Homework Answers

Answer is given below with working notes:

Add Answer to:

Due 2/20 before 11:00 am Exting. Debt 1. (P14-13) On June 30, Umno Inc., had outstanding...

Saved Help Save & Ext Sube On June 30, 2021, K Co. had outstanding 8%, $12,500,000...

Saved Help Save & Ext Sube On June 30, 2021, K Co. had outstanding 8%, $12,500,000 face value bonds maturing on June 30, 2026. Interest is payable semiannually every June 30 and December 31. On June 30, 2021, after amortization was recorded for the period, the unamortized bond premium was $52,000. On that date, K acquired all its outstanding bonds on the open market at 99 and retired them. At June 30, 2021, what amount should K Co. recognize as...

Saved Help Save & Ext Sube On June 30, 2021, K Co. had outstanding 8%, $12,500,000 face value bonds maturing on June 30, 2026. Interest is payable semiannually every June 30 and December 31. On June 30, 2021, after amortization was recorded for the period, the unamortized bond premium was $52,000. On that date, K acquired all its outstanding bonds on the open market at 99 and retired them. At June 30, 2021, what amount should K Co. recognize as...

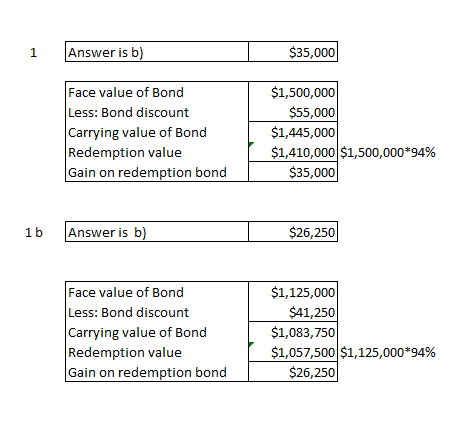

On June 30, 2021, K Co. had outstanding 9%, $19,500,000 face value bonds maturing on June...

On June 30, 2021, K Co. had outstanding 9%, $19,500,000 face value bonds maturing on June 30, 2026. Interest is payable semiannually every June 30 and December 31. On June 30, 2021, after amortization was recorded for the period, the unamortized bond premium was $59,000. On that date, K acquired all its outstanding bonds on the open market at 98 and retired them. At June 30, 2021, what amount should K Co. recognize as gain on redemption of bonds before...

On June 30, 2021, K Co. had outstanding 9%, $19,500,000 face value bonds maturing on June 30, 2026. Interest is payable semiannually every June 30 and December 31. On June 30, 2021, after amortization was recorded for the period, the unamortized bond premium was $59,000. On that date, K acquired all its outstanding bonds on the open market at 98 and retired them. At June 30, 2021, what amount should K Co. recognize as gain on redemption of bonds before...

On June 30, 2021, K Co. had outstanding 8%, $20,000,000 face value bonds maturing on June...

On June 30, 2021, K Co. had outstanding 8%, $20,000,000 face value bonds maturing on June 30, 2026. Interest is payable semiannually every June 30 and December 31. On June 30, 2021, after amortization was recorded for the period, the unamortized bond premium was $70,000. On that date, K acquired all its outstanding bonds on the open market at 98 and retired them. At June 30, 2021, what amount should K Co. recognize as gain on redemption of bonds before...

2. (P14-13) The 10% bonds payable of Nico had a net carrying amount of $1,140,000 on...

2. (P14-13) The 10% bonds payable of Nico had a net carrying amount of $1,140,000 on December 31, 2017. The bonds, which had a face value of $1,200,000, were issued at a discount to yield 12%. Amortization was recorded under the effective-interest method. Interest was paid on January 1 and July 1 of each year. The interest payment on July 1, 2018 was made as scheduled in the morning. Later that day, several years before their maturity, Nico retired the...

2. (P14-13) The 10% bonds payable of Nico had a net carrying amount of $1,140,000 on December 31, 2017. The bonds, which had a face value of $1,200,000, were issued at a discount to yield 12%. Amortization was recorded under the effective-interest method. Interest was paid on January 1 and July 1 of each year. The interest payment on July 1, 2018 was made as scheduled in the morning. Later that day, several years before their maturity, Nico retired the...

On June 30, 2018, Omara Co. had outstanding 8%, $4,000,000 face amount, 15-year bonds maturing on...

On June 30, 2018, Omara Co. had outstanding 8%, $4,000,000 face amount, 15-year bonds maturing on June 30, 2028. Interest is payable on June 30 and December 31. The unamortized balance in the bond discount account on June 30, 2018 was $180,000. On June 30, 2018, Omara acquired all of these bonds at 96 and retired them. What net carrying amount should be used in computing gain or loss on this early extinguishment of debt?

On December 31, 2018, Diaz Corp. is in financial difficulty and cannot pay a $900,000 note...

On December 31, 2018, Diaz Corp. is in financial difficulty and cannot pay a $900,000 note with $90,000 accrued interest payable to Cameron Ltd., which is now due. Cameron agrees to accept from Diaz equipment that has a fair value of $435,000, an original cost of $720,000, and accumulated depreciation of $345,000. Cameron also forgives the accrued interest, extends the maturity date to December 31, 2021, reduces the face amount of the note to $375,000, and reduces the interest rate...

CASE 1-5 Financial Statement Ratio Computation Refer to Campbell Soup Company's financial Campbell Soup statements in...

CASE 1-5 Financial Statement Ratio Computation Refer to Campbell Soup Company's financial Campbell Soup statements in Appendix A. Required: Compute the following ratios for Year 11. Liquidity ratios: Asset utilization ratios:* a. Current ratio n. Cash turnover b. Acid-test ratio 0. Accounts receivable turnover c. Days to sell inventory p. Inventory turnover d. Collection period 4. Working capital turnover Capital structure and solvency ratios: 1. Fixed assets turnover e. Total debt to total equity s. Total assets turnover f. Long-term...

CASE 1-5 Financial Statement Ratio Computation Refer to Campbell Soup Company's financial Campbell Soup statements in Appendix A. Required: Compute the following ratios for Year 11. Liquidity ratios: Asset utilization ratios:* a. Current ratio n. Cash turnover b. Acid-test ratio 0. Accounts receivable turnover c. Days to sell inventory p. Inventory turnover d. Collection period 4. Working capital turnover Capital structure and solvency ratios: 1. Fixed assets turnover e. Total debt to total equity s. Total assets turnover f. Long-term...

Saved Help Save & Ext Sube On June 30, 2021, K Co. had outstanding 8%, $12,500,000 face value bonds maturing on June 30, 2026. Interest is payable semiannually every June 30 and December 31. On June 30, 2021, after amortization was recorded for the period, the unamortized bond premium was $52,000. On that date, K acquired all its outstanding bonds on the open market at 99 and retired them. At June 30, 2021, what amount should K Co. recognize as...

Saved Help Save & Ext Sube On June 30, 2021, K Co. had outstanding 8%, $12,500,000 face value bonds maturing on June 30, 2026. Interest is payable semiannually every June 30 and December 31. On June 30, 2021, after amortization was recorded for the period, the unamortized bond premium was $52,000. On that date, K acquired all its outstanding bonds on the open market at 99 and retired them. At June 30, 2021, what amount should K Co. recognize as...

On June 30, 2021, K Co. had outstanding 9%, $19,500,000 face value bonds maturing on June 30, 2026. Interest is payable semiannually every June 30 and December 31. On June 30, 2021, after amortization was recorded for the period, the unamortized bond premium was $59,000. On that date, K acquired all its outstanding bonds on the open market at 98 and retired them. At June 30, 2021, what amount should K Co. recognize as gain on redemption of bonds before...

On June 30, 2021, K Co. had outstanding 9%, $19,500,000 face value bonds maturing on June 30, 2026. Interest is payable semiannually every June 30 and December 31. On June 30, 2021, after amortization was recorded for the period, the unamortized bond premium was $59,000. On that date, K acquired all its outstanding bonds on the open market at 98 and retired them. At June 30, 2021, what amount should K Co. recognize as gain on redemption of bonds before...

2. (P14-13) The 10% bonds payable of Nico had a net carrying amount of $1,140,000 on December 31, 2017. The bonds, which had a face value of $1,200,000, were issued at a discount to yield 12%. Amortization was recorded under the effective-interest method. Interest was paid on January 1 and July 1 of each year. The interest payment on July 1, 2018 was made as scheduled in the morning. Later that day, several years before their maturity, Nico retired the...

2. (P14-13) The 10% bonds payable of Nico had a net carrying amount of $1,140,000 on December 31, 2017. The bonds, which had a face value of $1,200,000, were issued at a discount to yield 12%. Amortization was recorded under the effective-interest method. Interest was paid on January 1 and July 1 of each year. The interest payment on July 1, 2018 was made as scheduled in the morning. Later that day, several years before their maturity, Nico retired the...

CASE 1-5 Financial Statement Ratio Computation Refer to Campbell Soup Company's financial Campbell Soup statements in Appendix A. Required: Compute the following ratios for Year 11. Liquidity ratios: Asset utilization ratios:* a. Current ratio n. Cash turnover b. Acid-test ratio 0. Accounts receivable turnover c. Days to sell inventory p. Inventory turnover d. Collection period 4. Working capital turnover Capital structure and solvency ratios: 1. Fixed assets turnover e. Total debt to total equity s. Total assets turnover f. Long-term...

CASE 1-5 Financial Statement Ratio Computation Refer to Campbell Soup Company's financial Campbell Soup statements in Appendix A. Required: Compute the following ratios for Year 11. Liquidity ratios: Asset utilization ratios:* a. Current ratio n. Cash turnover b. Acid-test ratio 0. Accounts receivable turnover c. Days to sell inventory p. Inventory turnover d. Collection period 4. Working capital turnover Capital structure and solvency ratios: 1. Fixed assets turnover e. Total debt to total equity s. Total assets turnover f. Long-term...

Most questions answered within 3 hours.

-

1.b. Fiscal policy is said to suffer from ‘crowding out’.

Explain what this means and why...

asked 2 minutes ago -

The equation for the reaction of nitrogen and oxygen to form

nitrogen oxide is written as...

asked 6 minutes ago -

A scientist reproducing some photoelectric effect experiments

shines a light on a metal electrode, but doesn't...

asked 9 minutes ago -

In a study designed to test the effectiveness of magnets for

treating back pain, 35 patients...

asked 29 minutes ago -

Here are summary statistics for randomly selected weights of

newborn girls:

nequals=193,

x overbarxequals=30.5

hg,

sequals=7.3...

asked 19 minutes ago -

Exercise #3:

Create the “MathTest” class. It will have two class variables:

1) a question and...

asked 21 minutes ago -

In epidemiology, how do you calculate the overall incidence of

cure within two groups? What formula...

asked 25 minutes ago -

A 1 liter solution contains 0.357 M ammonium chloride and 0.268

M ammonia. Addition of 0.295...

asked 26 minutes ago -

What are the advantages and disadvantages of using virtual

reality simulations in health care education?

asked 31 minutes ago -

Given input { 66, 28, 43, 29, 44, 69, 19 } and a hash function

h(x)...

asked 52 minutes ago -

A pebble with mass m is thrown straight up with an initial speed

v0 so that...

asked 56 minutes ago -

Let X be a discrete random variable that follows a

binomial distribution with n = 11...

asked 1 hour ago