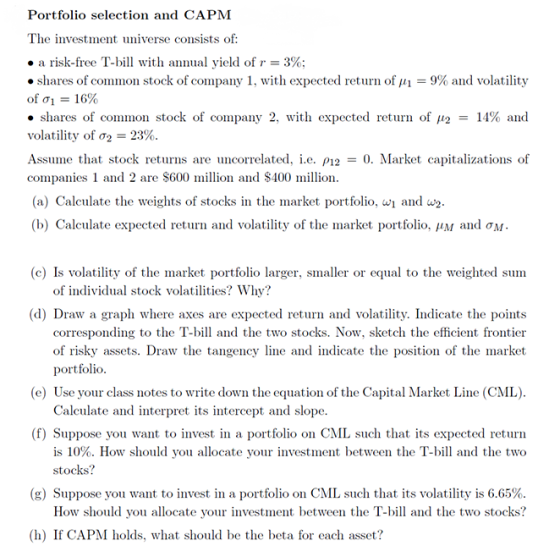

The investment universe consists of: a risk-free T-bill with annual yield of r = 3%; shares of common stock of company 1, with expected return of 1 = 9% and volatility of 1 = 16% shares of common stock of company 2, with expected return of 2 = 14% and volatility of 2 = 23%.

Homework Answers

Given,

Risk free return (Rf) = 3%

Expected Return of Security 1 (ERx) = 9%

Standard Deviation of Security 1 (SDx) = 16%

Expected Return of Security 2 (ERy) = 11%

Standard Deviation of Security 2 (SDy) = 23%

Coefficient of correlation = 0 (Hence, Covariance = 0)

(1). Weights of the securities

Weight of Security 1 (Wx) = [ (SDy)^2 - (Covariance)x,y ]/[ (SDx)^2 + (SDy)^2 – 2(Covariance x,y)]

=[ (0.23)^2 - 0 ]/[ (0.16)^2 + (0.23)^2 - 2(0)]

= ( 0.0529 – 0) /( 0.0256 + 0.0529 – 0)

= 0.0529/0.0785

= 0.6739

Weight of Security 2 (Wy) = 1 – 0.6739

= 0.3261

(2). Expected Return of Market Portfolio

(Rm) = (ERx)(Wx) + (ERy)(Wy)

= 9%(0.6739) + 14%(0.3261)

= 6.0651% + 4.5654%

= 10.6305%

Portfolio Risk = (Wx)^2*(SDx)^2 + (Wy)^2*(SDy)^2 + 2(Wx)(SDx)(Wy)(SDy)(Coefficient of correlation)

= (0.6739)^2*16^2 + (0.3261)^2*23^2 – 2*0.6739*16*0.3261*23*0

= 116.26 +56.25

= 172.51

Volatility of Market Portfolio = Square root of 172.51 = 13.1343%

(3). Weighted Average of individual stock volatilities = 16%(0.6739) + 23%(0.3261)

= 10.7824% + 7.5003%

= 18.2827%

Hence, Volatility of market portfolio (13.1343%) is smaller than weighted average of individual stock volaitilities.

Add Answer to:

The investment universe consists of: a risk-free T-bill with

annual yield of r = 3%; shares...

The investment universe consists of: a risk-free T-bill with annual yield of r = 3%; shares...

The investment universe consists of: a risk-free T-bill with

annual yield of r = 3%; shares of common stock of company 1, with

expected return of 1 = 9% and volatility of 1 = 16% shares of

common stock of company 2, with expected return of 2 = 14% and

volatility of 2 = 23%.

Portfolio selection and CAPM The investment universe consists of: . a risk-free T-bill with annual yield of r = 3%; . shares of common stock...

The investment universe consists of: a risk-free T-bill with

annual yield of r = 3%; shares of common stock of company 1, with

expected return of 1 = 9% and volatility of 1 = 16% shares of

common stock of company 2, with expected return of 2 = 14% and

volatility of 2 = 23%.

Portfolio selection and CAPM The investment universe consists of: . a risk-free T-bill with annual yield of r = 3%; . shares of common stock...

The risk-free rate is 0%. The market portfolio has an expected return of 20% and a volatility of 20%. You have $100 to invest. You decide to build a portfolio P which invests in both the risk-free investment and the market portfolio.

The risk-free rate is 0%. The market portfolio has an expected return of 20% and a volatility of 20%. You have $100 to invest. You decide to build a portfolio P which invests in both the risk-free investment and the market portfolio.a. How much should you invest in the market portfolio and the risk-free investment if you want portfolio P to have an expected return of 40%?b. How much should you invest in the market portfolio and the risk-free investment...

Booher Book Stores has a beta of 1.2. The yield on a 3-month T-bill is 4% and the yield on a 10-year T-bond is 6%. The m...

Booher Book Stores has a beta of 1.2. The yield on a 3-month T-bill is 4% and the yield on a 10-year T-bond is 6%. The market risk premium is 5.5%, and the return on an average stock in the market last year was 15%. What is the estimated cost of common equity using the CAPM?

(a) Suppose that the CAPM holds. Consider stocks A, B, C and D plotted in the graph below together with portfolios X, T (the tangency or market portfolio), Z, and the risk-free asset S. No explanation...

(a) Suppose that the CAPM holds. Consider stocks A, B, C and D

plotted in the graph below together with portfolios X, T (the

tangency or market portfolio), Z, and the risk-free asset S. No

explanation necessary.

(i) If you could invest in the risk-free asset S and only one of

the stocks A, B, C or D, which stock would you choose?

(ii) Which of the stocks, A, B, C, or D, has the highest

beta?

(iii) Which of...

(a) Suppose that the CAPM holds. Consider stocks A, B, C and D

plotted in the graph below together with portfolios X, T (the

tangency or market portfolio), Z, and the risk-free asset S. No

explanation necessary.

(i) If you could invest in the risk-free asset S and only one of

the stocks A, B, C or D, which stock would you choose?

(ii) Which of the stocks, A, B, C, or D, has the highest

beta?

(iii) Which of...

CAPM data: Market portfolio: Risk-free asset: Om = 0.2 E[RM]=18%, R, = 6% T-bills are also...

CAPM data: Market portfolio: Risk-free asset: Om = 0.2 E[RM]=18%, R, = 6% T-bills are also available. They are considered riskless and have a corresponding rate of return. You have $20,000 to invest. a) What are Br-Bills, and 07-Bills? (1 mark) b) Consider Portfolio X comprised of T-Bills and a $25,000 investment in the market portfolio i) Find 0,- (1 mark) ii) Solve for Br. (1 marks) c) Determine the weights of T-Bills and the market portfolio that combined would...

CAPM data: Market portfolio: Risk-free asset: Om = 0.2 E[RM]=18%, R, = 6% T-bills are also available. They are considered riskless and have a corresponding rate of return. You have $20,000 to invest. a) What are Br-Bills, and 07-Bills? (1 mark) b) Consider Portfolio X comprised of T-Bills and a $25,000 investment in the market portfolio i) Find 0,- (1 mark) ii) Solve for Br. (1 marks) c) Determine the weights of T-Bills and the market portfolio that combined would...

1. The universe of available securities includes two risky stock funds, A and B and T-bills....

1. The universe of available securities includes two risky stock funds, A and B and T-bills. The data for the universe are as follows: Expected Return Standard Deviation 109 20 Tbilis The correlation coefficient between funds A and B is -0.2. a. Find the optimal risky portfolio, P. and its expected return and standard deviation b. Find the slope of the CAL supported by T-bills and portfolio P. c. How much will an investor with 4-5 invest in funds A...

1. The universe of available securities includes two risky stock funds, A and B and T-bills. The data for the universe are as follows: Expected Return Standard Deviation 109 20 Tbilis The correlation coefficient between funds A and B is -0.2. a. Find the optimal risky portfolio, P. and its expected return and standard deviation b. Find the slope of the CAL supported by T-bills and portfolio P. c. How much will an investor with 4-5 invest in funds A...

2. Company A's stock has a beta of BA 1.5, and Company B's stock has a beta of βΒ-2.5. Expected r...

2. Company A's stock has a beta of BA 1.5, and Company B's stock has a beta of βΒ-2.5. Expected returns on this two stocks are E [rA]-9.5 and E rB 14.5. Assume CAPM holds. At age 30, you decide to allocate ALL your financial wealth of $100k between stock A and stock B, with portfolio weights wA + wB1. You would like this portfolio to be risky such that Bp- 3 (a) Solve for wA and wB- (b) State...

2. Company A's stock has a beta of BA 1.5, and Company B's stock has a beta of βΒ-2.5. Expected returns on this two stocks are E [rA]-9.5 and E rB 14.5. Assume CAPM holds. At age 30, you decide to allocate ALL your financial wealth of $100k between stock A and stock B, with portfolio weights wA + wB1. You would like this portfolio to be risky such that Bp- 3 (a) Solve for wA and wB- (b) State...

1. The universe of available securities includes two risky stock funds, A and B, and T-blls....

1. The universe of available securities includes two risky stock funds, A and B, and T-blls. The data for the universe are as follows Expected Return Standard Deviation A 10% 20% В 30 60 T-bills The correlation coefficient between funds A and B is -0.2. a. Find the optimal risky portfolio, P, and its expected return and standard deviation. b. Find the slope of the CAL supported by T-bills and portfolio P c. How much will an investor with A...

1. The universe of available securities includes two risky stock funds, A and B, and T-blls. The data for the universe are as follows Expected Return Standard Deviation A 10% 20% В 30 60 T-bills The correlation coefficient between funds A and B is -0.2. a. Find the optimal risky portfolio, P, and its expected return and standard deviation. b. Find the slope of the CAL supported by T-bills and portfolio P c. How much will an investor with A...

2. 3: Risk and Rates of Return: Risk in Portfolio Context Risk and Rates of Return:...

2. 3: Risk and Rates of Return: Risk in Portfolio Context Risk

and Rates of Return: Risk in Portfolio Context The capital asset

pricing model (CAPM) explains how risk should be considered when

stocks and other assets are held . The CAPM states that any stock's

required rate of return is the risk-free rate of return plus a risk

premium that reflects only the risk remaining diversification. Most

individuals hold stocks in portfolios. The risk of a stock held in...

2. 3: Risk and Rates of Return: Risk in Portfolio Context Risk

and Rates of Return: Risk in Portfolio Context The capital asset

pricing model (CAPM) explains how risk should be considered when

stocks and other assets are held . The CAPM states that any stock's

required rate of return is the risk-free rate of return plus a risk

premium that reflects only the risk remaining diversification. Most

individuals hold stocks in portfolios. The risk of a stock held in...

a. Compute the expected rate of return for Intel common stock, which has a 1.4 beta. The risk-free rate is 3 percent...

a. Compute the expected rate of return for Intel common stock,

which has a 1.4 beta. The risk-free rate is 3

percent and the market portfolio (composed of New York Stock

Exchange stocks) has an expected return of 12 percent.

b. Why is the rate you computed the expected rate?

P8-13 (similar to) Question Help (Expected rate of return using CAPM) a. Compute the expected rate of return for Intel common stock, which has a 1.4 beta. The risk-free rate...

a. Compute the expected rate of return for Intel common stock,

which has a 1.4 beta. The risk-free rate is 3

percent and the market portfolio (composed of New York Stock

Exchange stocks) has an expected return of 12 percent.

b. Why is the rate you computed the expected rate?

P8-13 (similar to) Question Help (Expected rate of return using CAPM) a. Compute the expected rate of return for Intel common stock, which has a 1.4 beta. The risk-free rate...

The investment universe consists of: a risk-free T-bill with

annual yield of r = 3%; shares of common stock of company 1, with

expected return of 1 = 9% and volatility of 1 = 16% shares of

common stock of company 2, with expected return of 2 = 14% and

volatility of 2 = 23%.

Portfolio selection and CAPM The investment universe consists of: . a risk-free T-bill with annual yield of r = 3%; . shares of common stock...

The investment universe consists of: a risk-free T-bill with

annual yield of r = 3%; shares of common stock of company 1, with

expected return of 1 = 9% and volatility of 1 = 16% shares of

common stock of company 2, with expected return of 2 = 14% and

volatility of 2 = 23%.

Portfolio selection and CAPM The investment universe consists of: . a risk-free T-bill with annual yield of r = 3%; . shares of common stock...

(a) Suppose that the CAPM holds. Consider stocks A, B, C and D

plotted in the graph below together with portfolios X, T (the

tangency or market portfolio), Z, and the risk-free asset S. No

explanation necessary.

(i) If you could invest in the risk-free asset S and only one of

the stocks A, B, C or D, which stock would you choose?

(ii) Which of the stocks, A, B, C, or D, has the highest

beta?

(iii) Which of...

(a) Suppose that the CAPM holds. Consider stocks A, B, C and D

plotted in the graph below together with portfolios X, T (the

tangency or market portfolio), Z, and the risk-free asset S. No

explanation necessary.

(i) If you could invest in the risk-free asset S and only one of

the stocks A, B, C or D, which stock would you choose?

(ii) Which of the stocks, A, B, C, or D, has the highest

beta?

(iii) Which of...

CAPM data: Market portfolio: Risk-free asset: Om = 0.2 E[RM]=18%, R, = 6% T-bills are also available. They are considered riskless and have a corresponding rate of return. You have $20,000 to invest. a) What are Br-Bills, and 07-Bills? (1 mark) b) Consider Portfolio X comprised of T-Bills and a $25,000 investment in the market portfolio i) Find 0,- (1 mark) ii) Solve for Br. (1 marks) c) Determine the weights of T-Bills and the market portfolio that combined would...

CAPM data: Market portfolio: Risk-free asset: Om = 0.2 E[RM]=18%, R, = 6% T-bills are also available. They are considered riskless and have a corresponding rate of return. You have $20,000 to invest. a) What are Br-Bills, and 07-Bills? (1 mark) b) Consider Portfolio X comprised of T-Bills and a $25,000 investment in the market portfolio i) Find 0,- (1 mark) ii) Solve for Br. (1 marks) c) Determine the weights of T-Bills and the market portfolio that combined would...

1. The universe of available securities includes two risky stock funds, A and B and T-bills. The data for the universe are as follows: Expected Return Standard Deviation 109 20 Tbilis The correlation coefficient between funds A and B is -0.2. a. Find the optimal risky portfolio, P. and its expected return and standard deviation b. Find the slope of the CAL supported by T-bills and portfolio P. c. How much will an investor with 4-5 invest in funds A...

1. The universe of available securities includes two risky stock funds, A and B and T-bills. The data for the universe are as follows: Expected Return Standard Deviation 109 20 Tbilis The correlation coefficient between funds A and B is -0.2. a. Find the optimal risky portfolio, P. and its expected return and standard deviation b. Find the slope of the CAL supported by T-bills and portfolio P. c. How much will an investor with 4-5 invest in funds A...

2. Company A's stock has a beta of BA 1.5, and Company B's stock has a beta of βΒ-2.5. Expected returns on this two stocks are E [rA]-9.5 and E rB 14.5. Assume CAPM holds. At age 30, you decide to allocate ALL your financial wealth of $100k between stock A and stock B, with portfolio weights wA + wB1. You would like this portfolio to be risky such that Bp- 3 (a) Solve for wA and wB- (b) State...

2. Company A's stock has a beta of BA 1.5, and Company B's stock has a beta of βΒ-2.5. Expected returns on this two stocks are E [rA]-9.5 and E rB 14.5. Assume CAPM holds. At age 30, you decide to allocate ALL your financial wealth of $100k between stock A and stock B, with portfolio weights wA + wB1. You would like this portfolio to be risky such that Bp- 3 (a) Solve for wA and wB- (b) State...

1. The universe of available securities includes two risky stock funds, A and B, and T-blls. The data for the universe are as follows Expected Return Standard Deviation A 10% 20% В 30 60 T-bills The correlation coefficient between funds A and B is -0.2. a. Find the optimal risky portfolio, P, and its expected return and standard deviation. b. Find the slope of the CAL supported by T-bills and portfolio P c. How much will an investor with A...

1. The universe of available securities includes two risky stock funds, A and B, and T-blls. The data for the universe are as follows Expected Return Standard Deviation A 10% 20% В 30 60 T-bills The correlation coefficient between funds A and B is -0.2. a. Find the optimal risky portfolio, P, and its expected return and standard deviation. b. Find the slope of the CAL supported by T-bills and portfolio P c. How much will an investor with A...

2. 3: Risk and Rates of Return: Risk in Portfolio Context Risk

and Rates of Return: Risk in Portfolio Context The capital asset

pricing model (CAPM) explains how risk should be considered when

stocks and other assets are held . The CAPM states that any stock's

required rate of return is the risk-free rate of return plus a risk

premium that reflects only the risk remaining diversification. Most

individuals hold stocks in portfolios. The risk of a stock held in...

2. 3: Risk and Rates of Return: Risk in Portfolio Context Risk

and Rates of Return: Risk in Portfolio Context The capital asset

pricing model (CAPM) explains how risk should be considered when

stocks and other assets are held . The CAPM states that any stock's

required rate of return is the risk-free rate of return plus a risk

premium that reflects only the risk remaining diversification. Most

individuals hold stocks in portfolios. The risk of a stock held in...

a. Compute the expected rate of return for Intel common stock,

which has a 1.4 beta. The risk-free rate is 3

percent and the market portfolio (composed of New York Stock

Exchange stocks) has an expected return of 12 percent.

b. Why is the rate you computed the expected rate?

P8-13 (similar to) Question Help (Expected rate of return using CAPM) a. Compute the expected rate of return for Intel common stock, which has a 1.4 beta. The risk-free rate...

a. Compute the expected rate of return for Intel common stock,

which has a 1.4 beta. The risk-free rate is 3

percent and the market portfolio (composed of New York Stock

Exchange stocks) has an expected return of 12 percent.

b. Why is the rate you computed the expected rate?

P8-13 (similar to) Question Help (Expected rate of return using CAPM) a. Compute the expected rate of return for Intel common stock, which has a 1.4 beta. The risk-free rate...

Most questions answered within 3 hours.

-

How many liters of 0.669 M KOH will be needed to raise the pH of

0.339...

asked 1 hour ago -

A liquid of density 1270 kg/m 3 flows steadily through a pipe of

varying diameter and...

asked 1 hour ago -

Questions: What should the American executive do?

'A visiting American executive finds that a foreign subsidiary...

asked 1 hour ago -

Activity based costing was introduced as an alternative to

absorption costing.

1. Discuss using illustration the...

asked 1 hour ago -

1. You own shares of Crane DVD Company and are interested in

selling them. With so...

asked 1 hour ago -

How many grams of He are necessary to fill a balloon having a

volume of 4.5E3...

asked 1 hour ago -

The 2 patients, still in the hospital, were interviewed by a

MoH epidemiologist. The interviews revealed...

asked 1 hour ago -

An uncharged capacitor and a resistor are connected in series to

a source of emf. If...

asked 2 hours ago -

If assets are $540,000 and liabilities are $236,000 what is the

amount of owner’s equity?

asked 2 hours ago -

MATH 3421 Maple Assignment 1 Due February 13, 2019 Maple is a

Computer Algebra System that...

asked 2 hours ago -

CODING IN JAVA

Dates are printed in several common formats. Two of the more

common formats...

asked 2 hours ago -

A hydrometer is a device used to measure the density of a

liquid. It is a...

asked 2 hours ago