Homework Answers

Hi. If you have any doubts

relating to the above solution feel free to rise your doubts

through comments. Thank You.

Hi. If you have any doubts

relating to the above solution feel free to rise your doubts

through comments. Thank You.

Add Answer to:

Problem 5-24 (LO 5-7) Check my work On January 1, 2018, Ackerman sold equipment to Brannigan...

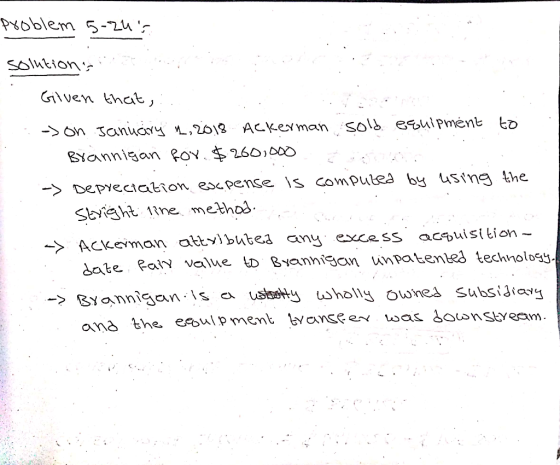

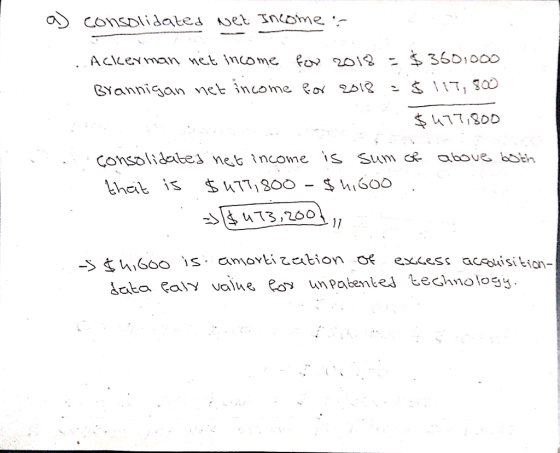

Problem 5-24 (LO 5-7) On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned...

Problem 5-24 (LO 5-7) On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $210,000 In cash. The equipment had originally cost $189,000 but had a book value of only $115,500 when transferred. On that date, the equipment had a five-year remaining life. Depreciation expense is computed using the straight-line method. Ackerman reported $310,000 In net Income in 2018 (not including any Investment Income) while Brannlgan reported $101,300. Ackerman attributed any excess acquisition date fair value...

Problem 5-24 (LO 5-7) On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $210,000 In cash. The equipment had originally cost $189,000 but had a book value of only $115,500 when transferred. On that date, the equipment had a five-year remaining life. Depreciation expense is computed using the straight-line method. Ackerman reported $310,000 In net Income in 2018 (not including any Investment Income) while Brannlgan reported $101,300. Ackerman attributed any excess acquisition date fair value...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $190,000 in...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $190,000 in cash. The equipment had originally cost $171,000 but had a book value of only $104,500 when transferred. On that date, the equipment had a five-year remaining life. Depreciation expense is computed using the straight-line method. Ackerman reported $470,000 in net income in 2018 (not including any investment income) while Brannigan reported $154,100. Ackerman attributed any excess acquisition-date fair value to Brannigan's unpatented technology, which...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $190,000 in cash. The equipment had originally cost $171,000 but had a book value of only $104,500 when transferred. On that date, the equipment had a five-year remaining life. Depreciation expense is computed using the straight-line method. Ackerman reported $470,000 in net income in 2018 (not including any investment income) while Brannigan reported $154,100. Ackerman attributed any excess acquisition-date fair value to Brannigan's unpatented technology, which...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $310,000 in...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $310,000 in cash. The equipment had originally cost $279,000 but had a book value of only $170,500 when transferred. On that date, the equipment had a five-year remaining life. Depreciation expense is computed using the straight-line method. Ackerman reported $410,000 in net income in 2018 (not including any investment income) while Brannigan reported $134,300. Ackerman attributed any excess acquisition-date fair value to Brannigan's unpatented technology, which...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $310,000 in cash. The equipment had originally cost $279,000 but had a book value of only $170,500 when transferred. On that date, the equipment had a five-year remaining life. Depreciation expense is computed using the straight-line method. Ackerman reported $410,000 in net income in 2018 (not including any investment income) while Brannigan reported $134,300. Ackerman attributed any excess acquisition-date fair value to Brannigan's unpatented technology, which...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $250,000 in...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $250,000 in cash. The equipment had originally cost $225,000 but had a book value of only $137,500 when transferred. On that date, the equipment had a five-year remaining life. Depreciation expense is computed using the straight-line method. Ackerman reported $350,000 in net income in 2018 (not including any investment income) while Brannigan reported $114,500. Ackerman attributed any excess acquisition date fair value to Brannigan's unpatented technology,...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $250,000 in cash. The equipment had originally cost $225,000 but had a book value of only $137,500 when transferred. On that date, the equipment had a five-year remaining life. Depreciation expense is computed using the straight-line method. Ackerman reported $350,000 in net income in 2018 (not including any investment income) while Brannigan reported $114,500. Ackerman attributed any excess acquisition date fair value to Brannigan's unpatented technology,...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $270,000 in...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $270,000 in cash. The equipment had originally cost $243,000 but had a book value of only $148,500 when transferred. On that date, the equipment had a five-year remaining life. Depreciation expense is computed using the straight-line method. Ackerman reported $370,000 in net income in 2018 (not including any investment income) while Brannigan reported $121,100. Ackerman attributed any excess acquisition-date fair value to Brannigan's unpatented technology, which...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $340,000 in...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $340,000 in cash. The equipment had originally cost $306,000 but had a book value of only $187,000 when transferred. On that date, the equipment had a five-year remaining life. Depreciation expense is computed using the straight-line method. Ackerman reported $440,000 in net income in 2018 (not including any investment income) while Brannigan reported $144,200. Ackerman attributed any excess acquisition-date fair value to Brannigan's unpatented technology, which...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $280,000 in...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $280,000 in cash. The equipment had originally cost $252,000 but had a book value of only $154,000 when transferred. On that date, the equipment had a five-year remaining life. Depreciation expense is computed using the straight-line method. Ackerman reported $380,000 in net income in 2018 (not including any investment income) while Brannigan reported $124,400. Ackerman attributed any excess acquisition-date fair value to Brannigan's unpatented technology, which...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $190,000 in...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $190,000 in cash. The equipment had originally cost $171,000 but had a book value of only $104,500 when transferred. On that date, the equipment had a five-year remaining life. Depreciation expense is computed using the straight-line method. Ackerman reported $470,000 in net income in 2018 (not including any investment income) while Brannigan reported $154,100. Ackerman attributed any excess acquisition-date fair value to Brannigan's unpatented technology, which...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $120,000...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $120,000 in cash. The equipment had originally cost $108,000 but had a book value of only $66,000 when transferred. On that date, the equipment had a five-year remaining life. Depreciation expense is computed using the straight-line method. Ackerman reported $540,000 in net income in 2018 (not including any investment income) while Brannigan reported $177,200. Ackerman attributed any excess acquisition-date fair value to Brannigan's unpatented technology, which...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $360,000 in...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $360,000 in cash. The equipment had originally cost $324,000 but had a book value of only $198,000 when transferred. On that date, the equipment had a five-year remaining life. Depreciation expense is computed using the straight-line method. Ackerman reported $460,000 in net income in 2018 (not including any investment income) while Brannigan reported $150,800. Ackerman attributed any excess acquisition-date fair value to Brannigan's unpatented technology, which...

Problem 5-24 (LO 5-7) On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $210,000 In cash. The equipment had originally cost $189,000 but had a book value of only $115,500 when transferred. On that date, the equipment had a five-year remaining life. Depreciation expense is computed using the straight-line method. Ackerman reported $310,000 In net Income in 2018 (not including any Investment Income) while Brannlgan reported $101,300. Ackerman attributed any excess acquisition date fair value...

Problem 5-24 (LO 5-7) On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $210,000 In cash. The equipment had originally cost $189,000 but had a book value of only $115,500 when transferred. On that date, the equipment had a five-year remaining life. Depreciation expense is computed using the straight-line method. Ackerman reported $310,000 In net Income in 2018 (not including any Investment Income) while Brannlgan reported $101,300. Ackerman attributed any excess acquisition date fair value...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $190,000 in cash. The equipment had originally cost $171,000 but had a book value of only $104,500 when transferred. On that date, the equipment had a five-year remaining life. Depreciation expense is computed using the straight-line method. Ackerman reported $470,000 in net income in 2018 (not including any investment income) while Brannigan reported $154,100. Ackerman attributed any excess acquisition-date fair value to Brannigan's unpatented technology, which...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $190,000 in cash. The equipment had originally cost $171,000 but had a book value of only $104,500 when transferred. On that date, the equipment had a five-year remaining life. Depreciation expense is computed using the straight-line method. Ackerman reported $470,000 in net income in 2018 (not including any investment income) while Brannigan reported $154,100. Ackerman attributed any excess acquisition-date fair value to Brannigan's unpatented technology, which...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $310,000 in cash. The equipment had originally cost $279,000 but had a book value of only $170,500 when transferred. On that date, the equipment had a five-year remaining life. Depreciation expense is computed using the straight-line method. Ackerman reported $410,000 in net income in 2018 (not including any investment income) while Brannigan reported $134,300. Ackerman attributed any excess acquisition-date fair value to Brannigan's unpatented technology, which...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $310,000 in cash. The equipment had originally cost $279,000 but had a book value of only $170,500 when transferred. On that date, the equipment had a five-year remaining life. Depreciation expense is computed using the straight-line method. Ackerman reported $410,000 in net income in 2018 (not including any investment income) while Brannigan reported $134,300. Ackerman attributed any excess acquisition-date fair value to Brannigan's unpatented technology, which...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $250,000 in cash. The equipment had originally cost $225,000 but had a book value of only $137,500 when transferred. On that date, the equipment had a five-year remaining life. Depreciation expense is computed using the straight-line method. Ackerman reported $350,000 in net income in 2018 (not including any investment income) while Brannigan reported $114,500. Ackerman attributed any excess acquisition date fair value to Brannigan's unpatented technology,...

On January 1, 2018, Ackerman sold equipment to Brannigan (a wholly owned subsidiary) for $250,000 in cash. The equipment had originally cost $225,000 but had a book value of only $137,500 when transferred. On that date, the equipment had a five-year remaining life. Depreciation expense is computed using the straight-line method. Ackerman reported $350,000 in net income in 2018 (not including any investment income) while Brannigan reported $114,500. Ackerman attributed any excess acquisition date fair value to Brannigan's unpatented technology,...

Most questions answered within 3 hours.

-

Calculate the pH of each of the following solutions.

0.50 M HBr

3.1×10−4 M KOH

4.2×10−5...

asked 2 hours ago -

For the year ended December 31, Depot Max’s cost of merchandise

sold was $85,600. Inventory at the...

asked 2 hours ago -

Week 10 - Professional Memo Assignment

Professional Memo Assignment

Your mission for this week, should you...

asked 2 hours ago -

Write a Python program that stores the data for each

player on the team, and it...

asked 3 hours ago -

In

the last 3 months, mike never knows when he is going to get his

allowance...

asked 3 hours ago -

Is Ca(OH)2 a Bronsted base, Lewis base, or both? Why?

asked 3 hours ago -

1A- Why don’t voters complain about U.S. tariffs on imported

sugar?

Because sugar is only a...

asked 3 hours ago -

Cash Payback Period

Primera Banco is evaluating two capital investment proposals for

a drive-up ATM kiosk,...

asked 3 hours ago -

Create a button in Swift (Xcode) that will create a charge,

create a charge using Stripe's...

asked 3 hours ago -

The reaction rate of CO and NO2 in the reaction

CO(g) + NO2(g) → CO2(g) +...

asked 3 hours ago -

Imagine that a chemist puts 6.40 mol each of

C3H8 and O2 in a 1.00-L container...

asked 3 hours ago -

How much money should be invested today in order to have $8340

at the end of...

asked 3 hours ago