Homework Answers

Add Answer to:

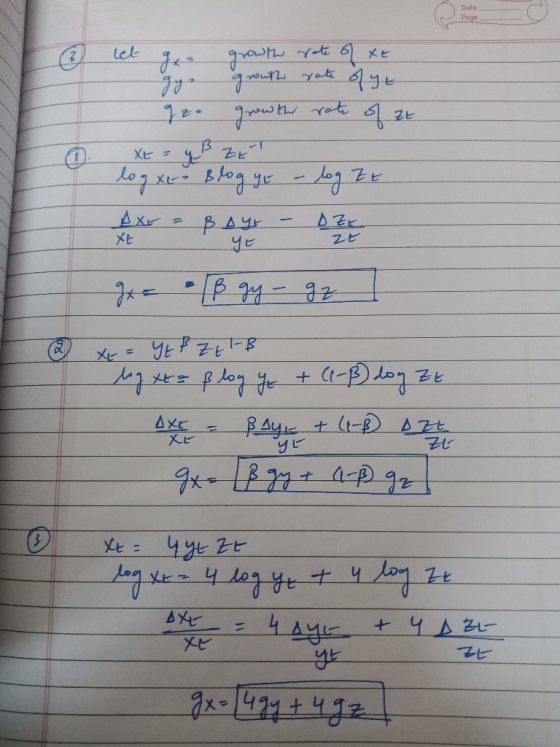

Problem 3 Express growth rates for xt in terms of growth rates of Yt and zt....

Zt is a function of Xt, Y4 and Ut. Express the growth rate of Zų as...

Zt is a function of Xt, Y4 and Ut. Express the growth rate of Zų as a function of growth rates of Xt, Yt and Ut for the following cases (no need to show the intermediate steps): Question 4.1 [5 points Zt = X Y3 Question 4.2 (5 points) Zt Question 4.3 [5 points) Z4 = VX+Y4

Zt is a function of Xt, Y4 and Ut. Express the growth rate of Zų as a function of growth rates of Xt, Yt and Ut for the following cases (no need to show the intermediate steps): Question 4.1 [5 points Zt = X Y3 Question 4.2 (5 points) Zt Question 4.3 [5 points) Z4 = VX+Y4

Problem 3 Consider a random walk on the integers. Suppose we start from 0, and at each step, we either go left or right with probability 1/2, ie, Xo--0, and Xt+1 Xt+Zt, where Zt-1 with probability 1/...

Problem 3 Consider a random walk on the integers. Suppose we start from 0, and at each step, we either go left or right with probability 1/2, ie, Xo--0, and Xt+1 Xt+Zt, where Zt-1 with probability 1/2, and Zt1 with probability 1/2. What is the probability distribution of XT? What is E(X) and Var(XT)?

Problem 3 Consider a random walk on the integers. Suppose we start from 0, and at each step, we either go left or right with probability...

Problem 3 Consider a random walk on the integers. Suppose we start from 0, and at each step, we either go left or right with probability 1/2, ie, Xo--0, and Xt+1 Xt+Zt, where Zt-1 with probability 1/2, and Zt1 with probability 1/2. What is the probability distribution of XT? What is E(X) and Var(XT)?

Problem 3 Consider a random walk on the integers. Suppose we start from 0, and at each step, we either go left or right with probability...

Suppose Zt = 2 + Xt -2Xt-1+Xt-2, where {Xt} is zero-mean stationary series with autocovariance function....

Suppose Zt = 2 + Xt -2Xt-1+Xt-2,

where {Xt} is zero-mean stationary series with autocovariance

function.

Calculate the autocovariance of Zt

Suppose Zt = 2 + Xt -2Xt-1+Xt-2,

where {Xt} is zero-mean stationary series with autocovariance

function.

Calculate the autocovariance of Zt

Find the spectral density of Xt =−0.7Xt−1+Zt −0.3Zt−1+0.7Zt−2, {Zt}~IID(0,2).

Find the spectral density of Xt =−0.7Xt−1+Zt −0.3Zt−1+0.7Zt−2, {Zt}~IID(0,2).

Consider the following AR(2) model: Xt – Xt–1 + + X4-2 = Zt, Z4 ~ WN(0,1)....

Consider the following AR(2) model: Xt – Xt–1 + + X4-2 = Zt, Z4 ~ WN(0,1). (a) Show that X+ is causal. (b) Find the first four coefficients (VO, ..., 43) of the MA(0) representation of Xt. (c) Find the pacf at lag 3, 233, of the AR(2) model.

Consider the following AR(2) model: Xt – Xt–1 + + X4-2 = Zt, Z4 ~ WN(0,1). (a) Show that X+ is causal. (b) Find the first four coefficients (VO, ..., 43) of the MA(0) representation of Xt. (c) Find the pacf at lag 3, 233, of the AR(2) model.

Consider the model defined by, Yt = BO + B1 Yt-1 + B2 Xt + Ut....

Consider the model defined by, Yt = BO + B1 Yt-1 + B2 Xt + Ut. Compute the long-run coefficients (2 decimals) for the model: Short-Run Long-Run BO 1.38 B1 0.60 B2 -5.26

Consider the model defined by, Yt = BO + B1 Yt-1 + B2 Xt + Ut. Compute the long-run coefficients (2 decimals) for the model: Short-Run Long-Run BO 1.38 B1 0.60 B2 -5.26

For the system in problem below, find the output yt if the input xt=ut, and y0-=4,...

For the system in problem below, find the output yt if the input xt=ut, and y0-=4, y'0=0. y''t+10y't+16yt=3x(t)

For the following system of first order difference equations xt+1=-xt-2yt +24 yt+1= -...

For the following system of first order difference equations xt+1=-xt-2yt +24 yt+1= -2xt+2yt+9 1) Present the system in matrix form. (2) Find the equilibrium vector. (3) Find the eigenvalues and eigenvectors for this system. (4) Find the general solution. (5) Plot the phase diagram.

Find the spectral density functions of the following MA process: Xt = Zt + 0.5Zt−1 −...

Find the spectral density functions of the following MA process: Xt = Zt + 0.5Zt−1 − 0.3Zt−2

Consider the process where B is a backwards shift operator so that BXt-Xt-i and the {Zt) are assu...

Consider the process where B is a backwards shift operator so that BXt-Xt-i and the {Zt) are assumed to be independent random errors. (a) [2 marks] Identify what kind of nonseasonal ARIMA(p,d,q) process this is; that is give the parameters (p,d,q) and give the abbreviated name for this particular process. (b) [3 marks] (i) Is this particular process stationary? Explain. (ii) Is this process invertible? Why?

Consider the process where B is a backwards shift operator so that BXt-Xt-i and...

Consider the process where B is a backwards shift operator so that BXt-Xt-i and the {Zt) are assumed to be independent random errors. (a) [2 marks] Identify what kind of nonseasonal ARIMA(p,d,q) process this is; that is give the parameters (p,d,q) and give the abbreviated name for this particular process. (b) [3 marks] (i) Is this particular process stationary? Explain. (ii) Is this process invertible? Why?

Consider the process where B is a backwards shift operator so that BXt-Xt-i and...

Zt is a function of Xt, Y4 and Ut. Express the growth rate of Zų as a function of growth rates of Xt, Yt and Ut for the following cases (no need to show the intermediate steps): Question 4.1 [5 points Zt = X Y3 Question 4.2 (5 points) Zt Question 4.3 [5 points) Z4 = VX+Y4

Zt is a function of Xt, Y4 and Ut. Express the growth rate of Zų as a function of growth rates of Xt, Yt and Ut for the following cases (no need to show the intermediate steps): Question 4.1 [5 points Zt = X Y3 Question 4.2 (5 points) Zt Question 4.3 [5 points) Z4 = VX+Y4

Problem 3 Consider a random walk on the integers. Suppose we start from 0, and at each step, we either go left or right with probability 1/2, ie, Xo--0, and Xt+1 Xt+Zt, where Zt-1 with probability 1/2, and Zt1 with probability 1/2. What is the probability distribution of XT? What is E(X) and Var(XT)?

Problem 3 Consider a random walk on the integers. Suppose we start from 0, and at each step, we either go left or right with probability...

Problem 3 Consider a random walk on the integers. Suppose we start from 0, and at each step, we either go left or right with probability 1/2, ie, Xo--0, and Xt+1 Xt+Zt, where Zt-1 with probability 1/2, and Zt1 with probability 1/2. What is the probability distribution of XT? What is E(X) and Var(XT)?

Problem 3 Consider a random walk on the integers. Suppose we start from 0, and at each step, we either go left or right with probability...

Suppose Zt = 2 + Xt -2Xt-1+Xt-2,

where {Xt} is zero-mean stationary series with autocovariance

function.

Calculate the autocovariance of Zt

Suppose Zt = 2 + Xt -2Xt-1+Xt-2,

where {Xt} is zero-mean stationary series with autocovariance

function.

Calculate the autocovariance of Zt

Consider the following AR(2) model: Xt – Xt–1 + + X4-2 = Zt, Z4 ~ WN(0,1). (a) Show that X+ is causal. (b) Find the first four coefficients (VO, ..., 43) of the MA(0) representation of Xt. (c) Find the pacf at lag 3, 233, of the AR(2) model.

Consider the following AR(2) model: Xt – Xt–1 + + X4-2 = Zt, Z4 ~ WN(0,1). (a) Show that X+ is causal. (b) Find the first four coefficients (VO, ..., 43) of the MA(0) representation of Xt. (c) Find the pacf at lag 3, 233, of the AR(2) model.

Consider the model defined by, Yt = BO + B1 Yt-1 + B2 Xt + Ut. Compute the long-run coefficients (2 decimals) for the model: Short-Run Long-Run BO 1.38 B1 0.60 B2 -5.26

Consider the model defined by, Yt = BO + B1 Yt-1 + B2 Xt + Ut. Compute the long-run coefficients (2 decimals) for the model: Short-Run Long-Run BO 1.38 B1 0.60 B2 -5.26

Consider the process where B is a backwards shift operator so that BXt-Xt-i and the {Zt) are assumed to be independent random errors. (a) [2 marks] Identify what kind of nonseasonal ARIMA(p,d,q) process this is; that is give the parameters (p,d,q) and give the abbreviated name for this particular process. (b) [3 marks] (i) Is this particular process stationary? Explain. (ii) Is this process invertible? Why?

Consider the process where B is a backwards shift operator so that BXt-Xt-i and...

Consider the process where B is a backwards shift operator so that BXt-Xt-i and the {Zt) are assumed to be independent random errors. (a) [2 marks] Identify what kind of nonseasonal ARIMA(p,d,q) process this is; that is give the parameters (p,d,q) and give the abbreviated name for this particular process. (b) [3 marks] (i) Is this particular process stationary? Explain. (ii) Is this process invertible? Why?

Consider the process where B is a backwards shift operator so that BXt-Xt-i and...

Most questions answered within 3 hours.

-

Bismuth-210 is beta emitter with a half-life of 5.0 days.

Part A

If a sample contains...

asked 1 minute ago -

The income statement for the month of June, 2014 of Happy Smiles

Enterprises contains the following...

asked 14 minutes ago -

To be done in java code. 2 words are anagrams if 1 word can be

formed...

asked 12 minutes ago -

Bright Sun, Inc. sold an issue of 30-year $1,000 par value bonds

to the public. The...

asked 9 minutes ago -

Two players take turns at removing 1 to 4 coins from an original

pile of 16...

asked 8 minutes ago -

1-Calculate the mass in grams of 2.55 moles of KCl

2- Calculate how many moles are...

asked 14 minutes ago -

1. Choose value for p between 0.20 and 0.80. It should have at

least two decimal...

asked 16 minutes ago -

QUESTIONS: 500 words for the question

In defining abnormality, the criteria of “deviance”, “distress”

and “dysfunction”...

asked 17 minutes ago -

A sample of n = 25 scores produces a t statistic of t =

-2.062. If...

asked 35 minutes ago -

Given the following, compute the after tax cost of debt: The par

value of the firms...

asked 29 minutes ago -

Coding in C. Please only use stdio.h (which would mean no malloc

or anything like that)...

asked 34 minutes ago -

Use the fundamental accounting equation to find the missing

amounts.

Scenario

Assets

Liabilities

Equity

1

$...

asked 32 minutes ago