For all questions, interest (r) and dividend (d) rates are continuously compounded unless specified otherwise. Q2)...

Homework Answers

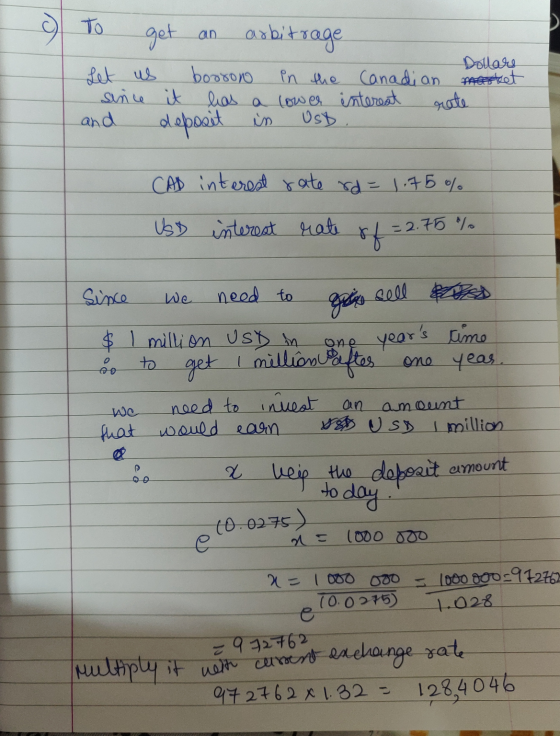

a) Calculating one-year forward rate:

Forward exchange rate = Spot rate X [(1+ domestic interest rate)/(1+ foreign interest rate)]

USD/CAD spot Exchange rate= $ 1.32

CAD Interet rate = 1.75% (continuous compounding)(rd)

USD Interest Rate = 2.75% (continuous compounding)(rf)

Since interest is continuous compounding:

Forward exchange rate = spot rate X (e(rdt))/erft) (note standard value of e= 2.718218)

=(1.32)*[ (e^(0.0175)/e^(0.0275)] = 1.31 (lower than current rate)

This means a stronger Canadian dollar ( relative to the US Dollar)

Add Answer to:

For all questions, interest (r) and dividend (d) rates are

continuously compounded unless specified otherwise.

Q2)...

For all questions, interest (r) and dividend (d) rates are continuously compounded unless specified otherwise. r...

For all questions, interest (r) and dividend (d) rates are continuously compounded unless specified otherwise. r = 4%, d = 0%, T = 3 months. a) P20 = $4.95, P18 = $2.90. Is there a possible arbitrage? If so, what is your proposed arbitrage portfolio and what is the present value of your profit? b) Instead of being able to buy and sell the options at the same price, assume there is a bid/ask spread. P20 = $4.85/$4.95 (bid/ask) and...

For all questions, interest (r) and dividend (d) rates are continuously compounded unless specified otherwise. 3....

For all questions, interest (r) and dividend (d) rates are continuously compounded unless specified otherwise. 3. r = 4%, d = 0%, T = 3 months. a) P20 = $4.95, P18 = $2.90. Is there a possible arbitrage? If so, what is your proposed arbitrage portfolio and what is the present value of your profit? b) Instead of being able to buy and sell the options at the same price, assume there is a bid/ask spread. P20 = $4.85/$4.95 (bid/ask)...

Three Exchange Rates are as follows: 1) US Dollars (USD) to Canadian Dollars (CAD) at CAD...

Three Exchange Rates are as follows: 1) US Dollars (USD) to Canadian Dollars (CAD) at CAD 1.05 to USD 1 2) CAD to Euros (EUR) at CAD 1.08 to EUR 1 3) EUR to USD at EUR 0.9 to USD 1 Suppose you start with USD 100,000, and do one round of "triangular arbitrage", that is convert make a total of 3 foreign exchange transactions to start from USD and return to USD. What will be your profit in USD?...

Question 9 (1 point) Three Exchange Rates are as follows: 1) US Dollars (USD) to Canadian...

Question 9 (1 point) Three Exchange Rates are as follows: 1) US Dollars (USD) to Canadian Dollars (CAD) at CAD 1.05 to USD 1 2) CAD to Euros (EUR) at CAD 1.08 to EUR 1 3) EUR to USD at EUR 0.9 to USD 1 Suppose you start with USD 100,000, and do one round of "triangular arbitrage". that is convert make a total of 3 foreign exchange transactions to start from USD and return to USD. What will be...

Question 9 (1 point) Three Exchange Rates are as follows: 1) US Dollars (USD) to Canadian Dollars (CAD) at CAD 1.05 to USD 1 2) CAD to Euros (EUR) at CAD 1.08 to EUR 1 3) EUR to USD at EUR 0.9 to USD 1 Suppose you start with USD 100,000, and do one round of "triangular arbitrage". that is convert make a total of 3 foreign exchange transactions to start from USD and return to USD. What will be...

You, as a U.S. investor, find the current annual interest rate in the U.S. is 3%...

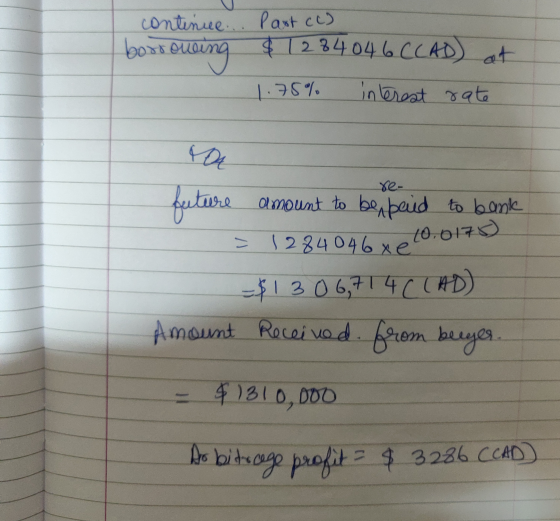

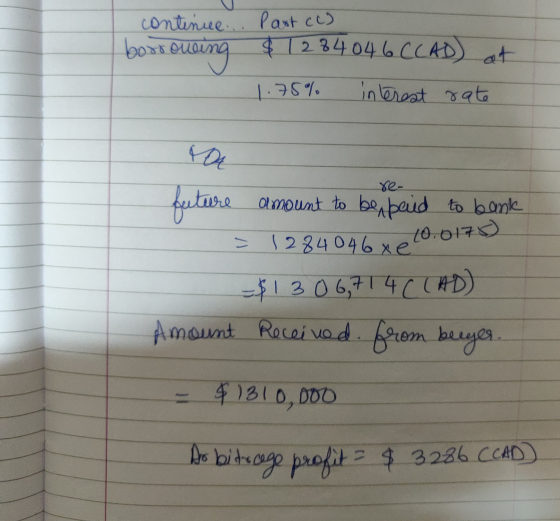

You, as a U.S. investor, find the current annual interest rate in the U.S. is 3% and the annual interest rate in Canada is 5%. The spot exchange rate for Canadian dollar is $0.95 per Canadian dollar, the 90-day Canadian dollar forward exchange rate is $0.928 per Canadian dollar. Explain your arbitrage strategy using the forward contract and the investment in the money market? How much arbitrage profit can you make if you can borrow up to $1 million Canadian...

You, as a U.S. investor, find the current annual interest rate in the U.S. is 3% and the annual interest rate in Canada is 5%. The spot exchange rate for Canadian dollar is $0.95 per Canadian dollar, the 90-day Canadian dollar forward exchange rate is $0.928 per Canadian dollar. Explain your arbitrage strategy using the forward contract and the investment in the money market? How much arbitrage profit can you make if you can borrow up to $1 million Canadian...

a) Bid Price of New Zealand Dollar - JP Morgan Bank USD0.6533 and Well Fargo USD0.6503...

a) Bid Price of New Zealand Dollar - JP Morgan Bank USD0.6533 and Well Fargo USD0.6503 Ask Price of New Zealand Dollar - JP Morgan Bank USD0.6563 and Well Fargo USD0.6523 Justify whether locational arbitrage is possible. If so, explain the steps involved in locational arbitrage, and estimate the profit from this arbitrage if you had USD1,000,000 to use. Discuss market forces factors that would occur to eliminate any further possibilities of locational arbitrage. (6 marks) b) Currency Pair Quoted...

Lesson 7: Principles of Market Valuation 7.1 Find a website that shows exchange rates for all major...

Lesson 7: Principles of Market Valuation 7.1 Find a website that shows exchange rates for all major international currencies. One such site is XE.com. Another is oanda.com. (10 marks) What is the current exchange rate between the Canadian dollar and the US dollar? (2 marks) XE.com allows you to see current exchange rates for gold ounces (type “gold” into the From or To box). (4 marks, 1 each) i. What is 1 ounce of gold worth in Canadian dollars? ii. In US dollars? iii. What does...

The spot exchange rate today is 1.32 US Dollars for every Euro. Suppose the 6-month continuously...

The spot exchange rate today is 1.32 US Dollars for every Euro. Suppose the 6-month continuously compounded interest rates are 2% in the US and 3% in Europe. (a) What should the price of a currency futures contract deliverable in 6 months be? (b) Suppose that the futures price quoted in the market is 1.30. What would you do to profit from the situation? Is it an arbitrage? Hint: Long a futures contract (for the quoted futures price), lend out...

QUESTION 1: Suppose that the current spot exchange rate is GBP1= €1.50 and the one-year forward...

QUESTION 1: Suppose that the current spot exchange rate is GBP1= €1.50 and the one-year forward exchange rate is GBP1=€1.60. One-year interest rate is 5.4% in euros and 5.2% in pounds. If you have EUR1,000,000, what is the Covered Interest arbitrage profit in EUR? QUESTION 2: Suppose that the current spot exchange rate is GBP1= €1.50 and the one-year forward exchange rate is GBP1=€1.60. One-year interest rate is 5.4% in euros and 5.2% in pounds. If you conduct covered interest...

Can anyone answer the question and explain it thx alot 22. Jet engine manufacturing entails enormous...

Can anyone answer the question and explain it thx alot

22. Jet engine manufacturing entails enormous economies of scale. Pratt & Whitney, a large U.S. jet engine producer, faces substantial competition from Rolls-Royce, the British engine manufacturer. What would be the BEST way for P&W to cope with a dollar that has recently appreciated by 50%? a) accelerate R&D spending and cost-cutting efforts b) shift some of its production abroad c) raise the foreign currency prices of its engines sold...

Can anyone answer the question and explain it thx alot

22. Jet engine manufacturing entails enormous economies of scale. Pratt & Whitney, a large U.S. jet engine producer, faces substantial competition from Rolls-Royce, the British engine manufacturer. What would be the BEST way for P&W to cope with a dollar that has recently appreciated by 50%? a) accelerate R&D spending and cost-cutting efforts b) shift some of its production abroad c) raise the foreign currency prices of its engines sold...

Question 9 (1 point) Three Exchange Rates are as follows: 1) US Dollars (USD) to Canadian Dollars (CAD) at CAD 1.05 to USD 1 2) CAD to Euros (EUR) at CAD 1.08 to EUR 1 3) EUR to USD at EUR 0.9 to USD 1 Suppose you start with USD 100,000, and do one round of "triangular arbitrage". that is convert make a total of 3 foreign exchange transactions to start from USD and return to USD. What will be...

Question 9 (1 point) Three Exchange Rates are as follows: 1) US Dollars (USD) to Canadian Dollars (CAD) at CAD 1.05 to USD 1 2) CAD to Euros (EUR) at CAD 1.08 to EUR 1 3) EUR to USD at EUR 0.9 to USD 1 Suppose you start with USD 100,000, and do one round of "triangular arbitrage". that is convert make a total of 3 foreign exchange transactions to start from USD and return to USD. What will be...

You, as a U.S. investor, find the current annual interest rate in the U.S. is 3% and the annual interest rate in Canada is 5%. The spot exchange rate for Canadian dollar is $0.95 per Canadian dollar, the 90-day Canadian dollar forward exchange rate is $0.928 per Canadian dollar. Explain your arbitrage strategy using the forward contract and the investment in the money market? How much arbitrage profit can you make if you can borrow up to $1 million Canadian...

You, as a U.S. investor, find the current annual interest rate in the U.S. is 3% and the annual interest rate in Canada is 5%. The spot exchange rate for Canadian dollar is $0.95 per Canadian dollar, the 90-day Canadian dollar forward exchange rate is $0.928 per Canadian dollar. Explain your arbitrage strategy using the forward contract and the investment in the money market? How much arbitrage profit can you make if you can borrow up to $1 million Canadian...

Can anyone answer the question and explain it thx alot

22. Jet engine manufacturing entails enormous economies of scale. Pratt & Whitney, a large U.S. jet engine producer, faces substantial competition from Rolls-Royce, the British engine manufacturer. What would be the BEST way for P&W to cope with a dollar that has recently appreciated by 50%? a) accelerate R&D spending and cost-cutting efforts b) shift some of its production abroad c) raise the foreign currency prices of its engines sold...

Can anyone answer the question and explain it thx alot

22. Jet engine manufacturing entails enormous economies of scale. Pratt & Whitney, a large U.S. jet engine producer, faces substantial competition from Rolls-Royce, the British engine manufacturer. What would be the BEST way for P&W to cope with a dollar that has recently appreciated by 50%? a) accelerate R&D spending and cost-cutting efforts b) shift some of its production abroad c) raise the foreign currency prices of its engines sold...

Most questions answered within 3 hours.

-

What is the purpose of the 2' hydroxyl group in RNA? What is

the reason this...

asked 3 minutes ago -

You currently have 20,000X ethidium bromide. You want to make

250 mL of 1X ethidium bromide...

asked 16 minutes ago -

What mass of lead is needed to absorb 348 J of heat if the temp

of...

asked 19 minutes ago -

Explain the difference between an auction with reserve

and an auction without reserve. if not specified,...

asked 21 minutes ago -

Write the net ionic equation for the precipitation reaction that

occurs when aqueous solutions of aluminum...

asked 24 minutes ago -

How do we find the slope distance, given the horizontal distance

and the zenith angle?

For...

asked 23 minutes ago -

The table to the right lists probabilities for the corresponding

numbers of girls in three births....

asked 34 minutes ago -

The inverse demand function for good X is P = 5−0.05Q. The

firm’s cost curve is...

asked 32 minutes ago -

The Fresh Connection is really pushing the new line of juice

products. Given that it takes...

asked 38 minutes ago -

An acute decrease in mean arterial pressure (by getting up very

quickly, for instance) will cause...

asked 37 minutes ago -

Is the pH of solutions important when using the Fluoride ISE? If

so, why?

asked 40 minutes ago -

Producer surplus is:

a.

always equal to consumer surplus.

b.

the amount paid to sellers above...

asked 42 minutes ago