Homework Answers

SOLUTION:

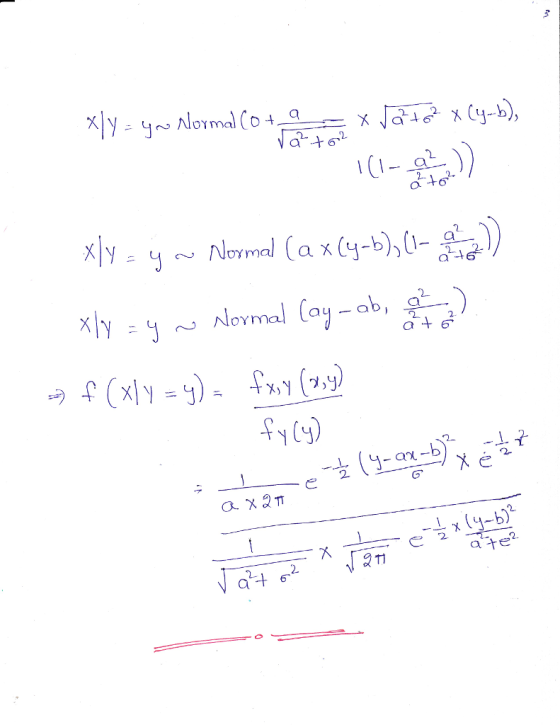

Given that,

X,Y have a bivariate normal distribution

marginal distribution X (0,1)

conditional distribution of Y given X = x is

(ax +b,

).

Add Answer to:

please help me

6. Suppose X, Y have a bivariate normal distribution with marginal dis- tribution...

6. Suppose that (W, Z) have a bivariate normal distribution, that W ∼ N (0, 1),...

6. Suppose that (W, Z) have a bivariate normal distribution,

that W ∼ N (0, 1), and that the conditional distribution of Z,

given that W = w, is N (aw + b, τ 2 ). (a) What is the marginal

distribution of Z? (b) What is the conditional distribution of W,

given that Z = z?

6. Suppose that (W, Z) have a bivariate normal distribution, that W N(0,1), and that the conditional distribution of Z, given that W-w....

6. Suppose that (W, Z) have a bivariate normal distribution,

that W ∼ N (0, 1), and that the conditional distribution of Z,

given that W = w, is N (aw + b, τ 2 ). (a) What is the marginal

distribution of Z? (b) What is the conditional distribution of W,

given that Z = z?

6. Suppose that (W, Z) have a bivariate normal distribution, that W N(0,1), and that the conditional distribution of Z, given that W-w....

Suppose that (W,Z) have a bivariate normal distribution, that W ~N(0,1), and that the conditional distribution...

Suppose that (W,Z) have a bivariate normal distribution, that W ~N(0,1), and that the conditional distribution of Z, given that Ww, is N(aw b,T2). (a) What is the marginal distribution of Z? (b) What is the conditional distribution of W, given that Z2?

Suppose that (W,Z) have a bivariate normal distribution, that W ~N(0,1), and that the conditional distribution of Z, given that Ww, is N(aw b,T2). (a) What is the marginal distribution of Z? (b) What is the conditional distribution of W, given that Z2?

6. Suppose that (W, Z) have a bivariate normal distribution, that W~N(0, 1), and that the...

6. Suppose that (W, Z) have a bivariate normal distribution, that W~N(0, 1), and that the conditional distribution of Z, given that W-w, is N(aw b, T2). (a) What is the marginal distribution of Z? b) What is the conditional distribution of W, given that Z-2?

6. Suppose that (W, Z) have a bivariate normal distribution, that W~N(0, 1), and that the conditional distribution of Z, given that W-w, is N(aw b, T2). (a) What is the marginal distribution of Z? b) What is the conditional distribution of W, given that Z-2?

The random variables Z and W have a bivariate normal dis- tribution with EZ] = E[W] = 0, Var(Z) =...

The random variables Z and W have a bivariate normal dis- tribution with EZ] = E[W] = 0, Var(Z) = Var(W) = 1, and oorrelation ρ E (-1,1). Given that Pl2+ W 1-8413, find the value ofp. Hint: 8413 = φ(1), where φ is the standard normal distribution function.]

The random variables Z and W have a bivariate normal dis- tribution with EZ] = E[W] = 0, Var(Z) = Var(W) = 1, and oorrelation ρ E (-1,1). Given that Pl2+...

The random variables Z and W have a bivariate normal dis- tribution with EZ] = E[W] = 0, Var(Z) = Var(W) = 1, and oorrelation ρ E (-1,1). Given that Pl2+ W 1-8413, find the value ofp. Hint: 8413 = φ(1), where φ is the standard normal distribution function.]

The random variables Z and W have a bivariate normal dis- tribution with EZ] = E[W] = 0, Var(Z) = Var(W) = 1, and oorrelation ρ E (-1,1). Given that Pl2+...

please help me 5. Suppose X and Y are standard normal random variables. Find an expres-...

please help me

5. Suppose X and Y are standard normal random variables. Find an expres- sion for P(X - 3Y S1) in terms of the standard normal distribution function In two cases: (i) X and Y are independent (ii) X and Y have bivariate normal distribution with correlation ρ-1/2.

please help me

5. Suppose X and Y are standard normal random variables. Find an expres- sion for P(X - 3Y S1) in terms of the standard normal distribution function In two cases: (i) X and Y are independent (ii) X and Y have bivariate normal distribution with correlation ρ-1/2.

6. Suppose that X and Y have a bivariate normal distribution with px 1 and y- (a) Order the follo...

6. Suppose that X and Y have a bivariate normal distribution with px 1 and y- (a) Order the following probabilities from largest to smallest, assuming p >0: P(X 2 (b) Repeat (a) assuming p < 0. (c) Repeat (a) assuming we are interested in (X 0.25) instead of (x 2 2).

6. Suppose that X and Y have a bivariate normal distribution with px 1 and y- (a) Order the following probabilities from largest to smallest, assuming p >0:...

6. Suppose that X and Y have a bivariate normal distribution with px 1 and y- (a) Order the following probabilities from largest to smallest, assuming p >0: P(X 2 (b) Repeat (a) assuming p < 0. (c) Repeat (a) assuming we are interested in (X 0.25) instead of (x 2 2).

6. Suppose that X and Y have a bivariate normal distribution with px 1 and y- (a) Order the following probabilities from largest to smallest, assuming p >0:...

Suppose (X, Y ) has bivariate normal distribution, E(X) = E(Y ) = 0,V ar(X) =...

Suppose (X, Y ) has bivariate

normal distribution, E(X) = E(Y ) = 0,V ar(X) = σX2 , V ar(Y ) =

σY2 and Correl(X, Y ) = ρ. Calculate the conditional expectation

E(X2|Y ).

I. Suppose (X,Y) has bivariate normal distribution, E(X) = E(Y) 0, Var(X)-σ , Var(Y) σ and Correl (X,Y)-p. Calculate the conditional expectation ECKY expectation E(X2Y)

Suppose (X, Y ) has bivariate

normal distribution, E(X) = E(Y ) = 0,V ar(X) = σX2 , V ar(Y ) =

σY2 and Correl(X, Y ) = ρ. Calculate the conditional expectation

E(X2|Y ).

I. Suppose (X,Y) has bivariate normal distribution, E(X) = E(Y) 0, Var(X)-σ , Var(Y) σ and Correl (X,Y)-p. Calculate the conditional expectation ECKY expectation E(X2Y)

bos on 559 2. Random variable X and Y have a bivariate normal distribution. The conditional...

bos on 559 2. Random variable X and Y have a bivariate normal distribution. The conditional density of X given Y = y is a OVH a. bivariate normal distribution Bossiu b. chi-square distribution c. linear distribution oms d. normal distribution e. not necessarily any of the above distributions. 3. The probability distribution for the random variable X is shown by the table. Use the transformation technique to construct the table for the probability distribution of Y = x2 +...

bos on 559 2. Random variable X and Y have a bivariate normal distribution. The conditional density of X given Y = y is a OVH a. bivariate normal distribution Bossiu b. chi-square distribution c. linear distribution oms d. normal distribution e. not necessarily any of the above distributions. 3. The probability distribution for the random variable X is shown by the table. Use the transformation technique to construct the table for the probability distribution of Y = x2 +...

1. Suppose (x, Y) has bivariate normal distribution, E(x) E(Y)- 0, Var(X) σ , Var(Y) σ...

1. Suppose (x, Y) has bivariate normal distribution, E(x) E(Y)- 0, Var(X) σ , Var(Y) σ and Correl(X, Y) p. Calculate the conditional expectation E(X2|Y).

1. Suppose (x, Y) has bivariate normal distribution, E(x) E(Y)- 0, Var(X) σ , Var(Y) σ and Correl(X, Y) p. Calculate the conditional expectation E(X2|Y).

17. Suppose that (X,Y) has a bivariate normal distribu- zion with parameters diy, x, 0y.p. io...

17. Suppose that (X,Y) has a bivariate normal distribu- zion with parameters diy, x, 0y.p. io show that (2 , 4") has a bivariate normal distri- bution with parameters 0, 1,0.1.p. b) What is the joint distribution of (aX + b,cY + d).

17. Suppose that (X,Y) has a bivariate normal distribu- zion with parameters diy, x, 0y.p. io show that (2 , 4") has a bivariate normal distri- bution with parameters 0, 1,0.1.p. b) What is the joint distribution of (aX + b,cY + d).

6. Suppose that (W, Z) have a bivariate normal distribution,

that W ∼ N (0, 1), and that the conditional distribution of Z,

given that W = w, is N (aw + b, τ 2 ). (a) What is the marginal

distribution of Z? (b) What is the conditional distribution of W,

given that Z = z?

6. Suppose that (W, Z) have a bivariate normal distribution, that W N(0,1), and that the conditional distribution of Z, given that W-w....

6. Suppose that (W, Z) have a bivariate normal distribution,

that W ∼ N (0, 1), and that the conditional distribution of Z,

given that W = w, is N (aw + b, τ 2 ). (a) What is the marginal

distribution of Z? (b) What is the conditional distribution of W,

given that Z = z?

6. Suppose that (W, Z) have a bivariate normal distribution, that W N(0,1), and that the conditional distribution of Z, given that W-w....

Suppose that (W,Z) have a bivariate normal distribution, that W ~N(0,1), and that the conditional distribution of Z, given that Ww, is N(aw b,T2). (a) What is the marginal distribution of Z? (b) What is the conditional distribution of W, given that Z2?

Suppose that (W,Z) have a bivariate normal distribution, that W ~N(0,1), and that the conditional distribution of Z, given that Ww, is N(aw b,T2). (a) What is the marginal distribution of Z? (b) What is the conditional distribution of W, given that Z2?

6. Suppose that (W, Z) have a bivariate normal distribution, that W~N(0, 1), and that the conditional distribution of Z, given that W-w, is N(aw b, T2). (a) What is the marginal distribution of Z? b) What is the conditional distribution of W, given that Z-2?

6. Suppose that (W, Z) have a bivariate normal distribution, that W~N(0, 1), and that the conditional distribution of Z, given that W-w, is N(aw b, T2). (a) What is the marginal distribution of Z? b) What is the conditional distribution of W, given that Z-2?

The random variables Z and W have a bivariate normal dis- tribution with EZ] = E[W] = 0, Var(Z) = Var(W) = 1, and oorrelation ρ E (-1,1). Given that Pl2+ W 1-8413, find the value ofp. Hint: 8413 = φ(1), where φ is the standard normal distribution function.]

The random variables Z and W have a bivariate normal dis- tribution with EZ] = E[W] = 0, Var(Z) = Var(W) = 1, and oorrelation ρ E (-1,1). Given that Pl2+...

The random variables Z and W have a bivariate normal dis- tribution with EZ] = E[W] = 0, Var(Z) = Var(W) = 1, and oorrelation ρ E (-1,1). Given that Pl2+ W 1-8413, find the value ofp. Hint: 8413 = φ(1), where φ is the standard normal distribution function.]

The random variables Z and W have a bivariate normal dis- tribution with EZ] = E[W] = 0, Var(Z) = Var(W) = 1, and oorrelation ρ E (-1,1). Given that Pl2+...

please help me

5. Suppose X and Y are standard normal random variables. Find an expres- sion for P(X - 3Y S1) in terms of the standard normal distribution function In two cases: (i) X and Y are independent (ii) X and Y have bivariate normal distribution with correlation ρ-1/2.

please help me

5. Suppose X and Y are standard normal random variables. Find an expres- sion for P(X - 3Y S1) in terms of the standard normal distribution function In two cases: (i) X and Y are independent (ii) X and Y have bivariate normal distribution with correlation ρ-1/2.

6. Suppose that X and Y have a bivariate normal distribution with px 1 and y- (a) Order the following probabilities from largest to smallest, assuming p >0: P(X 2 (b) Repeat (a) assuming p < 0. (c) Repeat (a) assuming we are interested in (X 0.25) instead of (x 2 2).

6. Suppose that X and Y have a bivariate normal distribution with px 1 and y- (a) Order the following probabilities from largest to smallest, assuming p >0:...

6. Suppose that X and Y have a bivariate normal distribution with px 1 and y- (a) Order the following probabilities from largest to smallest, assuming p >0: P(X 2 (b) Repeat (a) assuming p < 0. (c) Repeat (a) assuming we are interested in (X 0.25) instead of (x 2 2).

6. Suppose that X and Y have a bivariate normal distribution with px 1 and y- (a) Order the following probabilities from largest to smallest, assuming p >0:...

Suppose (X, Y ) has bivariate

normal distribution, E(X) = E(Y ) = 0,V ar(X) = σX2 , V ar(Y ) =

σY2 and Correl(X, Y ) = ρ. Calculate the conditional expectation

E(X2|Y ).

I. Suppose (X,Y) has bivariate normal distribution, E(X) = E(Y) 0, Var(X)-σ , Var(Y) σ and Correl (X,Y)-p. Calculate the conditional expectation ECKY expectation E(X2Y)

Suppose (X, Y ) has bivariate

normal distribution, E(X) = E(Y ) = 0,V ar(X) = σX2 , V ar(Y ) =

σY2 and Correl(X, Y ) = ρ. Calculate the conditional expectation

E(X2|Y ).

I. Suppose (X,Y) has bivariate normal distribution, E(X) = E(Y) 0, Var(X)-σ , Var(Y) σ and Correl (X,Y)-p. Calculate the conditional expectation ECKY expectation E(X2Y)

bos on 559 2. Random variable X and Y have a bivariate normal distribution. The conditional density of X given Y = y is a OVH a. bivariate normal distribution Bossiu b. chi-square distribution c. linear distribution oms d. normal distribution e. not necessarily any of the above distributions. 3. The probability distribution for the random variable X is shown by the table. Use the transformation technique to construct the table for the probability distribution of Y = x2 +...

bos on 559 2. Random variable X and Y have a bivariate normal distribution. The conditional density of X given Y = y is a OVH a. bivariate normal distribution Bossiu b. chi-square distribution c. linear distribution oms d. normal distribution e. not necessarily any of the above distributions. 3. The probability distribution for the random variable X is shown by the table. Use the transformation technique to construct the table for the probability distribution of Y = x2 +...

1. Suppose (x, Y) has bivariate normal distribution, E(x) E(Y)- 0, Var(X) σ , Var(Y) σ and Correl(X, Y) p. Calculate the conditional expectation E(X2|Y).

1. Suppose (x, Y) has bivariate normal distribution, E(x) E(Y)- 0, Var(X) σ , Var(Y) σ and Correl(X, Y) p. Calculate the conditional expectation E(X2|Y).

17. Suppose that (X,Y) has a bivariate normal distribu- zion with parameters diy, x, 0y.p. io show that (2 , 4") has a bivariate normal distri- bution with parameters 0, 1,0.1.p. b) What is the joint distribution of (aX + b,cY + d).

17. Suppose that (X,Y) has a bivariate normal distribu- zion with parameters diy, x, 0y.p. io show that (2 , 4") has a bivariate normal distri- bution with parameters 0, 1,0.1.p. b) What is the joint distribution of (aX + b,cY + d).

Most questions answered within 3 hours.

-

a bottle cap manufacturer with four machines and six operators

wants to see if variation in...

asked 34 minutes ago -

State Farm Insurance studies show that in Colorado, 55% of the

auto insurance claims submitted for...

asked 1 hour ago -

Complete the following reactions which form ethers (A

and B) and cyclic ethers (C-E) as major...

asked 1 hour ago -

in a perfectly elastic collision what is the velocity of ball A

if the original direction...

asked 2 hours ago -

PLEASE ANSWER ALL

1) The pressure of the atmosphere decreases with increasing

altitude in the

Choose...

asked 2 hours ago -

A simple random sample of 25,000 individuals are surveyed in

order to determine the prevalence of...

asked 2 hours ago -

People who do very detailed work close up, such as jewelers,

often can see objects clearly...

asked 2 hours ago -

14 years ago, Blue Lake Corp. issued 30 year to maturity

zero-coupon bonds with a par...

asked 2 hours ago -

Warnerwoods Company uses a perpetual inventory system. It

entered into the following purchases and sales transactions...

asked 2 hours ago -

Equivalent Units of Conversion Costs

The Rolling Department of Oak Ridge Steel Company had 6,842 tons...

asked 2 hours ago -

what does the concept of "core competence" mean? why

is this concept important? How would you...

asked 2 hours ago -

__________ is a type of visualization that is linked to strategy

and used within a formal...

asked 2 hours ago