Suppose the universe of available securities include only two risky stock funds, a and b, and...

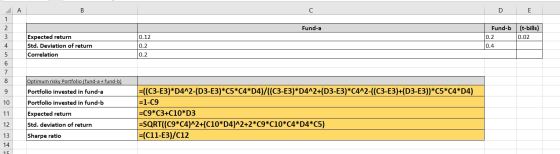

Suppose the universe of available securities include only two risky stock funds, a and b, and T-bills.

() The correlation between fund a and fund b is 0.20 (i.e., = . ).

|

Fund a |

12% |

20% |

|

Fund b |

20% |

40% |

|

T-bills |

2% |

0% |

(2) If you invest in the two risky funds, what is the best “reward-to-volatility ratio” you can achieve? (Hint: Compute the weights and for the optimal risky portfolio ; then use the weights to calculate E(r), ∂, and then finally the Sharpe ratio.

Homework Answers

Please refer to below spreadsheet for calculation and answer. Cell reference also provided.

Cell reference -

Please note:

We can calculate optimal portfolio weight with following formula

where,

B = Bond

S = Stock

E(R) = Expected Return

Rf = risk free rate

= Correlation Bond and

stock

= Correlation Bond and

stock

Hope this will help, please do comment if you need any further explanation. Your feedback would be highly appreciated.

Add Answer to:

Suppose the universe of available securities include only two

risky stock funds, a and b, and...

Suppose the universe of available securities include only two risky stock funds, a and b, and...

Suppose the universe of available securities include only two risky stock funds, a and b, and T-bills. () The correlation between fund a and fund b is 0.20 (i.e., = . ). E(r) ∂ Fund a 12% 20% Fund b 20% 40% T-bills 2% 0% (1) If you invest in the two risky funds, what is the lowest level of portfolio volatility you can achieve? What about the expected return of this portfolio? (Hint: Compute the weights and for the...

1. The universe of available securities includes two risky stock funds, A and B, and T-blls....

1. The universe of available securities includes two risky stock funds, A and B, and T-blls. The data for the universe are as follows Expected Return Standard Deviation A 10% 20% В 30 60 T-bills The correlation coefficient between funds A and B is -0.2. a. Find the optimal risky portfolio, P, and its expected return and standard deviation. b. Find the slope of the CAL supported by T-bills and portfolio P c. How much will an investor with A...

1. The universe of available securities includes two risky stock funds, A and B, and T-blls. The data for the universe are as follows Expected Return Standard Deviation A 10% 20% В 30 60 T-bills The correlation coefficient between funds A and B is -0.2. a. Find the optimal risky portfolio, P, and its expected return and standard deviation. b. Find the slope of the CAL supported by T-bills and portfolio P c. How much will an investor with A...

1. The universe of available securities includes two risky stock funds, A and B and T-bills....

1. The universe of available securities includes two risky stock funds, A and B and T-bills. The data for the universe are as follows: Expected Return Standard Deviation 109 20 Tbilis The correlation coefficient between funds A and B is -0.2. a. Find the optimal risky portfolio, P. and its expected return and standard deviation b. Find the slope of the CAL supported by T-bills and portfolio P. c. How much will an investor with 4-5 invest in funds A...

1. The universe of available securities includes two risky stock funds, A and B and T-bills. The data for the universe are as follows: Expected Return Standard Deviation 109 20 Tbilis The correlation coefficient between funds A and B is -0.2. a. Find the optimal risky portfolio, P. and its expected return and standard deviation b. Find the slope of the CAL supported by T-bills and portfolio P. c. How much will an investor with 4-5 invest in funds A...

You manage a risky portfolio with an expected rate of return of 19% and a standard...

You manage a risky portfolio with an expected rate of return of 19% and a standard deviation of 33%. The T-bill rate is 7%. Your client chooses to invest 80% of a portfolio in your fund and 20% in a T-bill money market fund. What is the reward-to-volatility (Sharpe) ratio (S) of your risky portfolio? Your client’s? (Do not round intermediate calculations. Round your answers to 4 decimal places.) Your reward-to-volatility ratio?________ Clients' reward-to-volatility ratio?_________

You manage a risky portfolio with an expected rate of return of 17% and a standard...

You manage a risky portfolio with an expected rate of return of 17% and a standard deviation of 37%. The T-bill rate is 5%. Your client chooses to invest 80% of a portfolio In your fund and 20% In a T-bill money market fund. What is the reward-to-volatility (Sharpe) ratio (9) of your risky portfolio? Your client's? (Do not round Intermediate calculations. Round your answers to 4 decimal places.) Your reward-to-volatility ratio Client's reward-to-volatility ratio

You manage a risky portfolio with an expected rate of return of 17% and a standard deviation of 37%. The T-bill rate is 5%. Your client chooses to invest 80% of a portfolio In your fund and 20% In a T-bill money market fund. What is the reward-to-volatility (Sharpe) ratio (9) of your risky portfolio? Your client's? (Do not round Intermediate calculations. Round your answers to 4 decimal places.) Your reward-to-volatility ratio Client's reward-to-volatility ratio

The universe of available securities includes two risky stocks A and B, and a risk-free asset....

The universe of available securities includes two risky stocks A and B, and a risk-free asset. The data for the universe are as follows: Assets Expected Return Standard Deviation Stock A 6% 25% Stock B 12% 42% Risk free 5% 0 The correlation coefficient between A and B is -0.2. The investor maximizes a utility function U=E(r)−σ2 (i.e. she has a coefficient of risk aversion equal to 2). Assume that to maximize his utility when there is no available risk-free...

Problem 6-15 You manage a risky portfolio with an expected rate of return of 22% and...

Problem 6-15 You manage a risky portfolio with an expected rate of return of 22% and a standard deviation of 34%. The T-bill rate is 6%. Your client chooses to invest 70% of a portfolio in your fund and 30% in a T-bill money market fund. What is the reward-to-volatility (Sharpe) ratio (S) of your risky portfolio? Your client's? (Do not round intermediate calculations. Round your answers to 4 decimal places.) Your reward-to-volatility ratio Client's reward-to-volatility ratio

Problem 6-15 You manage a risky portfolio with an expected rate of return of 22% and a standard deviation of 34%. The T-bill rate is 6%. Your client chooses to invest 70% of a portfolio in your fund and 30% in a T-bill money market fund. What is the reward-to-volatility (Sharpe) ratio (S) of your risky portfolio? Your client's? (Do not round intermediate calculations. Round your answers to 4 decimal places.) Your reward-to-volatility ratio Client's reward-to-volatility ratio

finance help please 1. Assume that you manage a risky portfolio with an expected rate of...

finance help please

1. Assume that you manage a risky portfolio with an expected rate of return of 18% and a standard deviation of 28%. The T-bill rate is 8%. Your client chooses to invest 70% of a portfolio in your fund and 30% in a T-bill money market fund. a) What is the expected value and standard deviation of the rate of return on his portfolio? b) Suppose that your risky portfolio includes the following investments in the given...

finance help please

1. Assume that you manage a risky portfolio with an expected rate of return of 18% and a standard deviation of 28%. The T-bill rate is 8%. Your client chooses to invest 70% of a portfolio in your fund and 30% in a T-bill money market fund. a) What is the expected value and standard deviation of the rate of return on his portfolio? b) Suppose that your risky portfolio includes the following investments in the given...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.0%. The probability distributions of the risky funds are: (Total 20 points) Expected Return of Market Standard Deviation Stock funds (S) 15% 32% Bond funds (B) 9% 23% The correlation between the fund returns is 0.15. a. Use the formula below to compute the...

A pension fund manager is considering three mutual funds. The first is a stock fund the second is...

A pension fund manager is considering three mutual funds. The first is a stock fund the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of th risky funds are The following data apply to Problems 8-12. Standard Deviation 32% 23 Expected Return 15% Stock fund (S Bond fund (B) The correlation between the fund returns is.15 8. Tabulate and draw...

A pension fund manager is considering three mutual funds. The first is a stock fund the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of th risky funds are The following data apply to Problems 8-12. Standard Deviation 32% 23 Expected Return 15% Stock fund (S Bond fund (B) The correlation between the fund returns is.15 8. Tabulate and draw...

1. The universe of available securities includes two risky stock funds, A and B, and T-blls. The data for the universe are as follows Expected Return Standard Deviation A 10% 20% В 30 60 T-bills The correlation coefficient between funds A and B is -0.2. a. Find the optimal risky portfolio, P, and its expected return and standard deviation. b. Find the slope of the CAL supported by T-bills and portfolio P c. How much will an investor with A...

1. The universe of available securities includes two risky stock funds, A and B, and T-blls. The data for the universe are as follows Expected Return Standard Deviation A 10% 20% В 30 60 T-bills The correlation coefficient between funds A and B is -0.2. a. Find the optimal risky portfolio, P, and its expected return and standard deviation. b. Find the slope of the CAL supported by T-bills and portfolio P c. How much will an investor with A...

1. The universe of available securities includes two risky stock funds, A and B and T-bills. The data for the universe are as follows: Expected Return Standard Deviation 109 20 Tbilis The correlation coefficient between funds A and B is -0.2. a. Find the optimal risky portfolio, P. and its expected return and standard deviation b. Find the slope of the CAL supported by T-bills and portfolio P. c. How much will an investor with 4-5 invest in funds A...

1. The universe of available securities includes two risky stock funds, A and B and T-bills. The data for the universe are as follows: Expected Return Standard Deviation 109 20 Tbilis The correlation coefficient between funds A and B is -0.2. a. Find the optimal risky portfolio, P. and its expected return and standard deviation b. Find the slope of the CAL supported by T-bills and portfolio P. c. How much will an investor with 4-5 invest in funds A...

You manage a risky portfolio with an expected rate of return of 17% and a standard deviation of 37%. The T-bill rate is 5%. Your client chooses to invest 80% of a portfolio In your fund and 20% In a T-bill money market fund. What is the reward-to-volatility (Sharpe) ratio (9) of your risky portfolio? Your client's? (Do not round Intermediate calculations. Round your answers to 4 decimal places.) Your reward-to-volatility ratio Client's reward-to-volatility ratio

You manage a risky portfolio with an expected rate of return of 17% and a standard deviation of 37%. The T-bill rate is 5%. Your client chooses to invest 80% of a portfolio In your fund and 20% In a T-bill money market fund. What is the reward-to-volatility (Sharpe) ratio (9) of your risky portfolio? Your client's? (Do not round Intermediate calculations. Round your answers to 4 decimal places.) Your reward-to-volatility ratio Client's reward-to-volatility ratio

Problem 6-15 You manage a risky portfolio with an expected rate of return of 22% and a standard deviation of 34%. The T-bill rate is 6%. Your client chooses to invest 70% of a portfolio in your fund and 30% in a T-bill money market fund. What is the reward-to-volatility (Sharpe) ratio (S) of your risky portfolio? Your client's? (Do not round intermediate calculations. Round your answers to 4 decimal places.) Your reward-to-volatility ratio Client's reward-to-volatility ratio

Problem 6-15 You manage a risky portfolio with an expected rate of return of 22% and a standard deviation of 34%. The T-bill rate is 6%. Your client chooses to invest 70% of a portfolio in your fund and 30% in a T-bill money market fund. What is the reward-to-volatility (Sharpe) ratio (S) of your risky portfolio? Your client's? (Do not round intermediate calculations. Round your answers to 4 decimal places.) Your reward-to-volatility ratio Client's reward-to-volatility ratio

finance help please

1. Assume that you manage a risky portfolio with an expected rate of return of 18% and a standard deviation of 28%. The T-bill rate is 8%. Your client chooses to invest 70% of a portfolio in your fund and 30% in a T-bill money market fund. a) What is the expected value and standard deviation of the rate of return on his portfolio? b) Suppose that your risky portfolio includes the following investments in the given...

finance help please

1. Assume that you manage a risky portfolio with an expected rate of return of 18% and a standard deviation of 28%. The T-bill rate is 8%. Your client chooses to invest 70% of a portfolio in your fund and 30% in a T-bill money market fund. a) What is the expected value and standard deviation of the rate of return on his portfolio? b) Suppose that your risky portfolio includes the following investments in the given...

A pension fund manager is considering three mutual funds. The first is a stock fund the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of th risky funds are The following data apply to Problems 8-12. Standard Deviation 32% 23 Expected Return 15% Stock fund (S Bond fund (B) The correlation between the fund returns is.15 8. Tabulate and draw...

A pension fund manager is considering three mutual funds. The first is a stock fund the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of th risky funds are The following data apply to Problems 8-12. Standard Deviation 32% 23 Expected Return 15% Stock fund (S Bond fund (B) The correlation between the fund returns is.15 8. Tabulate and draw...

Most questions answered within 3 hours.

-

Briefly discuss the following statements:

2.1 A partner never has the right to claim compensation for...

asked 15 seconds from now -

If a bond has an annual probability of default of 6%, 10% and

12% in years...

asked 8 minutes ago -

Let X be normally distributed with mean μ = 10 and standard

deviation σ = 6....

asked 13 minutes ago -

You're examining some of the tiny printing on one of the newer

twenty-dollar bills. A 1.5...

asked 17 minutes ago -

Discuss several common sources of secondary data coming from

government sources.

asked 20 minutes ago -

This is a basic java program where you convert units using only

loops, control statements and...

asked 21 minutes ago -

A sample survey at a supermarket showed that 204 of 300 shoppers

regularly use cents-off coupons....

asked 1 hour ago -

1. Find the area under the standard normal curve that lies

outside the interval between z=...

asked 37 minutes ago -

In ________ mode, the interpreter reads the contents of a file

that contains Python statements and...

asked 53 minutes ago -

1.

The second-order rate constant for self-reaction of hydroxyl

radicals

2 OH → H2O + O...

asked 43 minutes ago -

What is the most important factor leading to improved resource

efficiency over the long run?

asked 39 minutes ago -

Defend the effectiveness of teamwork in an organization.

(Use no more than 30 words)

asked 41 minutes ago