![Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, No](http://img.homeworklib.com/questions/e82dbbb0-731d-11ea-98cc-7700ef2e2349.png?x-oss-process=image/resize,w_560)

Homework Answers

Add Answer to:

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen,...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen,...

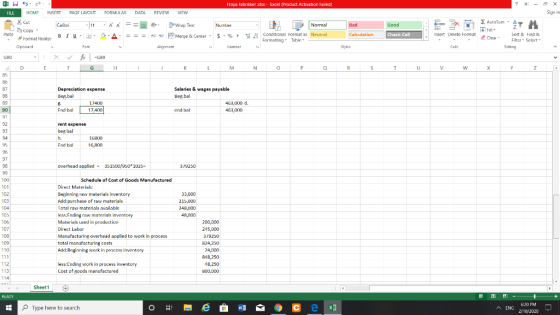

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen,...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $349,800 of manufacturing overhead for an estimated allocation base of 1,060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $349,800 of manufacturing overhead for an estimated allocation base of 1,060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen,...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen,...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $349.800 of manufacturing overhead for an estimated allocation base of 1.060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $349.800 of manufacturing overhead for an estimated allocation base of 1.060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Problem 3-15 Journal Entries; T-Accounts;...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements

[LO3-1, LO3-2, LO3-3, LO3-4]

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements

[LO3-1, LO3-2, LO3-3, LO3-4]

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] points Froya Fabrikker A/S of...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] points Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours....

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] points Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours....

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $374,000 of manufacturing overhead for an estimated allocation base of 1,100 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $374,000 of manufacturing overhead for an estimated allocation base of 1,100 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen,...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oll fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $329,000 of manufacturing overhead for an estimated allocation base of 940 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oll fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $329,000 of manufacturing overhead for an estimated allocation base of 940 direct labor-hours. The...

1. Prepare journal entries to record the preceding transactions. 2. Post your entries to T-accounts. (Don’t...

1. Prepare journal entries to record the preceding

transactions.

2. Post your entries to T-accounts. (Don’t forget to enter the

beginning inventory balances above.)

3. Prepare a schedule of cost of goods manufactured.

4A. Prepare a journal entry to close any balance in the

Manufacturing Overhead account to Cost of Goods Sold.

4B. Prepare a schedule of cost of goods sold.

5. Prepare an income statement for the year.

Froya Fabrikker A/S of Bergen, Norway, is a small company that...

1. Prepare journal entries to record the preceding

transactions.

2. Post your entries to T-accounts. (Don’t forget to enter the

beginning inventory balances above.)

3. Prepare a schedule of cost of goods manufactured.

4A. Prepare a journal entry to close any balance in the

Manufacturing Overhead account to Cost of Goods Sold.

4B. Prepare a schedule of cost of goods sold.

5. Prepare an income statement for the year.

Froya Fabrikker A/S of Bergen, Norway, is a small company that...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $336,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $336,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $349,800 of manufacturing overhead for an estimated allocation base of 1,060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $349,800 of manufacturing overhead for an estimated allocation base of 1,060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $349.800 of manufacturing overhead for an estimated allocation base of 1.060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $349.800 of manufacturing overhead for an estimated allocation base of 1.060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements

[LO3-1, LO3-2, LO3-3, LO3-4]

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements

[LO3-1, LO3-2, LO3-3, LO3-4]

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] points Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours....

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] points Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours....

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $374,000 of manufacturing overhead for an estimated allocation base of 1,100 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $374,000 of manufacturing overhead for an estimated allocation base of 1,100 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oll fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $329,000 of manufacturing overhead for an estimated allocation base of 940 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oll fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $329,000 of manufacturing overhead for an estimated allocation base of 940 direct labor-hours. The...

1. Prepare journal entries to record the preceding

transactions.

2. Post your entries to T-accounts. (Don’t forget to enter the

beginning inventory balances above.)

3. Prepare a schedule of cost of goods manufactured.

4A. Prepare a journal entry to close any balance in the

Manufacturing Overhead account to Cost of Goods Sold.

4B. Prepare a schedule of cost of goods sold.

5. Prepare an income statement for the year.

Froya Fabrikker A/S of Bergen, Norway, is a small company that...

1. Prepare journal entries to record the preceding

transactions.

2. Post your entries to T-accounts. (Don’t forget to enter the

beginning inventory balances above.)

3. Prepare a schedule of cost of goods manufactured.

4A. Prepare a journal entry to close any balance in the

Manufacturing Overhead account to Cost of Goods Sold.

4B. Prepare a schedule of cost of goods sold.

5. Prepare an income statement for the year.

Froya Fabrikker A/S of Bergen, Norway, is a small company that...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $336,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $336,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Most questions answered within 3 hours.

-

26) Briefly describe, using words or simple diagrams, the

chemiosmotic theory for coupling oxidation to phosphorylation...

asked 1 hour ago -

Suppose that XX is a random variable with mean 16 and standard

deviation 5 . Also...

asked 2 hours ago -

Calculate the number density of argon gas at a temperature of

24C and a pressure of...

asked 5 hours ago -

Alternative

Classification

How to Estimate

Probabilities from Data? ( For continuous Attributes)

And How to generate...

asked 5 hours ago -

An explosion breaks a 20.0-kg object into three parts. The

object is initially moving at a...

asked 6 hours ago -

Calculate the approximate number of residues of Rubisco, which

is involved in carbon fixation in plants,...

asked 7 hours ago -

Other decisions about scientific claims can have a much broader

impact.ENERGYarrow-10x10.png, environment, health, security - all...

asked 8 hours ago -

I need to write a research paper and work cited about this

topic: The United States...

asked 9 hours ago -

Hello! I was wondering if I could have some help?

If the vapor pressure of carvone...

asked 9 hours ago -

An economist wants to estimate the mean per capita income (in

thousands of dollars) for a...

asked 9 hours ago -

What would be the input/output characteristic of a circuit

obtained by putting two of your 2's-complementers...

asked 9 hours ago -

In Drosophila, the transition from the syncytial blastoderm

stage to the cellular blastoderm stage is a...

asked 10 hours ago