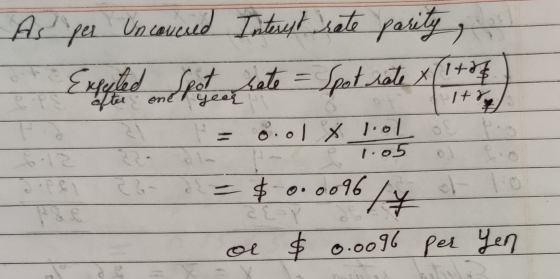

Assume that uncovered interest rate parity holds between the Japanese yen and the U.S. dollar. If...

Assume that uncovered interest rate parity holds between the Japanese yen and the U.S. dollar. If today the 1-year riskless interest rate in Japan is 5%, the one-year riskless interest rate in the U.S. is 1%, and the spot exchange rate is $.01 per yen, what is the expected exchange rate one-year from today? Suppose that expected inflation in the U.S. increased. What would happen to the current (spot) exchange, i.e. will it increase or decrease? Explain your reasoning.

Homework Answers

As per purchasing power parity which is a relationship between exchange rate and inflation says that if inflation is high in the particular country then its expected spot rate will be lower than current spot rate

Hence if expected inflation in the US increased then its expected spot rate of dollar will be lower and hence expected spot rate of yen will increase.

Hence in that case spot rate $0.01 per yen will increase

Add Answer to:

Assume that uncovered interest rate parity holds between the

Japanese yen and the U.S. dollar. If...

Assume interest rate parity holds. The one-year risk-free rate in the U.S. is 4.02 percent and...

Assume interest rate parity holds. The one-year risk-free rate in the U.S. is 4.02 percent and the one-year risk-free rate in Japan is 4.35 percent. The spot rate between the Japanese yen and the U.S. dollar is ¥114.33/$. What is the one-year forward exchange rate? Multiple Choice ¥117.53/$ ¥114.33/$ ¥113.97/$ ¥114.69/$ ¥116.56/$

a) If the dollar is expected to appreciate against the yen, uncovered interest parity implies that...

a) If the dollar is expected to appreciate against the yen, uncovered interest parity implies that the U.S. nominal interest rate must be greater than the Japanese nominal interest rate.

The spot rate between the Japanese yen and the U.S. dollar is ¥106.57/$, while the one-year...

The spot rate between the Japanese yen and the U.S. dollar is ¥106.57/$, while the one-year forward rate is ¥105.73/$. The one-year risk-free rate in the U.S. is 2.39 percent. If interest rate parity exists, what is the one-year risk-free rate in Japan?

Derek Tosh and Yen-Dollar Parity. Derek Tosh is attempting to determine whether US/Japanese financial conditions are...

Derek Tosh and Yen-Dollar Parity. Derek Tosh is attempting to determine whether US/Japanese financial conditions are at parity. The current spot rate is a flat ¥89.00/$, while the 360-day forward rate is ¥84.90/$. Forecast inflation is 1.099% for Japan, and 5.896% for the US. The 360-day euro-yen deposit rate is 4.703%, and the 360-day euro-dollar deposit rate is 9.498%. a. Calculate whether international parity conditions hold between Japan and the United States. b. Find the forecasted change in the Japanese...

Assume that interest rate parity holds. In the spot market 1 Japanese yen = $0.01081, while...

Assume that interest rate parity holds. In the spot market 1 Japanese yen = $0.01081, while in the 90-day forward market 1 Japanese yen = $0.01084. In Japan, 90-day risk-free securities yield 2.1%. What is the yield on 90-day risk-free securities in the United States? Round your answer to two decimal places. Do not round intermediate calculations.

Assume that interest rate parity holds. In the spot market 1 Japanese yen = $0.011, while...

Assume that interest rate parity holds. In the spot market 1 Japanese yen = $0.011, while in the 180-day forward market 1 Japanese yen = $0.0118. 180-day risk-free securities yield 1.4% in Japan. What is the yield on 180-day risk-free securities in the United States? Do not round intermediate calculations. Round your answer to two decimal places.

Assume that interest rate parity holds. In the spot market 1 Japanese yen = $0.011, while...

Assume that interest rate parity holds. In the spot market 1 Japanese yen = $0.011, while in the 180-day forward market 1 Japanese yen = $0.0112. 180-day risk-free securities yield 1.30% in Japan. What is the yield on 180-day risk-free securities in the United States? Do not round intermediate calculations. Round your answer to two decimal places.

Assume that interest rate parity holds. In the spot market 1 Japanese yen = $0.01392, while...

Assume that interest rate parity holds. In the spot market 1 Japanese yen = $0.01392, while in the 90-day forward market 1 Japanese yen = $0.01395. In Japan, 90-day risk-free securities yield 2.5%. What is the yield on 90-day risk-free securities in the United States? Round your answer to two decimal places. Do not round intermediate calculations. %

Quantitative Problem: Assume that interest rate parity holds. In the spot market 1 Japanese yen =...

Quantitative Problem: Assume that interest rate parity holds. In the spot market 1 Japanese yen = $0.009, while in the 180-day forward market 1 Japanese yen = $0.0093. 180-day risk-free securities yield 1.3% in Japan. What is the yield on 180-day risk-free securities in the United States? Do not round intermediate calculations. Round your answer to two decimal places.

Uncovered Interest Parity Explain the uncovered interest parity equation. (Write it and explain it). a. b. Why would we expect it to hold? l.e. what would happen if the equation does not hold? Assume...

Uncovered Interest Parity Explain the uncovered interest parity equation. (Write it and explain it). a. b. Why would we expect it to hold? l.e. what would happen if the equation does not hold? Assume the expected $/Yen exchange rate is 0.01 dollars per yen. Further assume that the US interest rate is 8% and the Japanese interest rate is 3%. According to uncovered interest parity, what would be the current S/Yen exchange rate? Show work. c.

Uncovered Interest Parity Explain...

Uncovered Interest Parity Explain the uncovered interest parity equation. (Write it and explain it). a. b. Why would we expect it to hold? l.e. what would happen if the equation does not hold? Assume the expected $/Yen exchange rate is 0.01 dollars per yen. Further assume that the US interest rate is 8% and the Japanese interest rate is 3%. According to uncovered interest parity, what would be the current S/Yen exchange rate? Show work. c.

Uncovered Interest Parity Explain...

Uncovered Interest Parity Explain the uncovered interest parity equation. (Write it and explain it). a. b. Why would we expect it to hold? l.e. what would happen if the equation does not hold? Assume the expected $/Yen exchange rate is 0.01 dollars per yen. Further assume that the US interest rate is 8% and the Japanese interest rate is 3%. According to uncovered interest parity, what would be the current S/Yen exchange rate? Show work. c.

Uncovered Interest Parity Explain...

Uncovered Interest Parity Explain the uncovered interest parity equation. (Write it and explain it). a. b. Why would we expect it to hold? l.e. what would happen if the equation does not hold? Assume the expected $/Yen exchange rate is 0.01 dollars per yen. Further assume that the US interest rate is 8% and the Japanese interest rate is 3%. According to uncovered interest parity, what would be the current S/Yen exchange rate? Show work. c.

Uncovered Interest Parity Explain...

Most questions answered within 3 hours.

-

a) Draw two water molecules.

b) Clearly name and label the type of bond that exists...

asked 59 minutes ago -

C - Language

Write a loop that sets each array element to the sum of itself...

asked 2 hours ago -

(63

#14)

which of the following statments best describes how chamging

the concentration of the substances...

asked 5 hours ago -

In the following reaction, which element is undergoing

oxidation: Na2SO3 + N2O --> N2 + Na2SO4...

asked 6 hours ago -

Which of the following pairs of ions have the same electron

configuration?

I: Br− and Se2−...

asked 9 hours ago -

The Foremost Composite Materials Company is planning a two-day

sales conference for October 19-20. The conference...

asked 9 hours ago -

3) Illustrate the observed pattern of relatedness of organisms

versus adaptations to specific conditions. This means...

asked 9 hours ago -

In winter a lake has a 0.35 m thick ice layer over 1.10 m of

water....

asked 10 hours ago -

Assuming the following has been encrypted with a Vigenere cipher

below, use the method(s) and assumptions...

asked 11 hours ago -

How would I use switch statements to write a program that will

take an input of...

asked 10 hours ago -

Imagine a reaction in which methane gas combusts at a constant

pressure of 1 atm and...

asked 11 hours ago -

Two parallel wires (each 12 m in length) are separated by a

distance of 0.065 m...

asked 11 hours ago