One Period Binomial Model, Using the AAPL option chain, solve for the at the money (X...

- One Period Binomial Model, Using the AAPL option chain, solve for the at the money (X = 225) call and put options. Assume U = 1.2, πu= 0.6, Rf = 0.50%. Show all your work.

Homework Answers

Answer:

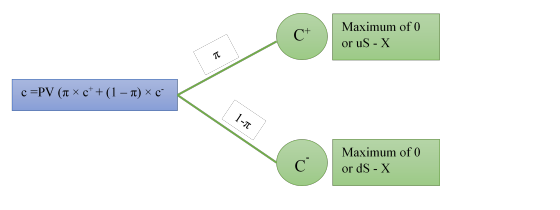

Binomial option pricing model is a risk-neutral model used to value path-dependent options such as American options. Under the binomial model, current value of an option equals the present value of the probability-weighted future payoffs from the options.

Add Answer to:

One Period Binomial Model, Using the AAPL option chain, solve

for the at the money (X...

One Period Binomial Model, Using the AAPL option chain, solve for the at the money (X...

One Period Binomial Model, Using the AAPL option chain, solve for the at the money (X = 225) call and put options. Assume U = 1.2, πu= 0.6, Rf = 0.50%. Show all your work.

NEED HELP WITH ALL QUESTIONS PLEASE!!!!! 14. Consider a one period binomial model. The initial stock...

NEED HELP WITH ALL QUESTIONS PLEASE!!!!!

14. Consider a one period binomial model. The initial stock price is $30. Over the next 3 months, the stock price could either go up to $36 (u = 1.2) or go down to $24 (d = 0.8). The continuously compounded interest rate is 6% per annum. Use this information to answer the remaining questions in this assignment. Consider a call option whose strike price is $32. How many shares should be bought or...

NEED HELP WITH ALL QUESTIONS PLEASE!!!!!

14. Consider a one period binomial model. The initial stock price is $30. Over the next 3 months, the stock price could either go up to $36 (u = 1.2) or go down to $24 (d = 0.8). The continuously compounded interest rate is 6% per annum. Use this information to answer the remaining questions in this assignment. Consider a call option whose strike price is $32. How many shares should be bought or...

1. (5 points) Find the value of a call option using a one-period binomial lattice model....

1. (5 points) Find the value of a call option using a one-period binomial lattice model. The underlying stock has initial price $100 and lattice parameters u = 5/4, d = 4/5. The risk free interest rate is 10% and the strike price is $105.

1. (5 points) Find the value of a call option using a one-period binomial lattice model. The underlying stock has initial price $100 and lattice parameters u = 5/4, d = 4/5. The risk free interest rate is 10% and the strike price is $105.

4. Option pricing model - Binomial approach Learn Corp. (Ticker: LC), an education technology company, is...

4. Option pricing model - Binomial approach Learn Corp. (Ticker: LC), an education technology company, is considered to be one of the least risky companies in the education sector. Investors trade call options for Learn Corp., whose stock is currently trading at $50.00. Suppose you are interested in buying a call option with a strike price of $40.00 that expires in 6 months. (Assume that you get the option for freel) Based on speculations and probability analysis, you compute and...

4. Option pricing model - Binomial approach Learn Corp. (Ticker: LC), an education technology company, is considered to be one of the least risky companies in the education sector. Investors trade call options for Learn Corp., whose stock is currently trading at $50.00. Suppose you are interested in buying a call option with a strike price of $40.00 that expires in 6 months. (Assume that you get the option for freel) Based on speculations and probability analysis, you compute and...

3. Use a one step binomial option pricing model to value a 1 year at the...

3. Use a one step binomial option pricing model to value a 1 year at the money call option on AT&T. Assume interest rates are 2%. How does your value compare with the market price?

3. Use a one step binomial option pricing model to value a 1 year at the money call option on AT&T. Assume interest rates are 2%. How does your value compare with the market price?

Consider a two-period binomial model on an European put option. The stock is currently worth 48....

Consider a two-period binomial model on an European put option. The stock is currently worth 48. The exercise price is 52. The risk-free rate is 5% U = 1.15 and D=.9 . Price the European put option.

Use a two-step binomial model to evaluate a call option on a stock with the following...

Use a two-step binomial model to evaluate a call option on a stock with the following price projections. The current stock price is $80 and the strike price on the options is $82. The option expires in 6 months so each step is 3 months. The risk- free rate is 5%. What is the value of the call option? Note: to be eligible for partial credit, please show your work as much as possible and be sure to clearly indicate...

Use a two-step binomial model to evaluate a call option on a stock with the following price projections. The current stock price is $80 and the strike price on the options is $82. The option expires in 6 months so each step is 3 months. The risk- free rate is 5%. What is the value of the call option? Note: to be eligible for partial credit, please show your work as much as possible and be sure to clearly indicate...

A certain Call option and Put option for Walker Industries stock both have an exercise (strike)...

A certain Call option and Put option for Walker Industries stock both have an exercise (strike) price of $35.00. The Call premium (price) is $3.21 and the Put premium (price) is $5.32. Assume the stock pays NO dividends, and that the risk-free rate is 4%. Both options expire in 41 days. 1. Using the put/call parity model, calculate the current stock price (S). (Show all work. Highlight in bold your answer.) [4 pts.] 2. Based upon your answer above for...

5. Option pricing - Single-period binomial approach A Aa The value of an option can be...

5. Option pricing - Single-period binomial approach A Aa The value of an option can be calculated by using a step-by-step approach in the case of single periods or by using sophisticated formulas that can be easily created through a spreadsheet. In the real world, two possible outcomes for a stock price in six months is an assumption. The stock markets are volatile, and stocks move up and down based on market- and firm-specific factors. Consider the case of Canada...

5. Option pricing - Single-period binomial approach A Aa The value of an option can be calculated by using a step-by-step approach in the case of single periods or by using sophisticated formulas that can be easily created through a spreadsheet. In the real world, two possible outcomes for a stock price in six months is an assumption. The stock markets are volatile, and stocks move up and down based on market- and firm-specific factors. Consider the case of Canada...

In a binomial tree model, S0=32. In the next period, ST is either 35 or 30....

In a binomial tree model, S0=32. In the next period, ST is either 35 or 30. Assume interest rate is 0. Calculate the price of a call option with strike equal to 31. A. 0.6 B. 1 C. 1.6 D. 2

NEED HELP WITH ALL QUESTIONS PLEASE!!!!!

14. Consider a one period binomial model. The initial stock price is $30. Over the next 3 months, the stock price could either go up to $36 (u = 1.2) or go down to $24 (d = 0.8). The continuously compounded interest rate is 6% per annum. Use this information to answer the remaining questions in this assignment. Consider a call option whose strike price is $32. How many shares should be bought or...

NEED HELP WITH ALL QUESTIONS PLEASE!!!!!

14. Consider a one period binomial model. The initial stock price is $30. Over the next 3 months, the stock price could either go up to $36 (u = 1.2) or go down to $24 (d = 0.8). The continuously compounded interest rate is 6% per annum. Use this information to answer the remaining questions in this assignment. Consider a call option whose strike price is $32. How many shares should be bought or...

1. (5 points) Find the value of a call option using a one-period binomial lattice model. The underlying stock has initial price $100 and lattice parameters u = 5/4, d = 4/5. The risk free interest rate is 10% and the strike price is $105.

1. (5 points) Find the value of a call option using a one-period binomial lattice model. The underlying stock has initial price $100 and lattice parameters u = 5/4, d = 4/5. The risk free interest rate is 10% and the strike price is $105.

4. Option pricing model - Binomial approach Learn Corp. (Ticker: LC), an education technology company, is considered to be one of the least risky companies in the education sector. Investors trade call options for Learn Corp., whose stock is currently trading at $50.00. Suppose you are interested in buying a call option with a strike price of $40.00 that expires in 6 months. (Assume that you get the option for freel) Based on speculations and probability analysis, you compute and...

4. Option pricing model - Binomial approach Learn Corp. (Ticker: LC), an education technology company, is considered to be one of the least risky companies in the education sector. Investors trade call options for Learn Corp., whose stock is currently trading at $50.00. Suppose you are interested in buying a call option with a strike price of $40.00 that expires in 6 months. (Assume that you get the option for freel) Based on speculations and probability analysis, you compute and...

3. Use a one step binomial option pricing model to value a 1 year at the money call option on AT&T. Assume interest rates are 2%. How does your value compare with the market price?

3. Use a one step binomial option pricing model to value a 1 year at the money call option on AT&T. Assume interest rates are 2%. How does your value compare with the market price?

Use a two-step binomial model to evaluate a call option on a stock with the following price projections. The current stock price is $80 and the strike price on the options is $82. The option expires in 6 months so each step is 3 months. The risk- free rate is 5%. What is the value of the call option? Note: to be eligible for partial credit, please show your work as much as possible and be sure to clearly indicate...

Use a two-step binomial model to evaluate a call option on a stock with the following price projections. The current stock price is $80 and the strike price on the options is $82. The option expires in 6 months so each step is 3 months. The risk- free rate is 5%. What is the value of the call option? Note: to be eligible for partial credit, please show your work as much as possible and be sure to clearly indicate...

5. Option pricing - Single-period binomial approach A Aa The value of an option can be calculated by using a step-by-step approach in the case of single periods or by using sophisticated formulas that can be easily created through a spreadsheet. In the real world, two possible outcomes for a stock price in six months is an assumption. The stock markets are volatile, and stocks move up and down based on market- and firm-specific factors. Consider the case of Canada...

5. Option pricing - Single-period binomial approach A Aa The value of an option can be calculated by using a step-by-step approach in the case of single periods or by using sophisticated formulas that can be easily created through a spreadsheet. In the real world, two possible outcomes for a stock price in six months is an assumption. The stock markets are volatile, and stocks move up and down based on market- and firm-specific factors. Consider the case of Canada...

Most questions answered within 3 hours.

-

Verify the MIRR is 9.29% given cash flows in years 1 and 2 of

$1,000 each,...

asked 14 minutes ago -

Calculate the pH of a 5.7 M solution of aniline (C6H5NH2; Kb =

3.8 x 10^-10)

asked 2 hours ago -

LSL R3, R3, R12

Memory

Address

Orig.

Data

Updated

Data

Register

Orig.

Data

Updated

Data

0x84F0...

asked 2 hours ago -

Air at 100 kPa and density of 1.2 kg/m3 flows upward through a

5-cm diameter inclined...

asked 2 hours ago -

Define the following concepts in your own words: (a) stiffness,

(b) strength, (c) strain,

(d) ductility,...

asked 3 hours ago -

In C++

In this homework, you will be tasked with creating functions to

manipulate strings that...

asked 3 hours ago -

An isolated colony represents a pure culture. one rare occasions

, however , a colony can...

asked 3 hours ago -

*****DO NOT ANSWER THIS QUESTION IF YOU DON'T

KNOW*******Rights and Duties of Auditors; Minimum 4000

words...

asked 4 hours ago -

The probability that Janie is wearing sunglasses is 1/4. The

probability that she is wearing sunglasses...

asked 5 hours ago -

Do you believe social media is more of a help or a hindrance in

controlling crises...

asked 5 hours ago -

Two long, parallel wires separated by 2.85 cm carry currents in

opposite directions. The current in...

asked 5 hours ago -

Question # 1. Develop a list of rehabilitation journals

that publish articles concerning career counseling for...

asked 5 hours ago