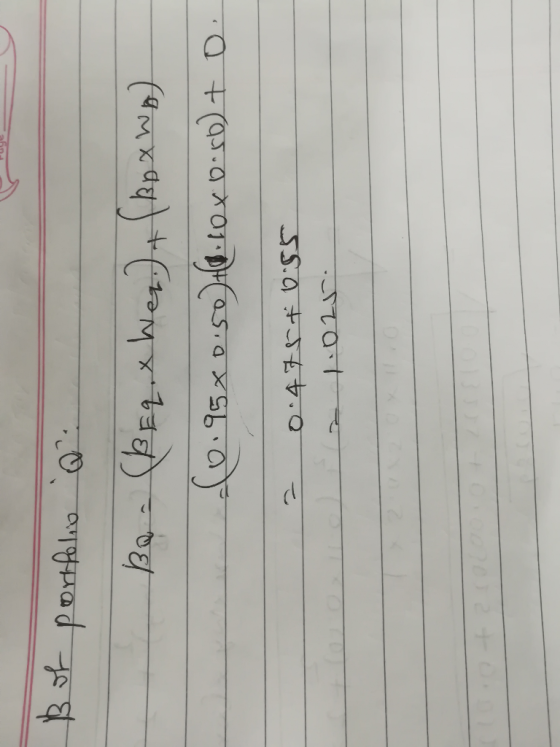

Suppose that the index model for stocks A and B is

estimated from excess returns with the following results:

RA = 2.5% + 0.95RM + eA

RB = –1.8% + 1.10RM + eB

σM = 27%; R-squareA = 0.23; R-squareB = 0.11

Assume you create a portfolio Q, with investment proportions of

0.50 in a risky portfolio P, 0.30 in the market index, and 0.20 in

T-bill. Portfolio P is composed of 60% Stock A and 40% Stock B.

a. What is the standard deviation of portfolio

Q?

b. What is the beta of portfolio Q?

c. What is the "firm-specific" risk of portfolio Q?

d. What is the covariance between the portfolio and the market

index?

Homework Answers

Add Answer to:

Suppose that the index model for stocks A and B is

estimated from excess returns with...

Suppose that the index model for stocks A and B is estimated from excess returns with...

Suppose that the index model for stocks A and B is estimated from excess returns with the following results: RA = 1.8% + 0.75RM + eA RB = –2.0% + 1.10RM + eB σM = 23%; R-squareA = 0.18; R-squareB = 0.10 Assume you create a portfolio Q, with investment proportions of 0.50 in a risky portfolio P, 0.30 in the market index, and 0.20 in T-bill. Portfolio P is composed of 60% Stock A and 40% Stock B. a....

Suppose that the index model for stocks A and B is estimated from excess returns with...

Suppose that the index model for stocks A and B is estimated

from excess returns with the following results:

RA = 3.00% + 1.05RM +

eA

RB = -1.20% + 1.20RM +

eB

σM = 29%;

R-squareA = 0.29;

R-squareB = 0.14

Assume you create portfolio P with investment

proportions of 0.60 in A and 0.40 in B.

a. What is the standard deviation of the portfolio? (Do not round your intermediate calculations. Round your answer to 2 decimal places.)...

Suppose that the index model for stocks A and B is estimated

from excess returns with the following results:

RA = 3.00% + 1.05RM +

eA

RB = -1.20% + 1.20RM +

eB

σM = 29%;

R-squareA = 0.29;

R-squareB = 0.14

Assume you create portfolio P with investment

proportions of 0.60 in A and 0.40 in B.

a. What is the standard deviation of the portfolio? (Do not round your intermediate calculations. Round your answer to 2 decimal places.)...

Suppose that the index model for stocks A and B is estimated from excess returns with...

Suppose that the index model for stocks A and B is estimated from excess returns with the following results: RA = 2.80% + 1.00RM + eA RB = -1.00% + 1.30RM + eB σM = 18%; R-squareA = 0.27; R-squareB = 0.13 Assume you create portfolio P with investment proportions of 0.70 in A and 0.30 in B. a. What is the standard deviation of the portfolio? (Do not round your intermediate calculations. Round your answer to 2 decimal places.)...

Suppose that the index model for stocks A and B is estimated from excess returns with...

Suppose that the index model for stocks A and B is estimated from excess returns with the following results: RA = 4.50% + 1.40RM + eA RB = -2.20% + 1.70RM + eB σM = 24%; R-squareA = 0.30; R-squareB = 0.20 Assume you create portfolio P with investment proportions of 0.60 in A and 0.40 in B. a. What is the standard deviation of the portfolio? (Do not round your intermediate calculations. Round your answer to 2 decimal places.)...

Suppose that the index model for stocks A and B is estimated from excess returns with...

Suppose that the index model for stocks A and B is estimated from excess returns with the following results: RA = 2.5% + 0.60RM + eA RB = -1.5% + 0.7RM + eB σM = 19%; R-squareA = 0.24; R-squareB = 0.18 What is the covariance between each stock and the market index? (Calculate using numbers in decimal form, not percentages. Do not round your intermediate calculations. Round your answers to 3 decimal places.)

Suppose that the index model for stocks A and B is estimated from excess returns with...

Suppose that the index model for stocks A and B is estimated from excess returns with the following results: RA = 3% + 0.7RM + eA & RB = –2% + 1.2RM + eB σM = 20%; R-squareA = 0.20; R-squareB = 0.12 Assume you create portfolio P with investment proportions of 0.60 in A and 0.40 in B. 1. What is the standard deviation of the portfolio? 2. What is the beta of your portfolio? 3. What is the...

Problem 8-10 Suppose that the index model for stocks A and B is estimated from excess...

Problem 8-10 Suppose that the index model for stocks A and B is estimated from excess returns with the following results: RA = 3.2% + 1.1RM + eA RB = –1.4% + 1.25RM + eB σM = 30%; R-squareA = 0.28; R-squareB = 0.12 Break down the variance of each stock to the systematic and firm-specific components. (Do not round intermediate calculations. Calculate using numbers in decimal form, not percentages. Round your answers to 4 decimal places.) Risk for...

I need the Firm-specific and the Covariance please Suppose that the index model for stocks A...

I need the Firm-specific and the Covariance please

Suppose that the index model for stocks A and B is returns with the following resi RA - 1.58% .SSR Re -1.403. B.GR O = 18; R-square -8.25 Assume you create portfolio Pwith Investment proportions of 0.60 in A and 0 40 in B a. What is the standard deviation of the portfolio? (Do not round your intermediate calculations Round your answer places.) Answer is complete and correct 17.58 b. What is...

I need the Firm-specific and the Covariance please

Suppose that the index model for stocks A and B is returns with the following resi RA - 1.58% .SSR Re -1.403. B.GR O = 18; R-square -8.25 Assume you create portfolio Pwith Investment proportions of 0.60 in A and 0 40 in B a. What is the standard deviation of the portfolio? (Do not round your intermediate calculations Round your answer places.) Answer is complete and correct 17.58 b. What is...

Suppose that the index model for stocks A and B is estimated from excess returns with...

Suppose that the index model for stocks A and B is estimated from excess returns with the following results: AA = 1.5% + 0.55AX + A Ag = -1.4% + 0.6A + og # = 18%; A-square a = 0.25; A-squareg = 0.16 What is the covariance between each stock and the market index? (Calculate using numbers in decimal form, not percentages. Do not round your intermediate calculations. Round your answers to 3 decimal places.) Covariance Stock A Stock B

Suppose that the index model for stocks A and B is estimated from excess returns with the following results: AA = 1.5% + 0.55AX + A Ag = -1.4% + 0.6A + og # = 18%; A-square a = 0.25; A-squareg = 0.16 What is the covariance between each stock and the market index? (Calculate using numbers in decimal form, not percentages. Do not round your intermediate calculations. Round your answers to 3 decimal places.) Covariance Stock A Stock B

Suppose that the index model for stocks A and B is estimated from excess returns with...

Suppose that the index model for stocks A and B is estimated from excess returns with the following results: RA - 1.6% + 0.70RM + eA RB = -1.8% + 0.9RM + eB OM - 227; R-square A = 0.20; R-squares - 0.15 What is the covariance between each stock and the market index? (Calculate using numbers in decimal form, not percentages. Do not round your intermediate calculations. Round your answers to 3 decimal places.) Covariance Stock A Stock B

Suppose that the index model for stocks A and B is estimated from excess returns with the following results: RA - 1.6% + 0.70RM + eA RB = -1.8% + 0.9RM + eB OM - 227; R-square A = 0.20; R-squares - 0.15 What is the covariance between each stock and the market index? (Calculate using numbers in decimal form, not percentages. Do not round your intermediate calculations. Round your answers to 3 decimal places.) Covariance Stock A Stock B

Suppose that the index model for stocks A and B is estimated

from excess returns with the following results:

RA = 3.00% + 1.05RM +

eA

RB = -1.20% + 1.20RM +

eB

σM = 29%;

R-squareA = 0.29;

R-squareB = 0.14

Assume you create portfolio P with investment

proportions of 0.60 in A and 0.40 in B.

a. What is the standard deviation of the portfolio? (Do not round your intermediate calculations. Round your answer to 2 decimal places.)...

Suppose that the index model for stocks A and B is estimated

from excess returns with the following results:

RA = 3.00% + 1.05RM +

eA

RB = -1.20% + 1.20RM +

eB

σM = 29%;

R-squareA = 0.29;

R-squareB = 0.14

Assume you create portfolio P with investment

proportions of 0.60 in A and 0.40 in B.

a. What is the standard deviation of the portfolio? (Do not round your intermediate calculations. Round your answer to 2 decimal places.)...

I need the Firm-specific and the Covariance please

Suppose that the index model for stocks A and B is returns with the following resi RA - 1.58% .SSR Re -1.403. B.GR O = 18; R-square -8.25 Assume you create portfolio Pwith Investment proportions of 0.60 in A and 0 40 in B a. What is the standard deviation of the portfolio? (Do not round your intermediate calculations Round your answer places.) Answer is complete and correct 17.58 b. What is...

I need the Firm-specific and the Covariance please

Suppose that the index model for stocks A and B is returns with the following resi RA - 1.58% .SSR Re -1.403. B.GR O = 18; R-square -8.25 Assume you create portfolio Pwith Investment proportions of 0.60 in A and 0 40 in B a. What is the standard deviation of the portfolio? (Do not round your intermediate calculations Round your answer places.) Answer is complete and correct 17.58 b. What is...

Suppose that the index model for stocks A and B is estimated from excess returns with the following results: AA = 1.5% + 0.55AX + A Ag = -1.4% + 0.6A + og # = 18%; A-square a = 0.25; A-squareg = 0.16 What is the covariance between each stock and the market index? (Calculate using numbers in decimal form, not percentages. Do not round your intermediate calculations. Round your answers to 3 decimal places.) Covariance Stock A Stock B

Suppose that the index model for stocks A and B is estimated from excess returns with the following results: AA = 1.5% + 0.55AX + A Ag = -1.4% + 0.6A + og # = 18%; A-square a = 0.25; A-squareg = 0.16 What is the covariance between each stock and the market index? (Calculate using numbers in decimal form, not percentages. Do not round your intermediate calculations. Round your answers to 3 decimal places.) Covariance Stock A Stock B

Suppose that the index model for stocks A and B is estimated from excess returns with the following results: RA - 1.6% + 0.70RM + eA RB = -1.8% + 0.9RM + eB OM - 227; R-square A = 0.20; R-squares - 0.15 What is the covariance between each stock and the market index? (Calculate using numbers in decimal form, not percentages. Do not round your intermediate calculations. Round your answers to 3 decimal places.) Covariance Stock A Stock B

Suppose that the index model for stocks A and B is estimated from excess returns with the following results: RA - 1.6% + 0.70RM + eA RB = -1.8% + 0.9RM + eB OM - 227; R-square A = 0.20; R-squares - 0.15 What is the covariance between each stock and the market index? (Calculate using numbers in decimal form, not percentages. Do not round your intermediate calculations. Round your answers to 3 decimal places.) Covariance Stock A Stock B

Most questions answered within 3 hours.

-

An empty test tube weighs 15.923 grams. Then,

MgCl2•6H2O is added into the test tube. After...

asked 43 minutes ago -

Please answer true or false. Words

cannot be changed or added in to make it true...

asked 42 minutes ago -

(a) A piston at 6.1 atm contains a gas that occupies a volume of

3.5 L....

asked 43 minutes ago -

Assume memory access is 10 units of time and disk access is

10000 units of time....

asked 1 hour ago -

1. Are all good samples random?

2. Magazines often report surveys giving statistics such as “63%...

asked 1 hour ago -

Under all the various types of market structures, firms

must eventually earn some economic profits for...

asked 1 hour ago -

Consider the following fitness regime for a single locus trait

with two co-dominant alleles: w11 =...

asked 1 hour ago -

A large cable company reports the following.

80% of its customers subscribe to its cable TV...

asked 1 hour ago -

Please answer the question in brief.

Discuss the role of ERP in organizations. Are ERP tools...

asked 1 hour ago -

Discuss the pros and cons of collaborative software such

as SameTime. Does it increase productivity? What...

asked 1 hour ago -

Buying your in-laws a gift because it’s expected is

due to the ____________ motive of gift-giving....

asked 1 hour ago -

Calculate the expected value, the variance, and the standard

deviation of the given random variable X....

asked 2 hours ago