Please find the call and put option prices using the information below. You must show your...

Please find the call and put option prices using the information below. You must show your work to receive credit.

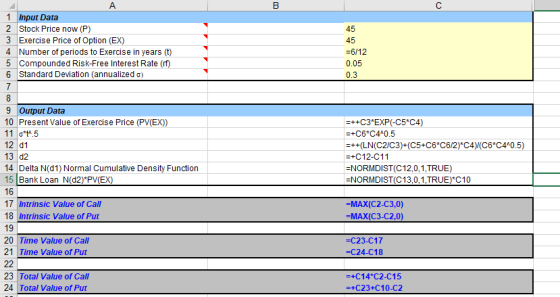

Stock Price=45

Exercise Price=45

Risk-free rate=5%

Time to maturity=6 months

Standard deviation=30%

Homework Answers

Call is 4.3357

Put is 3.2246

Add Answer to:

Please find the call and put option prices using the information

below. You must show your...

(Handwritten step by step please) Please find the call and put option prices using the information...

(Handwritten step by step please) Please find the call and put option prices using the information below. You must show your work to receive credit. Stock Price=45 Exercise Price=45 Risk-free rate=5% Time to maturity=6 months Standard deviation=30%

Please Show all work and formulas What are the prices of a call option and a...

Please Show all work and

formulas

What are the prices of a call option and a put option with the following characteristics? (Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Stock price = $89 Exercise price = $85 __ 4.00% per year, compounded Risk-free rate = continuously Maturity = 4 months Standard _ * = 53% per year deviation Call price Put price

Please Show all work and

formulas

What are the prices of a call option and a put option with the following characteristics? (Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Stock price = $89 Exercise price = $85 __ 4.00% per year, compounded Risk-free rate = continuously Maturity = 4 months Standard _ * = 53% per year deviation Call price Put price

What are the prices of a call option and a put option with the following characteristics?...

What are the prices of a call option and a put option with the following characteristics? (Do not round intermediate calculations and round your final answers to 2 decimal places. (e.g., 32.16)) Stock price = $85 Exercise price = $80 Risk-free rate = 3.80% per year, compounded continuously Maturity = 5 months Standard deviation = 55% per year Call price $ Put price $

What are the prices of a call option and a put option with the following characteristics?...

What are the prices of a call option and a put option with the following characteristics? (Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Stock price = $86 Exercise price = $85 Risk-free rate = 5.00% per year, compounded continuously Maturity = 4 months Standard deviation = 62% per year Call price $ Put price $

What are the prices of a call option and a put option with the following characteristics? Stock p...

What are the prices of a call option and a put option with the following characteristics? Stock price=$64 Exercise price =$60 Risk-free rate=2.7% per year compounded continuously. Maturity=4 months Stander deviation of =62% per year. Call price? put price?

What are the prices of a call option and a put option with the following characteristics?...

What are the prices of a call option and a put option with the following characteristics? (Do not round intermediate calculations and round your answers to 2 decimal places, e.9.,32.16.) Stock price $64 Exercise price $60 Risk-free rate continuously 2.7% per year, compounded Maturity4 months Standard-62% per year deviation Call price Put price

What are the prices of a call option and a put option with the following characteristics? (Do not round intermediate calculations and round your answers to 2 decimal places, e.9.,32.16.) Stock price $64 Exercise price $60 Risk-free rate continuously 2.7% per year, compounded Maturity4 months Standard-62% per year deviation Call price Put price

8. The five factors affecting prices of call and put options Both call and put options...

8. The five factors affecting prices of call and put options Both call and put options are affected by the following five factors: the exercise price, the underlying stock price, the time to expiration, the stock’s standard deviation, and the risk-free rate. However, the direction of the effects on call and put options could be different. Use the following table to identify whether each statement describes put options or call options: Statement Put Option Call Option 1. An increase in...

What are the deltas of a call option and a put option with the following characteristics?...

What are the deltas of a call option and a put option with the following characteristics? (A negative answer should be indicated by a minus sign. Do not round intermediate calculations and round your answers to 4 decimal places, e.g., 32.1616.) Stock price = $49 Exercise price = $45 Risk-free rate = 3.2% per year, compounded continuously Maturity = 8 months Standard deviation = 54% per year Call option delta __________ Put option delta __________

What are the deltas of a call option and a put option with the following characteristics?...

What are the deltas of a call option and a put option with the following characteristics? (Negative amount should be indicated by a minus sign. Do not round intermediate calculations and round your final answers to 4 decimal places. (e.g., 32.1616)) Stock price = $49 Exercise price = $45 Risk-free rate = 3.20% per year, compounded continuously Maturity = 8 months Standard deviation = 54% per year Call option delta Put option delta

5. We have we have the following information for a call and a put option on...

5. We have we have the following information for a call and a put option on XYZ stock. Exercise price: $100 Call option price: $7 Put option price: $5 Risk-free rate: 8% Current market price of XYZ: $97 Time to maturity: 0.5 years Calculate the mispricing and show the arbitrage process if stock price closes at 80

5. We have we have the following information for a call and a put option on XYZ stock. Exercise price: $100 Call option price: $7 Put option price: $5 Risk-free rate: 8% Current market price of XYZ: $97 Time to maturity: 0.5 years Calculate the mispricing and show the arbitrage process if stock price closes at 80

Please Show all work and

formulas

What are the prices of a call option and a put option with the following characteristics? (Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Stock price = $89 Exercise price = $85 __ 4.00% per year, compounded Risk-free rate = continuously Maturity = 4 months Standard _ * = 53% per year deviation Call price Put price

Please Show all work and

formulas

What are the prices of a call option and a put option with the following characteristics? (Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Stock price = $89 Exercise price = $85 __ 4.00% per year, compounded Risk-free rate = continuously Maturity = 4 months Standard _ * = 53% per year deviation Call price Put price

What are the prices of a call option and a put option with the following characteristics? (Do not round intermediate calculations and round your answers to 2 decimal places, e.9.,32.16.) Stock price $64 Exercise price $60 Risk-free rate continuously 2.7% per year, compounded Maturity4 months Standard-62% per year deviation Call price Put price

What are the prices of a call option and a put option with the following characteristics? (Do not round intermediate calculations and round your answers to 2 decimal places, e.9.,32.16.) Stock price $64 Exercise price $60 Risk-free rate continuously 2.7% per year, compounded Maturity4 months Standard-62% per year deviation Call price Put price

5. We have we have the following information for a call and a put option on XYZ stock. Exercise price: $100 Call option price: $7 Put option price: $5 Risk-free rate: 8% Current market price of XYZ: $97 Time to maturity: 0.5 years Calculate the mispricing and show the arbitrage process if stock price closes at 80

5. We have we have the following information for a call and a put option on XYZ stock. Exercise price: $100 Call option price: $7 Put option price: $5 Risk-free rate: 8% Current market price of XYZ: $97 Time to maturity: 0.5 years Calculate the mispricing and show the arbitrage process if stock price closes at 80

Most questions answered within 3 hours.

-

Using Python:

A Prime number is an integer greater than 1 that cannot be

formed by...

asked 18 minutes ago -

Read about Cokes strategy in Africa in the article below and

discuss the ethics of selling...

asked 5 minutes ago -

What made of a 40.0% NaOH solution should be diluted to 1.00 L

with water to...

asked 6 minutes ago -

Draw and describe the results of the Meselson-Stahl experiments

showing that DNA replication followed the Semi-conservative...

asked 11 minutes ago -

Deeply Explain the Following Web Development Softwares Along

With the Reasons to Choose them For Development....

asked 8 minutes ago -

essay question: why was Hurricane Katrina so devastating? How

and why did the levees break in...

asked 13 minutes ago -

Why might it be necessary to reduce consumer spending in order

to attain faster economic growth?...

asked 22 minutes ago -

Express your answer with the appropriate units.

1. How many milliliters of oxygen gas at STP...

asked 28 minutes ago -

A

solution is prepared by mixing 0.12L of 0.11 M sodium chloride with

0.26 L of...

asked 29 minutes ago -

Difference between follicle and egg.

Where exactly are LH and FSH located on the ovaries?

What...

asked 30 minutes ago -

D8AC:

Discuss in 500 words or more why Oracle 12c has introduced two

new roles –...

asked 30 minutes ago -

1) Who is a Hispanic consumer?

2) Who is a Latin consumer?

3) Are Hispanic and...

asked 48 minutes ago