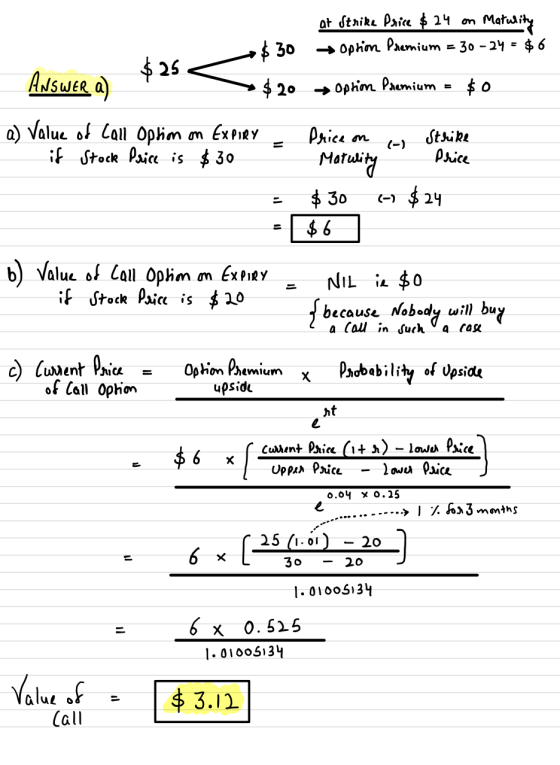

A stock sells for $25. Over the next 3 months you believe the stock will either...

A stock sells for $25. Over the next 3 months you believe the stock will either increase to $30 or decrease to $20.The annual risk-free rate is 4%.Use the binomial option pricing model and find the price of a 3-month call option with a strike of $24.What is the Delta of the option?

Homework Answers

Add Answer to:

A stock sells for $25. Over the next 3 months you believe the

stock will either...

IBM stock currently sells for 49 dollars per share. Over 12 months the price will either...

IBM stock currently sells for 49 dollars per share. Over 12 months the price will either go by 11.5 percent or down by -7.0 percent. The risk-free rate of interest is 4.5 percent continuously compounded. If you are short one call option with strike price 51 and maturity 12 months, what is the present value of a delta-neutral portfolio? 10.649 20.944 17.469 19.114

IBM stock currently sells for 49 dollars per share. Over 12 months the price will either go by 11.5 percent or down by -7.0 percent. The risk-free rate of interest is 4.5 percent continuously compounded. If you are short one call option with strike price 51 and maturity 12 months, what is the present value of a delta-neutral portfolio? 10.649 20.944 17.469 19.114

IBM stock currently sells for 49 dollars per share. Over 12 months the price will either...

IBM stock currently sells for 49 dollars per share. Over 12 months the price will either go up by 11.5 percent or down by -7.0 percent. The risk-free rate of interest is 4.5 percent continuously compounded. If you are short one call option with strike price 51 and maturity 12 months, what is the future value in 12 months of a delta-neutral portfolio? 21.908 18.764 20.533 18.273

IBM stock currently sells for 49 dollars per share. Over 12 months the price will either go up by 11.5 percent or down by -7.0 percent. The risk-free rate of interest is 4.5 percent continuously compounded. If you are short one call option with strike price 51 and maturity 12 months, what is the future value in 12 months of a delta-neutral portfolio? 21.908 18.764 20.533 18.273

Problem1 A stock is currently trading at S $40, during next 6 months stock price will increase to $44 or decrease to $32-6-month risk-free rate is rf-2%. a. [4pts) What positions in stock and T-...

Problem1 A stock is currently trading at S $40, during next 6 months stock price will increase to $44 or decrease to $32-6-month risk-free rate is rf-2%. a. [4pts) What positions in stock and T-bills will you put to replicate the pay off of a European call option with K = $38 and maturing in 6 months. b. 1pt What is the value of this European call option? Problem 2 Suppose that stock price will increase 5% and decrease 5%...

Problem1 A stock is currently trading at S $40, during next 6 months stock price will increase to $44 or decrease to $32-6-month risk-free rate is rf-2%. a. [4pts) What positions in stock and T-bills will you put to replicate the pay off of a European call option with K = $38 and maturing in 6 months. b. 1pt What is the value of this European call option? Problem 2 Suppose that stock price will increase 5% and decrease 5%...

IBM stock currently sells for 49 dollars per share. Over 12 month(s) the price will either...

IBM stock currently sells for 49 dollars per share. Over 12 month(s) the price will either go up by 11.5 percent or down by -7.0 percent. The risk-free rate of interest is 4.5 percent continuously compounded. If you are short one call option with strike price 51 and maturity 12 months how many shares of stock must you buy to establish a delta-neutral position? 0.22425 0.40099 -0.20075 0.62718

IBM stock currently sells for 49 dollars per share. Over 12 month(s) the price will either go up by 11.5 percent or down by -7.0 percent. The risk-free rate of interest is 4.5 percent continuously compounded. If you are short one call option with strike price 51 and maturity 12 months how many shares of stock must you buy to establish a delta-neutral position? 0.22425 0.40099 -0.20075 0.62718

IBM stock currently sells for 49 dollars per share. Over 12 months the price will either...

IBM stock currently sells for 49 dollars per share. Over 12 months the price will either go by 11.5 percent or down by -7.0 percent. The risk-free rate of interest is 4.5 percent continuously compounded. What is the value of a call option with strike price 51 and maturity 12 months? a. 0.12291 b. 1.9353 c. 2.1795 d. 1.3285

The current price of a non-dividend-paying stock is $30. Over the next six months it is...

The current price of a non-dividend-paying stock is $30. Over the next six months it is expected to rise to $36 or fall to $26. Assume that the risk-free rate is 10%. What, to the nearest cent, is the value of a 6-month European call option on the stock with a strike price of $33?

5. Consider a European call option on the stock of XYZ, with a strike price of...

5. Consider a European call option on the stock of XYZ, with a strike price of $25 and two months to expiration. The stock pays continuous dividends at the annual yield rate of 5%. The annual continuously compounded risk free interst rate is 11%. The stock currently trades for $23 per share. Suppose that in two months, the stock will trade for either S18 per share or $29 per share. Use the one-period binomial option pricing model to find today's...

5. Consider a European call option on the stock of XYZ, with a strike price of $25 and two months to expiration. The stock pays continuous dividends at the annual yield rate of 5%. The annual continuously compounded risk free interst rate is 11%. The stock currently trades for $23 per share. Suppose that in two months, the stock will trade for either S18 per share or $29 per share. Use the one-period binomial option pricing model to find today's...

The current price of Estelle Corporation stock is $25. Its stock price will either go up...

The current price of Estelle Corporation stock is $25. Its stock price will either go up by 20% or go down by 20% in one year. The stock pays no dividends. The one-year risk-free interest rate is 6%. Using the binomial model, calculate the price of a one-year call option on Estelle stock with a strike price of $25. The price of a one-year call option on Estelle stock with a strike price of $25 is $ (Round to the...

The current price of Estelle Corporation stock is $25. Its stock price will either go up by 20% or go down by 20% in one year. The stock pays no dividends. The one-year risk-free interest rate is 6%. Using the binomial model, calculate the price of a one-year call option on Estelle stock with a strike price of $25. The price of a one-year call option on Estelle stock with a strike price of $25 is $ (Round to the...

Question 2 11 pts IBM stock currently sells for 49 dollars per share. Over 12 months...

Question 2 11 pts IBM stock currently sells for 49 dollars per share. Over 12 months the price will either go up by 11.5 percent or down by -7.0 percent. The risk-free rate of interest is 4.5 percent continuously compounded. If you are short one call option with strike price 51 and maturity 12 months, what is the future value in 12 months of a delta-neutral portfolio? O21.908 18.764 20.533 18.273

Question 2 11 pts IBM stock currently sells for 49 dollars per share. Over 12 months the price will either go up by 11.5 percent or down by -7.0 percent. The risk-free rate of interest is 4.5 percent continuously compounded. If you are short one call option with strike price 51 and maturity 12 months, what is the future value in 12 months of a delta-neutral portfolio? O21.908 18.764 20.533 18.273

Question 2 11 pts IBM stock currently sells for 49 dollars per share. Over 12 months...

Question 2 11 pts IBM stock currently sells for 49 dollars per share. Over 12 months the price will either go up by 11.5 percent or down by -7.0 percent. The risk-free rate of interest is 4.5 percent continuously compounded. If you are short one call option with strike price 51 and maturity 12 months, what is the future value in 12 months of a delta-neutral portfolio? 21.908 18.764 20.533 18.273

Question 2 11 pts IBM stock currently sells for 49 dollars per share. Over 12 months the price will either go up by 11.5 percent or down by -7.0 percent. The risk-free rate of interest is 4.5 percent continuously compounded. If you are short one call option with strike price 51 and maturity 12 months, what is the future value in 12 months of a delta-neutral portfolio? 21.908 18.764 20.533 18.273

IBM stock currently sells for 49 dollars per share. Over 12 months the price will either go by 11.5 percent or down by -7.0 percent. The risk-free rate of interest is 4.5 percent continuously compounded. If you are short one call option with strike price 51 and maturity 12 months, what is the present value of a delta-neutral portfolio? 10.649 20.944 17.469 19.114

IBM stock currently sells for 49 dollars per share. Over 12 months the price will either go by 11.5 percent or down by -7.0 percent. The risk-free rate of interest is 4.5 percent continuously compounded. If you are short one call option with strike price 51 and maturity 12 months, what is the present value of a delta-neutral portfolio? 10.649 20.944 17.469 19.114

IBM stock currently sells for 49 dollars per share. Over 12 months the price will either go up by 11.5 percent or down by -7.0 percent. The risk-free rate of interest is 4.5 percent continuously compounded. If you are short one call option with strike price 51 and maturity 12 months, what is the future value in 12 months of a delta-neutral portfolio? 21.908 18.764 20.533 18.273

IBM stock currently sells for 49 dollars per share. Over 12 months the price will either go up by 11.5 percent or down by -7.0 percent. The risk-free rate of interest is 4.5 percent continuously compounded. If you are short one call option with strike price 51 and maturity 12 months, what is the future value in 12 months of a delta-neutral portfolio? 21.908 18.764 20.533 18.273

Problem1 A stock is currently trading at S $40, during next 6 months stock price will increase to $44 or decrease to $32-6-month risk-free rate is rf-2%. a. [4pts) What positions in stock and T-bills will you put to replicate the pay off of a European call option with K = $38 and maturing in 6 months. b. 1pt What is the value of this European call option? Problem 2 Suppose that stock price will increase 5% and decrease 5%...

Problem1 A stock is currently trading at S $40, during next 6 months stock price will increase to $44 or decrease to $32-6-month risk-free rate is rf-2%. a. [4pts) What positions in stock and T-bills will you put to replicate the pay off of a European call option with K = $38 and maturing in 6 months. b. 1pt What is the value of this European call option? Problem 2 Suppose that stock price will increase 5% and decrease 5%...

IBM stock currently sells for 49 dollars per share. Over 12 month(s) the price will either go up by 11.5 percent or down by -7.0 percent. The risk-free rate of interest is 4.5 percent continuously compounded. If you are short one call option with strike price 51 and maturity 12 months how many shares of stock must you buy to establish a delta-neutral position? 0.22425 0.40099 -0.20075 0.62718

IBM stock currently sells for 49 dollars per share. Over 12 month(s) the price will either go up by 11.5 percent or down by -7.0 percent. The risk-free rate of interest is 4.5 percent continuously compounded. If you are short one call option with strike price 51 and maturity 12 months how many shares of stock must you buy to establish a delta-neutral position? 0.22425 0.40099 -0.20075 0.62718

5. Consider a European call option on the stock of XYZ, with a strike price of $25 and two months to expiration. The stock pays continuous dividends at the annual yield rate of 5%. The annual continuously compounded risk free interst rate is 11%. The stock currently trades for $23 per share. Suppose that in two months, the stock will trade for either S18 per share or $29 per share. Use the one-period binomial option pricing model to find today's...

5. Consider a European call option on the stock of XYZ, with a strike price of $25 and two months to expiration. The stock pays continuous dividends at the annual yield rate of 5%. The annual continuously compounded risk free interst rate is 11%. The stock currently trades for $23 per share. Suppose that in two months, the stock will trade for either S18 per share or $29 per share. Use the one-period binomial option pricing model to find today's...

The current price of Estelle Corporation stock is $25. Its stock price will either go up by 20% or go down by 20% in one year. The stock pays no dividends. The one-year risk-free interest rate is 6%. Using the binomial model, calculate the price of a one-year call option on Estelle stock with a strike price of $25. The price of a one-year call option on Estelle stock with a strike price of $25 is $ (Round to the...

The current price of Estelle Corporation stock is $25. Its stock price will either go up by 20% or go down by 20% in one year. The stock pays no dividends. The one-year risk-free interest rate is 6%. Using the binomial model, calculate the price of a one-year call option on Estelle stock with a strike price of $25. The price of a one-year call option on Estelle stock with a strike price of $25 is $ (Round to the...

Question 2 11 pts IBM stock currently sells for 49 dollars per share. Over 12 months the price will either go up by 11.5 percent or down by -7.0 percent. The risk-free rate of interest is 4.5 percent continuously compounded. If you are short one call option with strike price 51 and maturity 12 months, what is the future value in 12 months of a delta-neutral portfolio? O21.908 18.764 20.533 18.273

Question 2 11 pts IBM stock currently sells for 49 dollars per share. Over 12 months the price will either go up by 11.5 percent or down by -7.0 percent. The risk-free rate of interest is 4.5 percent continuously compounded. If you are short one call option with strike price 51 and maturity 12 months, what is the future value in 12 months of a delta-neutral portfolio? O21.908 18.764 20.533 18.273

Question 2 11 pts IBM stock currently sells for 49 dollars per share. Over 12 months the price will either go up by 11.5 percent or down by -7.0 percent. The risk-free rate of interest is 4.5 percent continuously compounded. If you are short one call option with strike price 51 and maturity 12 months, what is the future value in 12 months of a delta-neutral portfolio? 21.908 18.764 20.533 18.273

Question 2 11 pts IBM stock currently sells for 49 dollars per share. Over 12 months the price will either go up by 11.5 percent or down by -7.0 percent. The risk-free rate of interest is 4.5 percent continuously compounded. If you are short one call option with strike price 51 and maturity 12 months, what is the future value in 12 months of a delta-neutral portfolio? 21.908 18.764 20.533 18.273

Most questions answered within 3 hours.

-

Angel Corporation has $10,000,000 of

8.0% 25 year bonds dated May 1, 2018 with interest payable...

asked 33 minutes ago -

7.

________ involves individuals trading goods they already have or

providing services in exchange for something...

asked 38 minutes ago -

Share your research problem. What databases did you search as

you gathered evidence to support your...

asked 38 minutes ago -

what process occurs to form microspores and megaspores in flowering

plants?

asked 45 minutes ago -

C++

I need to use the function getData to put in all my data using

arrays....

asked 44 minutes ago -

A block is hung by a string from the inside roof of a van. When

the...

asked 51 minutes ago -

Do you think companies should not go for long term debt in their

capital structure to...

asked 1 hour ago -

I create an address book where the user enters the name, phone

and email in the...

asked 1 hour ago -

The production capacity for acrylonitrile

(C3H3N) in the United States exceeds 2

million pounds per year....

asked 1 hour ago -

explain and comment out your answer

43. How many address lines are required to address a...

asked 1 hour ago -

A sample of 45 observations is selected from a normal

population. The sample mean is 49,...

asked 1 hour ago -

A construction company is planning to bid on a building

contract. The bid costs the company...

asked 1 hour ago