Homework Answers

The saving of 68basis points is shared between both companies in order to get equal or same borrowing cost.

Add Answer to:

Company Econ can borrow USD 10 million from Bank A for 2 years at a fixed...

Company A prefer fixed rate and can borrow from Bank A. Bank A's Pricing Schedule Fixed...

Company A prefer fixed rate and can borrow from Bank A. Bank A's Pricing Schedule Fixed interest Floating interest rate 9% LIBOR + 0.34% Bank A takes a commission of 0.2% Company B prefer floating rate and can borrow from Bank B. Bank B's Pricing Schedule Fixed interest Floating interest rate 7.7% LIBOR + 0.3% Bank B takes a commission of 0.3% . Both companies enter into an interest rate swap, what is the total cost saving? • If 40%...

Company A prefer fixed rate and can borrow from Bank A. Bank A's Pricing Schedule Fixed interest Floating interest rate 9% LIBOR + 0.34% Bank A takes a commission of 0.2% Company B prefer floating rate and can borrow from Bank B. Bank B's Pricing Schedule Fixed interest Floating interest rate 7.7% LIBOR + 0.3% Bank B takes a commission of 0.3% . Both companies enter into an interest rate swap, what is the total cost saving? • If 40%...

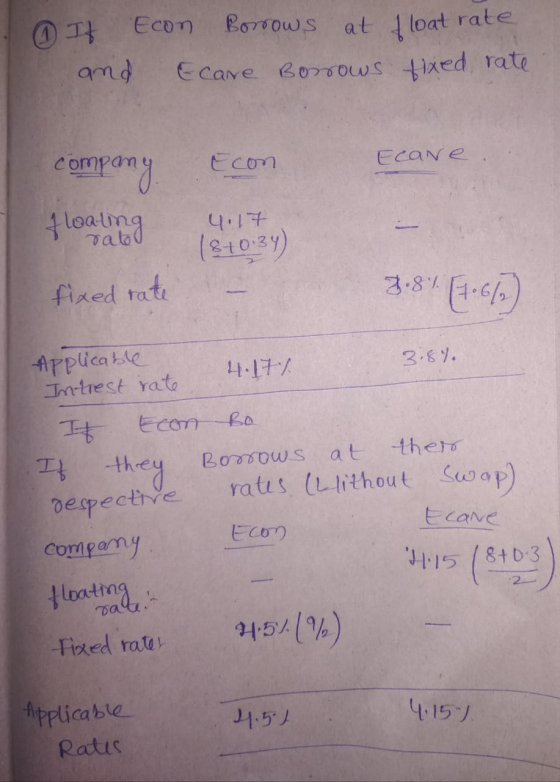

Financial Derivatives (FIN429) Tuesday 07-May-2019 QUESTION # 10 Max. Marks 10-4+2+2+2] o. prefers to borrow at...

Financial Derivatives (FIN429) Tuesday 07-May-2019 QUESTION # 10 Max. Marks 10-4+2+2+2] o. prefers to borrow at fl Co. and Cocoa Co. want to borrow USD 150 million for 10 years. Monoca at Hoating rate of interest, while Cocoa Co. has a preference to borrow at interest. Suppose that National Bank offers the followings to Monoca Co. and Cocoa Companies Quotes Fixed LIBOR-1% | 85% Monoca Co. | LIBOR+ 1.5% 9.5% Floating F cocoa Co. | aronl b hee e 1....

Financial Derivatives (FIN429) Tuesday 07-May-2019 QUESTION # 10 Max. Marks 10-4+2+2+2] o. prefers to borrow at fl Co. and Cocoa Co. want to borrow USD 150 million for 10 years. Monoca at Hoating rate of interest, while Cocoa Co. has a preference to borrow at interest. Suppose that National Bank offers the followings to Monoca Co. and Cocoa Companies Quotes Fixed LIBOR-1% | 85% Monoca Co. | LIBOR+ 1.5% 9.5% Floating F cocoa Co. | aronl b hee e 1....

Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow $10,000,000...

Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow $10,000,000 fixed for 5 years. Their external borrowing opportunities are shown here: Fixed-Rate Borrowing Cost Floating-Rate Borrowing Cost LIBOR LIBOR + 1.5% Company X Company Y 10% 12% A swap bank proposes the following interest only swap: Y will pay the swap bank annual payments on $10,000,000 with a fixed rate of rate of 9.90 percent. In exchange the swap bank will pay to company...

Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow $10,000,000 fixed for 5 years. Their external borrowing opportunities are shown here: Fixed-Rate Borrowing Cost Floating-Rate Borrowing Cost LIBOR LIBOR + 1.5% Company X Company Y 10% 12% A swap bank proposes the following interest only swap: Y will pay the swap bank annual payments on $10,000,000 with a fixed rate of rate of 9.90 percent. In exchange the swap bank will pay to company...

Company X wants to borrow $10,000,000 floating for 5 years & company Y wants to borrow...

Company X wants to borrow $10,000,000 floating for 5 years & company Y wants to borrow $10,000,000 fixed for 5 years. Company X and Y fixed rate borrowing costs are 10% and 12% respectively Company X and Y floating rate borrowing costs are LIBOR and LIBOR plus 1.5% respectively A swap bank proposes the following interest only swap X will pay the swap bank annual payments on $10,000,000 with the coupon rate of LIBOR- 0.15%, in exchange the swap bank...

Company X wants to borrow $10,000,000 floating for 5 years & company Y wants to borrow $10,000,000 fixed for 5 years. Company X and Y fixed rate borrowing costs are 10% and 12% respectively Company X and Y floating rate borrowing costs are LIBOR and LIBOR plus 1.5% respectively A swap bank proposes the following interest only swap X will pay the swap bank annual payments on $10,000,000 with the coupon rate of LIBOR- 0.15%, in exchange the swap bank...

Company X wants to borrow $10,000,000 floating for 5 years & company Y wants to borrow...

Company X wants to borrow $10,000,000 floating for 5 years & company Y wants to borrow $10,000,000 fixed for 5 years. Company X and Y fixed rate borrowing costs are 10% and 12% respectively Company X and Y floating rate borrowing costs are LIBOR and LIBOR plus 1.5% respectively. A swap bank proposes the following interest only swap Y will pay the swap bank annual payments on $10,000,000 with a fixed rate of rate of 9.90%. In exchange the swap...

Company X wants to borrow $10,000,000 floating for 5 years & company Y wants to borrow $10,000,000 fixed for 5 years. Company X and Y fixed rate borrowing costs are 10% and 12% respectively Company X and Y floating rate borrowing costs are LIBOR and LIBOR plus 1.5% respectively. A swap bank proposes the following interest only swap Y will pay the swap bank annual payments on $10,000,000 with a fixed rate of rate of 9.90%. In exchange the swap...

Company A wishes to borrow U.S. dollars at a fixed rate of interest. Company B wishes...

Company A wishes to borrow U.S. dollars at a fixed rate of interest. Company B wishes to borrow sterling (British Pounds) at a fixed rate of interest. They have been quoted the following rates per annum (adjusted for differential tax effects): Sterling US Dollars Company A 11.0% 7.0% Company B 10.6% 6.2% Design a swap that will net a bank, acting as intermediary, 10 basis points per annum and that will produce a gain of 15 basis points per annum...

QUESTION 1 Company X wants to borrow $10,000,000 floating for 5 years & company Y wants...

QUESTION 1 Company X wants to borrow $10,000,000 floating for 5 years & company Y wants to borrow $10,000,000 fixed for 5 years. Company X and Y fixed rate borrowing costs are 10% and 12% respectively. Company X and Y floating rate borrowing costs are LIBOR and LIBOR plus 1.5% respectively. A swap bank proposes the following interest only swap X will pay the swap bank annual payments on $10,000,000 with the coupon rate of LIBOR -0.15 percent; in exchange...

QUESTION 1 Company X wants to borrow $10,000,000 floating for 5 years & company Y wants to borrow $10,000,000 fixed for 5 years. Company X and Y fixed rate borrowing costs are 10% and 12% respectively. Company X and Y floating rate borrowing costs are LIBOR and LIBOR plus 1.5% respectively. A swap bank proposes the following interest only swap X will pay the swap bank annual payments on $10,000,000 with the coupon rate of LIBOR -0.15 percent; in exchange...

Firm ABC needs to borrow $1 million at a floating rate. In the market, firm ABC...

Firm ABC needs to borrow $1 million at a floating rate. In the market, firm ABC can borrow at 13% fixed rate per year or a floating rate equal to LIBOR. A swap bank proposes a swap contract. Firm ABC pays the swap bank a floating rate equal to LIBOR + 1% per year, and the swap bank pays firm ABC a fixed rate 15% per year. If firm ABC borrows $1 million at 13% fixed rate and gets into...

Companies A and B have been offered the following rates per annum on a $20 million...

Companies A and B have been offered the following rates per annum on a $20 million 5-year loan, and a bank, acting as intermediary, will charge 0.10% per annum (10 basis points) to arrange and manage the swap, which appears equally attractive to A and B. Fixed Rate Floating Rate Company A 6.0% LIBOR Company B 7.2% LIBOR + 0.50% Company A requires a floating-rate loan, and company B requires a fixed-rate loan. If Company A pays LIBOR to the...

Companies A and B have been offered the following rates per annum on a $20 million...

Companies A and B have been offered the following rates per annum on a $20 million 5-year loan, and a bank, acting as intermediary, will charge 0.10% per annum (10 basis points) to arrange and manage the swap, which appears equally attractive to A and B. Fixed Rate Floating Rate Company A 6.0% LIBOR Company B 7.2% LIBOR + 0.50% Company A requires a floating-rate loan, and company B requires a fixed-rate loan. If Company A pays LIBOR to the...

Company A prefer fixed rate and can borrow from Bank A. Bank A's Pricing Schedule Fixed interest Floating interest rate 9% LIBOR + 0.34% Bank A takes a commission of 0.2% Company B prefer floating rate and can borrow from Bank B. Bank B's Pricing Schedule Fixed interest Floating interest rate 7.7% LIBOR + 0.3% Bank B takes a commission of 0.3% . Both companies enter into an interest rate swap, what is the total cost saving? • If 40%...

Company A prefer fixed rate and can borrow from Bank A. Bank A's Pricing Schedule Fixed interest Floating interest rate 9% LIBOR + 0.34% Bank A takes a commission of 0.2% Company B prefer floating rate and can borrow from Bank B. Bank B's Pricing Schedule Fixed interest Floating interest rate 7.7% LIBOR + 0.3% Bank B takes a commission of 0.3% . Both companies enter into an interest rate swap, what is the total cost saving? • If 40%...

Financial Derivatives (FIN429) Tuesday 07-May-2019 QUESTION # 10 Max. Marks 10-4+2+2+2] o. prefers to borrow at fl Co. and Cocoa Co. want to borrow USD 150 million for 10 years. Monoca at Hoating rate of interest, while Cocoa Co. has a preference to borrow at interest. Suppose that National Bank offers the followings to Monoca Co. and Cocoa Companies Quotes Fixed LIBOR-1% | 85% Monoca Co. | LIBOR+ 1.5% 9.5% Floating F cocoa Co. | aronl b hee e 1....

Financial Derivatives (FIN429) Tuesday 07-May-2019 QUESTION # 10 Max. Marks 10-4+2+2+2] o. prefers to borrow at fl Co. and Cocoa Co. want to borrow USD 150 million for 10 years. Monoca at Hoating rate of interest, while Cocoa Co. has a preference to borrow at interest. Suppose that National Bank offers the followings to Monoca Co. and Cocoa Companies Quotes Fixed LIBOR-1% | 85% Monoca Co. | LIBOR+ 1.5% 9.5% Floating F cocoa Co. | aronl b hee e 1....

Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow $10,000,000 fixed for 5 years. Their external borrowing opportunities are shown here: Fixed-Rate Borrowing Cost Floating-Rate Borrowing Cost LIBOR LIBOR + 1.5% Company X Company Y 10% 12% A swap bank proposes the following interest only swap: Y will pay the swap bank annual payments on $10,000,000 with a fixed rate of rate of 9.90 percent. In exchange the swap bank will pay to company...

Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow $10,000,000 fixed for 5 years. Their external borrowing opportunities are shown here: Fixed-Rate Borrowing Cost Floating-Rate Borrowing Cost LIBOR LIBOR + 1.5% Company X Company Y 10% 12% A swap bank proposes the following interest only swap: Y will pay the swap bank annual payments on $10,000,000 with a fixed rate of rate of 9.90 percent. In exchange the swap bank will pay to company...

Company X wants to borrow $10,000,000 floating for 5 years & company Y wants to borrow $10,000,000 fixed for 5 years. Company X and Y fixed rate borrowing costs are 10% and 12% respectively Company X and Y floating rate borrowing costs are LIBOR and LIBOR plus 1.5% respectively A swap bank proposes the following interest only swap X will pay the swap bank annual payments on $10,000,000 with the coupon rate of LIBOR- 0.15%, in exchange the swap bank...

Company X wants to borrow $10,000,000 floating for 5 years & company Y wants to borrow $10,000,000 fixed for 5 years. Company X and Y fixed rate borrowing costs are 10% and 12% respectively Company X and Y floating rate borrowing costs are LIBOR and LIBOR plus 1.5% respectively A swap bank proposes the following interest only swap X will pay the swap bank annual payments on $10,000,000 with the coupon rate of LIBOR- 0.15%, in exchange the swap bank...

Company X wants to borrow $10,000,000 floating for 5 years & company Y wants to borrow $10,000,000 fixed for 5 years. Company X and Y fixed rate borrowing costs are 10% and 12% respectively Company X and Y floating rate borrowing costs are LIBOR and LIBOR plus 1.5% respectively. A swap bank proposes the following interest only swap Y will pay the swap bank annual payments on $10,000,000 with a fixed rate of rate of 9.90%. In exchange the swap...

Company X wants to borrow $10,000,000 floating for 5 years & company Y wants to borrow $10,000,000 fixed for 5 years. Company X and Y fixed rate borrowing costs are 10% and 12% respectively Company X and Y floating rate borrowing costs are LIBOR and LIBOR plus 1.5% respectively. A swap bank proposes the following interest only swap Y will pay the swap bank annual payments on $10,000,000 with a fixed rate of rate of 9.90%. In exchange the swap...

QUESTION 1 Company X wants to borrow $10,000,000 floating for 5 years & company Y wants to borrow $10,000,000 fixed for 5 years. Company X and Y fixed rate borrowing costs are 10% and 12% respectively. Company X and Y floating rate borrowing costs are LIBOR and LIBOR plus 1.5% respectively. A swap bank proposes the following interest only swap X will pay the swap bank annual payments on $10,000,000 with the coupon rate of LIBOR -0.15 percent; in exchange...

QUESTION 1 Company X wants to borrow $10,000,000 floating for 5 years & company Y wants to borrow $10,000,000 fixed for 5 years. Company X and Y fixed rate borrowing costs are 10% and 12% respectively. Company X and Y floating rate borrowing costs are LIBOR and LIBOR plus 1.5% respectively. A swap bank proposes the following interest only swap X will pay the swap bank annual payments on $10,000,000 with the coupon rate of LIBOR -0.15 percent; in exchange...

Most questions answered within 3 hours.

-

A regression equation that describes the relationship between

the amount of the bill ($) at a...

asked 43 minutes ago -

exercise on VSEPR and molecular structrue.

octahedral

SeCl62-

TeCl62-

ClF62-

distorted

SeF62–

IF6–

asked 1 hour ago -

284 mL of a 0.52 M potassium hydroxide solution is added to 467

mL of a...

asked 1 hour ago -

Little’s Law: Val d’Costa is a world famous ski village in the

French Alps. Because of...

asked 2 hours ago -

Find the absolute error D for the calculation if A + B/C=D A=

9.4 +/- 0.4...

asked 2 hours ago -

New Air Heating and Cooling, manufactures furnaces and central

air units. The company pride itself on...

asked 2 hours ago -

A coach uses a new technique to train gymnasts. Seven

gymnasts were randomly selected and their...

asked 4 hours ago -

While rotating the tires on your car you notice a rock [mass =

0.1 Kg] stuck...

asked 6 hours ago -

Using MARS simulator, write MIPS programs according to

the following scenarios: Receive a positive integer number...

asked 8 hours ago -

An object in front of a concave mirror has a real image that is

11.5 cm...

asked 8 hours ago -

Consider the reaction, C3 H8 + O2 --> CO2 + H2O. How many

moles of O2...

asked 10 hours ago -

You and your opponent both roll a fair die. If you both roll the

same number,...

asked 10 hours ago