Homework Answers

Add Answer to:

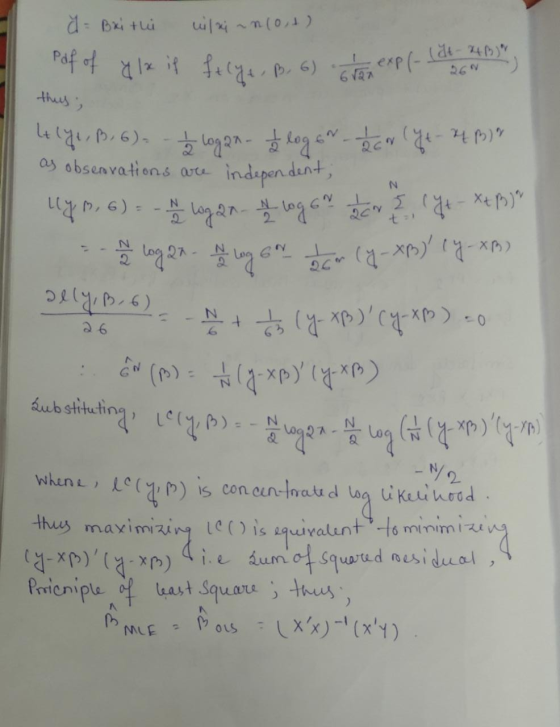

1) Suppose you have an iid sample of size n drawn from the following regression model:...

1. Consider the linear regression model iid 220 with є, 면 N(0, σ2), i = 1, . . . , n. Let Yh = β0+ßX, be the MLE of t...

1. Consider the linear regression model iid 220 with є, 면 N(0, σ2), i = 1, . . . , n. Let Yh = β0+ßX, be the MLE of the mean at covariate value Xh . (f) Suppose we estimate ơ2 by 82-SSE/(n-2). Derive the distribution for You can use the fact that SSE/σ2 ~ X2-2 without proof. (g) What is a (1-a)100% confidence interval for y? (h) Suppose we observe a new observation Ynet at covariate value X =...

1. Consider the linear regression model iid 220 with є, 면 N(0, σ2), i = 1, . . . , n. Let Yh = β0+ßX, be the MLE of the mean at covariate value Xh . (f) Suppose we estimate ơ2 by 82-SSE/(n-2). Derive the distribution for You can use the fact that SSE/σ2 ~ X2-2 without proof. (g) What is a (1-a)100% confidence interval for y? (h) Suppose we observe a new observation Ynet at covariate value X =...

Suppose X1, X2, .., Xn is an iid sample from where >0. (a) Derive the size...

Suppose X1, X2, .., Xn is an iid sample from where >0. (a) Derive the size α likelihood ratio test (LRT) for Ho : θ-Bo versus H : θ θο. Derive the power function of the LRT (b) Suppose that n 10, Derive the most powerful (MP) level α-0.10 test of Ho : θ 1 versus Hi: 0-2. Calculate the power of your test

Suppose X1, X2, .., Xn is an iid sample from where >0. (a) Derive the size α likelihood ratio test (LRT) for Ho : θ-Bo versus H : θ θο. Derive the power function of the LRT (b) Suppose that n 10, Derive the most powerful (MP) level α-0.10 test of Ho : θ 1 versus Hi: 0-2. Calculate the power of your test

1. Let X be an iid sample of size n from a continuous distribution with mean...

1. Let X be an iid sample of size n from a continuous distribution with mean /i, variance a2 and such that Xi e [0, 1] for all i e {1,...,n}. Let X = average. For a E (0,1), we wish to obtain a number q > 0 such that: (1/n) Xi be the sample Р(X € |и — 9. и + q) predict with probability approximately In other words, we wish to sample of size n, the average X...

1. Let X be an iid sample of size n from a continuous distribution with mean /i, variance a2 and such that Xi e [0, 1] for all i e {1,...,n}. Let X = average. For a E (0,1), we wish to obtain a number q > 0 such that: (1/n) Xi be the sample Р(X € |и — 9. и + q) predict with probability approximately In other words, we wish to sample of size n, the average X...

Suppose that you estimate a regression model with a sample size of 92 observations and 10...

Suppose that you estimate a regression model with a sample size of 92 observations and 10 explanatory variables, including the intercept, using ordinary least squares and the residual sum of squares from this estimated model is 22. You then conduct a Ramsey’s RESET on this model and the residual sum of squares from the Ramsey regression is 20. The test statistic associated with this Ramsey’s RESET is ______, and you can conclude at the 5-percent level of significance that _________________....

- Suppose a random sample of size n is taken from the following distribution with a...

- Suppose a random sample of size n is taken from the following distribution with a known positive parameter a. f(x;0,-) = a20 V 27797z exp 0; ; 0<x<00,0< < 0,0 < 8 < 00 elsewhere For this distruttore, the formats for mye or and x-a are respectively, Myo (1) = exp v{(1 - V1 –24*70)} for 1 < 2112 and exp{}(-VT - 2/0)} My-- (1) for 1 < ✓1 - 2t/0 2 Find the maximum likelihood estimators, 0 and...

- Suppose a random sample of size n is taken from the following distribution with a known positive parameter a. f(x;0,-) = a20 V 27797z exp 0; ; 0<x<00,0< < 0,0 < 8 < 00 elsewhere For this distruttore, the formats for mye or and x-a are respectively, Myo (1) = exp v{(1 - V1 –24*70)} for 1 < 2112 and exp{}(-VT - 2/0)} My-- (1) for 1 < ✓1 - 2t/0 2 Find the maximum likelihood estimators, 0 and...

Question 5. Given sample data (x, y), and sample size n. We fit the simple regression model: and estimate the least square estimators (a) Suppose A,-1, ß,-2, and x-1. Compute у. b) Suppose S and sry...

Question 5. Given sample data (x, y), and sample size n. We fit the simple regression model: and estimate the least square estimators (a) Suppose A,-1, ß,-2, and x-1. Compute у. b) Suppose S and sry 0.5, compute the R2.

Question 5. Given sample data (x, y), and sample size n. We fit the simple regression model: and estimate the least square estimators (a) Suppose A,-1, ß,-2, and x-1. Compute у. b) Suppose S and sry 0.5, compute the R2.

Question 5. Given sample data (x, y), and sample size n. We fit the simple regression model: and estimate the least square estimators (a) Suppose A,-1, ß,-2, and x-1. Compute у. b) Suppose S and sry 0.5, compute the R2.

Question 5. Given sample data (x, y), and sample size n. We fit the simple regression model: and estimate the least square estimators (a) Suppose A,-1, ß,-2, and x-1. Compute у. b) Suppose S and sry 0.5, compute the R2.

Suppose that X1, X2,....Xn is an iid sample of size n from a Pareto pdf of...

Suppose that X1, X2,....Xn is an iid sample of size n from a Pareto pdf of the form 0-1) otherwise, where θ > 0. (a) Find θ the method of moments (MOM) estimator for θ For what values of θ does θ exist? Why? (b) Find θ, the maximum likelihood estimator (MLE) for θ. (c) Show explicitly that the MLE depends on the sufficient statistic for this Pareto family but that the MOM estimator does not

Suppose that X1, X2,....Xn is an iid sample of size n from a Pareto pdf of the form 0-1) otherwise, where θ > 0. (a) Find θ the method of moments (MOM) estimator for θ For what values of θ does θ exist? Why? (b) Find θ, the maximum likelihood estimator (MLE) for θ. (c) Show explicitly that the MLE depends on the sufficient statistic for this Pareto family but that the MOM estimator does not

Question 3 3 pts Suppose that you estimate a regression model with a sample size of...

Question 3 3 pts Suppose that you estimate a regression model with a sample size of 112 observations and 10 explanatory variables, including the intercept, using ordinary least squares and the residual sum of squares from this estimated model is 22. You then conduct a Ramsey's RESET on this model and the residual sum of squares from the Ramsey regression is 20. The test statistic associated with this Ramsey's RESET is _, and you can conclude at the 5-percent level...

Question 3 3 pts Suppose that you estimate a regression model with a sample size of 112 observations and 10 explanatory variables, including the intercept, using ordinary least squares and the residual sum of squares from this estimated model is 22. You then conduct a Ramsey's RESET on this model and the residual sum of squares from the Ramsey regression is 20. The test statistic associated with this Ramsey's RESET is _, and you can conclude at the 5-percent level...

Question 3 3 pts Suppose that you estimate a regression model with a sample size of...

Question 3 3 pts Suppose that you estimate a regression model with a sample size of 112 observations and 10 explanatory variables, including the intercept, using ordinary least squares and the residual sum of squares from this estimated model is 22. You then conduct a Ramsey's RESET on this model and the residual sum of squares from the Ramsey regression is 20. The test statistic associated with this Ramsey's RESET is and you can conclude at the 5- percent level...

Question 3 3 pts Suppose that you estimate a regression model with a sample size of 112 observations and 10 explanatory variables, including the intercept, using ordinary least squares and the residual sum of squares from this estimated model is 22. You then conduct a Ramsey's RESET on this model and the residual sum of squares from the Ramsey regression is 20. The test statistic associated with this Ramsey's RESET is and you can conclude at the 5- percent level...

Suppose that Xi, X2,..., Xn is an iid sample from 20 for x R and σ...

Suppose that Xi, X2,..., Xn is an iid sample from 20 for x R and σ 〉 0. (a) Derive a size α likelihood ratio test (LRT) of H0 : σ (b) Derive the power function β(o) of the LRT 1 versus H1 : σ 1.

Suppose that Xi, X2,..., Xn is an iid sample from 20 for x R and σ 〉 0. (a) Derive a size α likelihood ratio test (LRT) of H0 : σ (b) Derive the power function β(o) of the LRT 1 versus H1 : σ 1.

1. Consider the linear regression model iid 220 with є, 면 N(0, σ2), i = 1, . . . , n. Let Yh = β0+ßX, be the MLE of the mean at covariate value Xh . (f) Suppose we estimate ơ2 by 82-SSE/(n-2). Derive the distribution for You can use the fact that SSE/σ2 ~ X2-2 without proof. (g) What is a (1-a)100% confidence interval for y? (h) Suppose we observe a new observation Ynet at covariate value X =...

1. Consider the linear regression model iid 220 with є, 면 N(0, σ2), i = 1, . . . , n. Let Yh = β0+ßX, be the MLE of the mean at covariate value Xh . (f) Suppose we estimate ơ2 by 82-SSE/(n-2). Derive the distribution for You can use the fact that SSE/σ2 ~ X2-2 without proof. (g) What is a (1-a)100% confidence interval for y? (h) Suppose we observe a new observation Ynet at covariate value X =...

Suppose X1, X2, .., Xn is an iid sample from where >0. (a) Derive the size α likelihood ratio test (LRT) for Ho : θ-Bo versus H : θ θο. Derive the power function of the LRT (b) Suppose that n 10, Derive the most powerful (MP) level α-0.10 test of Ho : θ 1 versus Hi: 0-2. Calculate the power of your test

Suppose X1, X2, .., Xn is an iid sample from where >0. (a) Derive the size α likelihood ratio test (LRT) for Ho : θ-Bo versus H : θ θο. Derive the power function of the LRT (b) Suppose that n 10, Derive the most powerful (MP) level α-0.10 test of Ho : θ 1 versus Hi: 0-2. Calculate the power of your test

1. Let X be an iid sample of size n from a continuous distribution with mean /i, variance a2 and such that Xi e [0, 1] for all i e {1,...,n}. Let X = average. For a E (0,1), we wish to obtain a number q > 0 such that: (1/n) Xi be the sample Р(X € |и — 9. и + q) predict with probability approximately In other words, we wish to sample of size n, the average X...

1. Let X be an iid sample of size n from a continuous distribution with mean /i, variance a2 and such that Xi e [0, 1] for all i e {1,...,n}. Let X = average. For a E (0,1), we wish to obtain a number q > 0 such that: (1/n) Xi be the sample Р(X € |и — 9. и + q) predict with probability approximately In other words, we wish to sample of size n, the average X...

- Suppose a random sample of size n is taken from the following distribution with a known positive parameter a. f(x;0,-) = a20 V 27797z exp 0; ; 0<x<00,0< < 0,0 < 8 < 00 elsewhere For this distruttore, the formats for mye or and x-a are respectively, Myo (1) = exp v{(1 - V1 –24*70)} for 1 < 2112 and exp{}(-VT - 2/0)} My-- (1) for 1 < ✓1 - 2t/0 2 Find the maximum likelihood estimators, 0 and...

- Suppose a random sample of size n is taken from the following distribution with a known positive parameter a. f(x;0,-) = a20 V 27797z exp 0; ; 0<x<00,0< < 0,0 < 8 < 00 elsewhere For this distruttore, the formats for mye or and x-a are respectively, Myo (1) = exp v{(1 - V1 –24*70)} for 1 < 2112 and exp{}(-VT - 2/0)} My-- (1) for 1 < ✓1 - 2t/0 2 Find the maximum likelihood estimators, 0 and...

Question 5. Given sample data (x, y), and sample size n. We fit the simple regression model: and estimate the least square estimators (a) Suppose A,-1, ß,-2, and x-1. Compute у. b) Suppose S and sry 0.5, compute the R2.

Question 5. Given sample data (x, y), and sample size n. We fit the simple regression model: and estimate the least square estimators (a) Suppose A,-1, ß,-2, and x-1. Compute у. b) Suppose S and sry 0.5, compute the R2.

Question 5. Given sample data (x, y), and sample size n. We fit the simple regression model: and estimate the least square estimators (a) Suppose A,-1, ß,-2, and x-1. Compute у. b) Suppose S and sry 0.5, compute the R2.

Question 5. Given sample data (x, y), and sample size n. We fit the simple regression model: and estimate the least square estimators (a) Suppose A,-1, ß,-2, and x-1. Compute у. b) Suppose S and sry 0.5, compute the R2.

Suppose that X1, X2,....Xn is an iid sample of size n from a Pareto pdf of the form 0-1) otherwise, where θ > 0. (a) Find θ the method of moments (MOM) estimator for θ For what values of θ does θ exist? Why? (b) Find θ, the maximum likelihood estimator (MLE) for θ. (c) Show explicitly that the MLE depends on the sufficient statistic for this Pareto family but that the MOM estimator does not

Suppose that X1, X2,....Xn is an iid sample of size n from a Pareto pdf of the form 0-1) otherwise, where θ > 0. (a) Find θ the method of moments (MOM) estimator for θ For what values of θ does θ exist? Why? (b) Find θ, the maximum likelihood estimator (MLE) for θ. (c) Show explicitly that the MLE depends on the sufficient statistic for this Pareto family but that the MOM estimator does not

Question 3 3 pts Suppose that you estimate a regression model with a sample size of 112 observations and 10 explanatory variables, including the intercept, using ordinary least squares and the residual sum of squares from this estimated model is 22. You then conduct a Ramsey's RESET on this model and the residual sum of squares from the Ramsey regression is 20. The test statistic associated with this Ramsey's RESET is _, and you can conclude at the 5-percent level...

Question 3 3 pts Suppose that you estimate a regression model with a sample size of 112 observations and 10 explanatory variables, including the intercept, using ordinary least squares and the residual sum of squares from this estimated model is 22. You then conduct a Ramsey's RESET on this model and the residual sum of squares from the Ramsey regression is 20. The test statistic associated with this Ramsey's RESET is _, and you can conclude at the 5-percent level...

Question 3 3 pts Suppose that you estimate a regression model with a sample size of 112 observations and 10 explanatory variables, including the intercept, using ordinary least squares and the residual sum of squares from this estimated model is 22. You then conduct a Ramsey's RESET on this model and the residual sum of squares from the Ramsey regression is 20. The test statistic associated with this Ramsey's RESET is and you can conclude at the 5- percent level...

Question 3 3 pts Suppose that you estimate a regression model with a sample size of 112 observations and 10 explanatory variables, including the intercept, using ordinary least squares and the residual sum of squares from this estimated model is 22. You then conduct a Ramsey's RESET on this model and the residual sum of squares from the Ramsey regression is 20. The test statistic associated with this Ramsey's RESET is and you can conclude at the 5- percent level...

Suppose that Xi, X2,..., Xn is an iid sample from 20 for x R and σ 〉 0. (a) Derive a size α likelihood ratio test (LRT) of H0 : σ (b) Derive the power function β(o) of the LRT 1 versus H1 : σ 1.

Suppose that Xi, X2,..., Xn is an iid sample from 20 for x R and σ 〉 0. (a) Derive a size α likelihood ratio test (LRT) of H0 : σ (b) Derive the power function β(o) of the LRT 1 versus H1 : σ 1.

Most questions answered within 3 hours.

-

Write a program to solve the Josephus problem, with the following

modification:

Sample Input:

./a.out n...

asked 1 hour ago -

At the start of a CD it is spinning at a rate of 525 rpm

(revolutions...

asked 1 hour ago -

4. Without doing any calculations, predict whether the observed

∆T would increase, decrease or remain the...

asked 3 hours ago -

Based on the range, which of the following sets of scores has

the greatest variability? 3,...

asked 4 hours ago -

Ripples in a pond travel at a velocity of 3 m/s with one peak

passing a...

asked 4 hours ago -

A man stands on the roof of a building of height 13.0 mm and

throws a...

asked 4 hours ago -

The extent to which assets are financed by borrowed funds and

other liabilities is indicated by:...

asked 5 hours ago -

Explain in detail

Germany is the fifth largest economy

explain what goods and services Germany specializes...

asked 5 hours ago -

The density of platinum is 21.45 g/mL. If a cube of platinum

with a mass of...

asked 5 hours ago -

Accounts Receivable

Sales

A/R Posting

Extended Sales Invoice

Packing Slip

Compare invoice to packing slip 2...

asked 5 hours ago -

Michaella, age 23, is a full-time law student and is claimed by

her parents as a...

asked 5 hours ago -

Why are polymers not typically casted into products?

asked 6 hours ago