1 hour ago -

X Company is trying to decide whether to continue using old

equipment to make Product A...

asked 1 hour ago -

IN PYTHON ONLY !! Program 2: Re-work

program #5 (WeeklyHours) from the previous assignment such that...

asked 1 hour ago -

The average length of time between arrivals at a turnpike

toll-booth is 26 seconds. What is...

asked 3 hours ago -

(a) A piston at 6.1 atm contains a gas that occupies a volume of

3.5 L....

asked 4 hours ago -

Please answer true or false. Words

cannot be changed or added in to make it true...

asked 4 hours ago -

An empty test tube weighs 15.923 grams. Then,

MgCl2•6H2O is added into the test tube. After...

asked 4 hours ago -

Assume memory access is 10 units of time and disk access is

10000 units of time....

asked 4 hours ago -

1. Are all good samples random?

2. Magazines often report surveys giving statistics such as “63%...

asked 5 hours ago -

Under all the various types of market structures, firms

must eventually earn some economic profits for...

asked 5 hours ago -

Consider the following fitness regime for a single locus trait

with two co-dominant alleles: w11 =...

asked 5 hours ago