Suppose that Treasury bills offer a return of about 6% and the expected market risk premium...

Suppose that Treasury bills offer a return of about 6% and the expected market risk premium is 8.5%. The standard deviation of Treasury-bill returns is zero and the standard deviation of market returns is 20%. Use the formula for portfolio risk to calculate the standard deviation of portfolios with different proportions in Treasury bills and the market. (Note: The covariance of two rates of return must be zero when the standard deviation of one return is zero.) Graph the expected returns and standard deviations.

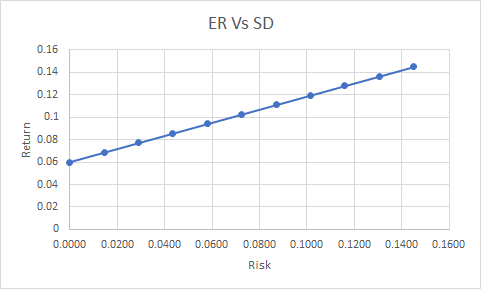

What is the slope of the line and what does it describe/signify?

What happens if an investment alternative does not plot on the line?

Homework Answers

T-bill return = 6%

So, rf = 6%

Standard Deviation = 0

Market risk premium = rm-rf = 8.5%

S0, rm = 14.50%

Standard Deviation = 0.2

used following formula to calculate portfolio return and portfolio risk/Standard deviation

ER = w1*r1 + w2*r2

SD = weight of market*standard deviation of market

| Weight of T-bill | Weight of market | ER | SD |

| 0 | 1 | 14.50% | 0.1450 |

| 0.1 | 0.9 | 13.65% | 0.1305 |

| 0.2 | 0.8 | 12.80% | 0.1160 |

| 0.3 | 0.7 | 11.95% | 0.1015 |

| 0.4 | 0.6 | 11.10% | 0.0870 |

| 0.5 | 0.5 | 10.25% | 0.0725 |

| 0.6 | 0.4 | 9.40% | 0.0580 |

| 0.7 | 0.3 | 8.55% | 0.0435 |

| 0.8 | 0.2 | 7.70% | 0.0290 |

| 0.9 | 0.1 | 6.85% | 0.0145 |

| 1 | 0 | 6.00% | 0.0000 |

Slope = 0.586

The Slope of the line measures the trade-off between risk and return. It tells the amount of return comes with a certain level of risk.

If an investment alternative does not plot on line, it is known as minimum variance frontier. Point on the curve with lowest standard deviation is also called global minimum variance portfolio. Curve above the global minimum variance portfolio is efficient frontier. This curve help to build efficient portfolio for an individual based on his/her risk aversion.

Add Answer to:

Suppose that Treasury bills offer a return of about 6% and the

expected market risk premium...

Question You manage an equity fund with an expected risk premium of 10% and an expected...

Question You manage an equity fund with an expected risk premium of 10% and an expected standard deviation of 14%. The rate on Treasury bills is 6 %. Your client chooses to invest $60,000 of her portfolio in your equity fund and $40,000 in a T-bill money market fund What is the expected return and standard deviation of return on your client's portfolio?

Question You manage an equity fund with an expected risk premium of 10% and an expected standard deviation of 14%. The rate on Treasury bills is 6 %. Your client chooses to invest $60,000 of her portfolio in your equity fund and $40,000 in a T-bill money market fund What is the expected return and standard deviation of return on your client's portfolio?

You manage an equity fund with an expected risk premium of 13.2% and a standard deviation...

You manage an equity fund with an expected risk premium of 13.2% and a standard deviation of 46%. The rate on Treasury bills is 4.6%. Your client chooses to invest $105,000 of her portfolio in your equity fund and $45,000 in a T-bill money market fund. What is the expected return and standard deviation of return on your client’s portfolio? (Round your answers to 2 decimal places.) Expected return % Standard deviation %

Course:Porfolio fund and management Question You manage an equity fund with an expected risk premium of...

Course:Porfolio fund and management

Question You manage an equity fund with an expected risk premium of 10% and a standard deviation of 14%. The rate on Treasury bills is 6%. Your client chooses to invest $60,000 of her portfolio in your equity fund and $40,000 in a T-bill money market fund What is the expected return and standard deviation of return on your client's portfolio?

Course:Porfolio fund and management

Question You manage an equity fund with an expected risk premium of 10% and a standard deviation of 14%. The rate on Treasury bills is 6%. Your client chooses to invest $60,000 of her portfolio in your equity fund and $40,000 in a T-bill money market fund What is the expected return and standard deviation of return on your client's portfolio?

expected return

a . Compute the expected return of the stocks A and B ? b . Compute the risks of the stocks A and B ? c . If the return of the Treasury Bills is 6 % . Compute the risk premium and the risk aversion of each stock d . Assume that you invest $ 120,000 in X and 30,000 in Y. Compute the expected return and the risk of your portfolio . e . Compute the reward to volatility of your portfolio...

a . Compute the expected return of the stocks A and B ? b . Compute the risks of the stocks A and B ? c . If the return of the Treasury Bills is 6 % . Compute the risk premium and the risk aversion of each stock d . Assume that you invest $ 120,000 in X and 30,000 in Y. Compute the expected return and the risk of your portfolio . e . Compute the reward to volatility of your portfolio...

Consider a stock with expected return of 12%. Treasury bills currently yield 4%. The expected return...

Consider a stock with expected return of 12%. Treasury bills currently yield 4%. The expected return on the market portfolio is 7%. What is the risk premium on this stock? Please explain do not use excel sheets.

1. The universe of available securities includes two risky stock funds, A and B and T-bills....

1. The universe of available securities includes two risky stock funds, A and B and T-bills. The data for the universe are as follows: Expected Return Standard Deviation 109 20 Tbilis The correlation coefficient between funds A and B is -0.2. a. Find the optimal risky portfolio, P. and its expected return and standard deviation b. Find the slope of the CAL supported by T-bills and portfolio P. c. How much will an investor with 4-5 invest in funds A...

1. The universe of available securities includes two risky stock funds, A and B and T-bills. The data for the universe are as follows: Expected Return Standard Deviation 109 20 Tbilis The correlation coefficient between funds A and B is -0.2. a. Find the optimal risky portfolio, P. and its expected return and standard deviation b. Find the slope of the CAL supported by T-bills and portfolio P. c. How much will an investor with 4-5 invest in funds A...

. The Treasury bill rate (i.e. risk-free rate) is 2.5%, and the expected return on the...

. The Treasury bill rate (i.e. risk-free rate) is 2.5%, and the expected return on the market portfolio is 12%. Using the capital asset pricing model: a. What is the risk premium on the market? b. What is the required rate of return on an investment with a beta of 1.15? c. If an investment with a beta of 0.80 offers an expected return of 10.5%, does it have a positive NPV?

Expected Return, Varianoe & Standard Deviation Suppose your expectations of the stock market are shown as...

Expected Return, Varianoe & Standard Deviation Suppose your expectations of the stock market are shown as follows: Prob r(s) Boom 0.2 30% Normal 0.5 20% Recession 0.3 -20% (Expected Return(E(r)), variance(o2) and standard deviation (o) Compute the mean of the rate of return on stocks. Risk Premium & Capital Allocation Consider when you decide to invest in a risky portfolio P (with the expected return of 20% and standard deviation of 30 %) and a Treasury bill (The rate of...

Expected Return, Varianoe & Standard Deviation Suppose your expectations of the stock market are shown as follows: Prob r(s) Boom 0.2 30% Normal 0.5 20% Recession 0.3 -20% (Expected Return(E(r)), variance(o2) and standard deviation (o) Compute the mean of the rate of return on stocks. Risk Premium & Capital Allocation Consider when you decide to invest in a risky portfolio P (with the expected return of 20% and standard deviation of 30 %) and a Treasury bill (The rate of...

HAPPY stock returns have a covariance with the market portfolio of 0.036. The standard deviation of the returns on the market portfolio is 20%, and the expected market risk premium is 7.5%. The company has bonds outstanding total market value of $35 mill

HAPPY stock returns have a covariance with the market portfolio of 0.036. The standard deviation of the returns on the market portfolio is 20%, and the expected market risk premium is 7.5%. The company has bonds outstanding total market value of $35 million. The bond is 10% annual coupon with one-year maturity and sold each at 101.852% of the face value of $1000. The company also has 6 million shares of common stock outstanding, each selling for $20. The corporate...

Asset A has a CAPM beta of 1.5. The covariance between asset A and asset B is 0.13. If the risk-free rate is 0.05, the expected market risk premium is 0.07, and the market risk premium has a standard...

Asset A has a CAPM beta of 1.5. The covariance between asset A and asset B is 0.13. If the risk-free rate is 0.05, the expected market risk premium is 0.07, and the market risk premium has a standard deviation of 25%, then what is asset B's expected return under the CAPM?

Asset A has a CAPM beta of 1.5. The covariance between asset A and asset B is 0.13. If the risk-free rate is 0.05, the expected market risk...

Asset A has a CAPM beta of 1.5. The covariance between asset A and asset B is 0.13. If the risk-free rate is 0.05, the expected market risk premium is 0.07, and the market risk premium has a standard deviation of 25%, then what is asset B's expected return under the CAPM?

Asset A has a CAPM beta of 1.5. The covariance between asset A and asset B is 0.13. If the risk-free rate is 0.05, the expected market risk...

Question You manage an equity fund with an expected risk premium of 10% and an expected standard deviation of 14%. The rate on Treasury bills is 6 %. Your client chooses to invest $60,000 of her portfolio in your equity fund and $40,000 in a T-bill money market fund What is the expected return and standard deviation of return on your client's portfolio?

Question You manage an equity fund with an expected risk premium of 10% and an expected standard deviation of 14%. The rate on Treasury bills is 6 %. Your client chooses to invest $60,000 of her portfolio in your equity fund and $40,000 in a T-bill money market fund What is the expected return and standard deviation of return on your client's portfolio?

Course:Porfolio fund and management

Question You manage an equity fund with an expected risk premium of 10% and a standard deviation of 14%. The rate on Treasury bills is 6%. Your client chooses to invest $60,000 of her portfolio in your equity fund and $40,000 in a T-bill money market fund What is the expected return and standard deviation of return on your client's portfolio?

Course:Porfolio fund and management

Question You manage an equity fund with an expected risk premium of 10% and a standard deviation of 14%. The rate on Treasury bills is 6%. Your client chooses to invest $60,000 of her portfolio in your equity fund and $40,000 in a T-bill money market fund What is the expected return and standard deviation of return on your client's portfolio?

1. The universe of available securities includes two risky stock funds, A and B and T-bills. The data for the universe are as follows: Expected Return Standard Deviation 109 20 Tbilis The correlation coefficient between funds A and B is -0.2. a. Find the optimal risky portfolio, P. and its expected return and standard deviation b. Find the slope of the CAL supported by T-bills and portfolio P. c. How much will an investor with 4-5 invest in funds A...

1. The universe of available securities includes two risky stock funds, A and B and T-bills. The data for the universe are as follows: Expected Return Standard Deviation 109 20 Tbilis The correlation coefficient between funds A and B is -0.2. a. Find the optimal risky portfolio, P. and its expected return and standard deviation b. Find the slope of the CAL supported by T-bills and portfolio P. c. How much will an investor with 4-5 invest in funds A...

Expected Return, Varianoe & Standard Deviation Suppose your expectations of the stock market are shown as follows: Prob r(s) Boom 0.2 30% Normal 0.5 20% Recession 0.3 -20% (Expected Return(E(r)), variance(o2) and standard deviation (o) Compute the mean of the rate of return on stocks. Risk Premium & Capital Allocation Consider when you decide to invest in a risky portfolio P (with the expected return of 20% and standard deviation of 30 %) and a Treasury bill (The rate of...

Expected Return, Varianoe & Standard Deviation Suppose your expectations of the stock market are shown as follows: Prob r(s) Boom 0.2 30% Normal 0.5 20% Recession 0.3 -20% (Expected Return(E(r)), variance(o2) and standard deviation (o) Compute the mean of the rate of return on stocks. Risk Premium & Capital Allocation Consider when you decide to invest in a risky portfolio P (with the expected return of 20% and standard deviation of 30 %) and a Treasury bill (The rate of...

Asset A has a CAPM beta of 1.5. The covariance between asset A and asset B is 0.13. If the risk-free rate is 0.05, the expected market risk premium is 0.07, and the market risk premium has a standard deviation of 25%, then what is asset B's expected return under the CAPM?

Asset A has a CAPM beta of 1.5. The covariance between asset A and asset B is 0.13. If the risk-free rate is 0.05, the expected market risk...

Asset A has a CAPM beta of 1.5. The covariance between asset A and asset B is 0.13. If the risk-free rate is 0.05, the expected market risk premium is 0.07, and the market risk premium has a standard deviation of 25%, then what is asset B's expected return under the CAPM?

Asset A has a CAPM beta of 1.5. The covariance between asset A and asset B is 0.13. If the risk-free rate is 0.05, the expected market risk...

Most questions answered within 3 hours.

-

3) What are the typical social structures in a global city?

asked 1 hour ago -

Luther Corporation

Consolidated Balance Sheet

December 31, 2019 and 2018 (in $ millions)

Assets

2019

2018...

asked 1 hour ago -

(Expected rate of return and risk) Carter Inc. is evaluating a

security. Calculate the investment’s expected...

asked 3 hours ago -

What specific indicators can point to lack of progress for

African Americans in American society?

asked 4 hours ago -

1-The Electrons in a beam are moving at 2.7×108 m/s in an

electric field of 15000...

asked 5 hours ago -

A gas tank is a vertical cylinder. It has a radius of 1m, a

height of...

asked 5 hours ago -

Accent Software faces the following conditions. All of these

support Accent’s use of a market-penetration pricing...

asked 6 hours ago -

A mathematically inclined friend emails you the following

instructions: "Meet me in the cafeteria the first...

asked 6 hours ago -

A monopoly sells in two countries . The demand curves in the two

countries are p1...

asked 7 hours ago -

A .15kg rubber ball is bounced off a wall. Before hitting the

wall, the ball moves...

asked 8 hours ago -

A manufacturing company preparing to build a new plant is

considering three potential locations for it....

asked 8 hours ago -

B. If compound Y has approximately the same values of solubility

in toluene as compound X,...

asked 9 hours ago