Plz give answer to follwoing multiple choices

Homework Answers

Add Answer to:

Plz give answer to follwoing multiple choices

Question 1 0.25 pts market, the product is homogeneous,...

2. The amount of a good that buyers are willing and able to buy at a...

2. The amount of a good that buyers are willing and able to buy at a specific price is known as: demand. sales. quantity demanded. product quantity. 3. The effect describes the change in consumer purchasing power that occurs when the price of a good changes. demand supply income substitution 4. The price of chicken has doubled. As a result, Andre will purchase pork instead of chicken. This is an example of the effect. substitution demand increasing cost income eos...

2. The amount of a good that buyers are willing and able to buy at a specific price is known as: demand. sales. quantity demanded. product quantity. 3. The effect describes the change in consumer purchasing power that occurs when the price of a good changes. demand supply income substitution 4. The price of chicken has doubled. As a result, Andre will purchase pork instead of chicken. This is an example of the effect. substitution demand increasing cost income eos...

Question 17 0.25 pts 17. If both supply and demand increase, will increase, and is unclear....

Question 17 0.25 pts 17. If both supply and demand increase, will increase, and is unclear. O a. price; quantity O b.supply; quantity O c.quantity; price O d. quantity; supply Question 18 0.25 pts 18. Lower resource cost will cause price to decrease. O True O False oo Question 19 0.25 pts 19. Turkey and chicken are substitutes. The price of turkey falls. As a result, we expect the price of chicken to increase. O True O False Question 20...

Question 17 0.25 pts 17. If both supply and demand increase, will increase, and is unclear. O a. price; quantity O b.supply; quantity O c.quantity; price O d. quantity; supply Question 18 0.25 pts 18. Lower resource cost will cause price to decrease. O True O False oo Question 19 0.25 pts 19. Turkey and chicken are substitutes. The price of turkey falls. As a result, we expect the price of chicken to increase. O True O False Question 20...

Question 11 0.16 pts If the price and quantity for an inferior good, Good X, is...

Question 11 0.16 pts If the price and quantity for an inferior good, Good X, is $8 and 6 units at the original equilibrium, what is one possibility for the new equilibrium of Good X if we see income increase and all other factors stay constant? O $6 and 8 units O $10 and 8 units $6 and 4 units O $10 and 2 units O $10 and 4 units Question 12 0.16 pts According to the law of demand,...

Question 11 0.16 pts If the price and quantity for an inferior good, Good X, is $8 and 6 units at the original equilibrium, what is one possibility for the new equilibrium of Good X if we see income increase and all other factors stay constant? O $6 and 8 units O $10 and 8 units $6 and 4 units O $10 and 2 units O $10 and 4 units Question 12 0.16 pts According to the law of demand,...

NI There is but one correct answer to each multiple choice question. If Demand decreases by...

NI There is but one correct answer to each multiple choice question. If Demand decreases by a greater amount than Supply decreases, then Pricean a. Increases, decreases b Deceases, increases c. Decreases, decrease 1. d. Increases, increase 2. A change in the demand for Pork can be caused by a. A change in the price for beef b) A change in the price for pork c. A change in the cost of producing pork 3. An increase in quantity supplied...

NI There is but one correct answer to each multiple choice question. If Demand decreases by a greater amount than Supply decreases, then Pricean a. Increases, decreases b Deceases, increases c. Decreases, decrease 1. d. Increases, increase 2. A change in the demand for Pork can be caused by a. A change in the price for beef b) A change in the price for pork c. A change in the cost of producing pork 3. An increase in quantity supplied...

Question 14 1 pts If the price elasticity of supply was calculated as 0.40 for a...

Question 14 1 pts If the price elasticity of supply was calculated as 0.40 for a product and the price increases by 12%, what would happen to the quantity supplied? O Quantity supplied would increase by 8%. O Quantity supplied would increase by 6.3%. O Quantity supplied would increase by 4.8%. Question 15 1 pts As we move along a typical negatively sloping, linear demand curve O the elasticity is constant. it results in elasticity and slope being the same....

Question 14 1 pts If the price elasticity of supply was calculated as 0.40 for a product and the price increases by 12%, what would happen to the quantity supplied? O Quantity supplied would increase by 8%. O Quantity supplied would increase by 6.3%. O Quantity supplied would increase by 4.8%. Question 15 1 pts As we move along a typical negatively sloping, linear demand curve O the elasticity is constant. it results in elasticity and slope being the same....

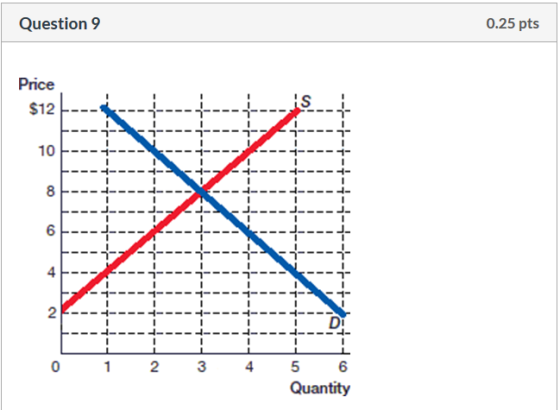

Please help with these four questions, Question 1 0.16 pts The change in equilibrium shown in...

Please help with these four questions,

Question 1 0.16 pts The change in equilibrium shown in the accompanying figure would be explained by a(n) price ofa in the price of an input and a(n) in the increase; increase; complement decrease; increase; substitute increase; increase; substitute increase; decrease; complement decrease; increase; complement Question 2 0.16 pts When people move to an area of the world that was previously unpopulated, we expect more consumers and more producers to spring up in that...

Please help with these four questions,

Question 1 0.16 pts The change in equilibrium shown in the accompanying figure would be explained by a(n) price ofa in the price of an input and a(n) in the increase; increase; complement decrease; increase; substitute increase; increase; substitute increase; decrease; complement decrease; increase; complement Question 2 0.16 pts When people move to an area of the world that was previously unpopulated, we expect more consumers and more producers to spring up in that...

This question will deal with demand, supply, equilibrium and comparative statics in a specific market: the...

This question will deal with demand, supply, equilibrium and comparative statics in a specific market: the market for pork. We will use specific equations for Demand and Supply of pork which come from an academic paper: “Production Subsidy and Countervailing Duties in Vertically Related Markets: The Hog-Pork Case Between Canada and the United States” written by Giancarlo Moschini and Karl D. Meilke which appeared in American Journal of Agricultural Economics, Vol. 74, No. 4 (Nov., 1992), pp.951-961. The authors estimated...

Part 1: Short Answer Questions (10 points each) 1) The estimated Canadian processed pork demand and...

Part 1: Short Answer Questions (10 points each) 1) The estimated Canadian processed pork demand and supply functions are as the follow- ings: Qp = 100-3 p + 3 p + 5 + 2 Y, Os = 100 + 6 - 8 PA where Q is the quantity in million kilograms (kg) of pork per year; p is the dollar price per kg, Po is the price of beef per kg, pe is the price of chicken per kg, P,...

Part 1: Short Answer Questions (10 points each) 1) The estimated Canadian processed pork demand and supply functions are as the follow- ings: Qp = 100-3 p + 3 p + 5 + 2 Y, Os = 100 + 6 - 8 PA where Q is the quantity in million kilograms (kg) of pork per year; p is the dollar price per kg, Po is the price of beef per kg, pe is the price of chicken per kg, P,...

please answer all the multiple choices 16 through 20 d a decrease in the supply of...

please answer all the multiple choices 16 through 20

d a decrease in the supply of leftuce an increase in the price and a decrease in the quanitity demanded Assume that pink salmon is a normal good and consumers income increases You accurately predict that in the market for pink salmon, there will be a an increase in the demand of pink salmon, an increase in the price and an increase in quantity supplied b an increase in the quantity...

please answer all the multiple choices 16 through 20

d a decrease in the supply of leftuce an increase in the price and a decrease in the quanitity demanded Assume that pink salmon is a normal good and consumers income increases You accurately predict that in the market for pink salmon, there will be a an increase in the demand of pink salmon, an increase in the price and an increase in quantity supplied b an increase in the quantity...

Please help with these questions, Question 5 0.16 pts When firms in a market expect the...

Please help with these questions,

Question 5 0.16 pts When firms in a market expect the price of their products to rise, the supply curve of their goods causing the equilibrium price to O decreases; rise increases; rise and the equilibrium quantity to fall decreases; fall increases; fall O increases; rise Question 6 0.16 pts Taxes cause the equilibrium price of a good to Ogo up only for producers. O decrease O go down only for consumers O increase. remain...

Please help with these questions,

Question 5 0.16 pts When firms in a market expect the price of their products to rise, the supply curve of their goods causing the equilibrium price to O decreases; rise increases; rise and the equilibrium quantity to fall decreases; fall increases; fall O increases; rise Question 6 0.16 pts Taxes cause the equilibrium price of a good to Ogo up only for producers. O decrease O go down only for consumers O increase. remain...

2. The amount of a good that buyers are willing and able to buy at a specific price is known as: demand. sales. quantity demanded. product quantity. 3. The effect describes the change in consumer purchasing power that occurs when the price of a good changes. demand supply income substitution 4. The price of chicken has doubled. As a result, Andre will purchase pork instead of chicken. This is an example of the effect. substitution demand increasing cost income eos...

2. The amount of a good that buyers are willing and able to buy at a specific price is known as: demand. sales. quantity demanded. product quantity. 3. The effect describes the change in consumer purchasing power that occurs when the price of a good changes. demand supply income substitution 4. The price of chicken has doubled. As a result, Andre will purchase pork instead of chicken. This is an example of the effect. substitution demand increasing cost income eos...

Question 17 0.25 pts 17. If both supply and demand increase, will increase, and is unclear. O a. price; quantity O b.supply; quantity O c.quantity; price O d. quantity; supply Question 18 0.25 pts 18. Lower resource cost will cause price to decrease. O True O False oo Question 19 0.25 pts 19. Turkey and chicken are substitutes. The price of turkey falls. As a result, we expect the price of chicken to increase. O True O False Question 20...

Question 17 0.25 pts 17. If both supply and demand increase, will increase, and is unclear. O a. price; quantity O b.supply; quantity O c.quantity; price O d. quantity; supply Question 18 0.25 pts 18. Lower resource cost will cause price to decrease. O True O False oo Question 19 0.25 pts 19. Turkey and chicken are substitutes. The price of turkey falls. As a result, we expect the price of chicken to increase. O True O False Question 20...

Question 11 0.16 pts If the price and quantity for an inferior good, Good X, is $8 and 6 units at the original equilibrium, what is one possibility for the new equilibrium of Good X if we see income increase and all other factors stay constant? O $6 and 8 units O $10 and 8 units $6 and 4 units O $10 and 2 units O $10 and 4 units Question 12 0.16 pts According to the law of demand,...

Question 11 0.16 pts If the price and quantity for an inferior good, Good X, is $8 and 6 units at the original equilibrium, what is one possibility for the new equilibrium of Good X if we see income increase and all other factors stay constant? O $6 and 8 units O $10 and 8 units $6 and 4 units O $10 and 2 units O $10 and 4 units Question 12 0.16 pts According to the law of demand,...

NI There is but one correct answer to each multiple choice question. If Demand decreases by a greater amount than Supply decreases, then Pricean a. Increases, decreases b Deceases, increases c. Decreases, decrease 1. d. Increases, increase 2. A change in the demand for Pork can be caused by a. A change in the price for beef b) A change in the price for pork c. A change in the cost of producing pork 3. An increase in quantity supplied...

NI There is but one correct answer to each multiple choice question. If Demand decreases by a greater amount than Supply decreases, then Pricean a. Increases, decreases b Deceases, increases c. Decreases, decrease 1. d. Increases, increase 2. A change in the demand for Pork can be caused by a. A change in the price for beef b) A change in the price for pork c. A change in the cost of producing pork 3. An increase in quantity supplied...

Question 14 1 pts If the price elasticity of supply was calculated as 0.40 for a product and the price increases by 12%, what would happen to the quantity supplied? O Quantity supplied would increase by 8%. O Quantity supplied would increase by 6.3%. O Quantity supplied would increase by 4.8%. Question 15 1 pts As we move along a typical negatively sloping, linear demand curve O the elasticity is constant. it results in elasticity and slope being the same....

Question 14 1 pts If the price elasticity of supply was calculated as 0.40 for a product and the price increases by 12%, what would happen to the quantity supplied? O Quantity supplied would increase by 8%. O Quantity supplied would increase by 6.3%. O Quantity supplied would increase by 4.8%. Question 15 1 pts As we move along a typical negatively sloping, linear demand curve O the elasticity is constant. it results in elasticity and slope being the same....

Please help with these four questions,

Question 1 0.16 pts The change in equilibrium shown in the accompanying figure would be explained by a(n) price ofa in the price of an input and a(n) in the increase; increase; complement decrease; increase; substitute increase; increase; substitute increase; decrease; complement decrease; increase; complement Question 2 0.16 pts When people move to an area of the world that was previously unpopulated, we expect more consumers and more producers to spring up in that...

Please help with these four questions,

Question 1 0.16 pts The change in equilibrium shown in the accompanying figure would be explained by a(n) price ofa in the price of an input and a(n) in the increase; increase; complement decrease; increase; substitute increase; increase; substitute increase; decrease; complement decrease; increase; complement Question 2 0.16 pts When people move to an area of the world that was previously unpopulated, we expect more consumers and more producers to spring up in that...

Part 1: Short Answer Questions (10 points each) 1) The estimated Canadian processed pork demand and supply functions are as the follow- ings: Qp = 100-3 p + 3 p + 5 + 2 Y, Os = 100 + 6 - 8 PA where Q is the quantity in million kilograms (kg) of pork per year; p is the dollar price per kg, Po is the price of beef per kg, pe is the price of chicken per kg, P,...

Part 1: Short Answer Questions (10 points each) 1) The estimated Canadian processed pork demand and supply functions are as the follow- ings: Qp = 100-3 p + 3 p + 5 + 2 Y, Os = 100 + 6 - 8 PA where Q is the quantity in million kilograms (kg) of pork per year; p is the dollar price per kg, Po is the price of beef per kg, pe is the price of chicken per kg, P,...

please answer all the multiple choices 16 through 20

d a decrease in the supply of leftuce an increase in the price and a decrease in the quanitity demanded Assume that pink salmon is a normal good and consumers income increases You accurately predict that in the market for pink salmon, there will be a an increase in the demand of pink salmon, an increase in the price and an increase in quantity supplied b an increase in the quantity...

please answer all the multiple choices 16 through 20

d a decrease in the supply of leftuce an increase in the price and a decrease in the quanitity demanded Assume that pink salmon is a normal good and consumers income increases You accurately predict that in the market for pink salmon, there will be a an increase in the demand of pink salmon, an increase in the price and an increase in quantity supplied b an increase in the quantity...

Please help with these questions,

Question 5 0.16 pts When firms in a market expect the price of their products to rise, the supply curve of their goods causing the equilibrium price to O decreases; rise increases; rise and the equilibrium quantity to fall decreases; fall increases; fall O increases; rise Question 6 0.16 pts Taxes cause the equilibrium price of a good to Ogo up only for producers. O decrease O go down only for consumers O increase. remain...

Please help with these questions,

Question 5 0.16 pts When firms in a market expect the price of their products to rise, the supply curve of their goods causing the equilibrium price to O decreases; rise increases; rise and the equilibrium quantity to fall decreases; fall increases; fall O increases; rise Question 6 0.16 pts Taxes cause the equilibrium price of a good to Ogo up only for producers. O decrease O go down only for consumers O increase. remain...

Most questions answered within 3 hours.

-

How does a linear regression allow you to better estimate

trends, costs, and other factors in...

asked 7 minutes ago -

1. (15%) Describe the difference between a pull (Kanban), push

and CONWIP production systems.

asked 3 minutes ago -

QUESTION 5

The total area under the Z distribution curve is equal to:

a.

10

b....

asked 12 minutes ago -

Using Python

The variables x and y refer to numbers. Write a code segment

that prompts...

asked 26 minutes ago -

If

the coefficient of static friction between a box and the floor is

0.35 with what...

asked 28 minutes ago -

A die is designed to punch holes with a radius of 1.08 10-2 m in

a...

asked 33 minutes ago -

government can increase import through

a. export subsidies

b. tax breaks

c. increase import tax

d....

asked 34 minutes ago -

Draw the following in the proper skeletal structure or line

angle formula.

5,6,6-tribromo-3,8-dicyclopropyl-7-isopentyldodecane

asked 39 minutes ago -

Two blocks of masses m1 and m2 hang at the ends of a string that

passes...

asked 40 minutes ago -

Linear programming is an excellent technique yet is not applied

nearly enough in the “real world.”...

asked 49 minutes ago -

What three alkenes yield 3-methylpentane on catalytic

hydrogenation?

asked 49 minutes ago -

In JAVA Create a program with an array with the following

data:

50 12 31 76...

asked 51 minutes ago