IF THIS IS NOT THE PAPERWORK YOU NEED LET ME KNOW WHAT YOU NEED!!!!

Homework Answers

| Nature of Material Mistatement |

| Revenue

that does not belong to the company but deliberately added to the

revenue section is called fictitious revenues. Employees are inspired to increase the sales because they want to meet their targets of sales which might lead to their promotions. These sales can either be made to actual customers of the company or fake customers that only exist in the records for the employees to conduct fraud. |

| Due to

the excessive figures in the sales, accountants may manipulate the figures and record the revenue in the earlier years of the services against the criteria for their personal financial interest. This will also inflate the debtors figure and overall misrepresentation to the financial statement. |

| Risk of material misstatement |

| The risk

of material misstatement is the risk that the financial statements

of an organization have been misstated to a material degree. This

risk is assessed by auditors at the following two levels: At the assertion level. This is further subdivided into inherent risk and control risk. Inherent risk is the susceptibility of an assertion to misstatement because of error or fraud, before considering controls. Control risk is the risk of misstatement that will not be prevented or detected by a reporting entity's internal controls. At the financial statement level. Relates to the financial statements as a whole. This risk is more likely when there is a possibility of fraud. When the risk of material misstatement is high, the level of detection risk is lowered (increases the amount of evidence obtained from substantive procedures). Doing so reduces the overall audit risk |

| Audit procedure to be performed |

| Create

awareness of hazards and risk. Identify who may be at risk (e.g., employees, cleaners, visitors, contractors, the public, etc.). Determine whether a control program is required for a particular hazard. Determine if existing control measures are adequate or if more should be done. Prevent risk , especially when done at the design or planning stage. Prioritize control measures. Meet legal requirements where applicable. |

Add Answer to:

IF THIS IS NOT THE PAPERWORK YOU NEED LET ME KNOW WHAT YOU

NEED!!!!

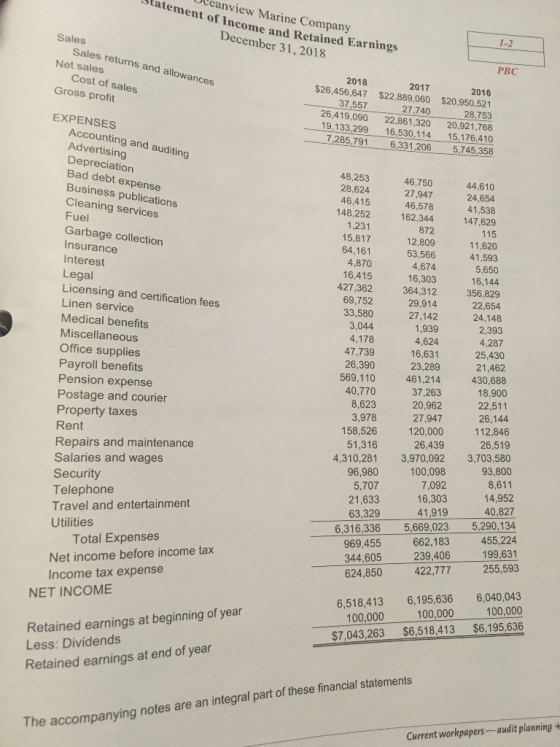

Uleanview Marine...

The question reads: The Engagement Letter for Oceanview Marine Company is missing 2 pieces. Make the...

The question reads: The Engagement Letter for Oceanview Marine Company is missing 2 pieces. Make the needed changes/additions directly on the Engagement Letter. LILTS BERGER & ASSOCIATES 4-1 Certified Public Accountants CW 11/23/2018 Ocean City, Florida 33140 October 30, 2018 Mr. Donald Phillips, President 36 Clearwater Lake Road Ocean City, Florida 33140 Dear Mr. Phillips: You have requested that we audit the financial statements of Oceanview Marine Company, which comprise the balance sheet for December 31, 2018, and the related...

Describe examples of characteristics of transactions and balances that might cause an auditor to determine that...

Describe examples of characteristics of transactions and balances that might cause an auditor to determine that a risk of material misstatement is a significant risk. Select the THREE characteristics of transactions and balances that might cause an auditor to determine that a risk of material misstatement is a significant risk and then select each characteristic's matching description. Characteristics Acceptable Audit Risk Fraud Risk Matters Requiring Significant judgement Non Routine Transactions Routine Transactions Characteristic Description Descriptions 1. This generally involves concealment...

The following audit procedures are included in the audit program of Holland Equipment, Inc. 1. Use...

The following audit procedures are included in the audit program of Holland Equipment, Inc. 1. Use audit software to examine journal entries in the sales, cash receipts, purchases, cash disbursements, payroll, and general journals for any amounts exceeding $1 million and for any entries with unusual account codings. Review related supporting documentation for reasonableness. 2. Examine the estimate for the Allowance for Doubtful Accounts recorded in the prior-year audited financial statements. Obtain information about receivable writeoffs recorded during the current...

Which of the six risks should be considered a significant risk? Explain why they represent a...

Which of the six risks should be considered a significant risk? Explain why they represent a significant risk. For each risk that you identified as a significant risk, describe how you might address the risk to give it special audit consideration. For example, a valuation risk might be addressed by engaging a valuation specialist. Begin by determining which of the six risks should be considered a significant risk. Then, for each risk that has been identified as a significant risk,...

Auditors have a responsibility to remain alert to audit evidence that contradicts other audit evidence obtained. The app...

REMOVEDAuditors have a responsibility to remain alert to audit evidence that contradicts other audit evidence obtained. The application of professional skepticism is essential to the critical assessment and questioning of contradictory audit evidence. When the auditor obtains information during the course of the audit that contradicts information obtained from another source, the auditor has a responsibility to resolve the matter and consider its impact on the sufficiency and appropriateness of audit evidence obtained and the effect, if any, on other...

a. Do you perceive &ny pluu Johnson? Explain. b. Do you perceive any problems with Johnson's...

a. Do you perceive &ny pluu Johnson? Explain. b. Do you perceive any problems with Johnson's reasoning or the appropriatenes dence used in that reasoning? 159 Chapter 4 Management Fraud and Audit Risk 4.53 Risk of Misstatement in Various Accounts. An auditor must identify the relevant asser- tions about cach significant financial statement account and disclosure and the gather evi- dence to conclude about whether a material misstatement exists for each assertion. The nature of each financial statement account and...

a. Do you perceive &ny pluu Johnson? Explain. b. Do you perceive any problems with Johnson's reasoning or the appropriatenes dence used in that reasoning? 159 Chapter 4 Management Fraud and Audit Risk 4.53 Risk of Misstatement in Various Accounts. An auditor must identify the relevant asser- tions about cach significant financial statement account and disclosure and the gather evi- dence to conclude about whether a material misstatement exists for each assertion. The nature of each financial statement account and...

The following audit procedures are included in the audit program because of heightened risks of material...

The following audit procedures are included in the audit program because of heightened risks of material misstatements due to fraud. Use audit software to search purchase transactions to identify any with nonstandard vendor numbers or with vendor names reflecting related parties. Search sales databases for missing bill of lading numbers. Use audit software to search for journal entries posted to the sales revenue account from a nonstandard source (other than the daily sales journal). Use audit software to search cash...

For the audit of Storey Corp the following audit procedures are included in the audit program...

For the audit of Storey Corp the following audit procedures are included in the audit program because of heightened risks of material misstatements due to fraud. 1. 2. 3. 4. 5. Use audit software to search cash disbursement master files for missing check numbers. Search the accounts receivable master file for account balances with missing or unusual customer numbers (e.g., "99999"). Use audit software to create a list of all credits to the repair and maintenance expense account for follow-up...

For the audit of Storey Corp the following audit procedures are included in the audit program because of heightened risks of material misstatements due to fraud. 1. 2. 3. 4. 5. Use audit software to search cash disbursement master files for missing check numbers. Search the accounts receivable master file for account balances with missing or unusual customer numbers (e.g., "99999"). Use audit software to create a list of all credits to the repair and maintenance expense account for follow-up...

14-56 1 During the course of the audit of Nature Sporting Goods, the auditor discovered the...

14-56 1 During the course of the audit of Nature Sporting Goods, the auditor discovered the following: . The accounts receivable confirmation work revealed one pricing misstatement. The book value of $12,955.68 should be $11,984.00. The total misstatement based on this differ- ence is $14,465, which includes a $972 known misstatement and an unknown projected misstatement of $13,493. Nature Sporting Goods had understated the accrued vacation pay by $13,000. A review of the prior-year documentation indicates the following uncorrected misstatements:...

14-56 1 During the course of the audit of Nature Sporting Goods, the auditor discovered the following: . The accounts receivable confirmation work revealed one pricing misstatement. The book value of $12,955.68 should be $11,984.00. The total misstatement based on this differ- ence is $14,465, which includes a $972 known misstatement and an unknown projected misstatement of $13,493. Nature Sporting Goods had understated the accrued vacation pay by $13,000. A review of the prior-year documentation indicates the following uncorrected misstatements:...

Review Garcia and Foster’s calculations of materiality thresholds for the 20X2 Audit . Determine if the...

Review Garcia and Foster’s calculations of materiality

thresholds for the 20X2 Audit . Determine if the auditors correctly

applied the materiality concept in their risk assessment

procedures. Describe any problems you find and provide suggestions

for improvement. This question relates to step 2 of the Garcia and

Foster Audit Plan.

Step 2: Requires the audit team to obtain and document its

understanding of the client’s environment including internal

controls. This understanding allows auditors to identify

significant risks in the audit...

Review Garcia and Foster’s calculations of materiality

thresholds for the 20X2 Audit . Determine if the auditors correctly

applied the materiality concept in their risk assessment

procedures. Describe any problems you find and provide suggestions

for improvement. This question relates to step 2 of the Garcia and

Foster Audit Plan.

Step 2: Requires the audit team to obtain and document its

understanding of the client’s environment including internal

controls. This understanding allows auditors to identify

significant risks in the audit...

a. Do you perceive &ny pluu Johnson? Explain. b. Do you perceive any problems with Johnson's reasoning or the appropriatenes dence used in that reasoning? 159 Chapter 4 Management Fraud and Audit Risk 4.53 Risk of Misstatement in Various Accounts. An auditor must identify the relevant asser- tions about cach significant financial statement account and disclosure and the gather evi- dence to conclude about whether a material misstatement exists for each assertion. The nature of each financial statement account and...

a. Do you perceive &ny pluu Johnson? Explain. b. Do you perceive any problems with Johnson's reasoning or the appropriatenes dence used in that reasoning? 159 Chapter 4 Management Fraud and Audit Risk 4.53 Risk of Misstatement in Various Accounts. An auditor must identify the relevant asser- tions about cach significant financial statement account and disclosure and the gather evi- dence to conclude about whether a material misstatement exists for each assertion. The nature of each financial statement account and...

For the audit of Storey Corp the following audit procedures are included in the audit program because of heightened risks of material misstatements due to fraud. 1. 2. 3. 4. 5. Use audit software to search cash disbursement master files for missing check numbers. Search the accounts receivable master file for account balances with missing or unusual customer numbers (e.g., "99999"). Use audit software to create a list of all credits to the repair and maintenance expense account for follow-up...

For the audit of Storey Corp the following audit procedures are included in the audit program because of heightened risks of material misstatements due to fraud. 1. 2. 3. 4. 5. Use audit software to search cash disbursement master files for missing check numbers. Search the accounts receivable master file for account balances with missing or unusual customer numbers (e.g., "99999"). Use audit software to create a list of all credits to the repair and maintenance expense account for follow-up...

14-56 1 During the course of the audit of Nature Sporting Goods, the auditor discovered the following: . The accounts receivable confirmation work revealed one pricing misstatement. The book value of $12,955.68 should be $11,984.00. The total misstatement based on this differ- ence is $14,465, which includes a $972 known misstatement and an unknown projected misstatement of $13,493. Nature Sporting Goods had understated the accrued vacation pay by $13,000. A review of the prior-year documentation indicates the following uncorrected misstatements:...

14-56 1 During the course of the audit of Nature Sporting Goods, the auditor discovered the following: . The accounts receivable confirmation work revealed one pricing misstatement. The book value of $12,955.68 should be $11,984.00. The total misstatement based on this differ- ence is $14,465, which includes a $972 known misstatement and an unknown projected misstatement of $13,493. Nature Sporting Goods had understated the accrued vacation pay by $13,000. A review of the prior-year documentation indicates the following uncorrected misstatements:...

Review Garcia and Foster’s calculations of materiality

thresholds for the 20X2 Audit . Determine if the auditors correctly

applied the materiality concept in their risk assessment

procedures. Describe any problems you find and provide suggestions

for improvement. This question relates to step 2 of the Garcia and

Foster Audit Plan.

Step 2: Requires the audit team to obtain and document its

understanding of the client’s environment including internal

controls. This understanding allows auditors to identify

significant risks in the audit...

Review Garcia and Foster’s calculations of materiality

thresholds for the 20X2 Audit . Determine if the auditors correctly

applied the materiality concept in their risk assessment

procedures. Describe any problems you find and provide suggestions

for improvement. This question relates to step 2 of the Garcia and

Foster Audit Plan.

Step 2: Requires the audit team to obtain and document its

understanding of the client’s environment including internal

controls. This understanding allows auditors to identify

significant risks in the audit...

Most questions answered within 3 hours.

-

Kylie is a single mom with two dependent children,

Tanner, age 7 and Olivia, age 11....

asked 48 minutes ago -

Phosphorous + bromine = phosphorous tribromide. If 35.0 g of

bromine are reacted and 27.9 grams...

asked 2 hours ago -

Derive the long wavelength limit of the Planck energy density

distribution

asked 2 hours ago -

Calculate the pH of each of the following solutions.

0.50 M HBr

3.1×10−4 M KOH

4.2×10−5...

asked 5 hours ago -

For the year ended December 31, Depot Max’s cost of merchandise

sold was $85,600. Inventory at the...

asked 5 hours ago -

Week 10 - Professional Memo Assignment

Professional Memo Assignment

Your mission for this week, should you...

asked 5 hours ago -

Write a Python program that stores the data for each

player on the team, and it...

asked 5 hours ago -

In

the last 3 months, mike never knows when he is going to get his

allowance...

asked 6 hours ago -

Is Ca(OH)2 a Bronsted base, Lewis base, or both? Why?

asked 6 hours ago -

1A- Why don’t voters complain about U.S. tariffs on imported

sugar?

Because sugar is only a...

asked 6 hours ago -

Cash Payback Period

Primera Banco is evaluating two capital investment proposals for

a drive-up ATM kiosk,...

asked 6 hours ago -

Create a button in Swift (Xcode) that will create a charge,

create a charge using Stripe's...

asked 6 hours ago