Suppose a Canadian agent (investor) with C$1.0 million is choosing between bank deposits denominated in either euro or Canadian dollars.

2. Suppose a Canadian agent (investor) with C$1.0 million is choosing between bank deposits denominated in either euro or Canadian dollars. Also suppose that the (one-year) interest rate paid on the C$ deposits is 1% (0.01) and on the euro deposit is 2% (0.02), the (one-year) forward C$-EURO exchange rate (FC$/€ ) is 1.60 and the current spot rate (EC$/€ ) is 1.65. Based on this information, answer the following questions.

(a) What is the forward spread? Is the Canadian dollar at forward premium or discount? And by how much (%)?

(b) What is the (hedged = riskless) rate of return on the euro deposits?

(c) Based on your answer above, is there an arbitrage opportunity between the two deposits? Explain why or why not.

(d) If the spot rate of exchange as well as the interest rates are kept at their current levels (stated above), what will be equilibrium forward rate as implied by the covered interest parity theory (CIP)?

Homework Answers

a) The forward for CAD/EUR is 1.60 while the spot rate is

1.65.

1.65 - 1.60 = 0.05

The forward exchange rate for CAD/EUR is at the premium by

0.05.

(0.05 / 1.65) * 100 = 3.03%

b) The return in CAD

1000000 * 0.01 = 10000 CAD

Return on EUR is 2%

1000000 / 1.65 = 606060.61

606060.61 * 0.02 = 12121.21

c) The arbitrage opportunity is possible if the exchange rate

deviates from the interest rate parity condition.

(Forward Rate / Spot Rate ) = (1+Interest Rate in EUR) /

(1+Interest Rate in CAD)

(Forward Rate / Spot Rate ) = 1.6 / 1.65 = 0.9697

(1+Interest Rate in EUR) / (1+Interest Rate in CAD) = (1.02 / 1.01)

= 1.0099

Since these two values are not equal so there is an opportunity for arbitrage.

d) If there is any discrepancy in the spot rate of forward rate

so that the interest rate parity condition is being violated then

arbitrage trade is possible and will result in risk less

profit.

However, the market forces will quickly negate that situation.

(Forward Rate / Spot Rate ) = (1+Interest Rate in EUR) /

(1+Interest Rate in CAD)

Forward Rate = Spot Rate * (1+Interest Rate in EUR) / (1+Interest

Rate in CAD)

1.65 * (1.02 / 1.01) = 1.65 * 1.0099

Forward Rate = 1.6663

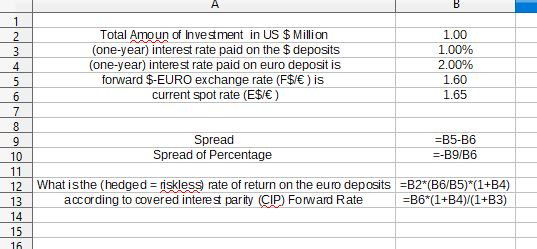

Total Amoun of Investment in US $ Million

Amount = 1.00

(one-year) interest rate paid on the $ deposits

RUSD = 1.00%

(one-year) interest rate paid on euro deposit is

REURO = 2.00%

forward $-EURO exchange rate (F$/€ ) is FR =

1.60

current spot rate (E$/€ ) SR = 1.65

Ans (a)

forward spread = Forward Price - Spot Price = FR - SR = 1.60 - 1.65 = ( 0.05)

As FR < SR, forward Dollar Rate is lower than the spot rate, So the Dollar is at Discount..

% of Discount = spread / Spot Price = 0.05 / 1.60 = 3.030%

Ans (b)

the (hedged = riskless) rate of return on the euro deposits

What is the (hedged = riskless) return on the euro deposits

= Amoun of Investment in US $ * ( Current Spot Rate / Forward Rate) * ( 1+ Euro Int Rate)

= Amnt * ( SR / FR) * ( 1+ REURO )

= 1 * (1.65/1.60) * (1 + 2%)

= 1.0518750

Here The Steps as follow :

Step 01: Convert the USD in EURO in Current Spot Rate = Amnt * SR

Step 02 : Invest this Amount in EURO Market for 01 Year = Amnt * SR * ( 1 + REURO )

Step 03 : Convert the EURO Return as per determined future rate = Amnt * SR * ( 1 + REURO ) / FR

rate of return on the euro deposits = ( return on the euro deposits - Amoun of Investment ) / Amoun of Investment

= ( 1.0518750 - 1) / 1 = 5.18%

the (hedged = riskless) rate of return on the euro deposits = 5.18% (Ans)

Ans c :

Riskless Return in EURO Deposit is 5.18% which is much higher than current prevailing Deposit rate in US Market is 01%.

So There is a Arbitrage Opportunity. (Ans)

Ans d.

according to covered interest parity (CIP) equilibrium Forward Rate

FR = SR * (1 + REURO ) / (1 + RUSD) = 1.65 * ( 1 + 2%) / (1 + 1%) = 1.666

so, equilibrium Forward Rate 1.666 E$/€ (Ans)

Add Answer to:

Suppose a Canadian agent (investor) with C$1.0 million is choosing between bank deposits denominated in either euro or Canadian dollars.

Consider a Spanish investor with 5,000 euros to place in a bank deposit in either Spain...

Consider a Spanish investor with 5,000 euros to place in a bank deposit in either Spain or Great Britain. The (one-year) interest rate on bank deposits is 3% in Britain and 4.5% in Spain. The (one-year) forward euro-pound exchange rate is 1.7 euros per pound and the spot rate is 1.6 euros per pound. Answer the following questions! a) What is the euro-denominated return (i.e. the total amount of Euros) on Spanish deposits for this investor? b) What is the...

Consider a Spanish investor with 5,000 euros to place in a bank deposit in either Spain or Great Britain. The (one-year) interest rate on bank deposits is 3% in Britain and 4.5% in Spain. The (one-year) forward euro-pound exchange rate is 1.7 euros per pound and the spot rate is 1.6 euros per pound. Answer the following questions! a) What is the euro-denominated return (i.e. the total amount of Euros) on Spanish deposits for this investor? b) What is the...

Please show work and choose A, B, C, or D. The 12-month interest rate on dollar-denominated...

Please show work and choose A, B, C, or D.

The 12-month interest rate on dollar-denominated assets (like bank deposits) is 2.00%. The 12- month interest rate on euro-denominated assets is 4.50%. The current spot exchange rate is $1.15 per euro. The current forward exchange rate is $1.05 per euro. You have an initial dollar fund of $100,000. Suppose that you decide to invest your dollar fund in euro-denominated assets while also using the forward exchange market to hedge against...

Please show work and choose A, B, C, or D.

The 12-month interest rate on dollar-denominated assets (like bank deposits) is 2.00%. The 12- month interest rate on euro-denominated assets is 4.50%. The current spot exchange rate is $1.15 per euro. The current forward exchange rate is $1.05 per euro. You have an initial dollar fund of $100,000. Suppose that you decide to invest your dollar fund in euro-denominated assets while also using the forward exchange market to hedge against...

3. a. Assume that the interest rate on Euro denominated assets is 5% and the interest...

3. a. Assume that the interest rate on Euro denominated assets is 5% and the interest rate on comparable dollar denominated assets is 10%. The spot exchange rate is $1/1E. If you expect the exchange rate changes to $1.05/1E, where would you want to keep your money? Calculate and show! b. The current interest rates on dollar and pound denominated deposits are 2% in the US and 3% in the UK. The current spot exchange rate is $2/1Pound. If the...

Q4. Suppose a Canadian bond portfolio manager wishes to enhance his yield on Canadian short-term bills....

Q4. Suppose a Canadian bond portfolio manager wishes to enhance his yield on Canadian short-term bills. Current one-year Canadian T-Bills yield 13%. The current spot rate is C$ 1.40/$. The one-year forward rate is C$ 1.50/$. The US one-year T-Bill rate is 6%. What is the Canadian T-Bill rate implied by interest rate parity? What percentage yield could the portfolio manager obtain by exploiting the arbitrage opportunity? (Show your calculations!)

Suppose a Canadian bond portfolio manager wishes to enhance his yield on Canadian short-term bills. Current...

Suppose a Canadian bond portfolio manager wishes to enhance his yield on Canadian short-term bills. Current one-year Canadian T-Bills yield 13%. The current spot rate is C$ 1.40/$. The one-year forward rate is C$ 1.50/$. The US one-year T-Bill rate is 6%. What is the Canadian T-Bill rate implied by interest rate parity? What percentage yield could the portfolio manager obtain by exploiting the arbitrage opportunity? (Show your calculations!)

Use the following information to answer question 5 and 6 Suppose that the current spot exchange...

Use the following information to answer question 5 and 6 Suppose that the current spot exchange rate between Japanese Yen and Euro is ¥130/€ and the one-year forward exchange rate is ¥138.25/€. The one-year interest rate is 2.0 % in yens and 1.25% in euro. 5. According to the Interest Rate Parity condition, what is the 1 year forward exchange rate? a. ¥139.27/€ b. ¥130.96/€ c. ¥129.04/€ d. ¥137.23/€ 6. What is your arbitrage strategy if you can borrow 10...

1. Suppose a Canadian dollar buys 0.68 Euro. How many Canadian dollars do you need to...

1. Suppose a Canadian dollar buys 0.68 Euro. How many Canadian dollars do you need to buy a Euro? 2. 1pt Suppose the Canadian dollar appreciated by 10%. Now how many Canadian dollars would be needed? 3. 2pt Suppose the Canadian dollar is worth 0.75 USD. Acadia tuition costs $10,000 CAD per year, and American tuition costs $12,000 USD per year. Calculate the real exchange rate. 4. 1pt Use the number derived from 3 to conclude whether or not tuition...

QUESTION 1: Suppose that the current spot exchange rate is GBP1= €1.50 and the one-year forward...

QUESTION 1: Suppose that the current spot exchange rate is GBP1= €1.50 and the one-year forward exchange rate is GBP1=€1.60. One-year interest rate is 5.4% in euros and 5.2% in pounds. If you have EUR1,000,000, what is the Covered Interest arbitrage profit in EUR? QUESTION 2: Suppose that the current spot exchange rate is GBP1= €1.50 and the one-year forward exchange rate is GBP1=€1.60. One-year interest rate is 5.4% in euros and 5.2% in pounds. If you conduct covered interest...

Please do Part A, B, C, D separately. Suppose that the following conditions all hold: uncovered...

Please do Part A, B, C, D

separately.

Suppose that the following conditions all hold: uncovered and covered interest rate parity, real interest rate parity, relative and absolute purchasing power parity. And suppose you have the following information: - The current nominal interest rate for a 1 year deposit in a Brazilian bank is 20%. - Inflation is expected to be 10 percentage points higher in Brazil than Argentina over the next year. - The forward exchange rate between Brazil...

Please do Part A, B, C, D

separately.

Suppose that the following conditions all hold: uncovered and covered interest rate parity, real interest rate parity, relative and absolute purchasing power parity. And suppose you have the following information: - The current nominal interest rate for a 1 year deposit in a Brazilian bank is 20%. - Inflation is expected to be 10 percentage points higher in Brazil than Argentina over the next year. - The forward exchange rate between Brazil...

Several factors affect the exchange rate of a currency with another currency. Which of the following...

Several factors affect the exchange rate of a currency with another currency. Which of the following statements are true about the factors that have an impact on exchange rates? Check all that apply. When a government limits imports and restricts foreign exchange transactions, its currency's value tends to increase relative to other currencies. An increase in inflation tends to increase the currency's value with respect to other currencies with lower inflation. If a government intends to prevent its currency's value...

Several factors affect the exchange rate of a currency with another currency. Which of the following statements are true about the factors that have an impact on exchange rates? Check all that apply. When a government limits imports and restricts foreign exchange transactions, its currency's value tends to increase relative to other currencies. An increase in inflation tends to increase the currency's value with respect to other currencies with lower inflation. If a government intends to prevent its currency's value...

Consider a Spanish investor with 5,000 euros to place in a bank deposit in either Spain or Great Britain. The (one-year) interest rate on bank deposits is 3% in Britain and 4.5% in Spain. The (one-year) forward euro-pound exchange rate is 1.7 euros per pound and the spot rate is 1.6 euros per pound. Answer the following questions! a) What is the euro-denominated return (i.e. the total amount of Euros) on Spanish deposits for this investor? b) What is the...

Consider a Spanish investor with 5,000 euros to place in a bank deposit in either Spain or Great Britain. The (one-year) interest rate on bank deposits is 3% in Britain and 4.5% in Spain. The (one-year) forward euro-pound exchange rate is 1.7 euros per pound and the spot rate is 1.6 euros per pound. Answer the following questions! a) What is the euro-denominated return (i.e. the total amount of Euros) on Spanish deposits for this investor? b) What is the...

Please show work and choose A, B, C, or D.

The 12-month interest rate on dollar-denominated assets (like bank deposits) is 2.00%. The 12- month interest rate on euro-denominated assets is 4.50%. The current spot exchange rate is $1.15 per euro. The current forward exchange rate is $1.05 per euro. You have an initial dollar fund of $100,000. Suppose that you decide to invest your dollar fund in euro-denominated assets while also using the forward exchange market to hedge against...

Please show work and choose A, B, C, or D.

The 12-month interest rate on dollar-denominated assets (like bank deposits) is 2.00%. The 12- month interest rate on euro-denominated assets is 4.50%. The current spot exchange rate is $1.15 per euro. The current forward exchange rate is $1.05 per euro. You have an initial dollar fund of $100,000. Suppose that you decide to invest your dollar fund in euro-denominated assets while also using the forward exchange market to hedge against...

Please do Part A, B, C, D

separately.

Suppose that the following conditions all hold: uncovered and covered interest rate parity, real interest rate parity, relative and absolute purchasing power parity. And suppose you have the following information: - The current nominal interest rate for a 1 year deposit in a Brazilian bank is 20%. - Inflation is expected to be 10 percentage points higher in Brazil than Argentina over the next year. - The forward exchange rate between Brazil...

Please do Part A, B, C, D

separately.

Suppose that the following conditions all hold: uncovered and covered interest rate parity, real interest rate parity, relative and absolute purchasing power parity. And suppose you have the following information: - The current nominal interest rate for a 1 year deposit in a Brazilian bank is 20%. - Inflation is expected to be 10 percentage points higher in Brazil than Argentina over the next year. - The forward exchange rate between Brazil...

Several factors affect the exchange rate of a currency with another currency. Which of the following statements are true about the factors that have an impact on exchange rates? Check all that apply. When a government limits imports and restricts foreign exchange transactions, its currency's value tends to increase relative to other currencies. An increase in inflation tends to increase the currency's value with respect to other currencies with lower inflation. If a government intends to prevent its currency's value...

Several factors affect the exchange rate of a currency with another currency. Which of the following statements are true about the factors that have an impact on exchange rates? Check all that apply. When a government limits imports and restricts foreign exchange transactions, its currency's value tends to increase relative to other currencies. An increase in inflation tends to increase the currency's value with respect to other currencies with lower inflation. If a government intends to prevent its currency's value...

Most questions answered within 3 hours.

-

You have been asked to develop a new line of organic skincare

products. Spend time with...

asked 30 minutes ago -

Summerdahl Resort's common stock is currently trading at $37 a

share. The stock is expected to...

asked 50 minutes ago -

To an economist, the field of industrial organization answers

which of the following questions?

asked 54 minutes ago -

How could meeting industry expectations, propel managers into

challenging and possible conflict of interest situations? How...

asked 1 hour ago -

You have been married to your spouse for 10 years. You have two

small children (ages...

asked 3 hours ago -

Spiderman makes a leap from one building to

another. He starts on one building that is...

asked 3 hours ago -

A

symbol is something that stands for something else. What are the

symbols in education?what are...

asked 3 hours ago -

The charge to the left in the figure above has a

magnitude of 2.90 nC, and...

asked 4 hours ago -

Verify the MIRR is 9.29% given cash flows in years 1 and 2 of

$1,000 each,...

asked 5 hours ago -

Calculate the pH of a 5.7 M solution of aniline (C6H5NH2; Kb =

3.8 x 10^-10)

asked 7 hours ago -

LSL R3, R3, R12

Memory

Address

Orig.

Data

Updated

Data

Register

Orig.

Data

Updated

Data

0x84F0...

asked 7 hours ago -

Air at 100 kPa and density of 1.2 kg/m3 flows upward through a

5-cm diameter inclined...

asked 7 hours ago