can someone please explain this question

Homework Answers

Please do Upvote if you are served. Feel free to reach out in the comments

Cheers!!!

Add Answer to:

can someone please explain this question

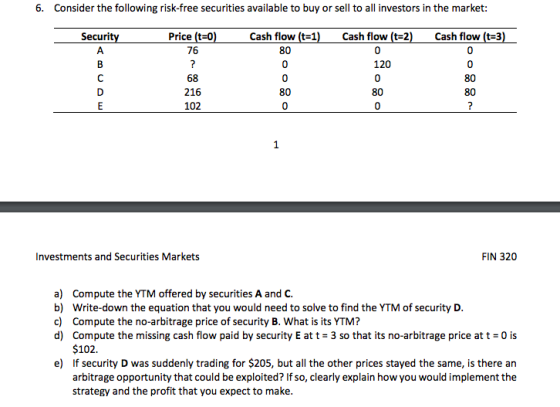

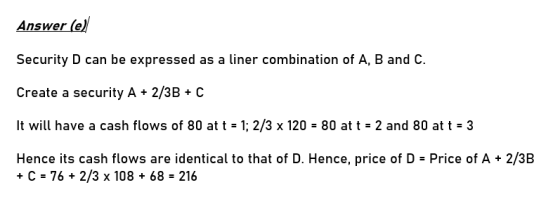

6. Consider the following risk-free securities available to buy or...

Can someone help me with this question. I was assuming a 1% ytm for C and...

Can someone help me with this question. I was assuming a 1% ytm

for C and D but not sure if I did it correctly.

Consider the following risk-free securities available to buy or sell to all investors in the market: 6. Cash flow (t=2) Price (t=0) Cash flow (t=1) Cash flow (t=3) Security 76 80 120 68 80 216 80 80 80 D 102 a) Compute the YTM offered by securities A and C. b) Write-down the equation that...

Can someone help me with this question. I was assuming a 1% ytm

for C and D but not sure if I did it correctly.

Consider the following risk-free securities available to buy or sell to all investors in the market: 6. Cash flow (t=2) Price (t=0) Cash flow (t=1) Cash flow (t=3) Security 76 80 120 68 80 216 80 80 80 D 102 a) Compute the YTM offered by securities A and C. b) Write-down the equation that...

Consider two securities that pay risk-free cash flows over the next two years and that have...

Consider two securities that pay risk-free cash flows over the next two years and that have the current market prices shown here: Security B1 Price Today $90 $72 Cash Flow in one Year Cash Flow in Two Years $100 $0 $0 $80 | B2 a) What is the no-arbitrage price of a security that pays cash flows of $100 in one year and $80 in two years? [2 points] b) What is the no-arbitrage price of a security that pays...

Consider two securities that pay risk-free cash flows over the next two years and that have the current market prices shown here: Security B1 Price Today $90 $72 Cash Flow in one Year Cash Flow in Two Years $100 $0 $0 $80 | B2 a) What is the no-arbitrage price of a security that pays cash flows of $100 in one year and $80 in two years? [2 points] b) What is the no-arbitrage price of a security that pays...

Help with finance question please. 7. Below is a list of prices for $1,000 par zero-coupon...

Help with finance question please.

7. Below is a list of prices for $1,000 par zero-coupon bonds of various maturities. Maturity (Years) Bond AWNA Price $930 $850 $770 $700 1.4 a. Compute the zero-coupon rates for years 1, 2, 3 and 4. b. Consider an 8% coupon $1,000 par bond (denoted by B) paying annual coupons and expiring in 4 years. Compute the no-arbitrage price of the bond and its yield-to-maturity. c. If the expectations hypothesis holds, what is your...

Help with finance question please.

7. Below is a list of prices for $1,000 par zero-coupon bonds of various maturities. Maturity (Years) Bond AWNA Price $930 $850 $770 $700 1.4 a. Compute the zero-coupon rates for years 1, 2, 3 and 4. b. Consider an 8% coupon $1,000 par bond (denoted by B) paying annual coupons and expiring in 4 years. Compute the no-arbitrage price of the bond and its yield-to-maturity. c. If the expectations hypothesis holds, what is your...

QUESTIONS Consider the performance of two securities and k over the five year period from 2014...

QUESTIONS Consider the performance of two securities and k over the five year period from 2014 to 2018. The annual return earned on each one of them is as provided in the table below Year 379 28.4 -15 a 2014 2015 2016 2017 2018 19.8 128 -208 58.6 -500 31.7 Required: Compute the following: a) Assume your organization had K150 million to invest on 01st January, 2014. If 70% was invested in security J over the holding period, the annual...

QUESTIONS Consider the performance of two securities and k over the five year period from 2014 to 2018. The annual return earned on each one of them is as provided in the table below Year 379 28.4 -15 a 2014 2015 2016 2017 2018 19.8 128 -208 58.6 -500 31.7 Required: Compute the following: a) Assume your organization had K150 million to invest on 01st January, 2014. If 70% was invested in security J over the holding period, the annual...

Questions 1 to 10 are false statements. Please re-write each statement so that it is true....

Questions 1 to 10 are false statements. Please re-write each statement so that it is true. It may be as simple as one word change or more complex. 3. Money market security prices and yields are more sensitive to changes in interest rates than long-term corporate bonds. 4. The majority of money market securities are low denomination, low risk investments designed to appeal to individual investors with excess cash. 5. Most money market securities are initially sold to individual investors....

Can) ou are in the process of purchasing a new automobile that will cost you $27,500....

Can) ou are in the process of purchasing a new automobile that will cost you $27,500. The dealership is offering you either a $2,500 rebate (applied toward the purchase price) or financing at a 0.9% APR for 48 months (with payments made at the end of the month) and no rebate. You have been pre-approved for an auto loan through your local credit union at an interest rate of 5.5% APR for 48 months. If you take the $2,500 rebate...

Can) ou are in the process of purchasing a new automobile that will cost you $27,500. The dealership is offering you either a $2,500 rebate (applied toward the purchase price) or financing at a 0.9% APR for 48 months (with payments made at the end of the month) and no rebate. You have been pre-approved for an auto loan through your local credit union at an interest rate of 5.5% APR for 48 months. If you take the $2,500 rebate...

My question is Q 6, diversification. thank you Chapter 13 Retum, Risk and the Security Market...

My question is Q 6, diversification. thank you

Chapter 13 Retum, Risk and the Security Market Line 5. Expected Portfoli d. The directors of Big Widget die in a plane crash. Congress approves changes to the tax code that will increase the top marginal corporate tax rate. The legisla orate tax rate. The legislation had been debated for the previous six months. ed Portfolio Returns (LO1] If a portfolio has a positive investment in every at can the expected return...

My question is Q 6, diversification. thank you

Chapter 13 Retum, Risk and the Security Market Line 5. Expected Portfoli d. The directors of Big Widget die in a plane crash. Congress approves changes to the tax code that will increase the top marginal corporate tax rate. The legisla orate tax rate. The legislation had been debated for the previous six months. ed Portfolio Returns (LO1] If a portfolio has a positive investment in every at can the expected return...

Can someone please help me with this? Using the following sample data size of 30 homes for the fo...

Can someone please help me with this? Using the following sample

data size of 30 homes for the following variables; variable a) is

address, variable b) is asking price, variable c) is square

footage, variable d) is number of days on market and variable e) is

cost per square foot, please answer the following below.

1) for variables b-e(asking price, square footage, number of

days on market and cost per square foot, determine 96% confidence

interval and interpret each result...

Can someone please help me with this? Using the following sample

data size of 30 homes for the following variables; variable a) is

address, variable b) is asking price, variable c) is square

footage, variable d) is number of days on market and variable e) is

cost per square foot, please answer the following below.

1) for variables b-e(asking price, square footage, number of

days on market and cost per square foot, determine 96% confidence

interval and interpret each result...

Can someone please tell me what chapters (1-5) these questions are based on? I have already answered the questions and u...

Can someone please tell me what chapters (1-5) these questions

are based on? I have already answered the questions and understand

how to solve the material, but i want to be able to pinpoint where

i can find this info. in the book. I am using Brigham’s

Fundamentals of Financial Management (pictures attached). If it is

hard to read, please let me know. i will post better pictures. i

know the time vale of money stuff already

EDIT: HERE IS...

Can someone please tell me what chapters (1-5) these questions

are based on? I have already answered the questions and understand

how to solve the material, but i want to be able to pinpoint where

i can find this info. in the book. I am using Brigham’s

Fundamentals of Financial Management (pictures attached). If it is

hard to read, please let me know. i will post better pictures. i

know the time vale of money stuff already

EDIT: HERE IS...

Can anybody help me with these questions pls Questions 1-10 are based on the following information....

Can

anybody help me with these questions pls

Questions 1-10 are based on the following information. Bond valuation. On Jan. 1. 2008, your cousin, Laura, purchased one 3-year semiannual bond with a coupon rate of 8%. The yield of the bond was at the time 1. How much did Laura pay for the hond a. 974.21 b. 974,69 c. 1.000 d767.90 2. This bond was a a discount bond b. premium bend c. par band d. all of the above....

Can

anybody help me with these questions pls

Questions 1-10 are based on the following information. Bond valuation. On Jan. 1. 2008, your cousin, Laura, purchased one 3-year semiannual bond with a coupon rate of 8%. The yield of the bond was at the time 1. How much did Laura pay for the hond a. 974.21 b. 974,69 c. 1.000 d767.90 2. This bond was a a discount bond b. premium bend c. par band d. all of the above....

Can someone help me with this question. I was assuming a 1% ytm

for C and D but not sure if I did it correctly.

Consider the following risk-free securities available to buy or sell to all investors in the market: 6. Cash flow (t=2) Price (t=0) Cash flow (t=1) Cash flow (t=3) Security 76 80 120 68 80 216 80 80 80 D 102 a) Compute the YTM offered by securities A and C. b) Write-down the equation that...

Can someone help me with this question. I was assuming a 1% ytm

for C and D but not sure if I did it correctly.

Consider the following risk-free securities available to buy or sell to all investors in the market: 6. Cash flow (t=2) Price (t=0) Cash flow (t=1) Cash flow (t=3) Security 76 80 120 68 80 216 80 80 80 D 102 a) Compute the YTM offered by securities A and C. b) Write-down the equation that...

Consider two securities that pay risk-free cash flows over the next two years and that have the current market prices shown here: Security B1 Price Today $90 $72 Cash Flow in one Year Cash Flow in Two Years $100 $0 $0 $80 | B2 a) What is the no-arbitrage price of a security that pays cash flows of $100 in one year and $80 in two years? [2 points] b) What is the no-arbitrage price of a security that pays...

Consider two securities that pay risk-free cash flows over the next two years and that have the current market prices shown here: Security B1 Price Today $90 $72 Cash Flow in one Year Cash Flow in Two Years $100 $0 $0 $80 | B2 a) What is the no-arbitrage price of a security that pays cash flows of $100 in one year and $80 in two years? [2 points] b) What is the no-arbitrage price of a security that pays...

Help with finance question please.

7. Below is a list of prices for $1,000 par zero-coupon bonds of various maturities. Maturity (Years) Bond AWNA Price $930 $850 $770 $700 1.4 a. Compute the zero-coupon rates for years 1, 2, 3 and 4. b. Consider an 8% coupon $1,000 par bond (denoted by B) paying annual coupons and expiring in 4 years. Compute the no-arbitrage price of the bond and its yield-to-maturity. c. If the expectations hypothesis holds, what is your...

Help with finance question please.

7. Below is a list of prices for $1,000 par zero-coupon bonds of various maturities. Maturity (Years) Bond AWNA Price $930 $850 $770 $700 1.4 a. Compute the zero-coupon rates for years 1, 2, 3 and 4. b. Consider an 8% coupon $1,000 par bond (denoted by B) paying annual coupons and expiring in 4 years. Compute the no-arbitrage price of the bond and its yield-to-maturity. c. If the expectations hypothesis holds, what is your...

QUESTIONS Consider the performance of two securities and k over the five year period from 2014 to 2018. The annual return earned on each one of them is as provided in the table below Year 379 28.4 -15 a 2014 2015 2016 2017 2018 19.8 128 -208 58.6 -500 31.7 Required: Compute the following: a) Assume your organization had K150 million to invest on 01st January, 2014. If 70% was invested in security J over the holding period, the annual...

QUESTIONS Consider the performance of two securities and k over the five year period from 2014 to 2018. The annual return earned on each one of them is as provided in the table below Year 379 28.4 -15 a 2014 2015 2016 2017 2018 19.8 128 -208 58.6 -500 31.7 Required: Compute the following: a) Assume your organization had K150 million to invest on 01st January, 2014. If 70% was invested in security J over the holding period, the annual...

Can) ou are in the process of purchasing a new automobile that will cost you $27,500. The dealership is offering you either a $2,500 rebate (applied toward the purchase price) or financing at a 0.9% APR for 48 months (with payments made at the end of the month) and no rebate. You have been pre-approved for an auto loan through your local credit union at an interest rate of 5.5% APR for 48 months. If you take the $2,500 rebate...

Can) ou are in the process of purchasing a new automobile that will cost you $27,500. The dealership is offering you either a $2,500 rebate (applied toward the purchase price) or financing at a 0.9% APR for 48 months (with payments made at the end of the month) and no rebate. You have been pre-approved for an auto loan through your local credit union at an interest rate of 5.5% APR for 48 months. If you take the $2,500 rebate...

My question is Q 6, diversification. thank you

Chapter 13 Retum, Risk and the Security Market Line 5. Expected Portfoli d. The directors of Big Widget die in a plane crash. Congress approves changes to the tax code that will increase the top marginal corporate tax rate. The legisla orate tax rate. The legislation had been debated for the previous six months. ed Portfolio Returns (LO1] If a portfolio has a positive investment in every at can the expected return...

My question is Q 6, diversification. thank you

Chapter 13 Retum, Risk and the Security Market Line 5. Expected Portfoli d. The directors of Big Widget die in a plane crash. Congress approves changes to the tax code that will increase the top marginal corporate tax rate. The legisla orate tax rate. The legislation had been debated for the previous six months. ed Portfolio Returns (LO1] If a portfolio has a positive investment in every at can the expected return...

Can someone please help me with this? Using the following sample

data size of 30 homes for the following variables; variable a) is

address, variable b) is asking price, variable c) is square

footage, variable d) is number of days on market and variable e) is

cost per square foot, please answer the following below.

1) for variables b-e(asking price, square footage, number of

days on market and cost per square foot, determine 96% confidence

interval and interpret each result...

Can someone please help me with this? Using the following sample

data size of 30 homes for the following variables; variable a) is

address, variable b) is asking price, variable c) is square

footage, variable d) is number of days on market and variable e) is

cost per square foot, please answer the following below.

1) for variables b-e(asking price, square footage, number of

days on market and cost per square foot, determine 96% confidence

interval and interpret each result...

Can someone please tell me what chapters (1-5) these questions

are based on? I have already answered the questions and understand

how to solve the material, but i want to be able to pinpoint where

i can find this info. in the book. I am using Brigham’s

Fundamentals of Financial Management (pictures attached). If it is

hard to read, please let me know. i will post better pictures. i

know the time vale of money stuff already

EDIT: HERE IS...

Can someone please tell me what chapters (1-5) these questions

are based on? I have already answered the questions and understand

how to solve the material, but i want to be able to pinpoint where

i can find this info. in the book. I am using Brigham’s

Fundamentals of Financial Management (pictures attached). If it is

hard to read, please let me know. i will post better pictures. i

know the time vale of money stuff already

EDIT: HERE IS...

Can

anybody help me with these questions pls

Questions 1-10 are based on the following information. Bond valuation. On Jan. 1. 2008, your cousin, Laura, purchased one 3-year semiannual bond with a coupon rate of 8%. The yield of the bond was at the time 1. How much did Laura pay for the hond a. 974.21 b. 974,69 c. 1.000 d767.90 2. This bond was a a discount bond b. premium bend c. par band d. all of the above....

Can

anybody help me with these questions pls

Questions 1-10 are based on the following information. Bond valuation. On Jan. 1. 2008, your cousin, Laura, purchased one 3-year semiannual bond with a coupon rate of 8%. The yield of the bond was at the time 1. How much did Laura pay for the hond a. 974.21 b. 974,69 c. 1.000 d767.90 2. This bond was a a discount bond b. premium bend c. par band d. all of the above....

Most questions answered within 3 hours.

-

Suppose that XX is a random variable with mean 16 and standard

deviation 5 . Also...

asked 21 minutes ago -

Calculate the number density of argon gas at a temperature of

24C and a pressure of...

asked 3 hours ago -

Alternative

Classification

How to Estimate

Probabilities from Data? ( For continuous Attributes)

And How to generate...

asked 3 hours ago -

An explosion breaks a 20.0-kg object into three parts. The

object is initially moving at a...

asked 4 hours ago -

Calculate the approximate number of residues of Rubisco, which

is involved in carbon fixation in plants,...

asked 5 hours ago -

Other decisions about scientific claims can have a much broader

impact.ENERGYarrow-10x10.png, environment, health, security - all...

asked 6 hours ago -

I need to write a research paper and work cited about this

topic: The United States...

asked 6 hours ago -

Hello! I was wondering if I could have some help?

If the vapor pressure of carvone...

asked 7 hours ago -

An economist wants to estimate the mean per capita income (in

thousands of dollars) for a...

asked 7 hours ago -

What would be the input/output characteristic of a circuit

obtained by putting two of your 2's-complementers...

asked 7 hours ago -

In Drosophila, the transition from the syncytial blastoderm

stage to the cellular blastoderm stage is a...

asked 7 hours ago -

Project management question:

Name 3 different types of resources (hint: humans are one

type)

asked 8 hours ago