To practice for the hedging alternatives: You plan to visit Geneva, Switzerland in three months to...

To practice for the hedging alternatives:

You plan to visit Geneva, Switzerland in three months to attend

an international business conference.

You expect to incur the total cost of SF 5,000 for lodging, meals

and transportation during your stay. As of today, the spot exchange

rate is $0.60/SF and the three-month forward rate is $0.63/SF. You

can buy the three-month call option on SF with the exercise rate of

$0.64/SF for the premium of $0.05 per SF.

Assume that your expected future spot exchange rate is the same as

the forward rate. The three-month interest rate is 6 percent per

annum in the United States and 4 percent per annum in

Switzerland.

(a) Calculate your expected dollar cost of buying SF5,000 if you

choose to hedge via call option on SF.

(b) Calculate the future dollar cost of meeting this SF obligation

if you decide to hedge using a forward contract.

(c) At what future spot exchange rate will you be indifferent

between the forward and option market hedges?

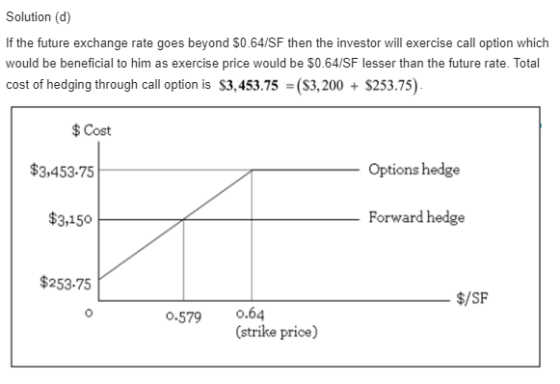

(d) Illustrate the future dollar costs of meeting the SF payable

against the future spot exchange rate under both the options and

forward market hedges.

Homework Answers

I have answered the question below

Please up vote for the same and thanks!!!

Do reach out in the comments for any queries

Answer:

Add Answer to:

To practice for the hedging alternatives:

You plan to visit Geneva, Switzerland in three months to...

Calculate the future dollar cost of meeting this SF obligation if you decide to hedge using...

Calculate the future dollar cost of meeting this SF

obligation if you decide to hedge using money market.

You plan to visit Geneva, Switzerland in three months to attend an international business conference. You expect to incur the total cost of SF 5,000 for lodging, meals and transportation during your stay. As of today, the spot exchange rate is $0.60/SF and the three-month forward rate is $0.63/SF. You can buy the three-month call option on SF with the exercise rate...

Calculate the future dollar cost of meeting this SF

obligation if you decide to hedge using money market.

You plan to visit Geneva, Switzerland in three months to attend an international business conference. You expect to incur the total cost of SF 5,000 for lodging, meals and transportation during your stay. As of today, the spot exchange rate is $0.60/SF and the three-month forward rate is $0.63/SF. You can buy the three-month call option on SF with the exercise rate...

6. Hedging with forwards, options and money market. Princess Cruise Company (PCC) purchased a ship from Mitsubishi Heavy...

6. Hedging with forwards, options and money market. Princess Cruise Company (PCC) purchased a ship from Mitsubishi Heavy Industry for 500 million yen payable in one year. The current spot rate is ¥124/$ and the one year forward rate is ¥110/$. The annual interest rate is 5 percent in Japan and 8 percent in the U.S. PCC can also buy a oneyear call option on yen at the strike price of $0.0081 per yen for a premium of 0.014 cents...

Boeing just signed a contract to sell a Boeing 737 aircraft to British Airways and will...

Boeing just signed a contract to sell a Boeing 737 aircraft to British Airways and will receive £60 million in six months. The current spot exchange rate is $1.3800/£ and the six-month forward rate is $1.4000/£. Boeing can buy a six-month put option on the British pound with an exercise price of $1.3500/£ for a premium of $0.020/£. Currently, the six-month interest rate is 1.880 percent per annum in the United States and 0.700 percent per annum in the UK....

Please answer Problem 6 from International Financial Management (8th Edition) home / study / business /...

Please answer Problem 6 from International Financial Management (8th Edition) home / study / business / financial accounting / financial accounting solutions manuals / international financial management / 8th edition / chapter 8 / problem 6p #6 Princess Cruise Company (PCC) Purchased a Ship for 500 Million Yen Payable in 1 Year. The Current Spot Rate is 124 Yen/$ and the 1 Year Forward Rate 110 Yen/$. The annual interest rate is 5% in Japan and 8% in the United...

Blue Creek Industrial of Atlanta purchased automated machinery from Sydney Manufacturing of Australia for : A$5,000,000...

Blue Creek Industrial of Atlanta purchased automated machinery from Sydney Manufacturing of Australia for : A$5,000,000 with payment due in 6 months. The forecasting department of the firm expects the spot rate in 6 months to be $0.7015/A$ The following quotes are available: Six month investment rate on US$ - 1.20% per annum Loan Rate on US$ - 4.10% per annum Six month investment rate on A$2.25% per annum Loan Rate on A$ - 5.00% per annum Spot exchange rate...

Hopkins Co. transported goods to Switzerland and will receive 3.5 million Swiss francs in six months....

Hopkins Co. transported goods to Switzerland and will receive 3.5 million Swiss francs in six months. It believes the six-month forward rate will be an accurate forecast of the future spot rate. The six-month forward rate of the Swiss franc is $.71. A put option is available with an exercise price of .72 and a premium of $.02. Would Hopkins prefer a put option hedge or no hedge? Explain.

Princess Cruise Company (PCC) purchased a ship from Mitsubishi Heavy Industry for 500 million yen...

Princess Cruise Company (PCC) purchased a ship from Mitsubishi Heavy Industry for 500 million yen payable in one year. The current spot rate is ¥124/$ and the one-year forward rate is 110¥/$. The annual interest rate is in Japan is 5% for lending and 6% for borrowing; and in the United States it is 7% for lending and 8% for borrowing. The WACC is 7%. PCC can also buy a one-year call option on yen at the strike price of...

A U.S.-based importer, Zarb Inc., makes a purchase of crystal glassware from a firm in Switzerland...

A U.S.-based importer, Zarb Inc., makes a purchase of crystal glassware from a firm in Switzerland for 39,960 Swiss francs, or $24,000, at the spot rate of 1.665 francs per dollar. The terms of the purchase are net 90 days, and the U.S. firm wants to cover this trade payable with a forward market hedge to eliminate its exchange rate risk. Suppose the firm completes a forward hedge at the 90-day forward rate of 1.682 francs. If the spot rate...

IBM purchased computer chips from NEC, a Japanese electronics concern, and was billed ¥300 million payable...

IBM purchased computer chips from NEC, a Japanese electronics concern, and was billed ¥300 million payable in 6 months. Currently, the spot exchange rate is ¥110/$ and the six-month forward rate is ¥100/$. The six-month money market interest rate is 2 percent per annum in the U.S. and 1.5 percent per annum in Japan. The management of IBM decided to use the money market hedge to deal with this yen account payable. A. Explain the process of a money market...

On June 1, the 4-month interest rates in Switzerland and the United States were, respectively, 2%...

On June 1, the 4-month interest rates in Switzerland and the United States were, respectively, 2% and 5% per annum with discrete compounding. The spot price of the Swiss franc was $0.8000/CHF. You took a short position of a CHF forward, CHF 100,000, delivery on October 1. One month later on July 1, three-month interest rates in Switzerland and the United States were, respectively, 2.5% and 4.5% per annum with discrete compounding. The spot exchange rate on the Swiss franc...

Calculate the future dollar cost of meeting this SF

obligation if you decide to hedge using money market.

You plan to visit Geneva, Switzerland in three months to attend an international business conference. You expect to incur the total cost of SF 5,000 for lodging, meals and transportation during your stay. As of today, the spot exchange rate is $0.60/SF and the three-month forward rate is $0.63/SF. You can buy the three-month call option on SF with the exercise rate...

Calculate the future dollar cost of meeting this SF

obligation if you decide to hedge using money market.

You plan to visit Geneva, Switzerland in three months to attend an international business conference. You expect to incur the total cost of SF 5,000 for lodging, meals and transportation during your stay. As of today, the spot exchange rate is $0.60/SF and the three-month forward rate is $0.63/SF. You can buy the three-month call option on SF with the exercise rate...

Most questions answered within 3 hours.

-

ORGANIC CHEMISTRY QUESTION 5

PART A--------

Describe a chemical test for the identification of a double...

asked 43 minutes ago -

Both Terence and Tong work at a local actuarial consulting firm

in Des Moines.

Terence arrives...

asked 1 hour ago -

QUESTION 11

. THE RESTING POTENTIAL IS CAUSED BY

.

. A.

. the rotation of...

asked 1 hour ago -

Need them in c++

1. Give the code for the

definition of a node for

the linked implementation of

a tree that contains...

asked 50 minutes ago -

For sputtering-cleaning and sputter-depositing a metal,

would you use an AC or DC plasma? Explain your...

asked 1 hour ago -

Defend ONE of the following statements:

Prices should reflect the value consumers are willing to

pay....

asked 1 hour ago -

A magnet of mass 0.10 kg is dropped from rest and falls

vertically through a 20.0...

asked 1 hour ago -

A friend approaches you about a nutritional product and ask you

if it is worth it....

asked 1 hour ago -

What is bacterial transformation? What are the differences and

similarities between transforming a bacterial cell with...

asked 1 hour ago -

A wire loop 20 cm high is dipped in soap solution and then held

vertically to...

asked 1 hour ago -

OK, now you're all mixed up and you slam into the wall with your

car (total...

asked 1 hour ago -

1. A.Explain why the spread (variance) of a sampling

distribution for estimating a mean would be...

asked 1 hour ago