Please solve it by hand or typing, don't use EXCEL

.

Homework Answers

Add Answer to:

Please solve it by hand or typing, don't use EXCEL

.

1. The following data was...

Please solve it by hand or typing, don't use EXCEL. 1. The following data was downloaded...

Please solve it by hand or typing, don't use EXCEL.

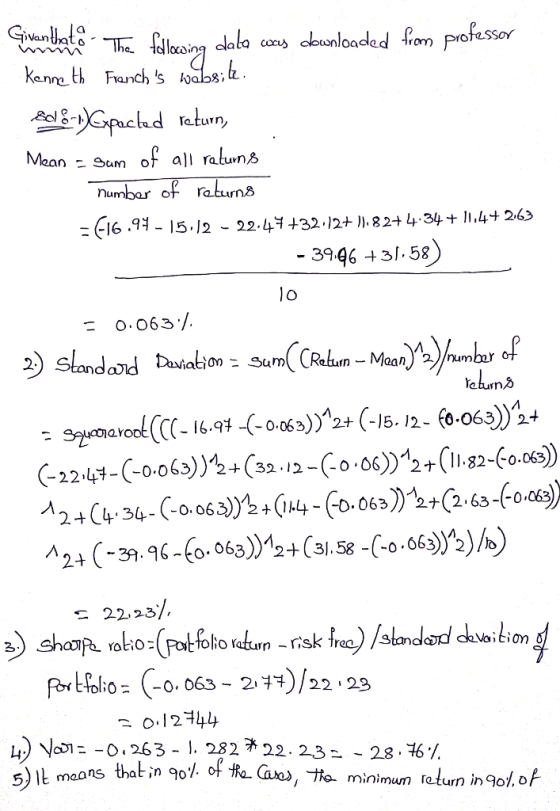

1. The following data was downloaded from Professor Kenneth French's website. The table shows the annual return of the U.S. stock market including NYSE, NASDAQ and Amex over the 10 years. (15pts) Year 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 Return (%) -16.97-15.12-22.47 32.12 11.82 4.34 11.4 263-39 96 3158 1) What would be your expected return of the stock market in 2010 based on the table?...

Please solve it by hand or typing, don't use EXCEL.

1. The following data was downloaded from Professor Kenneth French's website. The table shows the annual return of the U.S. stock market including NYSE, NASDAQ and Amex over the 10 years. (15pts) Year 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 Return (%) -16.97-15.12-22.47 32.12 11.82 4.34 11.4 263-39 96 3158 1) What would be your expected return of the stock market in 2010 based on the table?...

Please solve it by hand or typing, don't use EXCEL. 1. The following data was downloaded...

Please solve it by hand or typing, don't use EXCEL.

1. The following data was downloaded from Professor Kenneth French's website. The table shows the annual return of the U.S. stock market including NYSE, NASDAQ and Amex over the 10 years. (15pts) Year 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 Return (%) -16.97-15.12-22.47 32.12 11.82 4.34 11.4 263-39 96 3158 1) What would be your expected return of the stock market in 2010 based on the table?...

Please solve it by hand or typing, don't use EXCEL.

1. The following data was downloaded from Professor Kenneth French's website. The table shows the annual return of the U.S. stock market including NYSE, NASDAQ and Amex over the 10 years. (15pts) Year 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 Return (%) -16.97-15.12-22.47 32.12 11.82 4.34 11.4 263-39 96 3158 1) What would be your expected return of the stock market in 2010 based on the table?...

Please solve it by hand or typing, don't use EXCEL. 1. The following data was downloaded...

Please solve it by hand or typing, don't use EXCEL.

1. The following data was downloaded from Professor Kenneth French's website. The table shows the annual return of the U.S. stock market including NYSE, NASDAQ and Amex over the 10 years. (15pts) Year 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 Return (%) -16.97-15.12-22.47 32.12 11.82 4.34 11.4 263-39 96 3158 1) What would be your expected return of the stock market in 2010 based on the table?...

Please solve it by hand or typing, don't use EXCEL.

1. The following data was downloaded from Professor Kenneth French's website. The table shows the annual return of the U.S. stock market including NYSE, NASDAQ and Amex over the 10 years. (15pts) Year 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 Return (%) -16.97-15.12-22.47 32.12 11.82 4.34 11.4 263-39 96 3158 1) What would be your expected return of the stock market in 2010 based on the table?...

Please solve it by hand or typing, don't use EXCEL. 1. Suppose you have the expectations...

Please solve it by hand or typing, don't use EXCEL.

1. Suppose you have the expectations of the HPR on stock market as follows: State of Economy Recession Normal growth Expansion Probability 0.2 0.7 0.1 HPR -12% 8% 16% A. Compute the mean of HPR on stocks. (3pts) B. Compute the standard deviation of the HPR on stocks. (5pts)

Please solve it by hand or typing, don't use EXCEL.

1. Suppose you have the expectations of the HPR on stock market as follows: State of Economy Recession Normal growth Expansion Probability 0.2 0.7 0.1 HPR -12% 8% 16% A. Compute the mean of HPR on stocks. (3pts) B. Compute the standard deviation of the HPR on stocks. (5pts)

Please solve it by hand or typing, don't use EXCEL. 1. Suppose you have the expectations...

Please solve it by hand or typing, don't use EXCEL.

1. Suppose you have the expectations of the HPR on stock market as follows: State of Economy Recession Normal growth Expansion Probability 0.2 0.7 0.1 HPR -12% 8% 16% A. Compute the mean of HPR on stocks. (3pts) B. Compute the standard deviation of the HPR on stocks. (5pts)

Please solve it by hand or typing, don't use EXCEL.

1. Suppose you have the expectations of the HPR on stock market as follows: State of Economy Recession Normal growth Expansion Probability 0.2 0.7 0.1 HPR -12% 8% 16% A. Compute the mean of HPR on stocks. (3pts) B. Compute the standard deviation of the HPR on stocks. (5pts)

Please solve it by hand or typing, don't use EXCEL. 1. XYZ stock price and dividends...

Please solve it by hand or typing, don't use EXCEL.

1. XYZ stock price and dividends history are as follows Year Beginning-of-year price Dividend paid at year- $100 $110 $90 $95 end $4 $4 $4 $4 2005 2006 2007 2008 An investor buys three shares of XYZ at the beginning of 2005, buys another two shares at the beginning of 2006, sells one share at the beginning of 2007, and sells all four remaining shares at the beginning of 2008....

Please solve it by hand or typing, don't use EXCEL.

1. XYZ stock price and dividends history are as follows Year Beginning-of-year price Dividend paid at year- $100 $110 $90 $95 end $4 $4 $4 $4 2005 2006 2007 2008 An investor buys three shares of XYZ at the beginning of 2005, buys another two shares at the beginning of 2006, sells one share at the beginning of 2007, and sells all four remaining shares at the beginning of 2008....

Please solve it by hand or typing, don't use EXCEL. 1. XYZ stock price and dividends...

Please solve it by hand or typing, don't use EXCEL.

1. XYZ stock price and dividends history are as follows Year Beginning-of-year price Dividend paid at year- $100 $110 $90 $95 end $4 $4 $4 $4 2005 2006 2007 2008 An investor buys three shares of XYZ at the beginning of 2005, buys another two shares at the beginning of 2006, sells one share at the beginning of 2007, and sells all four remaining shares at the beginning of 2008....

Please solve it by hand or typing, don't use EXCEL.

1. XYZ stock price and dividends history are as follows Year Beginning-of-year price Dividend paid at year- $100 $110 $90 $95 end $4 $4 $4 $4 2005 2006 2007 2008 An investor buys three shares of XYZ at the beginning of 2005, buys another two shares at the beginning of 2006, sells one share at the beginning of 2007, and sells all four remaining shares at the beginning of 2008....

Please solve it by hand or typing, don't use EXCEL.

1. The following data was downloaded from Professor Kenneth French's website. The table shows the annual return of the U.S. stock market including NYSE, NASDAQ and Amex over the 10 years. (15pts) Year 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 Return (%) -16.97-15.12-22.47 32.12 11.82 4.34 11.4 263-39 96 3158 1) What would be your expected return of the stock market in 2010 based on the table?...

Please solve it by hand or typing, don't use EXCEL.

1. The following data was downloaded from Professor Kenneth French's website. The table shows the annual return of the U.S. stock market including NYSE, NASDAQ and Amex over the 10 years. (15pts) Year 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 Return (%) -16.97-15.12-22.47 32.12 11.82 4.34 11.4 263-39 96 3158 1) What would be your expected return of the stock market in 2010 based on the table?...

Please solve it by hand or typing, don't use EXCEL.

1. The following data was downloaded from Professor Kenneth French's website. The table shows the annual return of the U.S. stock market including NYSE, NASDAQ and Amex over the 10 years. (15pts) Year 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 Return (%) -16.97-15.12-22.47 32.12 11.82 4.34 11.4 263-39 96 3158 1) What would be your expected return of the stock market in 2010 based on the table?...

Please solve it by hand or typing, don't use EXCEL.

1. The following data was downloaded from Professor Kenneth French's website. The table shows the annual return of the U.S. stock market including NYSE, NASDAQ and Amex over the 10 years. (15pts) Year 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 Return (%) -16.97-15.12-22.47 32.12 11.82 4.34 11.4 263-39 96 3158 1) What would be your expected return of the stock market in 2010 based on the table?...

Please solve it by hand or typing, don't use EXCEL.

1. The following data was downloaded from Professor Kenneth French's website. The table shows the annual return of the U.S. stock market including NYSE, NASDAQ and Amex over the 10 years. (15pts) Year 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 Return (%) -16.97-15.12-22.47 32.12 11.82 4.34 11.4 263-39 96 3158 1) What would be your expected return of the stock market in 2010 based on the table?...

Please solve it by hand or typing, don't use EXCEL.

1. The following data was downloaded from Professor Kenneth French's website. The table shows the annual return of the U.S. stock market including NYSE, NASDAQ and Amex over the 10 years. (15pts) Year 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 Return (%) -16.97-15.12-22.47 32.12 11.82 4.34 11.4 263-39 96 3158 1) What would be your expected return of the stock market in 2010 based on the table?...

Please solve it by hand or typing, don't use EXCEL.

1. Suppose you have the expectations of the HPR on stock market as follows: State of Economy Recession Normal growth Expansion Probability 0.2 0.7 0.1 HPR -12% 8% 16% A. Compute the mean of HPR on stocks. (3pts) B. Compute the standard deviation of the HPR on stocks. (5pts)

Please solve it by hand or typing, don't use EXCEL.

1. Suppose you have the expectations of the HPR on stock market as follows: State of Economy Recession Normal growth Expansion Probability 0.2 0.7 0.1 HPR -12% 8% 16% A. Compute the mean of HPR on stocks. (3pts) B. Compute the standard deviation of the HPR on stocks. (5pts)

Please solve it by hand or typing, don't use EXCEL.

1. Suppose you have the expectations of the HPR on stock market as follows: State of Economy Recession Normal growth Expansion Probability 0.2 0.7 0.1 HPR -12% 8% 16% A. Compute the mean of HPR on stocks. (3pts) B. Compute the standard deviation of the HPR on stocks. (5pts)

Please solve it by hand or typing, don't use EXCEL.

1. Suppose you have the expectations of the HPR on stock market as follows: State of Economy Recession Normal growth Expansion Probability 0.2 0.7 0.1 HPR -12% 8% 16% A. Compute the mean of HPR on stocks. (3pts) B. Compute the standard deviation of the HPR on stocks. (5pts)

Please solve it by hand or typing, don't use EXCEL.

1. XYZ stock price and dividends history are as follows Year Beginning-of-year price Dividend paid at year- $100 $110 $90 $95 end $4 $4 $4 $4 2005 2006 2007 2008 An investor buys three shares of XYZ at the beginning of 2005, buys another two shares at the beginning of 2006, sells one share at the beginning of 2007, and sells all four remaining shares at the beginning of 2008....

Please solve it by hand or typing, don't use EXCEL.

1. XYZ stock price and dividends history are as follows Year Beginning-of-year price Dividend paid at year- $100 $110 $90 $95 end $4 $4 $4 $4 2005 2006 2007 2008 An investor buys three shares of XYZ at the beginning of 2005, buys another two shares at the beginning of 2006, sells one share at the beginning of 2007, and sells all four remaining shares at the beginning of 2008....

Please solve it by hand or typing, don't use EXCEL.

1. XYZ stock price and dividends history are as follows Year Beginning-of-year price Dividend paid at year- $100 $110 $90 $95 end $4 $4 $4 $4 2005 2006 2007 2008 An investor buys three shares of XYZ at the beginning of 2005, buys another two shares at the beginning of 2006, sells one share at the beginning of 2007, and sells all four remaining shares at the beginning of 2008....

Please solve it by hand or typing, don't use EXCEL.

1. XYZ stock price and dividends history are as follows Year Beginning-of-year price Dividend paid at year- $100 $110 $90 $95 end $4 $4 $4 $4 2005 2006 2007 2008 An investor buys three shares of XYZ at the beginning of 2005, buys another two shares at the beginning of 2006, sells one share at the beginning of 2007, and sells all four remaining shares at the beginning of 2008....

Most questions answered within 3 hours.

-

A circus performer stands on a platform and throws an apple from

a height of 44...

asked 6 minutes ago -

A project has an initial cost of $200,000 and uniform annual

benefits of $35,000. At the...

asked 10 minutes ago -

For a web site, computer program, or smartphone app of

your choice, write five user stories...

asked 19 minutes ago -

Decision Making Technology at UPS

Regardless of the specific decisions a manager makes, the

decision-making process...

asked 28 minutes ago -

Cadherins are transmembrane receptors that have 3

structural domains, each with distinct functions. Describe the

structure...

asked 50 minutes ago -

Oslo Company prepared the following contribution format income

statement based on a sales volume of 1,000...

asked 41 minutes ago -

Suppose you are a distance r from a magnetic dipole. Far from

the dipole, the magnetic...

asked 49 minutes ago -

The potential in a region of space due to a charge distribution

is given by the...

asked 46 minutes ago -

Extension of the shoulder joint is described as

a.

Movement of the humerus straight posteriorly from...

asked 54 minutes ago -

Suppose Nancy Ford buys a brand new Chevy Cruze in September

2019. The car comes up...

asked 55 minutes ago -

Each beaker in a series contains an identical sample of an

acetic acid/sodium acetate buffer. The...

asked 59 minutes ago -

Plato and Aristotle comprise two basic, but different, elements

of the western intellectual tradition. Compare and...

asked 1 hour ago