Suppose the exchange rate is $1.95/£. Let r $ = 7%, r £ = 4%, u...

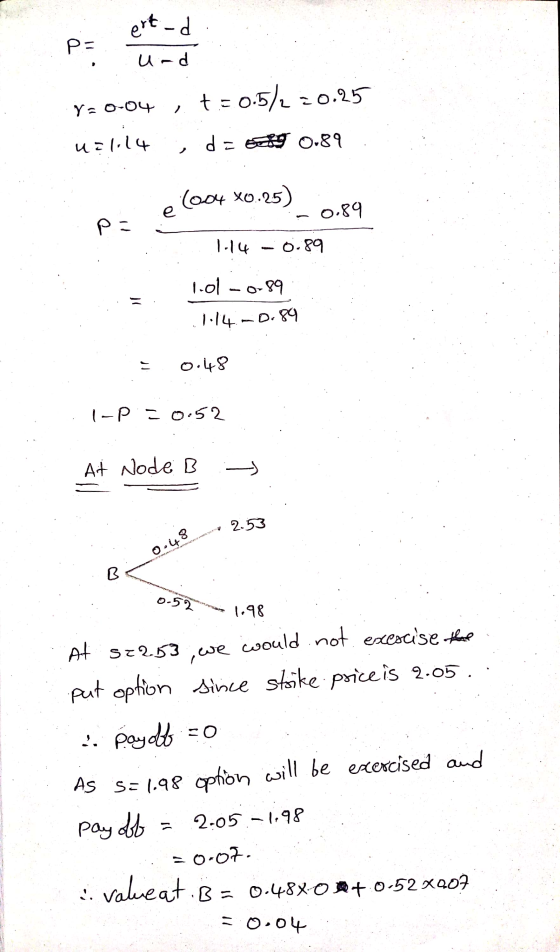

Suppose the exchange rate is $1.95/£. Let r $ = 7%, r £ = 4%, u = 1.14, d = 0.89, and T = 0.5. Using a 2-step binomial tree, calculate the value of a $2.05-strike European put option on the British pound? Please do NOT answer with Excel. Answer Choices: A. $0.1639 B. $0.1775 C. $0.1745 D. $0.1714 E. $0.1810

EDIT: This question does not need anymore information, everything I have written is all that was provided in the original question.

Homework Answers

Suppose the exchange rate is $1.95/£. Let r $ = 7%, r £ = 4%, u = 1.14, d = 0.89, and T = 0.5. Using a 2-step binomial tree, calculate the value of a $2.05-strike European put option on the British pound?

post all the necessary steps Suppose the exchange rate is $1.99/£. Let r$ = 6%, r£...

post all the necessary steps Suppose the exchange rate is $1.99/£. Let r$ = 6%, r£ = 7%, u = 1.27, d = 0.78, and T = 1. Using a 2-step binomial tree, calculate the value of a $2.10-strike European put option on the British pound. a. $0.2671 b. $0.3235 c. $0.3435 d. $0.3333 e. $0.3282

Suppose the exchange rate is $1.03/C$. Let r $ = 7%, r C$ = 3%, u...

Suppose the exchange rate is $1.03/C$. Let r $ = 7%,

r C$ = 3%, u = 1.28, d = 0.83, and T = 1.5. Using a

2-step binomial tree, calculate the value of a $1.10-strike

European put option on the Canadian dollar.

Option D is correct, but how? Can you provide solution for

Excel? formulas and steps or actual excel work sheet please?

Answers:

a.

$0.1049

b.

$0.1229

c.

$0.1302

d.

$0.1106

e.

$0.1166

Suppose the exchange rate is $1.03/C$. Let r $ = 7%,

r C$ = 3%, u = 1.28, d = 0.83, and T = 1.5. Using a

2-step binomial tree, calculate the value of a $1.10-strike

European put option on the Canadian dollar.

Option D is correct, but how? Can you provide solution for

Excel? formulas and steps or actual excel work sheet please?

Answers:

a.

$0.1049

b.

$0.1229

c.

$0.1302

d.

$0.1106

e.

$0.1166

Question I: Suppose that the exchange rate is $0.92/€. Let rs = 4%, and re =...

Question I: Suppose that the exchange rate is $0.92/€. Let rs = 4%, and re = 3%, u = 1.2, d = 0.9, T = 0.75, number of binomial periods = 3, and K = $0.85. Use Binomial Option pricing to answer the following two questions. (a) What is the price of a 9-month European call? (b) What is the price of a 9-month American call?

Question I: Suppose that the exchange rate is $0.92/€. Let rs = 4%, and re = 3%, u = 1.2, d = 0.9, T = 0.75, number of binomial periods = 3, and K = $0.85. Use Binomial Option pricing to answer the following two questions. (a) What is the price of a 9-month European call? (b) What is the price of a 9-month American call?

Question I: Suppose that the exchange rate is $0.92/€. Let rs = 4%, and re =...

Question I: Suppose that the exchange rate is $0.92/€. Let rs = 4%, and re = 3%, u = 1.2, d =0.9, T = 0.75, number of binomial periods = 3, and K = $0.85. Use Binomial Option pricing to answer the following two questions. Use the same inputs as in the previous (first) question, except that K = $1.00. (a) What is the price of a 9-month European call? (b) What is the price of a 9-month American call?

Question I: Suppose that the exchange rate is $0.92/€. Let rs = 4%, and re = 3%, u = 1.2, d =0.9, T = 0.75, number of binomial periods = 3, and K = $0.85. Use Binomial Option pricing to answer the following two questions. Use the same inputs as in the previous (first) question, except that K = $1.00. (a) What is the price of a 9-month European call? (b) What is the price of a 9-month American call?

Binomial Option Pricing 10.6 Let S = $100, K = $95, σ = 30%, r =...

Binomial Option Pricing 10.6 Let S = $100, K = $95, σ = 30%, r = 8%, T = 1, and δ = 0. Let u = 1.3, d = 0.8, and n = 2. Construct the binomial tree for a call option. At each node provide the premium, , and B. 10.7 Repeat the option price calculation in the previous question for stock prices of $80, $90, $110, $120, and $130, keeping everything else fixed. What happens to the...

Suppose the exchange rate is $1.03/C$. Let r $ = 7%,

r C$ = 3%, u = 1.28, d = 0.83, and T = 1.5. Using a

2-step binomial tree, calculate the value of a $1.10-strike

European put option on the Canadian dollar.

Option D is correct, but how? Can you provide solution for

Excel? formulas and steps or actual excel work sheet please?

Answers:

a.

$0.1049

b.

$0.1229

c.

$0.1302

d.

$0.1106

e.

$0.1166

Suppose the exchange rate is $1.03/C$. Let r $ = 7%,

r C$ = 3%, u = 1.28, d = 0.83, and T = 1.5. Using a

2-step binomial tree, calculate the value of a $1.10-strike

European put option on the Canadian dollar.

Option D is correct, but how? Can you provide solution for

Excel? formulas and steps or actual excel work sheet please?

Answers:

a.

$0.1049

b.

$0.1229

c.

$0.1302

d.

$0.1106

e.

$0.1166

Question I: Suppose that the exchange rate is $0.92/€. Let rs = 4%, and re = 3%, u = 1.2, d = 0.9, T = 0.75, number of binomial periods = 3, and K = $0.85. Use Binomial Option pricing to answer the following two questions. (a) What is the price of a 9-month European call? (b) What is the price of a 9-month American call?

Question I: Suppose that the exchange rate is $0.92/€. Let rs = 4%, and re = 3%, u = 1.2, d = 0.9, T = 0.75, number of binomial periods = 3, and K = $0.85. Use Binomial Option pricing to answer the following two questions. (a) What is the price of a 9-month European call? (b) What is the price of a 9-month American call?

Question I: Suppose that the exchange rate is $0.92/€. Let rs = 4%, and re = 3%, u = 1.2, d =0.9, T = 0.75, number of binomial periods = 3, and K = $0.85. Use Binomial Option pricing to answer the following two questions. Use the same inputs as in the previous (first) question, except that K = $1.00. (a) What is the price of a 9-month European call? (b) What is the price of a 9-month American call?

Question I: Suppose that the exchange rate is $0.92/€. Let rs = 4%, and re = 3%, u = 1.2, d =0.9, T = 0.75, number of binomial periods = 3, and K = $0.85. Use Binomial Option pricing to answer the following two questions. Use the same inputs as in the previous (first) question, except that K = $1.00. (a) What is the price of a 9-month European call? (b) What is the price of a 9-month American call?

Most questions answered within 3 hours.

-

Bernie's Beverages purchased some fixed assets classified as

5-year property for MACRS. The assets cost $28,000....

asked 4 minutes ago -

How many ATPs are produced from the catabolism of a 10-C

molecule of fatty acid under...

asked 8 minutes ago -

Before practicing a routine on the rings, a 64.8 kg gymnast

hangs motionless, with one hand...

asked 10 minutes ago -

If the K b of a weak base is 6.3 × 10 − 6 , what...

asked 16 minutes ago -

Which of the following is the minimum amount of moles of NaOH

that must be added...

asked 20 minutes ago -

Stories about organizational ________ provide important clues

about cultural values and norms.

a. myths

b. heroes...

asked 21 minutes ago -

Explain the criteria used in selecting a target market

BUS220 Retail Management, thank you!

asked 23 minutes ago -

Convert/Calculate the following:

Determine the identity of an elemental gas if 4.55 L weighing

35.4g, under...

asked 27 minutes ago -

Consider the equilibrium C(s)+ CO2(g) ⇌2 CO(g)

A 2.0 L flask contains a mixture of 0.10...

asked 25 minutes ago -

MATLAB

Part 1 – randFloatValue.m This function accepts two numbers,

lower and upper, and returns a...

asked 31 minutes ago -

You have been asked to hide prizes around your house for your

3-year old nephew. His...

asked 33 minutes ago -

Ammonia will decompose into nitrogen and hydrogen at high

temperature. An industrial chemist studying this reaction...

asked 39 minutes ago