Solid Box Fabrications manufactures boxes for workstations. The firm’s standard cost sheet prior to October of the current year and actual results for October are as follows:

![Required information {The following information applies to the questions displayed below.] Solid Box Fabrications manufacture](http://img.homeworklib.com/questions/123355a0-7115-11ea-87dd-736ca229df30.png?x-oss-process=image/resize,w_560)

Homework Answers

|

Master(Static) Budget |

Pro Forma Budgets |

||

| Units | 10,000 | 9,500 | 11,000 |

| Sales | 540,000 | 513,000 | 594,000 |

| Variable costs: | |||

| Direct materials | 132,300 | 125,685 | 145,530 |

| Direct labor | 77,000 | 73,150 | 84,700 |

| Manufacturing overheads | 20,000 | 19,000 | 22,000 |

| Selling and administrative | 50,000 | 47,500 | 55,000 |

| Total variable costs | 279,300 | 265,335 | 307,230 |

| Contribution margin | 260,700 | 247,665 | 286,770 |

| Fixed costs: | |||

| Manufacturing | 51,000 | 51,000 | 51,000 |

| Selling and administrative | 24,000 | 24,000 | 24,000 |

| Total fixed costs | 75,000 | 75,000 | 75,000 |

| Operating income | 185,700 | 172,665 | 211,770 |

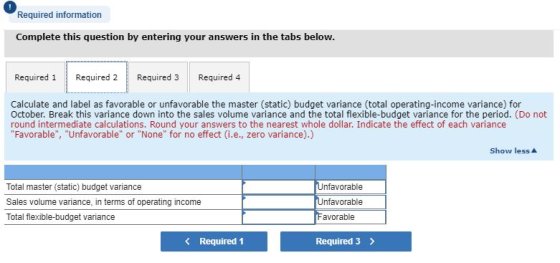

| Total master(static) budget variance | 5,660 | Unfavorable | |

| Sales

volume variance in terms of operating income |

13,035 | Unfavorable | |

| Total flexible budget variance | 7,375 | Favorable | |

| Selling price variance | 38,000 | Favorable | |

| Total variable cost flexible budget variance | 30,625 | Unfavorable | |

| Total fixed cost variance | - | Favorable | |

| Direct materials | |||

| Purchase price variance | 17,920 | Unfavorable | |

| Usage variance | 9,805 | Unfavorable | |

| Direct labor | |||

| Rate variance | 7,280 | Unfavorable | |

| Efficiency variance | 6,930 | Unfavorable | |

| Working Notes | |||

| Original Selling Price | 50.00 | ||

| Increase in Selling Price | 8% | ||

| Increase in Selling Price | 4.00 | ||

| Budgeted Selling Price for October | 54.00 | ||

| Original Purchase Price | 12.60 | ||

| Increase in Material Price | 5% | ||

| Increase in Material Price | 0.63 | ||

| Budgeted Material Price for October | 13.23 | ||

| Material per unit (in pounds) | 5.00 | ||

| Material cost per pound | 2.65 | ||

| Labor cost per hour | 14.00 | ||

| Increase in Labor cost | 10% | ||

| Increase in Labor cost | 1.40 | ||

| Budgeted Labor Cost in October | 15.40 | ||

| Labor hours per unit | 0.50 | ||

| Labor cost per unit | 7.70 | ||

| Increase in Fixed Costs | |||

| Manufacturing | Selling

and Admin. |

||

| Original Cost | 46,000 | 20,000 | |

| Increase in Insurance Costs | 5,000 | - | |

| Increase in Manager's Salary | - | 2,000 | |

| Increase in Advertisement Costs | - | 2,000 | |

| Fixed Costs in October | 51,000 | 24,000 | |

| Total master(static) budget variance | |||

| = Actual Operating Income - Static Budget Operating Income | |||

| = $ 180,040 - $ 185,700 | |||

| = - $ 5,660 | |||

| Sales volume variance | |||

| = ( Budgeted Sales Volume - Actual Sales Volume) * Budgeted Contribution | |||

| =( 10,000 - 9,500) * 26.18 | |||

| = 500 * $ 26.07 | |||

| = $ 13,035 | |||

| Total flexible budget variance | |||

| = Flexible Budget Operating Income - Actual Operating Income | |||

| = $ 172,665 - $ 180,040 | |||

| = - $ 7,375 | |||

| Selling price variance | |||

| =(Actual Selling Price - Budgeted Selling Variance) * Actual Units Sold | |||

| = ($ 58 - $ 54) * 9,500 | |||

| = $ 4 * 9,500 | |||

| = $ 38,000 | |||

| Total variable cost flexible budget variance | |||

| = Budgeted Flexible Variable Costs - Actual Variable Costs | |||

| = $ 265,335 - $ 295,960 | |||

| = - $ 30,625 | |||

| Total fixed cost variance | |||

| = Budgeted Fixed Costs - Actual Fixed Costs | |||

| = $ 75,000 - $ 75,000 | |||

| = $ 0 | |||

| Direct material purchase price variance | |||

| =( Budgeted Purchase Price - Actual Purchase Price)* Actual Quantity | |||

| =($ 2.65 - $ 3) * 51,200 | |||

| = - $ 0.35 * 51,200 | |||

| = - $ 17,920 | |||

| Direct material usage variance | |||

| =( Budgeted Quantity - Actual Quantity) * Budgeted Rates | |||

| =( 47,500 - 51,200) * $ 2.65 | |||

| = -3,700 * $ 2.65 | |||

| = - $ 9,805 | |||

| Direct labor rate variance | |||

| = (Budgeted labor rate - Actual labor rate) * Actual labor hours | |||

| =( $ 15.40 - $ 16.80) * 5,200 | |||

| = - $ 1.40 * 5,200 | |||

| = - $ 7,280 | |||

| Direct labor efficiency variance | |||

| = (Budgeted labor hours - Actual labor hours) * Budgeted labor rates | |||

| = (4,750 - 5,200) * $ 15.40 | |||

| = - 450 * $ 15.40 | |||

| = - $ 6,930 | |||

Add Answer to:

Solid Box Fabrications manufactures boxes for workstations. The

firm’s standard cost sheet prior to October of...

Exercise 4) Mighty Marketer manufactures boxes for marketing workstations. The firm's standard cost sheet prior to...

Exercise 4) Mighty Marketer manufactures boxes for marketing workstations. The firm's standard cost sheet prior to October and actual results for October 2019 are as follows: Actual Fixed Costs October 2019 9,500 $ 551.000 50.00 $ 144,000 Budget Information Standard Price & Variable Costs per Unit Units Sales $ Variable costs Direct materials 5 pounds at $2.40 per pound - $ 12.00 Direct labor 0.5 hour at $14 per hour 7.00 Manufacturing overhead 2.00 Selling and administrative 5.00 Total variable...

Exercise 4) Mighty Marketer manufactures boxes for marketing workstations. The firm's standard cost sheet prior to October and actual results for October 2019 are as follows: Actual Fixed Costs October 2019 9,500 $ 551.000 50.00 $ 144,000 Budget Information Standard Price & Variable Costs per Unit Units Sales $ Variable costs Direct materials 5 pounds at $2.40 per pound - $ 12.00 Direct labor 0.5 hour at $14 per hour 7.00 Manufacturing overhead 2.00 Selling and administrative 5.00 Total variable...

please help!! mondlel uu Exercise 4) Mighty Marketer manufactures boxes for marketing workstations. The firm's standard...

please help!!

mondlel uu Exercise 4) Mighty Marketer manufactures boxes for marketing workstations. The firm's standard cost sheet prior to October and actual results for October 2019 are as follows Budget Information Standard Price Actual & Variable Costs Fixed Results per Unit Costs October 2019 Units 9.500 105% Sales x 1.08 50.00 11.09 $ 551,000 Variable costs: 1.05 X Direct materials 5 pounds at $2.40 per pound $ 12.00 V $ 144,000 . Direct labor 2.05 0.5 hour at $14...

please help!!

mondlel uu Exercise 4) Mighty Marketer manufactures boxes for marketing workstations. The firm's standard cost sheet prior to October and actual results for October 2019 are as follows Budget Information Standard Price Actual & Variable Costs Fixed Results per Unit Costs October 2019 Units 9.500 105% Sales x 1.08 50.00 11.09 $ 551,000 Variable costs: 1.05 X Direct materials 5 pounds at $2.40 per pound $ 12.00 V $ 144,000 . Direct labor 2.05 0.5 hour at $14...

Assume that in October 2019 the Schmidt Machinery Company (Exhibit 14.1) manufactured and sold 950 units...

Assume that in October 2019 the Schmidt Machinery Company

(Exhibit 14.1) manufactured and sold 950 units for $854 each.

During this month, the company incurred $380,000 total variable

costs and $181,900 total fixed costs. The master (static) budget

data for the month are as given in Exhibit 14.1.

Required:

1. Prepare a flexible budget for the production and sale of 950

units.

2. Compute for October 2019:

a. The sales volume variance, in terms of operating income.

Indicate whether this...

Assume that in October 2019 the Schmidt Machinery Company

(Exhibit 14.1) manufactured and sold 950 units for $854 each.

During this month, the company incurred $380,000 total variable

costs and $181,900 total fixed costs. The master (static) budget

data for the month are as given in Exhibit 14.1.

Required:

1. Prepare a flexible budget for the production and sale of 950

units.

2. Compute for October 2019:

a. The sales volume variance, in terms of operating income.

Indicate whether this...

Rogen Corporation manufactures a single product. The standard cost per unit of product is shown below....

Rogen Corporation manufactures a single product. The standard

cost per unit of product is shown below.

Direct materials—1 pound plastic at $6 per pound

$ 6.00

Direct labor—1.50 hours at $12.20 per hour

18.30

Variable manufacturing overhead

9.00

Fixed manufacturing overhead

15.00

Total standard cost per unit

$48.30

The predetermined manufacturing overhead rate is $16 per direct

labor hour ($24.00 ÷ 1.50). It was computed from a master

manufacturing overhead budget based on normal production of 8,700

direct labor hours...

Rogen Corporation manufactures a single product. The standard

cost per unit of product is shown below.

Direct materials—1 pound plastic at $6 per pound

$ 6.00

Direct labor—1.50 hours at $12.20 per hour

18.30

Variable manufacturing overhead

9.00

Fixed manufacturing overhead

15.00

Total standard cost per unit

$48.30

The predetermined manufacturing overhead rate is $16 per direct

labor hour ($24.00 ÷ 1.50). It was computed from a master

manufacturing overhead budget based on normal production of 8,700

direct labor hours...

The standard cost sheet for Chambers Company, which manufactures one product, follows: $ 100 100 Direct...

The standard cost sheet for Chambers Company, which manufactures one product, follows: $ 100 100 Direct materials, 40 yards at $2.50 per yard Direct labor, 4 hours at $25 per hour Factory overhead applied at 70% of direct labor (variable costs - $50; fixed costs $20) Variable selling and administrative Fixed selling and administrative Total unit costs Standards have been computed based on a master budget activity level of 28,900 direct labor hours per month. Actual activity for the past...

The standard cost sheet for Chambers Company, which manufactures one product, follows: $ 100 100 Direct materials, 40 yards at $2.50 per yard Direct labor, 4 hours at $25 per hour Factory overhead applied at 70% of direct labor (variable costs - $50; fixed costs $20) Variable selling and administrative Fixed selling and administrative Total unit costs Standards have been computed based on a master budget activity level of 28,900 direct labor hours per month. Actual activity for the past...

Whispering Corporation manufactures a single product. The standard cost per unit of product is shown below. Direct ma...

Whispering Corporation manufactures a single product. The

standard cost per unit of product is shown below.

Direct materials—1 pound plastic at $7.00 per pound

$ 7.00

Direct labor—2.5 hours at $11.80 per hour

29.50

Variable manufacturing overhead

17.50

Fixed manufacturing overhead

17.50

Total standard cost per unit

$71.50

The predetermined manufacturing overhead rate is $14.00 per direct

labor hour ($35.00 ÷ 2.5). It was computed from a master

manufacturing overhead budget based on normal production of 13,250

direct labor hours...

Whispering Corporation manufactures a single product. The

standard cost per unit of product is shown below.

Direct materials—1 pound plastic at $7.00 per pound

$ 7.00

Direct labor—2.5 hours at $11.80 per hour

29.50

Variable manufacturing overhead

17.50

Fixed manufacturing overhead

17.50

Total standard cost per unit

$71.50

The predetermined manufacturing overhead rate is $14.00 per direct

labor hour ($35.00 ÷ 2.5). It was computed from a master

manufacturing overhead budget based on normal production of 13,250

direct labor hours...

The standard cost sheet for Chambers Company, which manufactures one product, follows: Direct materials, 40...

The standard cost sheet for Chambers Company, which manufactures

one product, follows:

Direct materials, 40 yards at $3.00 per yard

$

120

Direct labor, 5 hours at $30 per hour

150

Factory overhead applied at 70% of direct labor

(variable costs = $70; fixed costs = $35)

105

Variable selling and administrative

74

Fixed selling and administrative

50

Total unit costs

$

499

Standards have been computed based on a master budget activity

level of 29,800 direct labor-hours...

The standard cost sheet for Chambers Company, which manufactures

one product, follows:

Direct materials, 40 yards at $3.00 per yard

$

120

Direct labor, 5 hours at $30 per hour

150

Factory overhead applied at 70% of direct labor

(variable costs = $70; fixed costs = $35)

105

Variable selling and administrative

74

Fixed selling and administrative

50

Total unit costs

$

499

Standards have been computed based on a master budget activity

level of 29,800 direct labor-hours...

Comparison of Actual and Budgeted Operating Income EXHIBIT 14.1 SCHMIDT MACHINERY COMPANY Analysis of Operating Income...

Comparison of Actual and Budgeted Operating Income EXHIBIT 14.1 SCHMIDT MACHINERY COMPANY Analysis of Operating Income For October 2019 (1) (2) (3) Variances Actual Operating Income Master (Static) Budget 220U Units 780 1,000 $ 160,400U 100% $639,600 100% Sales $800,000 Variable costs 99.050F 350,950 55 450.000 56 $350,000 Contribution margin $288,650 45% 44% $ 61,350U 150.000 *** 160.650 Fixed costs 25 19 10.650U $128,000 20% $ Operating income $200,000 25% 72,000U *U denotes an unfavorable effect on operating income. *F...

Comparison of Actual and Budgeted Operating Income EXHIBIT 14.1 SCHMIDT MACHINERY COMPANY Analysis of Operating Income For October 2019 (1) (2) (3) Variances Actual Operating Income Master (Static) Budget 220U Units 780 1,000 $ 160,400U 100% $639,600 100% Sales $800,000 Variable costs 99.050F 350,950 55 450.000 56 $350,000 Contribution margin $288,650 45% 44% $ 61,350U 150.000 *** 160.650 Fixed costs 25 19 10.650U $128,000 20% $ Operating income $200,000 25% 72,000U *U denotes an unfavorable effect on operating income. *F...

Rogen Corporation manufactures a single product. The standard cost per unit of product is shown below....

Rogen Corporation manufactures a single product. The standard

cost per unit of product is shown below.

Direct materials—1 pound plastic at $6 per pound

$ 6.00

Direct labor—0.50 hours at $11.75 per hour

5.88

Variable manufacturing overhead

3.50

Fixed manufacturing overhead

1.50

Total standard cost per unit

$16.88

The predetermined manufacturing overhead rate is $10 per direct

labor hour ($5.00 ÷ 0.50). It was computed from a master

manufacturing overhead budget based on normal production of 2,950

direct labor hours...

Rogen Corporation manufactures a single product. The standard

cost per unit of product is shown below.

Direct materials—1 pound plastic at $6 per pound

$ 6.00

Direct labor—0.50 hours at $11.75 per hour

5.88

Variable manufacturing overhead

3.50

Fixed manufacturing overhead

1.50

Total standard cost per unit

$16.88

The predetermined manufacturing overhead rate is $10 per direct

labor hour ($5.00 ÷ 0.50). It was computed from a master

manufacturing overhead budget based on normal production of 2,950

direct labor hours...

Rogen Corporation manufactures a single product. The standard cost per unit of product is shown below. Direct materia...

Rogen Corporation manufactures a single product. The standard

cost per unit of product is shown below.

Direct materials—1 pound plastic at $6.00 per pound

$ 6.00

Direct labor—2.0 hours at $11.85 per hour

23.70

Variable manufacturing overhead

12.00

Fixed manufacturing overhead

12.00

Total standard cost per unit

$53.70

The predetermined manufacturing overhead rate is $12.00 per direct

labor hour ($24.00 ÷ 2.0). It was computed from a master

manufacturing overhead budget based on normal production of 11,800

direct labor hours...

Rogen Corporation manufactures a single product. The standard

cost per unit of product is shown below.

Direct materials—1 pound plastic at $6.00 per pound

$ 6.00

Direct labor—2.0 hours at $11.85 per hour

23.70

Variable manufacturing overhead

12.00

Fixed manufacturing overhead

12.00

Total standard cost per unit

$53.70

The predetermined manufacturing overhead rate is $12.00 per direct

labor hour ($24.00 ÷ 2.0). It was computed from a master

manufacturing overhead budget based on normal production of 11,800

direct labor hours...

Exercise 4) Mighty Marketer manufactures boxes for marketing workstations. The firm's standard cost sheet prior to October and actual results for October 2019 are as follows: Actual Fixed Costs October 2019 9,500 $ 551.000 50.00 $ 144,000 Budget Information Standard Price & Variable Costs per Unit Units Sales $ Variable costs Direct materials 5 pounds at $2.40 per pound - $ 12.00 Direct labor 0.5 hour at $14 per hour 7.00 Manufacturing overhead 2.00 Selling and administrative 5.00 Total variable...

Exercise 4) Mighty Marketer manufactures boxes for marketing workstations. The firm's standard cost sheet prior to October and actual results for October 2019 are as follows: Actual Fixed Costs October 2019 9,500 $ 551.000 50.00 $ 144,000 Budget Information Standard Price & Variable Costs per Unit Units Sales $ Variable costs Direct materials 5 pounds at $2.40 per pound - $ 12.00 Direct labor 0.5 hour at $14 per hour 7.00 Manufacturing overhead 2.00 Selling and administrative 5.00 Total variable...

please help!!

mondlel uu Exercise 4) Mighty Marketer manufactures boxes for marketing workstations. The firm's standard cost sheet prior to October and actual results for October 2019 are as follows Budget Information Standard Price Actual & Variable Costs Fixed Results per Unit Costs October 2019 Units 9.500 105% Sales x 1.08 50.00 11.09 $ 551,000 Variable costs: 1.05 X Direct materials 5 pounds at $2.40 per pound $ 12.00 V $ 144,000 . Direct labor 2.05 0.5 hour at $14...

please help!!

mondlel uu Exercise 4) Mighty Marketer manufactures boxes for marketing workstations. The firm's standard cost sheet prior to October and actual results for October 2019 are as follows Budget Information Standard Price Actual & Variable Costs Fixed Results per Unit Costs October 2019 Units 9.500 105% Sales x 1.08 50.00 11.09 $ 551,000 Variable costs: 1.05 X Direct materials 5 pounds at $2.40 per pound $ 12.00 V $ 144,000 . Direct labor 2.05 0.5 hour at $14...

Assume that in October 2019 the Schmidt Machinery Company

(Exhibit 14.1) manufactured and sold 950 units for $854 each.

During this month, the company incurred $380,000 total variable

costs and $181,900 total fixed costs. The master (static) budget

data for the month are as given in Exhibit 14.1.

Required:

1. Prepare a flexible budget for the production and sale of 950

units.

2. Compute for October 2019:

a. The sales volume variance, in terms of operating income.

Indicate whether this...

Assume that in October 2019 the Schmidt Machinery Company

(Exhibit 14.1) manufactured and sold 950 units for $854 each.

During this month, the company incurred $380,000 total variable

costs and $181,900 total fixed costs. The master (static) budget

data for the month are as given in Exhibit 14.1.

Required:

1. Prepare a flexible budget for the production and sale of 950

units.

2. Compute for October 2019:

a. The sales volume variance, in terms of operating income.

Indicate whether this...

Rogen Corporation manufactures a single product. The standard

cost per unit of product is shown below.

Direct materials—1 pound plastic at $6 per pound

$ 6.00

Direct labor—1.50 hours at $12.20 per hour

18.30

Variable manufacturing overhead

9.00

Fixed manufacturing overhead

15.00

Total standard cost per unit

$48.30

The predetermined manufacturing overhead rate is $16 per direct

labor hour ($24.00 ÷ 1.50). It was computed from a master

manufacturing overhead budget based on normal production of 8,700

direct labor hours...

Rogen Corporation manufactures a single product. The standard

cost per unit of product is shown below.

Direct materials—1 pound plastic at $6 per pound

$ 6.00

Direct labor—1.50 hours at $12.20 per hour

18.30

Variable manufacturing overhead

9.00

Fixed manufacturing overhead

15.00

Total standard cost per unit

$48.30

The predetermined manufacturing overhead rate is $16 per direct

labor hour ($24.00 ÷ 1.50). It was computed from a master

manufacturing overhead budget based on normal production of 8,700

direct labor hours...

The standard cost sheet for Chambers Company, which manufactures one product, follows: $ 100 100 Direct materials, 40 yards at $2.50 per yard Direct labor, 4 hours at $25 per hour Factory overhead applied at 70% of direct labor (variable costs - $50; fixed costs $20) Variable selling and administrative Fixed selling and administrative Total unit costs Standards have been computed based on a master budget activity level of 28,900 direct labor hours per month. Actual activity for the past...

The standard cost sheet for Chambers Company, which manufactures one product, follows: $ 100 100 Direct materials, 40 yards at $2.50 per yard Direct labor, 4 hours at $25 per hour Factory overhead applied at 70% of direct labor (variable costs - $50; fixed costs $20) Variable selling and administrative Fixed selling and administrative Total unit costs Standards have been computed based on a master budget activity level of 28,900 direct labor hours per month. Actual activity for the past...

Whispering Corporation manufactures a single product. The

standard cost per unit of product is shown below.

Direct materials—1 pound plastic at $7.00 per pound

$ 7.00

Direct labor—2.5 hours at $11.80 per hour

29.50

Variable manufacturing overhead

17.50

Fixed manufacturing overhead

17.50

Total standard cost per unit

$71.50

The predetermined manufacturing overhead rate is $14.00 per direct

labor hour ($35.00 ÷ 2.5). It was computed from a master

manufacturing overhead budget based on normal production of 13,250

direct labor hours...

Whispering Corporation manufactures a single product. The

standard cost per unit of product is shown below.

Direct materials—1 pound plastic at $7.00 per pound

$ 7.00

Direct labor—2.5 hours at $11.80 per hour

29.50

Variable manufacturing overhead

17.50

Fixed manufacturing overhead

17.50

Total standard cost per unit

$71.50

The predetermined manufacturing overhead rate is $14.00 per direct

labor hour ($35.00 ÷ 2.5). It was computed from a master

manufacturing overhead budget based on normal production of 13,250

direct labor hours...

The standard cost sheet for Chambers Company, which manufactures

one product, follows:

Direct materials, 40 yards at $3.00 per yard

$

120

Direct labor, 5 hours at $30 per hour

150

Factory overhead applied at 70% of direct labor

(variable costs = $70; fixed costs = $35)

105

Variable selling and administrative

74

Fixed selling and administrative

50

Total unit costs

$

499

Standards have been computed based on a master budget activity

level of 29,800 direct labor-hours...

The standard cost sheet for Chambers Company, which manufactures

one product, follows:

Direct materials, 40 yards at $3.00 per yard

$

120

Direct labor, 5 hours at $30 per hour

150

Factory overhead applied at 70% of direct labor

(variable costs = $70; fixed costs = $35)

105

Variable selling and administrative

74

Fixed selling and administrative

50

Total unit costs

$

499

Standards have been computed based on a master budget activity

level of 29,800 direct labor-hours...

Comparison of Actual and Budgeted Operating Income EXHIBIT 14.1 SCHMIDT MACHINERY COMPANY Analysis of Operating Income For October 2019 (1) (2) (3) Variances Actual Operating Income Master (Static) Budget 220U Units 780 1,000 $ 160,400U 100% $639,600 100% Sales $800,000 Variable costs 99.050F 350,950 55 450.000 56 $350,000 Contribution margin $288,650 45% 44% $ 61,350U 150.000 *** 160.650 Fixed costs 25 19 10.650U $128,000 20% $ Operating income $200,000 25% 72,000U *U denotes an unfavorable effect on operating income. *F...

Comparison of Actual and Budgeted Operating Income EXHIBIT 14.1 SCHMIDT MACHINERY COMPANY Analysis of Operating Income For October 2019 (1) (2) (3) Variances Actual Operating Income Master (Static) Budget 220U Units 780 1,000 $ 160,400U 100% $639,600 100% Sales $800,000 Variable costs 99.050F 350,950 55 450.000 56 $350,000 Contribution margin $288,650 45% 44% $ 61,350U 150.000 *** 160.650 Fixed costs 25 19 10.650U $128,000 20% $ Operating income $200,000 25% 72,000U *U denotes an unfavorable effect on operating income. *F...

Rogen Corporation manufactures a single product. The standard

cost per unit of product is shown below.

Direct materials—1 pound plastic at $6 per pound

$ 6.00

Direct labor—0.50 hours at $11.75 per hour

5.88

Variable manufacturing overhead

3.50

Fixed manufacturing overhead

1.50

Total standard cost per unit

$16.88

The predetermined manufacturing overhead rate is $10 per direct

labor hour ($5.00 ÷ 0.50). It was computed from a master

manufacturing overhead budget based on normal production of 2,950

direct labor hours...

Rogen Corporation manufactures a single product. The standard

cost per unit of product is shown below.

Direct materials—1 pound plastic at $6 per pound

$ 6.00

Direct labor—0.50 hours at $11.75 per hour

5.88

Variable manufacturing overhead

3.50

Fixed manufacturing overhead

1.50

Total standard cost per unit

$16.88

The predetermined manufacturing overhead rate is $10 per direct

labor hour ($5.00 ÷ 0.50). It was computed from a master

manufacturing overhead budget based on normal production of 2,950

direct labor hours...

Rogen Corporation manufactures a single product. The standard

cost per unit of product is shown below.

Direct materials—1 pound plastic at $6.00 per pound

$ 6.00

Direct labor—2.0 hours at $11.85 per hour

23.70

Variable manufacturing overhead

12.00

Fixed manufacturing overhead

12.00

Total standard cost per unit

$53.70

The predetermined manufacturing overhead rate is $12.00 per direct

labor hour ($24.00 ÷ 2.0). It was computed from a master

manufacturing overhead budget based on normal production of 11,800

direct labor hours...

Rogen Corporation manufactures a single product. The standard

cost per unit of product is shown below.

Direct materials—1 pound plastic at $6.00 per pound

$ 6.00

Direct labor—2.0 hours at $11.85 per hour

23.70

Variable manufacturing overhead

12.00

Fixed manufacturing overhead

12.00

Total standard cost per unit

$53.70

The predetermined manufacturing overhead rate is $12.00 per direct

labor hour ($24.00 ÷ 2.0). It was computed from a master

manufacturing overhead budget based on normal production of 11,800

direct labor hours...

Most questions answered within 3 hours.

-

A motor produces a torque of 0.25 N m at an angular velocity of

7200 revolutions...

asked 8 minutes ago -

***Please answer the below java question***

Are static methods inheritable? Can they be overridden?

asked 10 minutes ago -

In reaching her destination, a backpacker walks with an average

velocity of 1.13 m/s, due west....

asked 11 minutes ago -

Write two C programs that run a

server program and a client program concurrently.

Server program:...

asked 10 minutes ago -

Executive Program Practical Connection Assignment

Subject : Operations Security.

Assignment:

Provide a reflection of at least...

asked 20 minutes ago -

Every time Casey is at bat he has a 0.4 probability of

getting on base (assume...

asked 28 minutes ago -

The Walston Company is to be liquidated and has the following

liabilities:

Income taxes

$

9,400...

asked 35 minutes ago -

If

the more comprehensive data is available in MEPS, why does the NHIS

still exist? How...

asked 56 minutes ago -

Koo argues that the Japanese economy in the 1990s suffered from

a balance sheet recession. What...

asked 50 minutes ago -

Automobile mechanics conduct diagnosis tests on 150 new cars of

particular make and model to determine...

asked 44 minutes ago -

11) Find the proceeds of a 5 year non-interest

bearing note for $6500 discounted 2.5 years...

asked 50 minutes ago -

Required: Prepare the consolidated financial statements of

Griffin Ltd at 30 June 2019.

Griffin Ltd is...

asked 59 minutes ago