At the end of the current fiscal year, the City of Columbus General Fund pre-adjusted trial...

At the end of the current fiscal year, the City of Columbus General Fund pre-adjusted trial balance showed the following balances for operating and budgetary accounts and fund balance accounts.

| Debits | Credits | ||||||

| Appropriations | $ | 7,124,000 | |||||

| Estimated Other Financing Uses | 3,226,000 | ||||||

| Estimated Revenues | $ | 8,897,000 | |||||

| Encumbrances | 0 | ||||||

| Expenditures | 7,092,000 | ||||||

| Other Financing Uses | 3,220,000 | ||||||

| Revenues | 8,880,000 | ||||||

| Budgetary Fund Balance | 1,453,000 | ||||||

| Fund Balance—Nonspendable—Inventory of Supplies | 175,100 | ||||||

| Fund Balance—Unassigned | 2,009,000 | ||||||

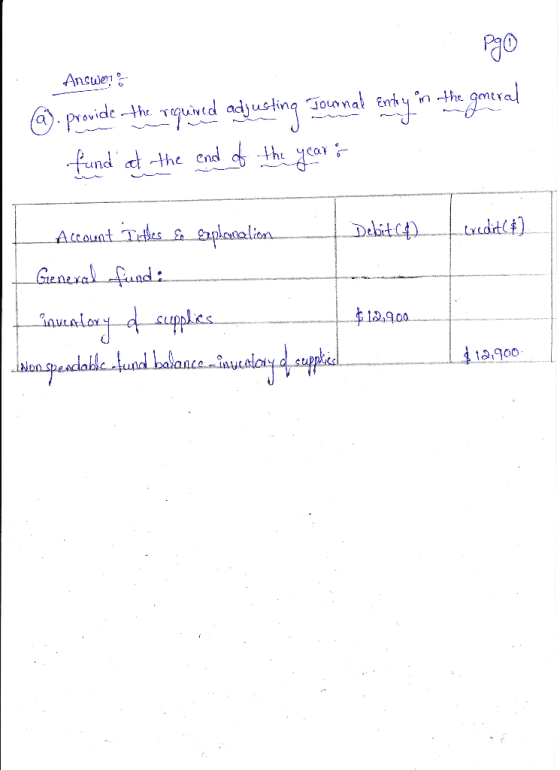

The City of Columbus uses the purchases method of accounting for its inventory of supplies in the General Fund. The city uses a periodic inventory system in which the amount of inventory used during the year and the amount on hand at the end of the year are determined by a physical inventory. During the year, $265,000 of supplies were purchased and recorded as expenditures. These purchases are included in the final expenditures balance of $7,092,000 shown above. The physical inventory revealed a supplies balance of $188,000 at the end of the fiscal year, an increase of $12,900 from the prior year.

Required

- Provide the required adjusting journal entry in the General Fund at the end of the year. (If no entry is required for a transaction/event, select "No Journal Entry Required" in the first account field.)

Homework Answers

Add Answer to:

At the end of the

current fiscal year, the City of Columbus General Fund pre-adjusted

trial...

At the end of the current fiscal year, the City of Columbus General Fund pre-adjusted trial...

At the end of the current fiscal year, the City of Columbus General Fund pre-adjusted trial balance showed the following balances for operating and budgetary accounts and fund balance accounts. Debits Credits Appropriations $ 5,824,000 Estimated Other Financing Uses 2,576,000 Estimated Revenues $ 7,597,000 Encumbrances 0 Expenditures 5,792,000 Other Financing Uses 2,570,000 Revenues 7,580,000 Budgetary Fund Balance 803,000 Fund Balance—Nonspendable—Inventory of Supplies 124,400 Fund Balance—Unassigned 1,986,000 The City of Columbus uses the purchases method of accounting for its inventory of...

At the end of the current fiscal year, the City of Columbus General Fund pre-adjusted trial...

At the end of the current fiscal year, the City of Columbus General Fund pre-adjusted trial balance showed the following balances for operating and budgetary accounts and fund balance accounts. Debits Credits $6,224,000 2,776,000 $7,997,000 Appropriations Estimated Other Financing Uses Estimated Revenues Encumbrances Expenditures Other Financing Uses Revenues Budgetary Fund Balance Fund Balance-Nonspendable-Inventory of Supplies Fund Balance-Unassigned 6,192,000 2,770,000 7,980,000 1,003,000 140,000 1,990,000 The City of Columbus uses the purchases method of accounting for its inventory of supplies in the...

At the end of the current fiscal year, the City of Columbus General Fund pre-adjusted trial balance showed the following balances for operating and budgetary accounts and fund balance accounts. Debits Credits $6,224,000 2,776,000 $7,997,000 Appropriations Estimated Other Financing Uses Estimated Revenues Encumbrances Expenditures Other Financing Uses Revenues Budgetary Fund Balance Fund Balance-Nonspendable-Inventory of Supplies Fund Balance-Unassigned 6,192,000 2,770,000 7,980,000 1,003,000 140,000 1,990,000 The City of Columbus uses the purchases method of accounting for its inventory of supplies in the...

At the end of the current fiscal year, the City of Columbus General Fund pre-adjusted trial...

At the end of the current fiscal year, the City of Columbus General Fund pre-adjusted trial balance showed the following balances for operating and budgetary accounts and fund balance accounts. Debits Credits $6,224,000 2,776,000 $7,997,000 Appropriations Estimated Other Financing Uses Estimated Revenues Encumbrances Expenditures Other Financing Uses Revenues Budgetary Fund Balance Fund Balance-Monspendable-Inventory of Supplies Fund Balance-Unassigned 6,192,000 2,770,000 7,980,000 1,603,000 140,000 1,990,000 The City of Columbus uses the purchases method of accounting for its inventory of supplies in the...

At the end of the current fiscal year, the City of Columbus General Fund pre-adjusted trial balance showed the following balances for operating and budgetary accounts and fund balance accounts. Debits Credits $6,224,000 2,776,000 $7,997,000 Appropriations Estimated Other Financing Uses Estimated Revenues Encumbrances Expenditures Other Financing Uses Revenues Budgetary Fund Balance Fund Balance-Monspendable-Inventory of Supplies Fund Balance-Unassigned 6,192,000 2,770,000 7,980,000 1,603,000 140,000 1,990,000 The City of Columbus uses the purchases method of accounting for its inventory of supplies in the...

At the end of fiscal year 2017, the City of Georgetown's General Fund pre-adjusting trial balance...

At the end of fiscal year 2017, the City of Georgetown's General Fund pre-adjusting trial balance showed the following balances for operating and budgetary accounts and fund balance accounts. Debits Credits Appropriations $ 6,224,000 Estimated Other Financing Uses 2,776,000 Estimated Revenues $ 7,997,000 Encumbrances 0 Expenditures 6,192,000 Other Financing Uses 2,770,000 Revenues 7,980,000 Budgetary Fund Balance 1,003,000 Fund Balance-Nonspendable-Inventory of Supplies 140,000 Fund Balance-Unassigned 1,990,000 Required Prepare the closing entries for the year.

The City of Morganville had the following pre-closing account balances in its General Fund as of April 30, 2017. Debits...

The City of Morganville had the following pre-closing account balances in its General Fund as of April 30, 2017. Debits and credits are not separated; each account had its “normal” balance. Among the expenditures recorded this year is an amount expended on supplies ordered at the end of the previous year. Assume that encumbrances do not lapse and that the City failed to make the journal entry(s) necessary to re-establish the encumbrance in the current year. Required: Prepare all...

The preclosing trial balance at December 31, 20X1, for Lone Wolf’s general fund follows. Debit Credit...

The preclosing trial balance at December 31, 20X1, for Lone Wolf’s general fund follows. Debit Credit Cash $ 94,000 Property Taxes Receivable—Delinquent 118,200 Allowance for Uncollectibles—Delinquent $ 7,100 Due from Other Funds 14,300 Vouchers Payable 63,000 Due to Other Funds 8,400 Fund Balance—Unassigned 120,000 Property Tax Revenue 1,140,000 Miscellaneous Revenue 38,000 Expenditures 1,125,000 Other Financing Uses—Transfer Out 25,000 Estimated Revenues Control 1,233,000 Appropriations Control 1,155,000 Estimated Other Financing Uses—Transfer Out 25,000 Encumbrances 39,000 Budgetary Fund Balance—Assigned for Encumbrances 39,000 Budgetary...

The preclosing trial balance at December 31, 20X1, for Lone Wolf's general fund follows Debit Credit $95,000 116,500 Cash Property Taxes Receivable-Delinquent Allowance for Uncollectibles-Delinqu...

The preclosing trial balance at December 31, 20X1, for Lone Wolf's general fund follows Debit Credit $95,000 116,500 Cash Property Taxes Receivable-Delinquent Allowance for Uncollectibles-Delinquent Due from Other Funds Vouchers Payable Due to Other Funds Fund Balance-Unassigned Property Tax Revenue Miscellaneous Revenue Expenditures Other Financing Uses-Transfer Out Estimated Revenues Control Appropriations Control Estimated Other Financing Uses-Transfer Out encumbranceS Budgetary Fund Balance-Assigned for Encumbrances Budgetary Fund Balance-Unassigned Total 7,400 14,800 70,000 8,900 118,000 1,145,000 35,000 1,140,000 18,000 1,208,000 1,150,000 18,000 37,000...

The preclosing trial balance at December 31, 20X1, for Lone Wolf's general fund follows Debit Credit $95,000 116,500 Cash Property Taxes Receivable-Delinquent Allowance for Uncollectibles-Delinquent Due from Other Funds Vouchers Payable Due to Other Funds Fund Balance-Unassigned Property Tax Revenue Miscellaneous Revenue Expenditures Other Financing Uses-Transfer Out Estimated Revenues Control Appropriations Control Estimated Other Financing Uses-Transfer Out encumbranceS Budgetary Fund Balance-Assigned for Encumbrances Budgetary Fund Balance-Unassigned Total 7,400 14,800 70,000 8,900 118,000 1,145,000 35,000 1,140,000 18,000 1,208,000 1,150,000 18,000 37,000...

· The City of Troutman had the following partial list of pre-closing account balances in its General Fund as of June...

· The City of Troutman had the following partial list of pre-closing account balances in its General Fund as of June 30, 2019. Debits Credits $3,675,000 385,000 111,000 60,000 107,000 290,000 Appropriations Control Budgetary Fund Balance Budgetary Fund Balance - Reserve for Encumbrances Due to Other Funds Encumbrances Control Estimated Other Financing Uses Control Estimated Revenues Control Expenditures Control Fund Balance Other Financing Uses Control-Transfers Out Revenues Control Taxes Receivable-Delinquent Vouchers Payable 3,860,000 3,405,000 272,000 315,000 3,968,000 85,000 275,000 Required:...

· The City of Troutman had the following partial list of pre-closing account balances in its General Fund as of June 30, 2019. Debits Credits $3,675,000 385,000 111,000 60,000 107,000 290,000 Appropriations Control Budgetary Fund Balance Budgetary Fund Balance - Reserve for Encumbrances Due to Other Funds Encumbrances Control Estimated Other Financing Uses Control Estimated Revenues Control Expenditures Control Fund Balance Other Financing Uses Control-Transfers Out Revenues Control Taxes Receivable-Delinquent Vouchers Payable 3,860,000 3,405,000 272,000 315,000 3,968,000 85,000 275,000 Required:...

Chapter 17 - Governmental Entities: Introduction and General Fund Accounting 2,000 84. The adjusted trial balance...

Chapter 17 - Governmental Entities: Introduction and General Fund Accounting 2,000 84. The adjusted trial balance for White River for the fiscal year ended June 30, 20X9, is presented below. Debits Credits Cash $ 51,000 Property Taxes Receivable-Delinquent 20,000 Allowance for Uncollectible Taxes-Delinquent $ 15,000 Inventory of Supplies Vouchers Payable 10,000 Due to Internal Service Fund 2,000 Fund Balance-Assigned for Inventories 2,000 Fund Balance-Assigned for Encumbrances 12,000 Fund Balance-Unassigned 6,000 Expenditures 718,000 Transfer Out to Internal Service Fund 40,000 Property...

Chapter 17 - Governmental Entities: Introduction and General Fund Accounting 2,000 84. The adjusted trial balance for White River for the fiscal year ended June 30, 20X9, is presented below. Debits Credits Cash $ 51,000 Property Taxes Receivable-Delinquent 20,000 Allowance for Uncollectible Taxes-Delinquent $ 15,000 Inventory of Supplies Vouchers Payable 10,000 Due to Internal Service Fund 2,000 Fund Balance-Assigned for Inventories 2,000 Fund Balance-Assigned for Encumbrances 12,000 Fund Balance-Unassigned 6,000 Expenditures 718,000 Transfer Out to Internal Service Fund 40,000 Property...

Create the balance sheet according to this trial balance The following unadjusted trial balances are for...

Create the balance sheet according to this trial balance The following unadjusted trial balances are for the governmental funds of the City of Copeland prepared from the current accounting records: General Fund Debit Credit Cash $ 19,000 Taxes Receivable 202,000 Allowance for Uncollectible Taxes $ 2,000 Vouchers Payable 24,000 Due to Debt Service Fund 10,000 Unavailable Revenues 16,000 Encumbrances Outstanding 9,000 Fund Balance—Unassigned 103,000 Revenues 176,000 Expenditures 110,000 Encumbrances 9,000 Estimated Revenues 190,000 Appropriations 171,000...

At the end of the current fiscal year, the City of Columbus General Fund pre-adjusted trial balance showed the following balances for operating and budgetary accounts and fund balance accounts. Debits Credits $6,224,000 2,776,000 $7,997,000 Appropriations Estimated Other Financing Uses Estimated Revenues Encumbrances Expenditures Other Financing Uses Revenues Budgetary Fund Balance Fund Balance-Nonspendable-Inventory of Supplies Fund Balance-Unassigned 6,192,000 2,770,000 7,980,000 1,003,000 140,000 1,990,000 The City of Columbus uses the purchases method of accounting for its inventory of supplies in the...

At the end of the current fiscal year, the City of Columbus General Fund pre-adjusted trial balance showed the following balances for operating and budgetary accounts and fund balance accounts. Debits Credits $6,224,000 2,776,000 $7,997,000 Appropriations Estimated Other Financing Uses Estimated Revenues Encumbrances Expenditures Other Financing Uses Revenues Budgetary Fund Balance Fund Balance-Nonspendable-Inventory of Supplies Fund Balance-Unassigned 6,192,000 2,770,000 7,980,000 1,003,000 140,000 1,990,000 The City of Columbus uses the purchases method of accounting for its inventory of supplies in the...

At the end of the current fiscal year, the City of Columbus General Fund pre-adjusted trial balance showed the following balances for operating and budgetary accounts and fund balance accounts. Debits Credits $6,224,000 2,776,000 $7,997,000 Appropriations Estimated Other Financing Uses Estimated Revenues Encumbrances Expenditures Other Financing Uses Revenues Budgetary Fund Balance Fund Balance-Monspendable-Inventory of Supplies Fund Balance-Unassigned 6,192,000 2,770,000 7,980,000 1,603,000 140,000 1,990,000 The City of Columbus uses the purchases method of accounting for its inventory of supplies in the...

At the end of the current fiscal year, the City of Columbus General Fund pre-adjusted trial balance showed the following balances for operating and budgetary accounts and fund balance accounts. Debits Credits $6,224,000 2,776,000 $7,997,000 Appropriations Estimated Other Financing Uses Estimated Revenues Encumbrances Expenditures Other Financing Uses Revenues Budgetary Fund Balance Fund Balance-Monspendable-Inventory of Supplies Fund Balance-Unassigned 6,192,000 2,770,000 7,980,000 1,603,000 140,000 1,990,000 The City of Columbus uses the purchases method of accounting for its inventory of supplies in the...

The preclosing trial balance at December 31, 20X1, for Lone Wolf's general fund follows Debit Credit $95,000 116,500 Cash Property Taxes Receivable-Delinquent Allowance for Uncollectibles-Delinquent Due from Other Funds Vouchers Payable Due to Other Funds Fund Balance-Unassigned Property Tax Revenue Miscellaneous Revenue Expenditures Other Financing Uses-Transfer Out Estimated Revenues Control Appropriations Control Estimated Other Financing Uses-Transfer Out encumbranceS Budgetary Fund Balance-Assigned for Encumbrances Budgetary Fund Balance-Unassigned Total 7,400 14,800 70,000 8,900 118,000 1,145,000 35,000 1,140,000 18,000 1,208,000 1,150,000 18,000 37,000...

The preclosing trial balance at December 31, 20X1, for Lone Wolf's general fund follows Debit Credit $95,000 116,500 Cash Property Taxes Receivable-Delinquent Allowance for Uncollectibles-Delinquent Due from Other Funds Vouchers Payable Due to Other Funds Fund Balance-Unassigned Property Tax Revenue Miscellaneous Revenue Expenditures Other Financing Uses-Transfer Out Estimated Revenues Control Appropriations Control Estimated Other Financing Uses-Transfer Out encumbranceS Budgetary Fund Balance-Assigned for Encumbrances Budgetary Fund Balance-Unassigned Total 7,400 14,800 70,000 8,900 118,000 1,145,000 35,000 1,140,000 18,000 1,208,000 1,150,000 18,000 37,000...

· The City of Troutman had the following partial list of pre-closing account balances in its General Fund as of June 30, 2019. Debits Credits $3,675,000 385,000 111,000 60,000 107,000 290,000 Appropriations Control Budgetary Fund Balance Budgetary Fund Balance - Reserve for Encumbrances Due to Other Funds Encumbrances Control Estimated Other Financing Uses Control Estimated Revenues Control Expenditures Control Fund Balance Other Financing Uses Control-Transfers Out Revenues Control Taxes Receivable-Delinquent Vouchers Payable 3,860,000 3,405,000 272,000 315,000 3,968,000 85,000 275,000 Required:...

· The City of Troutman had the following partial list of pre-closing account balances in its General Fund as of June 30, 2019. Debits Credits $3,675,000 385,000 111,000 60,000 107,000 290,000 Appropriations Control Budgetary Fund Balance Budgetary Fund Balance - Reserve for Encumbrances Due to Other Funds Encumbrances Control Estimated Other Financing Uses Control Estimated Revenues Control Expenditures Control Fund Balance Other Financing Uses Control-Transfers Out Revenues Control Taxes Receivable-Delinquent Vouchers Payable 3,860,000 3,405,000 272,000 315,000 3,968,000 85,000 275,000 Required:...

Chapter 17 - Governmental Entities: Introduction and General Fund Accounting 2,000 84. The adjusted trial balance for White River for the fiscal year ended June 30, 20X9, is presented below. Debits Credits Cash $ 51,000 Property Taxes Receivable-Delinquent 20,000 Allowance for Uncollectible Taxes-Delinquent $ 15,000 Inventory of Supplies Vouchers Payable 10,000 Due to Internal Service Fund 2,000 Fund Balance-Assigned for Inventories 2,000 Fund Balance-Assigned for Encumbrances 12,000 Fund Balance-Unassigned 6,000 Expenditures 718,000 Transfer Out to Internal Service Fund 40,000 Property...

Chapter 17 - Governmental Entities: Introduction and General Fund Accounting 2,000 84. The adjusted trial balance for White River for the fiscal year ended June 30, 20X9, is presented below. Debits Credits Cash $ 51,000 Property Taxes Receivable-Delinquent 20,000 Allowance for Uncollectible Taxes-Delinquent $ 15,000 Inventory of Supplies Vouchers Payable 10,000 Due to Internal Service Fund 2,000 Fund Balance-Assigned for Inventories 2,000 Fund Balance-Assigned for Encumbrances 12,000 Fund Balance-Unassigned 6,000 Expenditures 718,000 Transfer Out to Internal Service Fund 40,000 Property...

Most questions answered within 3 hours.

-

Antimony, Sb, has two stable isotopes: 121Sb, 120.904u, and

123Sb, 122.904u. What is the percent abundance...

asked 9 minutes ago -

Compare the solubility of calcium fluoride in

each of the following aqueous solutions:

Clear All

0.10...

asked 3 minutes ago -

The annual maintenance costs associated with a machine are $1000

for the first 10 years and...

asked 8 minutes ago -

Milano Pizza is a small neighborhood pizzeria that has a small

area for in-store dining as...

asked 24 minutes ago -

Suppose the current exchange rate for the Russian ruble is RUB

64.18. The expected exchange rate...

asked 25 minutes ago -

Instructions Part 1 - Implementation of a Doubly Linked

List Attached you will find the code...

asked 2 hours ago -

You work for a factory making bricks. A coworker accidentally

contaminated one of the bricks with...

asked 2 hours ago -

for python-3

I want to prompt the user to enter their first name and then

Call...

asked 2 hours ago -

Q3 If the formation of a hairpin loop requires a minimum

stem

length of 6 contiguous...

asked 2 hours ago -

Enzymes work by lowering the _____ of a reaction.

Select one:

a. activation energy

b. entropy...

asked 3 hours ago -

Assume three digits are used to represent positive integers and

also assume the following operations are...

asked 4 hours ago -

How many stairs can a 63-kg person climb up with the energy

contained in a candy...

asked 4 hours ago