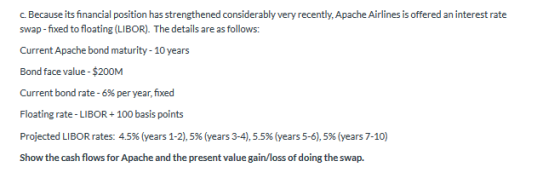

| Cash Flows | |||||

| Bond outstanding | Original | Swap Pmts. | Net | ||

| Maturity (yrs.) | Year 1 | ||||

| Fixed rate | Year 2 | ||||

| Spread over LIBOR | Year 3 | ||||

| LIBOR: | Year 4 | ||||

| Years 1-2 | Year 5 | ||||

| Years 3-4 | Year 6 | ||||

| Years 5-6 | Year 7 | ||||

| Years 7-10 | Year 8 | ||||

| Year 9 | |||||

| Year 10 | |||||

| Present value of net | |||||

Homework Answers

Answer.

No Required rate of return given for Apache, Hence it is assumed Apache can invest gains at 6%

| CashFlows | |||||||

| Bond outstanding | 200 | Original | Swap Pmts. | Net | DF | PV | |

| Maturity (yrs.) | 10 | Year 1 | 12 | 11 | 1 | 0.943 | 0.943 |

| Fixed rate | 6 | Year 2 | 12 | 11 | 1 | 0.890 | 0.890 |

| Spread over LIBOR | 100 | Year 3 | 12 | 12 | 0 | ||

| LIBOR: | Year 4 | 12 | 12 | 0 | |||

| Years 1-2 | 4.5 | Year 5 | 12 | 13 | -1 | 0.747 | -0.747 |

| Years 3-4 | 5 | Year 6 | 12 | 13 | -1 | 0.705 | -0.705 |

| Years 5-6 | 5.5 | Year 7 | 12 | 12 | 0 | ||

| Years 7-10 | 5 | Year 8 | 12 | 12 | 0 | ||

| Year 9 | 12 | 12 | 0 | ||||

| Year 10 | 12 | 12 | 0 | ||||

| Present value of net | 0.381 | ||||||

Add Answer to:

Cash Flows

Bond

outstanding

Original

Swap Pmts.

Net

Maturity

(yrs.)

Year

1

Fixed

rate

Year

2...

This problem illustrates how to [1] determine the payments of an interest rate swap, [2] value...

This problem illustrates how to [1] determine the payments of an interest rate swap, [2] value the swap, [3] and hedge with the swap. The problem is based on the WSJ article “School District, Bank in Swap clash”. The setting: The local school district was planning to build a new high school. The estimated cost of the building was around $100M. To finance the building the school district needed to issue a bond for about $58M. It had two choices:...

Microsoft issues a four year, floating-rate bond for the amount of $100 Million. It pays annually...

Microsoft issues a four year, floating-rate bond for the amount of $100 Million. It pays annually to bondholders. Because Microsoft would prefer to have a fixed rate payment, it enters into a SWAP with Citibank. Year LIBOR (%) Fixed-Rate payments to Citibank Floating-Rate payments from Citibank Net payment to Citibank Payment to bondholders Net payment by Microsoft 1 4 4 2 3 2 5 5 1 4 3 6 6 0 5 4 7 7 -1 6 Explain the conditions...

Consider the following information about an interest rate swap: two-year term, semiannual payment, fixed rate =...

Consider the following information about an interest rate swap: two-year term, semiannual payment, fixed rate = notional USD 10 million. Calculate the net coupon exchange for the first period if LIBOR is 5% at the beginning of the period and 5.5% at the end of the period Q2. 6%, floating rate = LIBOR + 50 basis points, A. Fixed-rate payer pays USD 0 B. Fixed-rate payer pays USD 25,000 C. Fixed-rate payer pays USD 50,000 D. Fixed-rate payer receives USD...

Consider the following information about an interest rate swap: two-year term, semiannual payment, fixed rate = notional USD 10 million. Calculate the net coupon exchange for the first period if LIBOR is 5% at the beginning of the period and 5.5% at the end of the period Q2. 6%, floating rate = LIBOR + 50 basis points, A. Fixed-rate payer pays USD 0 B. Fixed-rate payer pays USD 25,000 C. Fixed-rate payer pays USD 50,000 D. Fixed-rate payer receives USD...

Consider a plain vanilla fixed for floating interest rate swap with a notional principal of 4,100,000...

Consider a plain vanilla fixed for floating interest rate swap with a notional principal of 4,100,000 and annual payments. Initially the swap was supposed to last for five years and now three years remain. If the initial fixed rate is 0.09, LIBOR is 0.08, and the year three payment was just made (two years of payments remain on the swap), What is the absolute value of the swap?

Cement Al-Yamamah has just entered into a two-year floating-for-fixed swap contract, where payments are made every...

Cement Al-Yamamah has just entered into a two-year

floating-for-fixed swap contract, where payments are made every six

months. The 6-month LIBOR is 4.11%. The 6 to 12 months forward

LIBOR rate is 5.92% and the 12 to 18 month forward LIBOR rate is

8.19. The two-year swap rate is 5.1%. If the OIS rate is 3.5% and

the term structure of the OIS rate is flat, what is the 18 to 24

month Forward LIBOR rate? All rates are semi-annually...

Cement Al-Yamamah has just entered into a two-year

floating-for-fixed swap contract, where payments are made every six

months. The 6-month LIBOR is 4.11%. The 6 to 12 months forward

LIBOR rate is 5.92% and the 12 to 18 month forward LIBOR rate is

8.19. The two-year swap rate is 5.1%. If the OIS rate is 3.5% and

the term structure of the OIS rate is flat, what is the 18 to 24

month Forward LIBOR rate? All rates are semi-annually...

Betsco, Inc. has previously issued a bond that currently has 7 years left until maturity. The...

Betsco, Inc. has previously issued a bond that currently has 7 years left until maturity. The coupon rate of the bond is tied to LIBOR (specifically, its rate is LIBOR + 5%). The Director expects interest rate movements to negatively affect the interest expense generated by this debt obligation. Therefore, she wishes to effectively change her liability from floating to fixed. The most recently issued Treasury Note is yielding 6%. She contacts several banks that quote her the following: Bank...

a) ABC Ltd is interested to sell an existing fixed-for-floating interest rate swap to one of...

a) ABC Ltd is interested to sell an existing fixed-for-floating interest rate swap to one of its corporate clients. Under the existing swap, ABC Ltd pays 10% pa and receive 3-month LIBOR on a $10 million principal. Cash flows are exchanged every quarter. The swap has a remaining life of 16 months. Data shows that the 3-month LIBOR rate 1 month ago was 11.8% pa; 2 months’ ago it was 12% pa; 3 months’ ago it was 12.2% pa and...

QUESTION # 2 Consider a 1-year swap initiated on January 10th, 2013, between Sony and Samsung, Under the terms of the swap contract Sony is agreed to pay Samsung an interest of 6% per annum on a...

QUESTION # 2 Consider a 1-year swap initiated on January 10th, 2013, between Sony and Samsung, Under the terms of the swap contract Sony is agreed to pay Samsung an interest of 6% per annum on a notional principle of Max. Marks 2+1] $200 n Samsung agrees to pay a 3-month LIBOR rate on the same principal. In addition, the payments are exchanged every three months, andthe6%is quoted with quarterly compounding. Following Table shows the LIBOR Samsung (complete the Table...

QUESTION # 2 Consider a 1-year swap initiated on January 10th, 2013, between Sony and Samsung, Under the terms of the swap contract Sony is agreed to pay Samsung an interest of 6% per annum on a notional principle of Max. Marks 2+1] $200 n Samsung agrees to pay a 3-month LIBOR rate on the same principal. In addition, the payments are exchanged every three months, andthe6%is quoted with quarterly compounding. Following Table shows the LIBOR Samsung (complete the Table...

Consider the following plain vanilla interest rate swap: Volkswagen borrowed $200mm for four years with annual...

Consider the following plain vanilla interest rate swap:

Volkswagen borrowed $200mm for four years with annual payments at a

floating rate of one-year Libor, but now wants fixed rate

liabilities. The World Bank borrowed $200mm for four years with

annual payments of 6%.

1) If two entered into a plain vanilla interest rate swap with

no exchange at time 0, what would the swap rate be? Use the zero

coupon bond prices implied by the yield curve below (assume

continuous...

Consider the following plain vanilla interest rate swap:

Volkswagen borrowed $200mm for four years with annual payments at a

floating rate of one-year Libor, but now wants fixed rate

liabilities. The World Bank borrowed $200mm for four years with

annual payments of 6%.

1) If two entered into a plain vanilla interest rate swap with

no exchange at time 0, what would the swap rate be? Use the zero

coupon bond prices implied by the yield curve below (assume

continuous...

On December 31, 2020, Blossom Corp. had a $9-million, 9% fixed-rate note outstanding that was payable...

On December 31, 2020, Blossom Corp. had a $9-million, 9%

fixed-rate note outstanding that was payable in two years. It

decided to enter into a two-year swap with First Bank to convert

the fixed-rate debt to floating-rate debt. The terms of the swap

specified that Master will receive interest at a fixed rate of 9%

and will pay a variable rate equal to the six-month LIBOR rate,

based on the $9-million amount. The LIBOR rate on December 31,

2020, was...

On December 31, 2020, Blossom Corp. had a $9-million, 9%

fixed-rate note outstanding that was payable in two years. It

decided to enter into a two-year swap with First Bank to convert

the fixed-rate debt to floating-rate debt. The terms of the swap

specified that Master will receive interest at a fixed rate of 9%

and will pay a variable rate equal to the six-month LIBOR rate,

based on the $9-million amount. The LIBOR rate on December 31,

2020, was...

Consider the following information about an interest rate swap: two-year term, semiannual payment, fixed rate = notional USD 10 million. Calculate the net coupon exchange for the first period if LIBOR is 5% at the beginning of the period and 5.5% at the end of the period Q2. 6%, floating rate = LIBOR + 50 basis points, A. Fixed-rate payer pays USD 0 B. Fixed-rate payer pays USD 25,000 C. Fixed-rate payer pays USD 50,000 D. Fixed-rate payer receives USD...

Consider the following information about an interest rate swap: two-year term, semiannual payment, fixed rate = notional USD 10 million. Calculate the net coupon exchange for the first period if LIBOR is 5% at the beginning of the period and 5.5% at the end of the period Q2. 6%, floating rate = LIBOR + 50 basis points, A. Fixed-rate payer pays USD 0 B. Fixed-rate payer pays USD 25,000 C. Fixed-rate payer pays USD 50,000 D. Fixed-rate payer receives USD...

Cement Al-Yamamah has just entered into a two-year

floating-for-fixed swap contract, where payments are made every six

months. The 6-month LIBOR is 4.11%. The 6 to 12 months forward

LIBOR rate is 5.92% and the 12 to 18 month forward LIBOR rate is

8.19. The two-year swap rate is 5.1%. If the OIS rate is 3.5% and

the term structure of the OIS rate is flat, what is the 18 to 24

month Forward LIBOR rate? All rates are semi-annually...

Cement Al-Yamamah has just entered into a two-year

floating-for-fixed swap contract, where payments are made every six

months. The 6-month LIBOR is 4.11%. The 6 to 12 months forward

LIBOR rate is 5.92% and the 12 to 18 month forward LIBOR rate is

8.19. The two-year swap rate is 5.1%. If the OIS rate is 3.5% and

the term structure of the OIS rate is flat, what is the 18 to 24

month Forward LIBOR rate? All rates are semi-annually...

QUESTION # 2 Consider a 1-year swap initiated on January 10th, 2013, between Sony and Samsung, Under the terms of the swap contract Sony is agreed to pay Samsung an interest of 6% per annum on a notional principle of Max. Marks 2+1] $200 n Samsung agrees to pay a 3-month LIBOR rate on the same principal. In addition, the payments are exchanged every three months, andthe6%is quoted with quarterly compounding. Following Table shows the LIBOR Samsung (complete the Table...

QUESTION # 2 Consider a 1-year swap initiated on January 10th, 2013, between Sony and Samsung, Under the terms of the swap contract Sony is agreed to pay Samsung an interest of 6% per annum on a notional principle of Max. Marks 2+1] $200 n Samsung agrees to pay a 3-month LIBOR rate on the same principal. In addition, the payments are exchanged every three months, andthe6%is quoted with quarterly compounding. Following Table shows the LIBOR Samsung (complete the Table...

Consider the following plain vanilla interest rate swap:

Volkswagen borrowed $200mm for four years with annual payments at a

floating rate of one-year Libor, but now wants fixed rate

liabilities. The World Bank borrowed $200mm for four years with

annual payments of 6%.

1) If two entered into a plain vanilla interest rate swap with

no exchange at time 0, what would the swap rate be? Use the zero

coupon bond prices implied by the yield curve below (assume

continuous...

Consider the following plain vanilla interest rate swap:

Volkswagen borrowed $200mm for four years with annual payments at a

floating rate of one-year Libor, but now wants fixed rate

liabilities. The World Bank borrowed $200mm for four years with

annual payments of 6%.

1) If two entered into a plain vanilla interest rate swap with

no exchange at time 0, what would the swap rate be? Use the zero

coupon bond prices implied by the yield curve below (assume

continuous...

On December 31, 2020, Blossom Corp. had a $9-million, 9%

fixed-rate note outstanding that was payable in two years. It

decided to enter into a two-year swap with First Bank to convert

the fixed-rate debt to floating-rate debt. The terms of the swap

specified that Master will receive interest at a fixed rate of 9%

and will pay a variable rate equal to the six-month LIBOR rate,

based on the $9-million amount. The LIBOR rate on December 31,

2020, was...

On December 31, 2020, Blossom Corp. had a $9-million, 9%

fixed-rate note outstanding that was payable in two years. It

decided to enter into a two-year swap with First Bank to convert

the fixed-rate debt to floating-rate debt. The terms of the swap

specified that Master will receive interest at a fixed rate of 9%

and will pay a variable rate equal to the six-month LIBOR rate,

based on the $9-million amount. The LIBOR rate on December 31,

2020, was...

Most questions answered within 3 hours.

-

During the current financial year, the owner of Omega

Enterprises withdrew supplies of $2,000 for personal...

asked 1 minute ago -

PLEASE SHOW MATH CALCULATION(formulas)it has to be done on excel

P12-4 Last year (2016), Richter Condos...

asked 9 minutes ago -

A couple of small ice cubes at 0 °C are added to glass of warm

water...

asked 2 minutes ago -

Regarding language development, which of the following

statements is FALSE?

Babies are able to cry from...

asked 3 minutes ago -

A machine shop owner wishes to assign each of three machinists

(labeled 1, 2, and 3)...

asked 4 minutes ago -

Slow 'n Steady, Inc., has a stock price of $30, will pay a

dividend next year...

asked 5 minutes ago -

A 0.25μF capacitor is charged to 50 V . It is then connected in

series with...

asked 26 minutes ago -

Calculate the current, I, through the batteries for:

- a 2-bulb parallel circuit

- How does...

asked 27 minutes ago -

Choose the sentence that uses correct punctuation.

1a. The prefatory parts of a report include the...

asked 33 minutes ago -

For the element arsenic, which one of the following sets of

quantum numbers could not apply...

asked 43 minutes ago -

Compare and contrast the architectures of 3 types of ADCs:

Flash, SAR, and pipelined. Use the...

asked 44 minutes ago -

Given P(A) = 0.40, P(B) = 0.50, P(A ∩ B) = 0.15. Which of the

following...

asked 48 minutes ago