-

At the end of 2020, its first year of operations, Wesley Co.

prepared a reconciliation between pretax financial income and

taxable income as follows: Pretax financial income $ 520,000 Extra

depreciation taken for tax purposes (1,200,000) Estimated expenses

deductible for taxes when paid 890,000 Taxable income $ 210,000 Use

of the depreciable assets will result in taxable amounts of

$400,000 in each of the next three years. The estimated litigation

expenses of $890,000 will be deductible in 2023 when settlement...

-

Oriole Co. at the end of 2020, its first year of operations,

prepared a reconciliation between pretax financial income and

taxable income as follows:

Pretax financial income

$2505000

Estimated litigation expense

3505000

Extra depreciation for taxes

(5514000)

Taxable income

$ 496000

The estimated litigation expense of $3505000 will be deductible in

2021 when it is expected to be paid. Use of the depreciable assets

will result in taxable amounts of $1838000 in each of the next 3

years. The income tax...

-

Hopkins Co. at the end of 2017, its first year of operations, prepared a reconciliation between pretax financial income and taxable income as follows: Pretax financial income $3,000,000 Estimated litigation expense 4,000,000 Extra depreciation for taxes (6,000,000) Taxable income $3,000,000 $1,000,000 The estimated litigation expense of $4,000,000 will be deductible in 2018 when it is expected to be paid. Use of the depreciable assets will result in taxable amounts of $2,000,000 in each of the next three years. The income...

Hopkins Co. at the end of 2017, its first year of operations, prepared a reconciliation between pretax financial income and taxable income as follows: Pretax financial income $3,000,000 Estimated litigation expense 4,000,000 Extra depreciation for taxes (6,000,000) Taxable income $3,000,000 $1,000,000 The estimated litigation expense of $4,000,000 will be deductible in 2018 when it is expected to be paid. Use of the depreciable assets will result in taxable amounts of $2,000,000 in each of the next three years. The income...

-

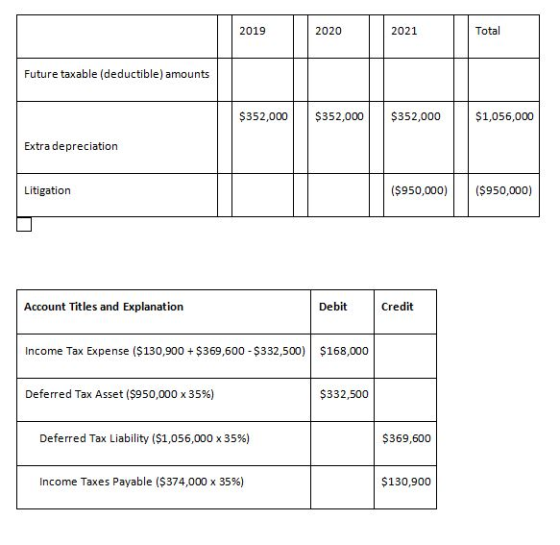

Hopkins Co. at the end of 2020, its first year of operations,

prepared a reconciliation between pretax financial income and

taxable income as follows:

Pretax financial income $3,000,000

Estimated litigation

expense

4,000,000

Extra depreciation for

taxes (6,000,000)

Taxable income $1,000,000

1). The estimated litigation expense of $4,000,000 will be

deductible in 2021 when it is expected to be paid. Use of the

depreciable assets will result in taxable amounts of $2,000,000 in

each of the next three years. The income tax...

-

Crane Co. at the end of 2017, Its first year of operations, prepared a reconciliation between pretax financial Income and taxable Income as follows Pretax Anancial income Estimated litigation expense Extra depreciation for taxes Taxable income $2890000 4440000 (5460000) $ 1870000 expense of $44000ill e deductible in201pectbeps oecable ssets unts d 183200 assets will result in taxable amounts of $1820000 in each of the next 3 years. The income tax rate is 30% for all years. Income taxes payable is...

Crane Co. at the end of 2017, Its first year of operations, prepared a reconciliation between pretax financial Income and taxable Income as follows Pretax Anancial income Estimated litigation expense Extra depreciation for taxes Taxable income $2890000 4440000 (5460000) $ 1870000 expense of $44000ill e deductible in201pectbeps oecable ssets unts d 183200 assets will result in taxable amounts of $1820000 in each of the next 3 years. The income tax rate is 30% for all years. Income taxes payable is...

-

During 2020, Indigo Co.’s first year of operations, the company

reports pretax financial income at $274,700. Indigo’s enacted tax

rate is 45% for 2020 and 20% for all later years. Indigo expects to

have taxable income in each of the next 5 years. The effects on

future tax returns of temporary differences existing at December

31, 2020, are summarized as follows.

Future Years

2021

2022

2023

2024

2025

Total

Future taxable (deductible) amounts:

Installment sales

$29,400

$29,400

$29,400

$88,200

Depreciation...

-

Mathis Co. at the end of 2014, its first year of

operations, prepared a reconciliation between pretax financial

income and taxable income as follows:

Pretax financial

income

$ 500,000

Estimated litigation

expense

1,250,000

Installment

sales

(1,000,000)

Taxable

income

$ 750,000

The estimated litigation expense of $1,250,000 will be

deductible in 2016 when it is expected to be paid. The gross profit

from the installment sales will be realized in the amount of

$500,000 in each of the next two years....

-

The records for Bosch Co. show this data for 2018: Gross profit on instalilment sales recorded on the books was ss00,000. Gross profit from collections of in Life insurance on officers was $4,600 the books was $500,000. Gross profit from collections of Installment recelvables was $360,000. n s used and n nary for $s300,00, Srh-o over a ten-yer life no salvege valua) s used. For tax purposes, MACRS Interest recelved on tax exempt lowa State bonds was $9,800. . The...

The records for Bosch Co. show this data for 2018: Gross profit on instalilment sales recorded on the books was ss00,000. Gross profit from collections of in Life insurance on officers was $4,600 the books was $500,000. Gross profit from collections of Installment recelvables was $360,000. n s used and n nary for $s300,00, Srh-o over a ten-yer life no salvege valua) s used. For tax purposes, MACRS Interest recelved on tax exempt lowa State bonds was $9,800. . The...

-

Question 15 Taxable income and preta financial income would be computations have been prepared til for Grouper Co. except for its treatments of gross profit on installment Sales and estimated costs of warranties. The following income 2016 2017 2018 Taxable income Excess of revenues over expenses (excluding two temporary Terences) Installment gross profit collected Expenditures for warranties Taxable income 5166,000 7,500 (4,800) $168,700 200.000 7.500 92.900 7.500 (4,800 ) $205,700 (4.800) 995,600 2016 2017 2018 Pretax financial income Excess of...

Question 15 Taxable income and preta financial income would be computations have been prepared til for Grouper Co. except for its treatments of gross profit on installment Sales and estimated costs of warranties. The following income 2016 2017 2018 Taxable income Excess of revenues over expenses (excluding two temporary Terences) Installment gross profit collected Expenditures for warranties Taxable income 5166,000 7,500 (4,800) $168,700 200.000 7.500 92.900 7.500 (4,800 ) $205,700 (4.800) 995,600 2016 2017 2018 Pretax financial income Excess of...

-

Problem 19-4 The accounting records of Sweet Inc. show the following data for 2017 (its first year of operations). 1. Life insurance expense on officers was $8,300. 2. Equipment was acquired in early January for $308,000. Straight-line depreciation over a 5-year life is used, with no salvage value. For tax purposes, Sweet used a 30% rate to calculate depreciation. 3. Interest revenue on State of New York bonds totaled $3,600. 4. Product warranties were estimated to be $54,600 in 2017....

Problem 19-4 The accounting records of Sweet Inc. show the following data for 2017 (its first year of operations). 1. Life insurance expense on officers was $8,300. 2. Equipment was acquired in early January for $308,000. Straight-line depreciation over a 5-year life is used, with no salvage value. For tax purposes, Sweet used a 30% rate to calculate depreciation. 3. Interest revenue on State of New York bonds totaled $3,600. 4. Product warranties were estimated to be $54,600 in 2017....

Hopkins Co. at the end of 2017, its first year of operations, prepared a reconciliation between pretax financial income and taxable income as follows: Pretax financial income $3,000,000 Estimated litigation expense 4,000,000 Extra depreciation for taxes (6,000,000) Taxable income $3,000,000 $1,000,000 The estimated litigation expense of $4,000,000 will be deductible in 2018 when it is expected to be paid. Use of the depreciable assets will result in taxable amounts of $2,000,000 in each of the next three years. The income...

Hopkins Co. at the end of 2017, its first year of operations, prepared a reconciliation between pretax financial income and taxable income as follows: Pretax financial income $3,000,000 Estimated litigation expense 4,000,000 Extra depreciation for taxes (6,000,000) Taxable income $3,000,000 $1,000,000 The estimated litigation expense of $4,000,000 will be deductible in 2018 when it is expected to be paid. Use of the depreciable assets will result in taxable amounts of $2,000,000 in each of the next three years. The income...

Crane Co. at the end of 2017, Its first year of operations, prepared a reconciliation between pretax financial Income and taxable Income as follows Pretax Anancial income Estimated litigation expense Extra depreciation for taxes Taxable income $2890000 4440000 (5460000) $ 1870000 expense of $44000ill e deductible in201pectbeps oecable ssets unts d 183200 assets will result in taxable amounts of $1820000 in each of the next 3 years. The income tax rate is 30% for all years. Income taxes payable is...

Crane Co. at the end of 2017, Its first year of operations, prepared a reconciliation between pretax financial Income and taxable Income as follows Pretax Anancial income Estimated litigation expense Extra depreciation for taxes Taxable income $2890000 4440000 (5460000) $ 1870000 expense of $44000ill e deductible in201pectbeps oecable ssets unts d 183200 assets will result in taxable amounts of $1820000 in each of the next 3 years. The income tax rate is 30% for all years. Income taxes payable is...

The records for Bosch Co. show this data for 2018: Gross profit on instalilment sales recorded on the books was ss00,000. Gross profit from collections of in Life insurance on officers was $4,600 the books was $500,000. Gross profit from collections of Installment recelvables was $360,000. n s used and n nary for $s300,00, Srh-o over a ten-yer life no salvege valua) s used. For tax purposes, MACRS Interest recelved on tax exempt lowa State bonds was $9,800. . The...

The records for Bosch Co. show this data for 2018: Gross profit on instalilment sales recorded on the books was ss00,000. Gross profit from collections of in Life insurance on officers was $4,600 the books was $500,000. Gross profit from collections of Installment recelvables was $360,000. n s used and n nary for $s300,00, Srh-o over a ten-yer life no salvege valua) s used. For tax purposes, MACRS Interest recelved on tax exempt lowa State bonds was $9,800. . The...

Question 15 Taxable income and preta financial income would be computations have been prepared til for Grouper Co. except for its treatments of gross profit on installment Sales and estimated costs of warranties. The following income 2016 2017 2018 Taxable income Excess of revenues over expenses (excluding two temporary Terences) Installment gross profit collected Expenditures for warranties Taxable income 5166,000 7,500 (4,800) $168,700 200.000 7.500 92.900 7.500 (4,800 ) $205,700 (4.800) 995,600 2016 2017 2018 Pretax financial income Excess of...

Question 15 Taxable income and preta financial income would be computations have been prepared til for Grouper Co. except for its treatments of gross profit on installment Sales and estimated costs of warranties. The following income 2016 2017 2018 Taxable income Excess of revenues over expenses (excluding two temporary Terences) Installment gross profit collected Expenditures for warranties Taxable income 5166,000 7,500 (4,800) $168,700 200.000 7.500 92.900 7.500 (4,800 ) $205,700 (4.800) 995,600 2016 2017 2018 Pretax financial income Excess of...

Problem 19-4 The accounting records of Sweet Inc. show the following data for 2017 (its first year of operations). 1. Life insurance expense on officers was $8,300. 2. Equipment was acquired in early January for $308,000. Straight-line depreciation over a 5-year life is used, with no salvage value. For tax purposes, Sweet used a 30% rate to calculate depreciation. 3. Interest revenue on State of New York bonds totaled $3,600. 4. Product warranties were estimated to be $54,600 in 2017....

Problem 19-4 The accounting records of Sweet Inc. show the following data for 2017 (its first year of operations). 1. Life insurance expense on officers was $8,300. 2. Equipment was acquired in early January for $308,000. Straight-line depreciation over a 5-year life is used, with no salvage value. For tax purposes, Sweet used a 30% rate to calculate depreciation. 3. Interest revenue on State of New York bonds totaled $3,600. 4. Product warranties were estimated to be $54,600 in 2017....