Tinkle-Tinkle Glass Company makes glass globe paper weights for desks. The company uses a job-order cost...

Tinkle-Tinkle Glass Company makes glass globe paper weights for desks. The company uses a job-order cost system and predetermined overhead rates to apply manufacturing overhead cost to jobs. The predetermined overhead rate in the Fabrication Department is based on machine hours, and the rate in the Finishing Department is based on direct labor hours. At the beginning of the year, the company’s management made the following estimates for the year:

Department

Fabrication Finishing

Machine hours 84,000 27,000

Direct labor hours 28,000 44,000

Direct material cost $415,000 $214,000

Direct labor cost $300,000 $690,000

Fixed manufacturing overhead cost $800,000 $280,000

Variable manufacturing overhead per machine hour $2.25 --

Variable manufacturing overhead per direct labor hour -- $2.15

Job 25 (the Christmas holiday special) was started on September 1 and completed on September 30. The company’s cost records show the following information concerning the job:

Department

Fabrication Finishing

Machine hours 310 75

Direct labor hours 110 133

Direct materials cost $1,320 $1,050

Direct labor cost $910 1,095

- Compute the predetermined overhead rate used during the year in the Fabrication Department. (Round to two decimal places.) Be careful to use the proper cost driver.

- Compute the predetermined overhead rate used during the year in the Finishing Department. (Round to two decimal places.) Be careful to use the proper cost driver.

- Compute the total overhead cost applied to Job 25 (in dollars and cents).

- What would be the total cost recorded for Job 25? (Round to two decimal places.)

- If Job 25 contained 65 units, what would be the unit product cost? (Round to two decimal places.)

- If it contained 750 units, what would be the unit product cost? (Round to two decimal places.)

- At the end of the year, the records of Tinkle-Tinkle Glass revealed the following actual cost and

operating data for all jobs during the year:

Department

Fabrication Finishing

Machines hours 85,900 30,000

Direct labor hours 32,500 29,000

Direct materials cost $425,000 $163,000

Manufacturing overhead cost $713,000 $288,000

What was the amount of actual overhead in each department at the end of the year? Was it underapplied or overapplied? (You should have a total of four answers for this question.)

Homework Answers

Solution:

1. Predetermined OH rate in the Fabrication Dept. = Total estimated fixed OH costs / Machine hours

= $800,000 / 84,000

= $9.52 (rounded off)

2. Predetermined OH rate in Finishing Dept. = Total estimated fixed OH costs / Direct labor hours

= $280,000 / 44,000

= $6.36 (Rounded off)

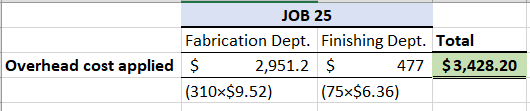

3. Overhead cost applied to Job 25 can be computed as follows:

4. Total cost recorded can be computed as follows:

5. Unit product cost = $7,803.20 / 65 = $120.05

6. Unit product cost = $7,803.20 / 750 = $10.40

7.

Add Answer to:

Tinkle-Tinkle Glass

Company makes glass globe paper weights for desks. The company uses

a job-order cost...

Tinkle-Tinkle Glass Company makes glass globe paper weights for desks. The company uses a job-order cost...

Tinkle-Tinkle Glass Company makes glass globe paper weights for desks. The company uses a job-order cost system and predetermined overhead rates to apply manufacturing overhead cost to jobs. The predetermined overhead rate in the Fabrication Department is based on machine hours, and the rate in the Finishing Department is based on direct labor hours. At the beginning of the year, the company’s management made the following estimates for the year: Department Fabrication Finishing Machine hours 84,000 27,000 Direct...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 7,800 64,000 68,300 3,600...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 7,800 64,000 68,300 3,600...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 8,500 90,000 60,700 1,100...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 8,500 90,000 60,700 1,100...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Department Cutting Finishing Direct labor-hours 7,900 86,000 Machine-hours 64,600 2,600 Total fixed manufacturing overhead cost $ 390,000 $ 410,000 Variable manufacturing overhead per machine-hour $ 3.00...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 6,000 30,000 48,000 5,000...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 6,000 30,000 48,000 5,000...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 7,800 68,000 66,700 3,600...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 7,800 68,000 66,700 3,600...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 6,300 78,000 58,200...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 6,300 78,000 58,200...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 8,000 71,000 69,000 2,500...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 8,000 71,000 69,000 2,500...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 8,300 72,000 66,200 3,900...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 8,300 72,000 66,200 3,900...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 8,500 65,000 62,700 1,200...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 8,500 65,000 62,700 1,200...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 7,800 64,000 68,300 3,600...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 7,800 64,000 68,300 3,600...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 8,500 90,000 60,700 1,100...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 8,500 90,000 60,700 1,100...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 6,000 30,000 48,000 5,000...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 6,000 30,000 48,000 5,000...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 7,800 68,000 66,700 3,600...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 7,800 68,000 66,700 3,600...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 6,300 78,000 58,200...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 6,300 78,000 58,200...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 8,000 71,000 69,000 2,500...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 8,000 71,000 69,000 2,500...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 8,300 72,000 66,200 3,900...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 8,300 72,000 66,200 3,900...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 8,500 65,000 62,700 1,200...

White Company has two departments, Cutting and Finishing. The company uses a job-order costing system and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Department Cutting Finishing 8,500 65,000 62,700 1,200...

Most questions answered within 3 hours.

-

The production capacity for acrylonitrile

(C3H3N) in the United States exceeds 2

million pounds per year....

asked 2 minutes ago -

explain and comment out your answer

43. How many address lines are required to address a...

asked 8 minutes ago -

A sample of 45 observations is selected from a normal

population. The sample mean is 49,...

asked 23 minutes ago -

A construction company is planning to bid on a building

contract. The bid costs the company...

asked 20 minutes ago -

A firm operating in a purely competitive environment is faced

with a market price of $250....

asked 27 minutes ago -

•Let’s say someone claims the average population size is

600 feet squared and the housing authority...

asked 35 minutes ago -

Cynaide is a deadly poison that blocks the last step in the

electron transport chain of...

asked 39 minutes ago -

Your friend tells you that there is a vending machine on campus

that dispenses M&M packs...

asked 54 minutes ago -

What advantages are there to using piperidine rather than

hydroxide as a base?

asked 53 minutes ago -

7. The life of a Freeze Breeze electric fan is normally

distributed with a mean 4...

asked 56 minutes ago -

1. A 751 mL NaCl solution is diluted to a volume of 1.06 L and a...

asked 1 hour ago -

8

A $20,000 face value STRIPS is currently quoted at 38.642 and

has 8 years to...

asked 1 hour ago