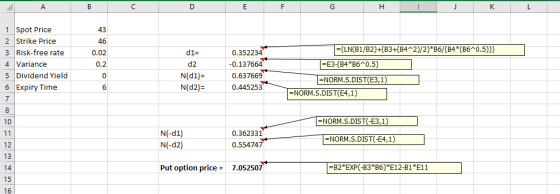

5. Stock TB12 is currently trading at $43. The annual variance of stock return is 0.2,...

5. Stock TB12 is currently trading at $43. The annual variance of stock return is 0.2, the annual

effective risk-free rate is 2%, and the exercise price of a 6-year put option is 46. The put price

is:

Can you show the inputs for d1 and d2

Thanks

Homework Answers

Please do rate me and mention doubts, if any, in the comments section.

Add Answer to:

5. Stock TB12 is currently trading at $43. The annual variance

of stock return is 0.2,...

Stock price: $48 Exercise price : 46 Time to expiration: 1 year Stock price variance: 0.40...

Stock price: $48 Exercise price : 46 Time to expiration: 1 year Stock price variance: 0.40 per year Risk-free interest rate (compounded continuously) 5% per year A) at what price should a European call option with the above characteristics sell (Note: when calculating N(d1) and N(d2). please carry your estimates out to 4 digits B) Is this call option in the money, at the money, or out of the money. C) At what price should the corresponding put option sell?

Problem1 A stock is currently trading at S $40, during next 6 months stock price will increase to $44 or decrease to $32-6-month risk-free rate is rf-2%. a. [4pts) What positions in stock and T-...

Problem1 A stock is currently trading at S $40, during next 6 months stock price will increase to $44 or decrease to $32-6-month risk-free rate is rf-2%. a. [4pts) What positions in stock and T-bills will you put to replicate the pay off of a European call option with K = $38 and maturing in 6 months. b. 1pt What is the value of this European call option? Problem 2 Suppose that stock price will increase 5% and decrease 5%...

Problem1 A stock is currently trading at S $40, during next 6 months stock price will increase to $44 or decrease to $32-6-month risk-free rate is rf-2%. a. [4pts) What positions in stock and T-bills will you put to replicate the pay off of a European call option with K = $38 and maturing in 6 months. b. 1pt What is the value of this European call option? Problem 2 Suppose that stock price will increase 5% and decrease 5%...

1. The stock of the McCall Corporation is currently trading at $42 per share. The stock’s...

1. The stock of the McCall Corporation is currently trading at $42 per share. The stock’s volatility as measured by its standard deviation is 20%. If the strike (exercise) price for a certain set of options on McCall stock carry a strike price of $40, and the options run for 6 months (180 days), determine the Black-Scholes model values for: N (d1), N (d2), N (- d1), and N (- d2). (Assume the risk-free rate is 10% and that the...

RST, Inc. stock is currently trading for $33 per share. The stock pays no dividends. A...

RST, Inc. stock is currently trading for $33 per share. The stock pays no dividends. A one-year European call option on RST with a strike price of $36 is currently trading for $2.99. If the risk-free interest rate is 6% per year, what is the price of a one-year European put option on RST with a strike price of $36? (Rounded to the nearest cent.)

RST, Inc. stock is currently trading for $33 per share. The stock pays no dividends. A one-year European call option on RST with a strike price of $36 is currently trading for $2.99. If the risk-free interest rate is 6% per year, what is the price of a one-year European put option on RST with a strike price of $36? (Rounded to the nearest cent.)

The current price of a stock is $ 48.36 and the annual risk-free rate is 5.3...

The current price of a stock is $ 48.36 and the annual risk-free rate is 5.3 percent. A put option with an exercise price of $55 and one year until expiration has a current value of $ 7.82 . What is the value of a call option written on the stock with the same exercise price and expiration date as the put option? Show your answer to the nearest .01. Do not use $ or , in your answer. Because...

Dynamic Energy Systems stock is currently trading for $29 per share. The stock pays no dividends....

Dynamic Energy Systems stock is currently trading for $29 per share. The stock pays no dividends. A one-year European put option on Dynamic with a strike price of $32 is currently trading for $3.69. If the risk-free interest rate is 3% per year, what is the price of a one-year European call option on Dynamic with a strike price of $32? (Rounded to the nearest cent.)

Dynamic Energy Systems stock is currently trading for $29 per share. The stock pays no dividends. A one-year European put option on Dynamic with a strike price of $32 is currently trading for $3.69. If the risk-free interest rate is 3% per year, what is the price of a one-year European call option on Dynamic with a strike price of $32? (Rounded to the nearest cent.)

Assume Coca-Cola stock is currently trading at $46 per share and that an investor forecasts future...

Assume Coca-Cola stock is currently trading at $46 per share and that an investor forecasts future dividends to be $1.80 in year 1 (D1), $2.00 in year 2 (D2), and $2.25 in year 3 (D3) along with an expected stock price at the horizon date of $50 (P3). What is the implied rate of return to an investor who buys the stock today at its current price if the forecasts are correct? *Hint: You need to use the internal rate...

On October 2, 2018, Tesla stock was trading $305.65. There are options on Tesla stock, Below...

On October 2, 2018, Tesla stock was trading $305.65. There are options on Tesla stock, Below are the yarigble inputs you require. Using the Black-Scholes-Merton model and Solyer, solve for the implied volatility that causes the option to be valued at $44.25. The appropriate risk free rate c.c. is 0.85%. These are European Options. Underlying So Call or Put Strike 306.65 Put 300.00 10/2/18 3/15/19 Today Maturity Time to Expiration Volatility Risk Free Rate 59.52% 0.85% #N/ A #N/A #N/A...

On October 2, 2018, Tesla stock was trading $305.65. There are options on Tesla stock, Below are the yarigble inputs you require. Using the Black-Scholes-Merton model and Solyer, solve for the implied volatility that causes the option to be valued at $44.25. The appropriate risk free rate c.c. is 0.85%. These are European Options. Underlying So Call or Put Strike 306.65 Put 300.00 10/2/18 3/15/19 Today Maturity Time to Expiration Volatility Risk Free Rate 59.52% 0.85% #N/ A #N/A #N/A...

The current price of a stock is $ 53.15 and the annual risk-free rate is 6.6...

The current price of a stock is $ 53.15 and the annual risk-free rate is 6.6 percent. A put option with an exercise price of $55 and one year until expiration has a current value of $ 4.98 . What is the value of a call option written on the stock with the same exercise price and expiration date as the put option? Note, the given interest rate is an effective rate, so for calculation purposes, you need only discount...

Long pul 2. Springtime Insurance Brokers Ltd. (SIBL stock is currently selling for $42. A put...

Long pul 2. Springtime Insurance Brokers Ltd. (SIBL stock is currently selling for $42. A put option on the stock with a value of $3 has an exercise price of $40 and 6 months until expiration. To prevent arbitrage opportunities, what should be the value of a call option with the same strike price and expiration date? Assume that the options are European and that the effective annual risk-free rate is 6%. the State Focus

Long pul 2. Springtime Insurance Brokers Ltd. (SIBL stock is currently selling for $42. A put option on the stock with a value of $3 has an exercise price of $40 and 6 months until expiration. To prevent arbitrage opportunities, what should be the value of a call option with the same strike price and expiration date? Assume that the options are European and that the effective annual risk-free rate is 6%. the State Focus

Problem1 A stock is currently trading at S $40, during next 6 months stock price will increase to $44 or decrease to $32-6-month risk-free rate is rf-2%. a. [4pts) What positions in stock and T-bills will you put to replicate the pay off of a European call option with K = $38 and maturing in 6 months. b. 1pt What is the value of this European call option? Problem 2 Suppose that stock price will increase 5% and decrease 5%...

Problem1 A stock is currently trading at S $40, during next 6 months stock price will increase to $44 or decrease to $32-6-month risk-free rate is rf-2%. a. [4pts) What positions in stock and T-bills will you put to replicate the pay off of a European call option with K = $38 and maturing in 6 months. b. 1pt What is the value of this European call option? Problem 2 Suppose that stock price will increase 5% and decrease 5%...

RST, Inc. stock is currently trading for $33 per share. The stock pays no dividends. A one-year European call option on RST with a strike price of $36 is currently trading for $2.99. If the risk-free interest rate is 6% per year, what is the price of a one-year European put option on RST with a strike price of $36? (Rounded to the nearest cent.)

RST, Inc. stock is currently trading for $33 per share. The stock pays no dividends. A one-year European call option on RST with a strike price of $36 is currently trading for $2.99. If the risk-free interest rate is 6% per year, what is the price of a one-year European put option on RST with a strike price of $36? (Rounded to the nearest cent.)

Dynamic Energy Systems stock is currently trading for $29 per share. The stock pays no dividends. A one-year European put option on Dynamic with a strike price of $32 is currently trading for $3.69. If the risk-free interest rate is 3% per year, what is the price of a one-year European call option on Dynamic with a strike price of $32? (Rounded to the nearest cent.)

Dynamic Energy Systems stock is currently trading for $29 per share. The stock pays no dividends. A one-year European put option on Dynamic with a strike price of $32 is currently trading for $3.69. If the risk-free interest rate is 3% per year, what is the price of a one-year European call option on Dynamic with a strike price of $32? (Rounded to the nearest cent.)

On October 2, 2018, Tesla stock was trading $305.65. There are options on Tesla stock, Below are the yarigble inputs you require. Using the Black-Scholes-Merton model and Solyer, solve for the implied volatility that causes the option to be valued at $44.25. The appropriate risk free rate c.c. is 0.85%. These are European Options. Underlying So Call or Put Strike 306.65 Put 300.00 10/2/18 3/15/19 Today Maturity Time to Expiration Volatility Risk Free Rate 59.52% 0.85% #N/ A #N/A #N/A...

On October 2, 2018, Tesla stock was trading $305.65. There are options on Tesla stock, Below are the yarigble inputs you require. Using the Black-Scholes-Merton model and Solyer, solve for the implied volatility that causes the option to be valued at $44.25. The appropriate risk free rate c.c. is 0.85%. These are European Options. Underlying So Call or Put Strike 306.65 Put 300.00 10/2/18 3/15/19 Today Maturity Time to Expiration Volatility Risk Free Rate 59.52% 0.85% #N/ A #N/A #N/A...

Long pul 2. Springtime Insurance Brokers Ltd. (SIBL stock is currently selling for $42. A put option on the stock with a value of $3 has an exercise price of $40 and 6 months until expiration. To prevent arbitrage opportunities, what should be the value of a call option with the same strike price and expiration date? Assume that the options are European and that the effective annual risk-free rate is 6%. the State Focus

Long pul 2. Springtime Insurance Brokers Ltd. (SIBL stock is currently selling for $42. A put option on the stock with a value of $3 has an exercise price of $40 and 6 months until expiration. To prevent arbitrage opportunities, what should be the value of a call option with the same strike price and expiration date? Assume that the options are European and that the effective annual risk-free rate is 6%. the State Focus

Most questions answered within 3 hours.

-

Minitab Problem: Take the Lake Hume June rainfall data and find

use the processes outlined in...

asked 13 minutes ago -

X Company is trying to decide whether to continue using old

equipment to make Product A...

asked 14 minutes ago -

IN PYTHON ONLY !! Program 2: Re-work

program #5 (WeeklyHours) from the previous assignment such that...

asked 50 minutes ago -

The average length of time between arrivals at a turnpike

toll-booth is 26 seconds. What is...

asked 2 hours ago -

(a) A piston at 6.1 atm contains a gas that occupies a volume of

3.5 L....

asked 3 hours ago -

Please answer true or false. Words

cannot be changed or added in to make it true...

asked 3 hours ago -

An empty test tube weighs 15.923 grams. Then,

MgCl2•6H2O is added into the test tube. After...

asked 3 hours ago -

Assume memory access is 10 units of time and disk access is

10000 units of time....

asked 4 hours ago -

1. Are all good samples random?

2. Magazines often report surveys giving statistics such as “63%...

asked 4 hours ago -

Under all the various types of market structures, firms

must eventually earn some economic profits for...

asked 4 hours ago -

Consider the following fitness regime for a single locus trait

with two co-dominant alleles: w11 =...

asked 4 hours ago -

A large cable company reports the following.

80% of its customers subscribe to its cable TV...

asked 4 hours ago