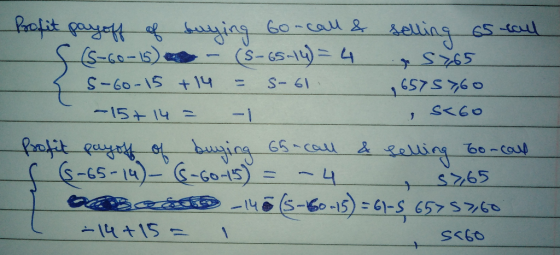

suppose a call option with a strike price of $60 has a premium of $15, while...

Homework Answers

c. do nothing because arbitrage isn’t possible

Please do rate me and mention doubts in the comments section.

Please do rate me and mention doubts in the comments section.

Add Answer to:

suppose a call option with a strike price of $60 has a premium

of $15, while...

Assume that the stock price is $56, call option price is $9, the put option price is...

Assume that the stock price is $56, call option price is $9, the put option price is $5, risk-free rate is 5%, the maturity of both options is 1 year , and the strike price of both options is 58. An investor can __the put option, ___the call option, ___the stock, and ______ to explore the arbitrage opportunity. A. sell, buy, short-sell, borrow B. buy, sell, buy, borrow C. sell, buy, short-sell, lend D. buy, sell, buy, lend

Suppose that you sell for $14 a call option with a strike price of $47, sell...

Suppose that you sell for $14 a call option with a strike price of $47, sell for $7 a call option with a strike price of $57, and buy for $9 each two call options with a strike price of $52. What is your minimum possible profit?

A call option has a premium of 2.50, the strike price is 23, and the underlying...

A call option has a premium of 2.50, the strike price is 23, and the underlying stock price is 22. What is the option's time value?

A call option on a stock with a strike price of $60 costs $8. A put...

A call option on a stock with a strike price of $60 costs $8. A put option on the same stock with the same strike price costs $6. They both expire in 1 year. (a) How can these two options be used to create a straddle? (b) What is the initial investment? (c) Construct a table showing how the payoff and profit varies with ST in 1 year, for the straddle that you constructed. Whenever you need to refer to...

There are following options available on the market: a. CALL with a strike price of 100...

There are following options available on the market: a. CALL with a strike price of 100 PLN and premium of 5 PLN b. PUT with a strike price of 100 PLN and premium of 10 PLN Is an arbitrage possible explain your strategy? Would it be possible if you could either buy or write above options with the same characteristic- explain your strategy

There are following options available on the market: a. CALL with a strike price of 100 PLN and premium of 5 PLN b. PUT with a strike price of 100 PLN and premium of 10 PLN Is an arbitrage possible explain your strategy? Would it be possible if you could either buy or write above options with the same characteristic- explain your strategy

The current stock price is 100. The call option premium with a strike price 100 is...

The current stock price is 100. The call option premium with a strike price 100 is 8. The effective risk-free interest rate is 2%. The stock pays no dividend. What is the price of a put option with strike price 100? (Both options mature in 3 months.)

Long currency straddle Call option premium = $0.05/€, Put option premium = $0.05/€ Strike price =...

Long currency straddle Call option premium = $0.05/€, Put option premium = $0.05/€ Strike price = $1.10/€, Option contract size = €62,500 Draw graphs of call option, put option, and straddle Mark BE point and Strike prices Mark each premium Spot exchange rate $1.00/€ $1.05/€ $1.10/€ $1.15/€ $1.20/€ $1.25/€ Long call option Exercise (N/Y) Holder’s net profit per unit Long put option Exercise (N/Y) Holder’s net profit per unit Net profit Net profit per unit (graph) Short currency straddle Call...

There are following options available on the market a. CALL with a strike price of 100...

There are following options available on the market a. CALL with a strike price of 100 PLN and premium of 5 PLN b. PUT with a strike price of 100 PLN and premium of 10 PLN Is an arbitrage possible- explain your strategy? Would it be possible if you could either buy or write above options with the same characteristic-explain your strategy. [1,5 pt.] Result: NO YES

There are following options available on the market a. CALL with a strike price of 100 PLN and premium of 5 PLN b. PUT with a strike price of 100 PLN and premium of 10 PLN Is an arbitrage possible- explain your strategy? Would it be possible if you could either buy or write above options with the same characteristic-explain your strategy. [1,5 pt.] Result: NO YES

There are following options available on the market a. CALL with a strike price of 100...

There are following options available on the market a. CALL with a strike price of 100 PLN and premium of 5 PLN b. PUT with a strike price of 100 PLN and premium of 10 PLN Is an arbitrage possible- explain your strategy? Would it be possible if you could either buy or write above options with the same characteristic-explain your strategy. [1,5 pt.] Result: NO YES

There are following options available on the market a. CALL with a strike price of 100 PLN and premium of 5 PLN b. PUT with a strike price of 100 PLN and premium of 10 PLN Is an arbitrage possible- explain your strategy? Would it be possible if you could either buy or write above options with the same characteristic-explain your strategy. [1,5 pt.] Result: NO YES

Suppose you sold a call option with a $50 premium. The strike price is $1,200. What...

Suppose you sold a call option with a $50 premium. The strike price is $1,200. What is your expected payoff if the price of the underlying asset is $1,000.

There are following options available on the market: a. CALL with a strike price of 100 PLN and premium of 5 PLN b. PUT with a strike price of 100 PLN and premium of 10 PLN Is an arbitrage possible explain your strategy? Would it be possible if you could either buy or write above options with the same characteristic- explain your strategy

There are following options available on the market: a. CALL with a strike price of 100 PLN and premium of 5 PLN b. PUT with a strike price of 100 PLN and premium of 10 PLN Is an arbitrage possible explain your strategy? Would it be possible if you could either buy or write above options with the same characteristic- explain your strategy

There are following options available on the market a. CALL with a strike price of 100 PLN and premium of 5 PLN b. PUT with a strike price of 100 PLN and premium of 10 PLN Is an arbitrage possible- explain your strategy? Would it be possible if you could either buy or write above options with the same characteristic-explain your strategy. [1,5 pt.] Result: NO YES

There are following options available on the market a. CALL with a strike price of 100 PLN and premium of 5 PLN b. PUT with a strike price of 100 PLN and premium of 10 PLN Is an arbitrage possible- explain your strategy? Would it be possible if you could either buy or write above options with the same characteristic-explain your strategy. [1,5 pt.] Result: NO YES

There are following options available on the market a. CALL with a strike price of 100 PLN and premium of 5 PLN b. PUT with a strike price of 100 PLN and premium of 10 PLN Is an arbitrage possible- explain your strategy? Would it be possible if you could either buy or write above options with the same characteristic-explain your strategy. [1,5 pt.] Result: NO YES

There are following options available on the market a. CALL with a strike price of 100 PLN and premium of 5 PLN b. PUT with a strike price of 100 PLN and premium of 10 PLN Is an arbitrage possible- explain your strategy? Would it be possible if you could either buy or write above options with the same characteristic-explain your strategy. [1,5 pt.] Result: NO YES

Most questions answered within 3 hours.

-

Under all the various types of market structures, firms

must eventually earn some economic profits for...

asked 3 minutes ago -

Consider the following fitness regime for a single locus trait

with two co-dominant alleles: w11 =...

asked 8 minutes ago -

A large cable company reports the following.

80% of its customers subscribe to its cable TV...

asked 23 minutes ago -

Please answer the question in brief.

Discuss the role of ERP in organizations. Are ERP tools...

asked 9 minutes ago -

Discuss the pros and cons of collaborative software such

as SameTime. Does it increase productivity? What...

asked 21 minutes ago -

1. Are all good samples random?

2. Magazines often report surveys giving statistics such as “63%...

asked 16 minutes ago -

Buying your in-laws a gift because it’s expected is

due to the ____________ motive of gift-giving....

asked 24 minutes ago -

Calculate the expected value, the variance, and the standard

deviation of the given random variable X....

asked 1 hour ago -

A hospital performs 100 surgeries per week. The probability that

complications after surgery occur is 10%....

asked 1 hour ago -

1 point) Given the significance level α=0.01 find the following:

(a) left-tailed z value z= (b)...

asked 1 hour ago -

Assuming you are the head of the software development unit at

Cyber.Soft, explain and justify why...

asked 32 minutes ago -

Magnesium and nitrogen react in a combination reaction to

produce magnesium nitride. 3 Mg + N2...

asked 40 minutes ago