Homework Answers

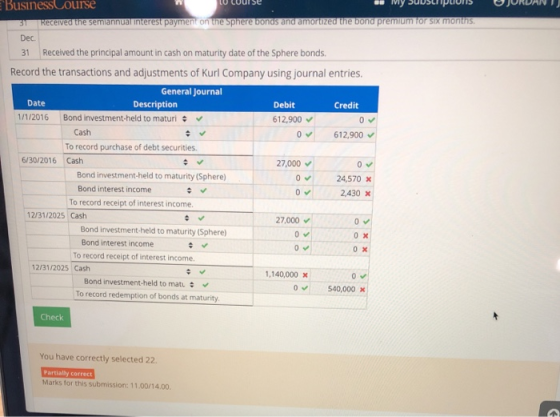

| Date | Particular | Debit | Credit |

|---|---|---|---|

| 1/1/2016 | Bond Investment - held to maturity | $ 612,900 | |

| To Cash | $ 612,900 | ||

| (To record purchase of debt securities) | |||

| 06/30/2016 | Cash | $ 27,000 | |

| To Bond Investment - held to maturity | $ 645 | ||

| To Bond Interest Income | $ 26,355 | ||

| (To record receipt of interest income) | |||

| 12/31/2025 | Cash | $ 27,000 | |

| To Bond Investment - held to maturity | $ 645 | ||

| To Bond Interest Income | $ 26,355 | ||

| (To record receipt of interest income) | |||

| 12/31/2025 | Bond Investment - held to maturity | $ 600,000 | |

| To Cash | $ 600,000 | ||

| (To record redemption of bonds at maturity) |

Add Answer to:

Accounting for Debt Securities- Held-to-Maturity

Kurl Company had the following transactuons and adjustments

related to a...

Accounting for Debt Securities–Available-for-Sale Hilyn Company had the following transactions and adjustments related to a bond...

Accounting for Debt Securities–Available-for-Sale Hilyn Company had the following transactions and adjustments related to a bond investment: 2016 Jan. Purchased $800,000 face value of Cynad, Inc.'s 9 percent bonds at 99 plus a brokerage commission of $1,400. The bonds pay interest on June 30 and December 31 and mature in 15 years. Hilyn does 1 not expect to sell the bonds in the near future, nor does it intend to hold the bonds to maturity. June 30 Received the semiannual...

Accounting for Debt Securities–Available-for-Sale Hilyn Company had the following transactions and adjustments related to a bond investment: 2016 Jan. Purchased $800,000 face value of Cynad, Inc.'s 9 percent bonds at 99 plus a brokerage commission of $1,400. The bonds pay interest on June 30 and December 31 and mature in 15 years. Hilyn does 1 not expect to sell the bonds in the near future, nor does it intend to hold the bonds to maturity. June 30 Received the semiannual...

Accounting for Debt Securities—Trading Gressens Company had the following transactions and adjustments related to a bon...

Accounting for Debt Securities—Trading Gressens Company had the following transactions and adjustments related to a bond investment: 2016 Oct. Purchased $500,000 face value of Skyline, Inc.'s 7 percent bonds at 97 plus a brokerage commission of $1,000. The bonds pay interest on September 30 and March 31 and mature in 20 years. Gressens 1 expects to sell the bonds in the near future. Dec. 31 Made the adjusting entry to record interest earned on investment in the Skyline bonds. Dec....

Accounting for Debt Securities—Trading Gressens Company had the following transactions and adjustments related to a bond investment: 2016 Oct. Purchased $500,000 face value of Skyline, Inc.'s 7 percent bonds at 97 plus a brokerage commission of $1,000. The bonds pay interest on September 30 and March 31 and mature in 20 years. Gressens 1 expects to sell the bonds in the near future. Dec. 31 Made the adjusting entry to record interest earned on investment in the Skyline bonds. Dec....

Accounting for Debt Securities—Available-for-Sale Hilo Company had the following transactions and adjustments related to a bond...

Accounting for Debt Securities—Available-for-Sale Hilo Company had the following transactions and adjustments related to a bond investment: 2019 Jan. 1 Purchased $800,000 face value of Cynad, Inc.’s 9 percent bonds at 99 plus a brokerage commission of $1,400. The bonds pay interest on June 30 and December 31 and mature in 20 years. Hilo does not expect to sell the bonds in the near future, nor does it intend to hold the bonds to maturity. June 30 Received the semiannual...

HW 17-7-Debt Securities AS CORRECTED Presented below is an amortization schedue related to the Orlando Magic's...

HW 17-7-Debt Securities AS CORRECTED Presented below is an amortization schedue related to the Orlando Magic's 5 year, $200,000 bond with a 5% interest rate and a 5% yield, purchased on December 31, 2018 for $191,575. Bond Discount Carrying Amount Date Cash Received Interest Revenue Amortization of Bond 12/31/2018 191,575 12/31/2019 10,000 11,495 1,495 193,070 12/31/2020 10,000 11,584 1,584 194,654 12/31/2021 10,000 11,679 1,679 196,333 12/31/2022 10,000 11,780 1,780 198,113 12/31/2023 10,000 11,887 1,887 200,000 Instructions (a) Prepare the journal...

HW 17-7-Debt Securities AS CORRECTED Presented below is an amortization schedue related to the Orlando Magic's 5 year, $200,000 bond with a 5% interest rate and a 5% yield, purchased on December 31, 2018 for $191,575. Bond Discount Carrying Amount Date Cash Received Interest Revenue Amortization of Bond 12/31/2018 191,575 12/31/2019 10,000 11,495 1,495 193,070 12/31/2020 10,000 11,584 1,584 194,654 12/31/2021 10,000 11,679 1,679 196,333 12/31/2022 10,000 11,780 1,780 198,113 12/31/2023 10,000 11,887 1,887 200,000 Instructions (a) Prepare the journal...

In footnotes to its 2016 annual report, Bancfirst Corp. reported that held-to-maturity debt securities with an...

In footnotes to its 2016 annual report, Bancfirst Corp. reported that held-to-maturity debt securities with an amortized cost of $4,365 thousand had an estimated fair value of $4,403 thousand. a. What amount does Bancfirst report on its 2016 balance sheet for these held-to-maturity securities? b. If these debt securities had instead been classified as available-for-sale securities, how would Bancfirst’s pretax income have been affected

Chapter 1 Intercorporate Investments: An Overview Held-to-maturity securities are recorded at amortized cost which approximates fair...

Chapter 1 Intercorporate Investments: An Overview Held-to-maturity securities are recorded at amortized cost which approximates fair market value. The Company evaluates whether the decline in fair value of its investments is other-than-temporary at each quarter-end. This evaluation consists of a review by management, and includes market pri information and maturity dates for the securities held, market and economic trends in the industry and information on the issuer's financial condition and, if applicable, information on the guarantors financial condition. Factors considered...

Chapter 1 Intercorporate Investments: An Overview Held-to-maturity securities are recorded at amortized cost which approximates fair market value. The Company evaluates whether the decline in fair value of its investments is other-than-temporary at each quarter-end. This evaluation consists of a review by management, and includes market pri information and maturity dates for the securities held, market and economic trends in the industry and information on the issuer's financial condition and, if applicable, information on the guarantors financial condition. Factors considered...

Which of the following statement(s) is (are) true about reporting held to maturity securities? I. Investments...

Which of the following statement(s) is (are) true about reporting held to maturity securities? I. Investments in debt securities that are classified as held to maturity are reported at amortized cost. II. Interest revenue on debt securities that are classified as held to maturity are recognized as other comprehensive income. III. The market value of investments in debt securities that are classified as held to maturity must be disclosed. a. I and II b. I and III c. I, II,...

Exercise 15-4 Accounting for short-term held-to-maturity securities LO P2 Prepare journal entries to record the following...

Exercise 15-4 Accounting for short-term held-to-maturity

securities LO P2

Prepare journal entries to record the following transactions

involving the short-term securities investments of Natura Co., all

of which occurred during year 2017.

On June 15, paid $278,000 cash to purchase Remedy’s 90-day

short-term debt securities ($278,000 principal), dated June 15,

that pay 5% interest (categorized as held-to-maturity

securities).

On September 16, received a check from Remedy in payment of the

principal and 90 days' interest on the debt securities purchased...

Exercise 15-4 Accounting for short-term held-to-maturity

securities LO P2

Prepare journal entries to record the following transactions

involving the short-term securities investments of Natura Co., all

of which occurred during year 2017.

On June 15, paid $278,000 cash to purchase Remedy’s 90-day

short-term debt securities ($278,000 principal), dated June 15,

that pay 5% interest (categorized as held-to-maturity

securities).

On September 16, received a check from Remedy in payment of the

principal and 90 days' interest on the debt securities purchased...

On December 31, 2015, ABC Company issued $170,000 par of a 7% interest rate and a...

On December 31, 2015, ABC Company issued $170,000 par of a 7% interest rate and a 4% yield for $192,705, which were purchased by DEF Company. Interest is received yearly on December 31. The effective interest method is used for any premium or discount to be amortized by the investor. Presented below is an amortization schedule prepard by DEF Company related to this debt investment in ABC Company’s bonds. Date Cash Received Interest Revenue Bond Premium Amortization Carrying Amount of...

Exercise 12.2 Securities held-to-maturity: bond investment; effective interest, premium (LO12-1) Mills Corporation acquired as a long-term...

Exercise 12.2 Securities held-to-maturity: bond investment; effective interest, premium (LO12-1) Mills Corporation acquired as a long-term investment $240 million of x bonds, dated July 1. on July 2018. Company management has positive intent and ability to hold the bonds until maturity. The market interest rate (yield was 4% for bonds of similar risk and maturity Mills paid $280 million for the bonds. The company will recewe interest semiannually on June 30 and December 31 As a result of changing market...

Exercise 12.2 Securities held-to-maturity: bond investment; effective interest, premium (LO12-1) Mills Corporation acquired as a long-term investment $240 million of x bonds, dated July 1. on July 2018. Company management has positive intent and ability to hold the bonds until maturity. The market interest rate (yield was 4% for bonds of similar risk and maturity Mills paid $280 million for the bonds. The company will recewe interest semiannually on June 30 and December 31 As a result of changing market...

Accounting for Debt Securities–Available-for-Sale Hilyn Company had the following transactions and adjustments related to a bond investment: 2016 Jan. Purchased $800,000 face value of Cynad, Inc.'s 9 percent bonds at 99 plus a brokerage commission of $1,400. The bonds pay interest on June 30 and December 31 and mature in 15 years. Hilyn does 1 not expect to sell the bonds in the near future, nor does it intend to hold the bonds to maturity. June 30 Received the semiannual...

Accounting for Debt Securities–Available-for-Sale Hilyn Company had the following transactions and adjustments related to a bond investment: 2016 Jan. Purchased $800,000 face value of Cynad, Inc.'s 9 percent bonds at 99 plus a brokerage commission of $1,400. The bonds pay interest on June 30 and December 31 and mature in 15 years. Hilyn does 1 not expect to sell the bonds in the near future, nor does it intend to hold the bonds to maturity. June 30 Received the semiannual...

Accounting for Debt Securities—Trading Gressens Company had the following transactions and adjustments related to a bond investment: 2016 Oct. Purchased $500,000 face value of Skyline, Inc.'s 7 percent bonds at 97 plus a brokerage commission of $1,000. The bonds pay interest on September 30 and March 31 and mature in 20 years. Gressens 1 expects to sell the bonds in the near future. Dec. 31 Made the adjusting entry to record interest earned on investment in the Skyline bonds. Dec....

Accounting for Debt Securities—Trading Gressens Company had the following transactions and adjustments related to a bond investment: 2016 Oct. Purchased $500,000 face value of Skyline, Inc.'s 7 percent bonds at 97 plus a brokerage commission of $1,000. The bonds pay interest on September 30 and March 31 and mature in 20 years. Gressens 1 expects to sell the bonds in the near future. Dec. 31 Made the adjusting entry to record interest earned on investment in the Skyline bonds. Dec....

HW 17-7-Debt Securities AS CORRECTED Presented below is an amortization schedue related to the Orlando Magic's 5 year, $200,000 bond with a 5% interest rate and a 5% yield, purchased on December 31, 2018 for $191,575. Bond Discount Carrying Amount Date Cash Received Interest Revenue Amortization of Bond 12/31/2018 191,575 12/31/2019 10,000 11,495 1,495 193,070 12/31/2020 10,000 11,584 1,584 194,654 12/31/2021 10,000 11,679 1,679 196,333 12/31/2022 10,000 11,780 1,780 198,113 12/31/2023 10,000 11,887 1,887 200,000 Instructions (a) Prepare the journal...

HW 17-7-Debt Securities AS CORRECTED Presented below is an amortization schedue related to the Orlando Magic's 5 year, $200,000 bond with a 5% interest rate and a 5% yield, purchased on December 31, 2018 for $191,575. Bond Discount Carrying Amount Date Cash Received Interest Revenue Amortization of Bond 12/31/2018 191,575 12/31/2019 10,000 11,495 1,495 193,070 12/31/2020 10,000 11,584 1,584 194,654 12/31/2021 10,000 11,679 1,679 196,333 12/31/2022 10,000 11,780 1,780 198,113 12/31/2023 10,000 11,887 1,887 200,000 Instructions (a) Prepare the journal...

Chapter 1 Intercorporate Investments: An Overview Held-to-maturity securities are recorded at amortized cost which approximates fair market value. The Company evaluates whether the decline in fair value of its investments is other-than-temporary at each quarter-end. This evaluation consists of a review by management, and includes market pri information and maturity dates for the securities held, market and economic trends in the industry and information on the issuer's financial condition and, if applicable, information on the guarantors financial condition. Factors considered...

Chapter 1 Intercorporate Investments: An Overview Held-to-maturity securities are recorded at amortized cost which approximates fair market value. The Company evaluates whether the decline in fair value of its investments is other-than-temporary at each quarter-end. This evaluation consists of a review by management, and includes market pri information and maturity dates for the securities held, market and economic trends in the industry and information on the issuer's financial condition and, if applicable, information on the guarantors financial condition. Factors considered...

Exercise 15-4 Accounting for short-term held-to-maturity

securities LO P2

Prepare journal entries to record the following transactions

involving the short-term securities investments of Natura Co., all

of which occurred during year 2017.

On June 15, paid $278,000 cash to purchase Remedy’s 90-day

short-term debt securities ($278,000 principal), dated June 15,

that pay 5% interest (categorized as held-to-maturity

securities).

On September 16, received a check from Remedy in payment of the

principal and 90 days' interest on the debt securities purchased...

Exercise 15-4 Accounting for short-term held-to-maturity

securities LO P2

Prepare journal entries to record the following transactions

involving the short-term securities investments of Natura Co., all

of which occurred during year 2017.

On June 15, paid $278,000 cash to purchase Remedy’s 90-day

short-term debt securities ($278,000 principal), dated June 15,

that pay 5% interest (categorized as held-to-maturity

securities).

On September 16, received a check from Remedy in payment of the

principal and 90 days' interest on the debt securities purchased...

Exercise 12.2 Securities held-to-maturity: bond investment; effective interest, premium (LO12-1) Mills Corporation acquired as a long-term investment $240 million of x bonds, dated July 1. on July 2018. Company management has positive intent and ability to hold the bonds until maturity. The market interest rate (yield was 4% for bonds of similar risk and maturity Mills paid $280 million for the bonds. The company will recewe interest semiannually on June 30 and December 31 As a result of changing market...

Exercise 12.2 Securities held-to-maturity: bond investment; effective interest, premium (LO12-1) Mills Corporation acquired as a long-term investment $240 million of x bonds, dated July 1. on July 2018. Company management has positive intent and ability to hold the bonds until maturity. The market interest rate (yield was 4% for bonds of similar risk and maturity Mills paid $280 million for the bonds. The company will recewe interest semiannually on June 30 and December 31 As a result of changing market...

Most questions answered within 3 hours.

-

4. Without doing any calculations, predict whether the observed

∆T would increase, decrease or remain the...

asked 27 minutes ago -

Based on the range, which of the following sets of scores has

the greatest variability? 3,...

asked 1 hour ago -

Ripples in a pond travel at a velocity of 3 m/s with one peak

passing a...

asked 1 hour ago -

A man stands on the roof of a building of height 13.0 mm and

throws a...

asked 1 hour ago -

The extent to which assets are financed by borrowed funds and

other liabilities is indicated by:...

asked 2 hours ago -

Explain in detail

Germany is the fifth largest economy

explain what goods and services Germany specializes...

asked 2 hours ago -

The density of platinum is 21.45 g/mL. If a cube of platinum

with a mass of...

asked 2 hours ago -

Accounts Receivable

Sales

A/R Posting

Extended Sales Invoice

Packing Slip

Compare invoice to packing slip 2...

asked 2 hours ago -

Michaella, age 23, is a full-time law student and is claimed by

her parents as a...

asked 2 hours ago -

Why are polymers not typically casted into products?

asked 3 hours ago -

When rolling a die 129 times, what is the probability of rolling

a 6 no more...

asked 3 hours ago -

4. A call option currently sells for $7.75. It has a strike

price of $85 and...

asked 3 hours ago