Investment PortfolioYou are an investment manager for Simple Asset Management, acompany that specializes in...

Investment Portfolio

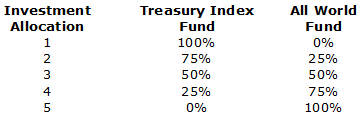

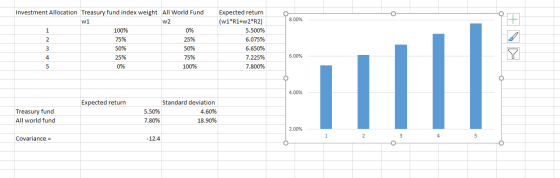

You are an investment manager for Simple Asset Management, a company that specializes in developing simple investment portfolios consisting of no more than three assets such as stocks, bonds, etc., for investors who like to keep things simple. One of your more popular investments is called the All World Fund and is composed of global stocks with good dividend yields. A client is interested in constructing a portfolio that consists of the All World Fund and the Treasury Index Fund, which consists of U.S. Treasury securities (government bonds).

You calculate a 7.8% expected return on the All World Fund with a return standard deviation (a measure of risk) of 18.90%. The expected return of the Treasury Index Fund is 5.50% with a return standard deviation of 4.6%. To analyze the relationship between the two investments, you also calculate the covariance between the two of –12.4.

Which graph below best represents the expected returns for the

following investment allocations?

a. |

b. |

c. |

d. |

Homework Answers

Add Answer to:

Investment PortfolioYou are an investment manager for Simple Asset Management, acompany that specializes in...

Investment Portfolio You are an investment manager for Simple Asset Management, a company that specializes in...

Investment Portfolio You are an investment manager for Simple Asset Management, a company that specializes in developing simple investment portfolios consisting of no more than three assets such as stocks, bonds, etc., for investors who like to keep things simple. One of your more popular investments is called the All World Fund and is composed of global stocks with good dividend yields. A client is interested in constructing a portfolio that consists of the All World Fund and the Treasury...

J. P. Morgan Asset Management publishes information about financial investments. Over the past 10 years, the...

3. P. Morgan Asset Management publishes information about financial investments. Over the past 10 years, the expected retum for the S&P 500 was 5.04 %with a standard deviation of 19.45 %and the expected return over that same period for a Core Bonds fund was 5.78 %with a standard deviation of 2.13 %(J. P. Morgan Asset Management, Guide to the Markets, 1st Quarter, 2012). The publication also reported that the correlation between the Sap 500 and Core Bonds is -0.32. You...

2. You are the risk manager in a major investment bank. The bank's current portfolio consists...

2. You are the risk manager in a major investment bank. The bank's current portfolio consists of U.S. stocks (50%), bonds (20%), and derivatives (30%). The expected returns and standard deviations of these investments are Expected Return Standard Deviation Stocks Bonds Derivatives 13% 17% 25% 25% 9% 50% A trader comes up with an idea about investing in some new emerging markets: the markets of Polynesia, Micronesia, and New Caledonia. These markets have the follow- ing characteristics: 18% Expected Return...

2. You are the risk manager in a major investment bank. The bank's current portfolio consists of U.S. stocks (50%), bonds (20%), and derivatives (30%). The expected returns and standard deviations of these investments are Expected Return Standard Deviation Stocks Bonds Derivatives 13% 17% 25% 25% 9% 50% A trader comes up with an idea about investing in some new emerging markets: the markets of Polynesia, Micronesia, and New Caledonia. These markets have the follow- ing characteristics: 18% Expected Return...

Pinulo retums? 1 0 capital asset pricing model given historical data 2. Consider Table 1. (%)...

Pinulo retums? 1 0 capital asset pricing model given historical data 2. Consider Table 1. (%) 3.77 Table 1 Summary Statistics Alpha, Beta, Expected Return and Variance a/c to the Stocks Sample Single Index Model Covariance Residual and Return Alpha Beta with Market Expected Variance Variance Market (%) (%) Return (%) (%) 3.60 3.59 4.80 Market 4.20 0.00 8.70 (a) Consider Table 1. Using the single index model, calculate beta and alpha for stocks 1 and 2. Interpret your findings....

Pinulo retums? 1 0 capital asset pricing model given historical data 2. Consider Table 1. (%) 3.77 Table 1 Summary Statistics Alpha, Beta, Expected Return and Variance a/c to the Stocks Sample Single Index Model Covariance Residual and Return Alpha Beta with Market Expected Variance Variance Market (%) (%) Return (%) (%) 3.60 3.59 4.80 Market 4.20 0.00 8.70 (a) Consider Table 1. Using the single index model, calculate beta and alpha for stocks 1 and 2. Interpret your findings....

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund (S) 15 % 32 % Bond fund (B) 9 % 23 % The correlation between the fund returns is 0.15. a. What would be the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long- term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Expected Return 15% Stock fund (5) Bond fund (B) Standard Deviation 32% 23% 9% The correlation between the fund returns is 0.15. a. What would be the investment proportions of...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long- term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Expected Return 15% Stock fund (5) Bond fund (B) Standard Deviation 32% 23% 9% The correlation between the fund returns is 0.15. a. What would be the investment proportions of...

Please asnwer all the question 1) Your portfolio consists of $3,000 in ABC stock, $4,500 of...

Please asnwer all the question 1) Your portfolio consists of $3,000 in ABC stock, $4,500 of DEF stock and $2,500 of GHI stock. Expected rates of return are ABC 5%, DEF 12%, and GHI 16%. What is the portfolio expected rate of return? A) 10.9% B) 12.0% C) 11.4% D) 16.0% 2) You are considering investing in a portfolio consisting of 40% Electric General and 60% Buckstar. If the expected rate of return on Electric General is 16% and the...

Stocks A and B each have an expected return of 15%, a standard deviation of 17%,...

Stocks A and B each have an expected return of 15%, a standard deviation of 17%, and a beta of 1.2. The returns on the two stocks have a correlation coefficient of <1.0. You have a portfolio that consists A) The portfolio's beta is less than 12. B) The portfolio's standard deviation is greater than 17%. C) The portfolio's standard deviation is less than 17%. D) The portfolio's expected return is 15%.

Stocks A and B each have an expected return of 15%, a standard deviation of 17%, and a beta of 1.2. The returns on the two stocks have a correlation coefficient of <1.0. You have a portfolio that consists A) The portfolio's beta is less than 12. B) The portfolio's standard deviation is greater than 17%. C) The portfolio's standard deviation is less than 17%. D) The portfolio's expected return is 15%.

A pension fund manager is considering three mutual funds for investment. The first one is a...

A pension fund manager is considering three mutual funds for investment. The first one is a stock fund, the second is a bond fund and the third is a money market fund. The money market fund yields a risk-free return of 5%. The inputs for the risky funds are given in the following table. Fund Expected Return Standard Deviation Stock fund 13% 33% Bond fund 6% 16% The correlation coefficient between the stock and the bond funds is 0.4. a....

State of Nature Probability Investment A Return Investment B Return I 0.25 6% 15% II 0.4...

State of Nature Probability Investment A Return Investment B Return I 0.25 6% 15% II 0.4 9% 12% III 0.35 5% -3% Given the above information on two investments A and B, calculate the statistics below. The correlation coefficient between A and B is 0.6472. Note that since the correlation is given, you do not have to do the long calculation for covariance, just use the shortcut s AB = r ABs As B . Expected Return for Investment A...

2. You are the risk manager in a major investment bank. The bank's current portfolio consists of U.S. stocks (50%), bonds (20%), and derivatives (30%). The expected returns and standard deviations of these investments are Expected Return Standard Deviation Stocks Bonds Derivatives 13% 17% 25% 25% 9% 50% A trader comes up with an idea about investing in some new emerging markets: the markets of Polynesia, Micronesia, and New Caledonia. These markets have the follow- ing characteristics: 18% Expected Return...

2. You are the risk manager in a major investment bank. The bank's current portfolio consists of U.S. stocks (50%), bonds (20%), and derivatives (30%). The expected returns and standard deviations of these investments are Expected Return Standard Deviation Stocks Bonds Derivatives 13% 17% 25% 25% 9% 50% A trader comes up with an idea about investing in some new emerging markets: the markets of Polynesia, Micronesia, and New Caledonia. These markets have the follow- ing characteristics: 18% Expected Return...

Pinulo retums? 1 0 capital asset pricing model given historical data 2. Consider Table 1. (%) 3.77 Table 1 Summary Statistics Alpha, Beta, Expected Return and Variance a/c to the Stocks Sample Single Index Model Covariance Residual and Return Alpha Beta with Market Expected Variance Variance Market (%) (%) Return (%) (%) 3.60 3.59 4.80 Market 4.20 0.00 8.70 (a) Consider Table 1. Using the single index model, calculate beta and alpha for stocks 1 and 2. Interpret your findings....

Pinulo retums? 1 0 capital asset pricing model given historical data 2. Consider Table 1. (%) 3.77 Table 1 Summary Statistics Alpha, Beta, Expected Return and Variance a/c to the Stocks Sample Single Index Model Covariance Residual and Return Alpha Beta with Market Expected Variance Variance Market (%) (%) Return (%) (%) 3.60 3.59 4.80 Market 4.20 0.00 8.70 (a) Consider Table 1. Using the single index model, calculate beta and alpha for stocks 1 and 2. Interpret your findings....

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long- term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Expected Return 15% Stock fund (5) Bond fund (B) Standard Deviation 32% 23% 9% The correlation between the fund returns is 0.15. a. What would be the investment proportions of...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long- term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Expected Return 15% Stock fund (5) Bond fund (B) Standard Deviation 32% 23% 9% The correlation between the fund returns is 0.15. a. What would be the investment proportions of...

Stocks A and B each have an expected return of 15%, a standard deviation of 17%, and a beta of 1.2. The returns on the two stocks have a correlation coefficient of <1.0. You have a portfolio that consists A) The portfolio's beta is less than 12. B) The portfolio's standard deviation is greater than 17%. C) The portfolio's standard deviation is less than 17%. D) The portfolio's expected return is 15%.

Stocks A and B each have an expected return of 15%, a standard deviation of 17%, and a beta of 1.2. The returns on the two stocks have a correlation coefficient of <1.0. You have a portfolio that consists A) The portfolio's beta is less than 12. B) The portfolio's standard deviation is greater than 17%. C) The portfolio's standard deviation is less than 17%. D) The portfolio's expected return is 15%.

Most questions answered within 3 hours.

-

[1] Household statistics include individuals living alone or in

groups in:

A) apartments.

B) military barracks....

asked 15 minutes ago -

Japan’s combination of X and Y

Canada’s combination of X and Y

100x and 0y

50x...

asked 5 minutes ago -

Determine the temperature (in Celsius) at which 1.00 mole of an

ideal gas will have a...

asked 12 minutes ago -

What is the % w/v when 80 mL of a 2.0% solution is mixed with 50...

asked 19 minutes ago -

How can I solve the following using a TI83

Claim: Most adults would erase all of...

asked 31 minutes ago -

Analysis of 3-ethyl-3-buten-2-ol gave C, 72.13%; H, 11.92%.

Calculate the percent deviation of these results from...

asked 28 minutes ago -

Which VALS segment is most likely to have a top of the line

brand new (2015)...

asked 32 minutes ago -

Write a program to score the paper-rock-scissor game. Each of

two users types in either P,R...

asked 52 minutes ago -

Calculate the equillibrium constent K for a redox reaction that

has E°cell = -.98 V at...

asked 1 hour ago -

A concave spherical mirror has a radius of curvature of

magnitude 19.6 cm.

(a) Find the...

asked 1 hour ago -

3. draw a diagram of the magnetic field:

a. around a long straight wire with a...

asked 1 hour ago -

If you titrated 30.0 mL of 0.1 M HCl with 0.1 M NaOH, indicate

the approximate...

asked 1 hour ago