Suppose the market for canola oil is perfectly competitive. There are 1,000 firms in the market,...

Suppose the market for canola oil is perfectly competitive. There are 1,000 firms in the market, each of which have a fixed cost of FC=2 and a marginal cost of MC= 1+Q, where q is quantity produced by an individual firm. Let QS denote the total quantity supplied in the market. The market demand is QD= 15,250-250P

A) Find the market supply equation, that is write QS as a function of price P

B)What is the equilibrium price? What is the equilibrium quantity of canola oil bought and sold? How much profit is a given firm making? Are firms profit maximizing at this equilibrium? Show your calculations?

C) Can you tell if this is a long run equilibrium? If not, how would a long run equilibrium be different?

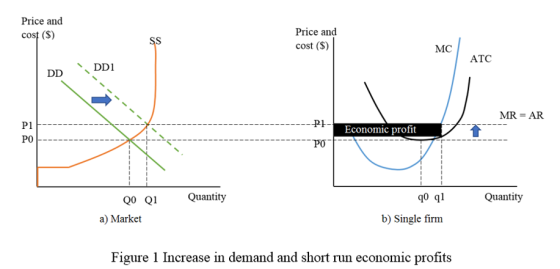

D) How would an increase for demand of canola oil affect the quantity produced by each firm in the short run? How would it affect their profits in the short run? Use a supply and demand diagram to support your answer.

Homework Answers

Each of the 1000 firms has a fixed cost of FC = 2 and a marginal cost of MC= 1+Q, where q is quantity produced by an individual firm. The market demand is QD= 15,250-250P

A) Each firm has a supply equation of q = MC - 1 or q = P - 1. For 1000 firms, market supply is 1000q = Qs = 1000P - 1000.

B) At the equilibrium Qs = Qd

1000P - 1000 = 15250 - 250P

1250P = 16250

P = $13 and so Q = 12000. This gives q = 13 - 1 = 12 units.

Equilibrium price is $13 per unit and the quantity of canola oil bought and sold is 12000 units.

Profit = 13*12 - 2 - 13*12 = -2. Each firm is making a loss of -2.

C) This is not a long run equilibrium because in the long run there would no economic losses (or profit) to any firm.

D) Increase in the demand of canola oil will shifts the demand curve to the right, raising the price and increasing the quantity produced by each firm in the short run. This would reduce their losses or increase their profits in the short run

Add Answer to:

Suppose the market for canola oil is perfectly competitive.

There are 1,000 firms in the market,...

1. Suppose the market for canola oil is perfectly competitive. There are 1.000 firms in the...

1. Suppose the market for canola oil is perfectly competitive. There are 1.000 firms in the market, each of which have a fixed cost of FC = 2 and a marginal cost of MC = 1 + q, where q is the quantity produced by an individual firm. Let Q. denote the total quantity supplied in the market. The market demand for canola oil is given by Qd = 15, 250 - 250P. a) Find the market supply equation, that...

1. Suppose the market for canola oil is perfectly competitive. There are 1.000 firms in the market, each of which have a fixed cost of FC = 2 and a marginal cost of MC = 1 + q, where q is the quantity produced by an individual firm. Let Q. denote the total quantity supplied in the market. The market demand for canola oil is given by Qd = 15, 250 - 250P. a) Find the market supply equation, that...

Please show all work. PART II. Problems 1. Suppose the market for canola oil is perfectly competitive. There are 1....

Please show all work.

PART II. Problems 1. Suppose the market for canola oil is perfectly competitive. There are 1.000 firms in the market, each of which have a fixed cost of FC = 2 and a marginal cost of MC = 1 + q, where q is the quantity produced by an individual firm. Let s denote the total quantity supplied in the market. The market demand for canola oil is given by Qd = 15, 250 - 250P....

Please show all work.

PART II. Problems 1. Suppose the market for canola oil is perfectly competitive. There are 1.000 firms in the market, each of which have a fixed cost of FC = 2 and a marginal cost of MC = 1 + q, where q is the quantity produced by an individual firm. Let s denote the total quantity supplied in the market. The market demand for canola oil is given by Qd = 15, 250 - 250P....

The canola oil industry is perfectly competitive. Every producer has the following total cost function: LTC...

The canola oil industry is perfectly competitive. Every producer has the following total cost function: LTC = 2Q3 – 15Q2 + 40Q, where Q is measured in tons of canola oil. The corresponding marginal cost function is given by LMC = 6Q2 – 30Q + 40. a. In long-run equilibrium, how much will each firm produce? b. What is the long-run equilibrium price? c. Suppose that the market demand for canola oil is given by Q = 999 – 0.25P....

3) There are 1,000 identical perfectly competitive real-estate firms selling office space in Syracuse, NY. The Marginal...

3) There are 1,000 identical perfectly competitive real-estate firms selling office space in Syracuse, NY. The Marginal Cost of producing each square foot of space is constant and equal to $20. There are no fixed costs of production. So the firm’s short-run and long-run cost function is c(q) = 20q. The market demand is Q = 10,000 - 250p. a) What is the equilibrium price and quantity of office space in the real-estate market in the short-run? How much does...

[1] A perfectly competitive aluminum producer is currently producing a quantity where the market price is...

[1] A perfectly competitive aluminum producer is currently producing a quantity where the market price is $0.67 per pound (i.e., 67 cents per pound), average total cost is $0.70, and average variable cost of $0.60 (which corresponds to the minimum point on the average variable cost curve). Would you recommend this firm expand output, contract output, or shut down in the short-run? Provide a graph to illustrate your answer. [2] Suppose the local crawfish market is perfectly competitive, with the...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs for each firm are given by SMC = q + 2 and market demand is given by Qd = 1000-20P (5pts) Calculate the short run equilibrium price and quantity for each firm.. b. (3pts) Suppose each firm has a U-shaped, long-run average cost curve that reaches a minimum of $10. Calculate the long run equilibrium price and the total industry output.. (4pts) What is...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs for each firm are given by SMC = q + 2 and market demand is given by Qd = 1000-20P (5pts) Calculate the short run equilibrium price and quantity for each firm.. b. (3pts) Suppose each firm has a U-shaped, long-run average cost curve that reaches a minimum of $10. Calculate the long run equilibrium price and the total industry output.. (4pts) What is...

Consider a perfectly competitive market comprised of identical firms each facing the following cost function: C(q)...

Consider a perfectly competitive market comprised of identical firms each facing the following cost function: C(q) = 4 +q? where q is the firm-specific level of production of the representative firm. The market demand function is Q(p) = 400 - 4p where Q(p) is the aggregate demand in the market (expressed as function of price) and p is the price a) Derive the firm-specific supply function of the representative firm as a function of price b) Assume there are N...

Consider a perfectly competitive market comprised of identical firms each facing the following cost function: C(q) = 4 +q? where q is the firm-specific level of production of the representative firm. The market demand function is Q(p) = 400 - 4p where Q(p) is the aggregate demand in the market (expressed as function of price) and p is the price a) Derive the firm-specific supply function of the representative firm as a function of price b) Assume there are N...

please answer ASAP please help A perfectly competitive industry is composed of 100 identical firms with...

please answer ASAP

please help

A perfectly competitive industry is composed of 100 identical firms with cost structure: TCVC FC AVC ATC MC a) Complete the preceding Table. b) Assuming that the market price is p-8, what are the quantity produced by each firm and the profit it makes? c) Suppose that the market demand schedule is as follows: P QD 0 700 2 650 4 600 6 550 500 10 450 is the price p = 8 a short-run...

please answer ASAP

please help

A perfectly competitive industry is composed of 100 identical firms with cost structure: TCVC FC AVC ATC MC a) Complete the preceding Table. b) Assuming that the market price is p-8, what are the quantity produced by each firm and the profit it makes? c) Suppose that the market demand schedule is as follows: P QD 0 700 2 650 4 600 6 550 500 10 450 is the price p = 8 a short-run...

1. For a perfectly competitive firm, long-run average cost is: LAC = 300 - 20Q +...

1. For a perfectly competitive firm, long-run average cost is: LAC = 300 - 20Q + 1.8Q2, where Q denotes the firm’s output. The firm’s long-run profit-maximizing price is _____. 2. Demand for a good is given by: QD = 50 – 2P and supply by QS = 1P – 10, where P is the market price of the good. In equilibrium, price would be ___. 3. Demand for a good is given by: QD = 50 – 2P and...

(a) All firms in a perfectly competitive industry face the same long-run average cost curve, AC...

(a) All firms in a perfectly competitive industry face the same long-run average cost curve, AC = 0.05q – 5 + 500/q, and the same long-run marginal cost curve given by MC = 0.1q – 5. The market demand for the product of these firms is QD = 100,000 – 10,000P. i.Calculate the equilibrium price and quantity. ii.Assuming the market is in long-run equilibrium, how many firms will be on the market? (b) Suppose the demand for cotton T-shirts is...

1. Suppose the market for canola oil is perfectly competitive. There are 1.000 firms in the market, each of which have a fixed cost of FC = 2 and a marginal cost of MC = 1 + q, where q is the quantity produced by an individual firm. Let Q. denote the total quantity supplied in the market. The market demand for canola oil is given by Qd = 15, 250 - 250P. a) Find the market supply equation, that...

1. Suppose the market for canola oil is perfectly competitive. There are 1.000 firms in the market, each of which have a fixed cost of FC = 2 and a marginal cost of MC = 1 + q, where q is the quantity produced by an individual firm. Let Q. denote the total quantity supplied in the market. The market demand for canola oil is given by Qd = 15, 250 - 250P. a) Find the market supply equation, that...

Please show all work.

PART II. Problems 1. Suppose the market for canola oil is perfectly competitive. There are 1.000 firms in the market, each of which have a fixed cost of FC = 2 and a marginal cost of MC = 1 + q, where q is the quantity produced by an individual firm. Let s denote the total quantity supplied in the market. The market demand for canola oil is given by Qd = 15, 250 - 250P....

Please show all work.

PART II. Problems 1. Suppose the market for canola oil is perfectly competitive. There are 1.000 firms in the market, each of which have a fixed cost of FC = 2 and a marginal cost of MC = 1 + q, where q is the quantity produced by an individual firm. Let s denote the total quantity supplied in the market. The market demand for canola oil is given by Qd = 15, 250 - 250P....

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs for each firm are given by SMC = q + 2 and market demand is given by Qd = 1000-20P (5pts) Calculate the short run equilibrium price and quantity for each firm.. b. (3pts) Suppose each firm has a U-shaped, long-run average cost curve that reaches a minimum of $10. Calculate the long run equilibrium price and the total industry output.. (4pts) What is...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs for each firm are given by SMC = q + 2 and market demand is given by Qd = 1000-20P (5pts) Calculate the short run equilibrium price and quantity for each firm.. b. (3pts) Suppose each firm has a U-shaped, long-run average cost curve that reaches a minimum of $10. Calculate the long run equilibrium price and the total industry output.. (4pts) What is...

Consider a perfectly competitive market comprised of identical firms each facing the following cost function: C(q) = 4 +q? where q is the firm-specific level of production of the representative firm. The market demand function is Q(p) = 400 - 4p where Q(p) is the aggregate demand in the market (expressed as function of price) and p is the price a) Derive the firm-specific supply function of the representative firm as a function of price b) Assume there are N...

Consider a perfectly competitive market comprised of identical firms each facing the following cost function: C(q) = 4 +q? where q is the firm-specific level of production of the representative firm. The market demand function is Q(p) = 400 - 4p where Q(p) is the aggregate demand in the market (expressed as function of price) and p is the price a) Derive the firm-specific supply function of the representative firm as a function of price b) Assume there are N...

please answer ASAP

please help

A perfectly competitive industry is composed of 100 identical firms with cost structure: TCVC FC AVC ATC MC a) Complete the preceding Table. b) Assuming that the market price is p-8, what are the quantity produced by each firm and the profit it makes? c) Suppose that the market demand schedule is as follows: P QD 0 700 2 650 4 600 6 550 500 10 450 is the price p = 8 a short-run...

please answer ASAP

please help

A perfectly competitive industry is composed of 100 identical firms with cost structure: TCVC FC AVC ATC MC a) Complete the preceding Table. b) Assuming that the market price is p-8, what are the quantity produced by each firm and the profit it makes? c) Suppose that the market demand schedule is as follows: P QD 0 700 2 650 4 600 6 550 500 10 450 is the price p = 8 a short-run...

Most questions answered within 3 hours.

-

Exercise 1. Two players, 1 and 2, take turns choosing numbers; 1

goes first. On his...

asked 10 minutes ago -

Are the following two functions overloaded?

int xyz(int x, int y = 100000);

int xyz(int x,...

asked 18 minutes ago -

An interest rate swap has three years of remaining life.

Payments are exchanged annually. Interest at...

asked 25 minutes ago -

Ensign Johnson is domiciled in Georgia. His wife is domiciled in

New York and moved to...

asked 22 minutes ago -

there are many issues that can be addressed when performing a

RCA. Assuming that there is...

asked 24 minutes ago -

ata pertaining to the postretirement health care benefit plan of

Danielson Delivery Service include the following...

asked 26 minutes ago -

Getting along with the members of your team requires good ____

skills.

a.

authoritative

b.

problem...

asked 33 minutes ago -

During June, Propene Company produced 20,000 chainsaw blades.

The standard quantity of material allowed per unit...

asked 39 minutes ago -

Draw the molecular orbital energy level diagrams and write the

electron configurations of (a) Be2, (b)...

asked 40 minutes ago -

We put a mixture of helium, oxygen and nitrogen gases in a

closed container at 25...

asked 50 minutes ago -

You measure 22 dogs' weights, and find they have a mean weight

of 64 ounces. Assume...

asked 57 minutes ago -

Complete and balance the following methesis reaction in aqueous

solution.

Instructions

• Use proper element capitalization....

asked 1 hour ago