Homework Answers

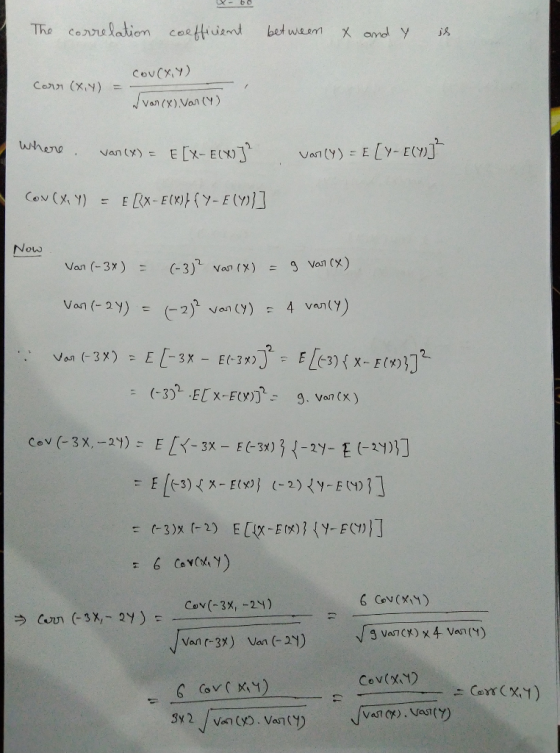

Ans. Since variances as well as coavariances are independent of change of origin but depend on change of scale.

The correlation coefficient is ratio of covariance and variance, being independent of change of origin and sclae but depend on sign.

Add Answer to:

11. Let the correlation coefficient of X and Y be ρ(X,Y)-N C XY VVar(X)VVar(Y) -p(X, Y)....

Let ρ represent the true population coefficient of correlation of two variables X and Y ....

Let ρ represent the true population coefficient of correlation of two variables X and Y . Suppose you want to test the hypothesis that ρ = 0. Explain how you would test this hypothesis. [Hint: by the relationship between b1 and rXY ]

20, variances a,a and correlation 4. Let X. Y be normal bivariate r.v. with coefficient p....

20, variances a,a and correlation 4. Let X. Y be normal bivariate r.v. with coefficient p. a) Write what are E (X|Y), var (X|Y)? b) Show that σi + σισ E (XXY) afo(-p) +2pa 102+0 var (XXY 2) Hint. (X, XY)is normal bivariate: apply a).

20, variances a,a and correlation 4. Let X. Y be normal bivariate r.v. with coefficient p. a) Write what are E (X|Y), var (X|Y)? b) Show that σi + σισ E (XXY) afo(-p) +2pa 102+0 var (XXY 2) Hint. (X, XY)is normal bivariate: apply a).

4.2 The Correlation Coefficient 1. Let the random variables X and Y have the joint PMF...

4.2 The Correlation Coefficient 1. Let the random variables X and Y have the joint PMF of the form x + y , x= 1,2, y = 1,2,3. p(x,y) = 21 They satisfy 11 12 Mx = 16 of = 12 of = 212 2 My = 27 Find the covariance Cov(X,Y) and the correlation coefficient p. Are X and Y independent or dependent?

4.2 The Correlation Coefficient 1. Let the random variables X and Y have the joint PMF of the form x + y , x= 1,2, y = 1,2,3. p(x,y) = 21 They satisfy 11 12 Mx = 16 of = 12 of = 212 2 My = 27 Find the covariance Cov(X,Y) and the correlation coefficient p. Are X and Y independent or dependent?

3. Suppose that (M, ρ) is a compact metric space and f : (M, p)-+ (M,p) is a function such that (Vz, y E M) ρ (z, y) ρ (f (x), f (y)). a. Let x E (M, ρ) and consider the sequence of points {f(n)...

3. Suppose that (M, ρ) is a compact metric space and f : (M, p)-+ (M,p) is a function such that (Vz, y E M) ρ (z, y) ρ (f (x), f (y)). a. Let x E (M, ρ) and consider the sequence of points {f(n) (X)}n 1 . (Remember: fn) denotes the composition of f with itself, n times, so for each n, f+() rn, k E N) such that ρ (f(m) (x) ,f(n +k) (r)) < ε ....

3. Suppose that (M, ρ) is a compact metric space and f : (M, p)-+ (M,p) is a function such that (Vz, y E M) ρ (z, y) ρ (f (x), f (y)). a. Let x E (M, ρ) and consider the sequence of points {f(n) (X)}n 1 . (Remember: fn) denotes the composition of f with itself, n times, so for each n, f+() rn, k E N) such that ρ (f(m) (x) ,f(n +k) (r)) < ε ....

56. Let S = N × N and let ρ be a binary relation on şdefined...

56. Let S = N × N and let ρ be a binary relation on şdefined by (x,y)ρ(z, w)艹x + y-z + w. Show that p is an equivalence relation on S and describe the resulting equivalence classes.

56. Let S = N × N and let ρ be a binary relation on şdefined by (x,y)ρ(z, w)艹x + y-z + w. Show that p is an equivalence relation on S and describe the resulting equivalence classes.

Let X and Y have the following joint distribution X/Y 0 1 0 0.4 0.1 1...

Let X and Y have the following joint distribution X/Y 0 1 0 0.4 0.1 1 0.1 0.1 2 0.1 0.2 a) Find Cov(4+2X, 3-2Y) b) Let Z = 3X-2Y+2 Find E[Z] and σ 2Z c) Calculate the correlation coefficient between X and Y. What does this suggest about the relationship between X and Y? d) Show that for two nonzero constants a and b Cov(X+a, Y+b) = Cov(X,Y)

4.7 Let r'n be the Pearson correlation coefficient from a sample size of n. It is...

4.7 Let r'n be the Pearson correlation coefficient from a sample size of n. It is known that rn is asymptotically distributed as N (p, (1 – p2)2/n), where p is the population correlation coefficient. Show that Fisher's Z-transformation Z = { In((1 + ra)/(1 – in)) is actually a variance-stabilizing transformation.

4.7 Let r'n be the Pearson correlation coefficient from a sample size of n. It is known that rn is asymptotically distributed as N (p, (1 – p2)2/n), where p is the population correlation coefficient. Show that Fisher's Z-transformation Z = { In((1 + ra)/(1 – in)) is actually a variance-stabilizing transformation.

(a) Find the correlation coefficient ρX,Y . (b) Are X and Y independent? Explain why. Let...

(a) Find the correlation coefficient ρX,Y .

(b) Are X and Y independent? Explain why.

Let (X, Y) have joint pdf given by 0 y 00, ey f(x, y) 0, o.w., (a) Find the correlation coefficient px,y. (20 pts) (b) Are X and Y independent? Explain why. (10 pts)

(a) Find the correlation coefficient ρX,Y .

(b) Are X and Y independent? Explain why.

Let (X, Y) have joint pdf given by 0 y 00, ey f(x, y) 0, o.w., (a) Find the correlation coefficient px,y. (20 pts) (b) Are X and Y independent? Explain why. (10 pts)

6.72 Let Y =X+N where X and N are independent Gaussian random variables with different variance and N is zero mean. (a) Plot the correlation coefficient between the “observed signal” Y and the “desire...

6.72 Let Y =X+N where X and N are independent Gaussian random variables with different variance and N is zero mean. (a) Plot the correlation coefficient between the “observed signal” Y and the “desired signal” X as a funtion of the signal-to-noise ratio (b) Find the minimum mean square error estimator for X given Y (c)Find the MAP and ML estimators for X given Y (d) Compare the mean square error of the estimators in parts a, b, and c.

5. Let X1,X2, . , Xn be a random sample from a distribution with finite variance. Show that (i) COV(Xi-X, X )-0 f ) ρ (Xi-XX,-X)--n-1, 1 # J, 1,,-1, , n. OV&.for any two random variables X and Y)...

5. Let X1,X2, . , Xn be a random sample from a distribution with finite variance. Show that (i) COV(Xi-X, X )-0 f ) ρ (Xi-XX,-X)--n-1, 1 # J, 1,,-1, , n. OV&.for any two random variables X and Y) or each 1, and (11 CoV(X,Y) var(x)var(y) (Recall that p vararo

5. Let X1,X2, . , Xn be a random sample from a distribution with finite variance. Show that (i) COV(Xi-X, X )-0 f ) ρ (Xi-XX,-X)--n-1, 1 # J,...

5. Let X1,X2, . , Xn be a random sample from a distribution with finite variance. Show that (i) COV(Xi-X, X )-0 f ) ρ (Xi-XX,-X)--n-1, 1 # J, 1,,-1, , n. OV&.for any two random variables X and Y) or each 1, and (11 CoV(X,Y) var(x)var(y) (Recall that p vararo

5. Let X1,X2, . , Xn be a random sample from a distribution with finite variance. Show that (i) COV(Xi-X, X )-0 f ) ρ (Xi-XX,-X)--n-1, 1 # J,...

20, variances a,a and correlation 4. Let X. Y be normal bivariate r.v. with coefficient p. a) Write what are E (X|Y), var (X|Y)? b) Show that σi + σισ E (XXY) afo(-p) +2pa 102+0 var (XXY 2) Hint. (X, XY)is normal bivariate: apply a).

20, variances a,a and correlation 4. Let X. Y be normal bivariate r.v. with coefficient p. a) Write what are E (X|Y), var (X|Y)? b) Show that σi + σισ E (XXY) afo(-p) +2pa 102+0 var (XXY 2) Hint. (X, XY)is normal bivariate: apply a).

4.2 The Correlation Coefficient 1. Let the random variables X and Y have the joint PMF of the form x + y , x= 1,2, y = 1,2,3. p(x,y) = 21 They satisfy 11 12 Mx = 16 of = 12 of = 212 2 My = 27 Find the covariance Cov(X,Y) and the correlation coefficient p. Are X and Y independent or dependent?

4.2 The Correlation Coefficient 1. Let the random variables X and Y have the joint PMF of the form x + y , x= 1,2, y = 1,2,3. p(x,y) = 21 They satisfy 11 12 Mx = 16 of = 12 of = 212 2 My = 27 Find the covariance Cov(X,Y) and the correlation coefficient p. Are X and Y independent or dependent?

3. Suppose that (M, ρ) is a compact metric space and f : (M, p)-+ (M,p) is a function such that (Vz, y E M) ρ (z, y) ρ (f (x), f (y)). a. Let x E (M, ρ) and consider the sequence of points {f(n) (X)}n 1 . (Remember: fn) denotes the composition of f with itself, n times, so for each n, f+() rn, k E N) such that ρ (f(m) (x) ,f(n +k) (r)) < ε ....

3. Suppose that (M, ρ) is a compact metric space and f : (M, p)-+ (M,p) is a function such that (Vz, y E M) ρ (z, y) ρ (f (x), f (y)). a. Let x E (M, ρ) and consider the sequence of points {f(n) (X)}n 1 . (Remember: fn) denotes the composition of f with itself, n times, so for each n, f+() rn, k E N) such that ρ (f(m) (x) ,f(n +k) (r)) < ε ....

56. Let S = N × N and let ρ be a binary relation on şdefined by (x,y)ρ(z, w)艹x + y-z + w. Show that p is an equivalence relation on S and describe the resulting equivalence classes.

56. Let S = N × N and let ρ be a binary relation on şdefined by (x,y)ρ(z, w)艹x + y-z + w. Show that p is an equivalence relation on S and describe the resulting equivalence classes.

4.7 Let r'n be the Pearson correlation coefficient from a sample size of n. It is known that rn is asymptotically distributed as N (p, (1 – p2)2/n), where p is the population correlation coefficient. Show that Fisher's Z-transformation Z = { In((1 + ra)/(1 – in)) is actually a variance-stabilizing transformation.

4.7 Let r'n be the Pearson correlation coefficient from a sample size of n. It is known that rn is asymptotically distributed as N (p, (1 – p2)2/n), where p is the population correlation coefficient. Show that Fisher's Z-transformation Z = { In((1 + ra)/(1 – in)) is actually a variance-stabilizing transformation.

(a) Find the correlation coefficient ρX,Y .

(b) Are X and Y independent? Explain why.

Let (X, Y) have joint pdf given by 0 y 00, ey f(x, y) 0, o.w., (a) Find the correlation coefficient px,y. (20 pts) (b) Are X and Y independent? Explain why. (10 pts)

(a) Find the correlation coefficient ρX,Y .

(b) Are X and Y independent? Explain why.

Let (X, Y) have joint pdf given by 0 y 00, ey f(x, y) 0, o.w., (a) Find the correlation coefficient px,y. (20 pts) (b) Are X and Y independent? Explain why. (10 pts)

5. Let X1,X2, . , Xn be a random sample from a distribution with finite variance. Show that (i) COV(Xi-X, X )-0 f ) ρ (Xi-XX,-X)--n-1, 1 # J, 1,,-1, , n. OV&.for any two random variables X and Y) or each 1, and (11 CoV(X,Y) var(x)var(y) (Recall that p vararo

5. Let X1,X2, . , Xn be a random sample from a distribution with finite variance. Show that (i) COV(Xi-X, X )-0 f ) ρ (Xi-XX,-X)--n-1, 1 # J,...

5. Let X1,X2, . , Xn be a random sample from a distribution with finite variance. Show that (i) COV(Xi-X, X )-0 f ) ρ (Xi-XX,-X)--n-1, 1 # J, 1,,-1, , n. OV&.for any two random variables X and Y) or each 1, and (11 CoV(X,Y) var(x)var(y) (Recall that p vararo

5. Let X1,X2, . , Xn be a random sample from a distribution with finite variance. Show that (i) COV(Xi-X, X )-0 f ) ρ (Xi-XX,-X)--n-1, 1 # J,...

Most questions answered within 3 hours.

-

Write a program to solve the Josephus problem, with the following

modification:

Sample Input:

./a.out n...

asked 1 hour ago -

At the start of a CD it is spinning at a rate of 525 rpm

(revolutions...

asked 2 hours ago -

4. Without doing any calculations, predict whether the observed

∆T would increase, decrease or remain the...

asked 3 hours ago -

Based on the range, which of the following sets of scores has

the greatest variability? 3,...

asked 4 hours ago -

Ripples in a pond travel at a velocity of 3 m/s with one peak

passing a...

asked 4 hours ago -

A man stands on the roof of a building of height 13.0 mm and

throws a...

asked 4 hours ago -

The extent to which assets are financed by borrowed funds and

other liabilities is indicated by:...

asked 5 hours ago -

Explain in detail

Germany is the fifth largest economy

explain what goods and services Germany specializes...

asked 5 hours ago -

The density of platinum is 21.45 g/mL. If a cube of platinum

with a mass of...

asked 5 hours ago -

Accounts Receivable

Sales

A/R Posting

Extended Sales Invoice

Packing Slip

Compare invoice to packing slip 2...

asked 5 hours ago -

Michaella, age 23, is a full-time law student and is claimed by

her parents as a...

asked 5 hours ago -

Why are polymers not typically casted into products?

asked 6 hours ago