The 1 year forward rate is CAD 1.34/Euro. The Canadian risk free rate is 4.7%, the...

The 1 year forward rate is CAD 1.34/Euro. The Canadian risk free rate is 4.7%, the Euro risk free rate is 3.0%. If the Law of One Price holds, what should the spot exchange rate be, in CAD per Euro?

Homework Answers

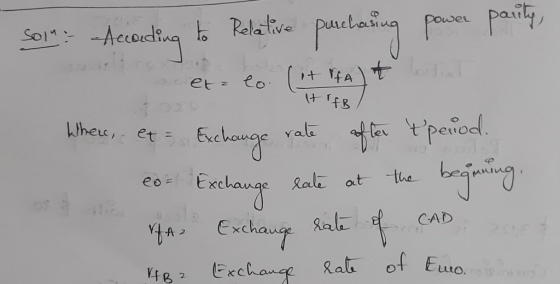

In the above case, risk free rates of Canada and Europe, and ome year forward exchange rate of Canada and Europe are given. The exchange rate is calculated from Relative Purchasing power parity theory as shown in the below images:

Add Answer to:

The 1 year forward rate is CAD 1.34/Euro. The Canadian risk free

rate is 4.7%, the...

The 1 year forward rate is CAD 1.36/Euro. The Canadian risk free rate is 3.4%, the...

The 1 year forward rate is CAD 1.36/Euro. The Canadian risk free rate is 3.4%, the Euro risk free rate is 2.6%. If the Law of One Price holds, what should the spot exchange rate be, in CAD per Euro?

Calculate the following currency forward rates A) 1-year USD/CAD Spot rate: Risk-free USD rate: Risk-free CAD...

Calculate the following currency forward rates A) 1-year USD/CAD Spot rate: Risk-free USD rate: Risk-free CAD rate: 1.4040 2.37% p.a.d 0.92% pa.d B) 6-month CHF/JPY Spot rate: Risk-free CHF rate: Risk-free JPY rate: 121.61 -0.70% pa.d 0.19% p.a.d C) 3-month EUR/MXN Spot rate: Risk-free EUR rate: Risk-free MXN rate: 23.8 -0.61% 5.30%

Calculate the following currency forward rates A) 1-year USD/CAD Spot rate: Risk-free USD rate: Risk-free CAD rate: 1.4040 2.37% p.a.d 0.92% pa.d B) 6-month CHF/JPY Spot rate: Risk-free CHF rate: Risk-free JPY rate: 121.61 -0.70% pa.d 0.19% p.a.d C) 3-month EUR/MXN Spot rate: Risk-free EUR rate: Risk-free MXN rate: 23.8 -0.61% 5.30%

You want to find out forward rate by interest rate parity. Suppose U.S. risk free rate...

You want to find out forward rate by interest rate parity. Suppose U.S. risk free rate is 4.0% , and Canadian risk-free rate is 2.3% . The current spot exchange rate is 1.16 canadian dollar per U.S. dollar. What is the approximate 2 year forward rate if interest rate parity holds?

1. The present exchange rate between US dollars and Euros is 1.34 $/Euro. The price of...

1. The present exchange rate between US dollars and Euros is 1.34 $/Euro. The price of a domestic 180-day Treasury bill is S99.50 per $100 face value. The price of the analogous Buro instrument is 98.50 Euros per 100 Euro face value (a) What is the theoretical 180-day forward exchange rate? (b) Suppose the 180-day forward exchange rate available in the marketplace is 1.31 $/Euro. This is less than the theoretical forward exchange rate, so an arbitrage is possible. Describe...

1. The present exchange rate between US dollars and Euros is 1.34 $/Euro. The price of a domestic 180-day Treasury bill is S99.50 per $100 face value. The price of the analogous Buro instrument is 98.50 Euros per 100 Euro face value (a) What is the theoretical 180-day forward exchange rate? (b) Suppose the 180-day forward exchange rate available in the marketplace is 1.31 $/Euro. This is less than the theoretical forward exchange rate, so an arbitrage is possible. Describe...

The present exchange rate between US dollars and Euros is 1.34 $/Euro. The price of a...

The present exchange rate between US dollars and Euros is 1.34 $/Euro. The price of a domestic 180-day Treasury bill is $99.50 per $100 face value. The price of the analogous Euro instrument is 98.50 Euros per 100 Euro face value. a. What is the theoretical 180-day forward exchange rate? b.Suppose the 180-day forward exchange rate available in the marketplace is 1.31 $/Euro. This is less than the theoretical forward exchange rate, so an arbitrage is possible. Describe a risk-free...

Given that the spot rate is 1.5 euros per pound and the forward euro-pound exchange rate...

Given that the spot rate is 1.5 euros per pound and the forward euro-pound exchange rate is 1.575 euros per pound calculate the forward premium discDunt on the British pound and indicate which of the two it is. Consider a Dutch investor with 1 000 euros to pace in a bank deposit in either the Netherlands or Great Britain. The one-year interest rate on bank deposits is 2% in Britain and 4.04% in the Netherlands. The one year forward euro-pound...

Given that the spot rate is 1.5 euros per pound and the forward euro-pound exchange rate is 1.575 euros per pound calculate the forward premium discDunt on the British pound and indicate which of the two it is. Consider a Dutch investor with 1 000 euros to pace in a bank deposit in either the Netherlands or Great Britain. The one-year interest rate on bank deposits is 2% in Britain and 4.04% in the Netherlands. The one year forward euro-pound...

Suppose the one-year forward $1€ exchange rate is $1.7 per euro and the spot exchange rate...

Suppose the one-year forward $1€ exchange rate is $1.7 per euro and the spot exchange rate is $1.8 per euro. What is the forward premium on euros (the forward discount on dollars)? The forward premium on euros is percent. (Give your answer as a percentage with one decimal and do not forget a negative sign, if appropriate.)

Suppose the one-year forward $1€ exchange rate is $1.7 per euro and the spot exchange rate is $1.8 per euro. What is the forward premium on euros (the forward discount on dollars)? The forward premium on euros is percent. (Give your answer as a percentage with one decimal and do not forget a negative sign, if appropriate.)

Suppose the one-year forward $7€ exchange rate is $1.9 per euro and the spot exchange rate...

Suppose the one-year forward $7€ exchange rate is $1.9 per euro and the spot exchange rate is $1.6 per euro. What is the forward premium on euros (the forward discount on dollars)? The forward premium on euros is 18.8 percent. (Give your answer as a percentage with one decimal and do not forget a negative sign, if appropriate.) Given the above information, what is the difference between the interest rate on one-year dollar deposits and that on one-year euro deposits...

Suppose the one-year forward $7€ exchange rate is $1.9 per euro and the spot exchange rate is $1.6 per euro. What is the forward premium on euros (the forward discount on dollars)? The forward premium on euros is 18.8 percent. (Give your answer as a percentage with one decimal and do not forget a negative sign, if appropriate.) Given the above information, what is the difference between the interest rate on one-year dollar deposits and that on one-year euro deposits...

In currency markets the letters CAD refers the Canadian dollar whereas USD refers to the US...

In currency markets the letters CAD refers the Canadian dollar whereas USD refers to the US dollar. The CAD/USD spot exchange is 1.40. The continuously compounded risk free rate in both countries is 0.25%. The volatility of price changes in the exchange rate is 25%. Using Black-Scholes, determine the price of 1-year European call option (in CAD) to buy USD if the CAD/USD strike is 1.5. a) 0.04 c) 0.08 e) 0.12 b) 0.06 d) 0.10

In currency markets the letters CAD refers the Canadian dollar whereas USD refers to the US dollar. The CAD/USD spot exchange is 1.40. The continuously compounded risk free rate in both countries is 0.25%. The volatility of price changes in the exchange rate is 25%. Using Black-Scholes, determine the price of 1-year European call option (in CAD) to buy USD if the CAD/USD strike is 1.5. a) 0.04 c) 0.08 e) 0.12 b) 0.06 d) 0.10

Assume a risk-free asset in the U.S. is currently yielding 2.1 percent while a Canadian risk-free...

Assume a risk-free asset in the U.S. is currently yielding 2.1 percent while a Canadian risk-free asset is yielding 2.6 percent. The current spot rate is CAD1.323. What is the approximate 2-year forward rate if interest rate parity holds? CAD1.3414 CAD1.3363 CCAD1.3396 CAD1.3450 CCAD1.3335

Assume a risk-free asset in the U.S. is currently yielding 2.1 percent while a Canadian risk-free asset is yielding 2.6 percent. The current spot rate is CAD1.323. What is the approximate 2-year forward rate if interest rate parity holds? CAD1.3414 CAD1.3363 CCAD1.3396 CAD1.3450 CCAD1.3335

Calculate the following currency forward rates A) 1-year USD/CAD Spot rate: Risk-free USD rate: Risk-free CAD rate: 1.4040 2.37% p.a.d 0.92% pa.d B) 6-month CHF/JPY Spot rate: Risk-free CHF rate: Risk-free JPY rate: 121.61 -0.70% pa.d 0.19% p.a.d C) 3-month EUR/MXN Spot rate: Risk-free EUR rate: Risk-free MXN rate: 23.8 -0.61% 5.30%

Calculate the following currency forward rates A) 1-year USD/CAD Spot rate: Risk-free USD rate: Risk-free CAD rate: 1.4040 2.37% p.a.d 0.92% pa.d B) 6-month CHF/JPY Spot rate: Risk-free CHF rate: Risk-free JPY rate: 121.61 -0.70% pa.d 0.19% p.a.d C) 3-month EUR/MXN Spot rate: Risk-free EUR rate: Risk-free MXN rate: 23.8 -0.61% 5.30%

1. The present exchange rate between US dollars and Euros is 1.34 $/Euro. The price of a domestic 180-day Treasury bill is S99.50 per $100 face value. The price of the analogous Buro instrument is 98.50 Euros per 100 Euro face value (a) What is the theoretical 180-day forward exchange rate? (b) Suppose the 180-day forward exchange rate available in the marketplace is 1.31 $/Euro. This is less than the theoretical forward exchange rate, so an arbitrage is possible. Describe...

1. The present exchange rate between US dollars and Euros is 1.34 $/Euro. The price of a domestic 180-day Treasury bill is S99.50 per $100 face value. The price of the analogous Buro instrument is 98.50 Euros per 100 Euro face value (a) What is the theoretical 180-day forward exchange rate? (b) Suppose the 180-day forward exchange rate available in the marketplace is 1.31 $/Euro. This is less than the theoretical forward exchange rate, so an arbitrage is possible. Describe...

Given that the spot rate is 1.5 euros per pound and the forward euro-pound exchange rate is 1.575 euros per pound calculate the forward premium discDunt on the British pound and indicate which of the two it is. Consider a Dutch investor with 1 000 euros to pace in a bank deposit in either the Netherlands or Great Britain. The one-year interest rate on bank deposits is 2% in Britain and 4.04% in the Netherlands. The one year forward euro-pound...

Given that the spot rate is 1.5 euros per pound and the forward euro-pound exchange rate is 1.575 euros per pound calculate the forward premium discDunt on the British pound and indicate which of the two it is. Consider a Dutch investor with 1 000 euros to pace in a bank deposit in either the Netherlands or Great Britain. The one-year interest rate on bank deposits is 2% in Britain and 4.04% in the Netherlands. The one year forward euro-pound...

Suppose the one-year forward $1€ exchange rate is $1.7 per euro and the spot exchange rate is $1.8 per euro. What is the forward premium on euros (the forward discount on dollars)? The forward premium on euros is percent. (Give your answer as a percentage with one decimal and do not forget a negative sign, if appropriate.)

Suppose the one-year forward $1€ exchange rate is $1.7 per euro and the spot exchange rate is $1.8 per euro. What is the forward premium on euros (the forward discount on dollars)? The forward premium on euros is percent. (Give your answer as a percentage with one decimal and do not forget a negative sign, if appropriate.)

Suppose the one-year forward $7€ exchange rate is $1.9 per euro and the spot exchange rate is $1.6 per euro. What is the forward premium on euros (the forward discount on dollars)? The forward premium on euros is 18.8 percent. (Give your answer as a percentage with one decimal and do not forget a negative sign, if appropriate.) Given the above information, what is the difference between the interest rate on one-year dollar deposits and that on one-year euro deposits...

Suppose the one-year forward $7€ exchange rate is $1.9 per euro and the spot exchange rate is $1.6 per euro. What is the forward premium on euros (the forward discount on dollars)? The forward premium on euros is 18.8 percent. (Give your answer as a percentage with one decimal and do not forget a negative sign, if appropriate.) Given the above information, what is the difference between the interest rate on one-year dollar deposits and that on one-year euro deposits...

In currency markets the letters CAD refers the Canadian dollar whereas USD refers to the US dollar. The CAD/USD spot exchange is 1.40. The continuously compounded risk free rate in both countries is 0.25%. The volatility of price changes in the exchange rate is 25%. Using Black-Scholes, determine the price of 1-year European call option (in CAD) to buy USD if the CAD/USD strike is 1.5. a) 0.04 c) 0.08 e) 0.12 b) 0.06 d) 0.10

In currency markets the letters CAD refers the Canadian dollar whereas USD refers to the US dollar. The CAD/USD spot exchange is 1.40. The continuously compounded risk free rate in both countries is 0.25%. The volatility of price changes in the exchange rate is 25%. Using Black-Scholes, determine the price of 1-year European call option (in CAD) to buy USD if the CAD/USD strike is 1.5. a) 0.04 c) 0.08 e) 0.12 b) 0.06 d) 0.10

Assume a risk-free asset in the U.S. is currently yielding 2.1 percent while a Canadian risk-free asset is yielding 2.6 percent. The current spot rate is CAD1.323. What is the approximate 2-year forward rate if interest rate parity holds? CAD1.3414 CAD1.3363 CCAD1.3396 CAD1.3450 CCAD1.3335

Assume a risk-free asset in the U.S. is currently yielding 2.1 percent while a Canadian risk-free asset is yielding 2.6 percent. The current spot rate is CAD1.323. What is the approximate 2-year forward rate if interest rate parity holds? CAD1.3414 CAD1.3363 CCAD1.3396 CAD1.3450 CCAD1.3335

Most questions answered within 3 hours.

-

Explain some different types of fungi. State the different

divisions undergo by fungi.

asked 10 minutes ago -

The shortest time that 120 C can flow through a 20 A circuit

breaker without tripping...

asked 11 minutes ago -

A software design pattern is a general, reusable solution to a

commonly occurring problem, acting as...

asked 13 minutes ago -

The mean waiting time at the drive-through of a fast-food

restaurant from the time an order...

asked 30 minutes ago -

The pitch (p) of a helix is defined as p = dn, in which n is...

asked 32 minutes ago -

Do you agree that the declining stock of social capital is the

blame for the failure...

asked 36 minutes ago -

A researcher is interested in whether coffee consumption helps

with performance on reading comprehension tasks. The...

asked 45 minutes ago -

it has been estimated since the beginning of the human race that

about 133 metric ton...

asked 51 minutes ago -

Where must Medicare prescription drug plans allow for

participants to fill their prescriptions?

asked 54 minutes ago -

Five moles of monatomic ideal gas have initial pressure 2.50 ×

103 Pa and initial volume...

asked 1 hour ago -

A resistor and the capacitor are used to control the timing in

the RC circuit of...

asked 1 hour ago -

Living in a group could bring several disadvantages to an

individual. What are some of the...

asked 1 hour ago