Homework Answers

Ans) Perfectly competitive market is where there are many sellers selling homogeneous products. Price is decided by forces of demand and supply. This price is equal to marginal revenue of an individual firm. A profit maximising firm produces the quantity where MR and MC curve intersect.

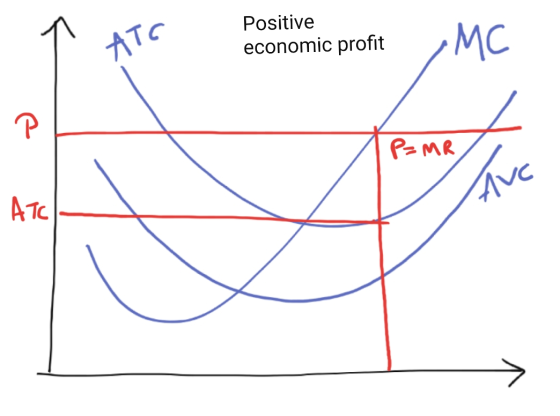

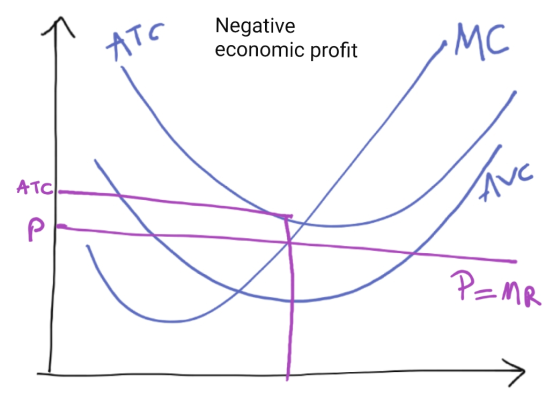

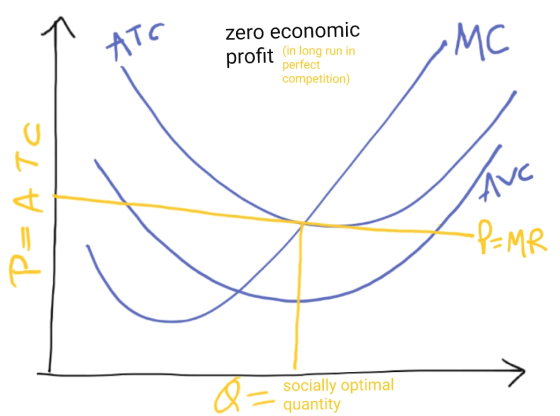

Firms earn positive economic profit when price (or marginal revenue) is above ATC. Firm earns negative economic profit when price is below ATC. And it earns zero economic profit when price is equal to ATC.

Option a is long run equilibrium for a competitive firm where it earns zero economic profit.

Answer is Option b.

Add Answer to:

When a competitive firm will produce and earn economic profits. marginal revenue = average total cost...

In the short run, a perfectly competitive firm might earn negative economic profits and then decide...

In the short run, a perfectly competitive firm might earn negative economic profits and then decide to shut down. On a graph, show this situation, using marginal revenue, marginal cost, average-total-cost, and average-variable-cost curves. Indicate the level of output at which the firm will no longer produce. Explain why your graph shows the shut down point.

The monopolist chooses to produce: O at an inefficient outcome. where marginal cost equals marginal revenue....

The monopolist chooses to produce: O at an inefficient outcome. where marginal cost equals marginal revenue. at a lower quantity than the perfectly competitive firm. O All of these statements are true. In the short run, monopolistically competitive firms: will earn zero economic profits by acting like a monopolist. O can earn positive economic profits by acting like a perfectly competitive firm. will earn zero economic profits by acting like a perfectly competitive firm. can earn positive economic profits by...

The monopolist chooses to produce: O at an inefficient outcome. where marginal cost equals marginal revenue. at a lower quantity than the perfectly competitive firm. O All of these statements are true. In the short run, monopolistically competitive firms: will earn zero economic profits by acting like a monopolist. O can earn positive economic profits by acting like a perfectly competitive firm. will earn zero economic profits by acting like a perfectly competitive firm. can earn positive economic profits by...

15. When marginal cost is less than average total cost, a. marginal cost must be falling....

15. When marginal cost is less than average total cost, a. marginal cost must be falling. b. average variable cost must be falling. c. average total cost is falling. d. average total cost is rising. 16. Which of the following is not a characteristic of a competitive market? a. Buyers and sellers are price takers. b. Each firm sells a virtually identical product. c. Entry is limited d. Each firm chooses an output level that maximizes profits. 17. If a...

15. When marginal cost is less than average total cost, a. marginal cost must be falling. b. average variable cost must be falling. c. average total cost is falling. d. average total cost is rising. 16. Which of the following is not a characteristic of a competitive market? a. Buyers and sellers are price takers. b. Each firm sells a virtually identical product. c. Entry is limited d. Each firm chooses an output level that maximizes profits. 17. If a...

Plastic and Co manufactures industrial plastic containers. As petroleum prices fall, the price of plastic materials...

Plastic and Co manufactures industrial plastic containers. As petroleum prices fall, the price of plastic materials also falls. As a result, a: Plastic and Co’s marginal cost curve will shift. b: The market price for the plastic containers will rise, other things equal. c: The fixed cost curve for Plastic and Co would shift downward. d: Average cost curve of plastic containers will shift upward. When ________, a competitive firm will produce and earn economic profits. a: marginal revenue is...

1l. If a monopolistically competitive firm is incurring losses, then at the profit-max a price is above the average total cost curve. b. price is below the average total cost curve c. price is equal...

1l. If a monopolistically competitive firm is incurring losses, then at the profit-max a price is above the average total cost curve. b. price is below the average total cost curve c. price is equal to marginal revenue. d. price is less than marginal revenue. e. average total cost equals marginal cost. Both competitive and monopolistically competitive firms a. can maximize profit by raising price. b. cannot control or set their own price c. can maximize profit by producing to...

1l. If a monopolistically competitive firm is incurring losses, then at the profit-max a price is above the average total cost curve. b. price is below the average total cost curve c. price is equal to marginal revenue. d. price is less than marginal revenue. e. average total cost equals marginal cost. Both competitive and monopolistically competitive firms a. can maximize profit by raising price. b. cannot control or set their own price c. can maximize profit by producing to...

1) A perfectly competitive firm faces the following Total revenue, Total cost and Marginal cost functions:...

1) A perfectly competitive firm faces the following Total revenue, Total cost and Marginal cost functions: TR = 10Q TC = 2 + 2Q + Q2 MC = 2 + 2Q At the level of output maximizing profit , the above firm's level of economic profit is A) $0 B) $4 C) $6 D) $8 *Additional information after I did the math: The price this firm charges for its product is $10, the level of output maximizing profit is 4...

QUESTION 7 Monopolistic competitive firms in the long run earn: positive economic profits. zero pure economic...

QUESTION 7 Monopolistic competitive firms in the long run earn: positive economic profits. zero pure economic profits. negative economic profits. Positive, zero, or negative economic profits. QUESTION 8 Which of the following statements best describes firms under monopolistic competition? Profits will be positive in the long run. Price always equals average variable cost. In the long run, positive economic profit will be eliminated. Marginal revenue equals minimum average total cost in the short run. QUESTION 9 Which of the following...

Profits will always be maximized when total revenue equals total cost =T or F If marginal...

Profits will always be maximized when total revenue equals total cost =T or F If marginal revenue for an extra unit is positive, then selling the extra unit causes total revenue to rise. T or F Given a downward-sloping demand curve and positive marginal costs, profit-maximizing firms will always sell less output at higher prices than will revenue-maximizing firms. T or F Marginal profit is the difference between marginal revenue and marginal cost, and will always equal zero at the...

8. Refer to the graph above depicting a perfectly competitive firm. When maximizing profit, the total...

8. Refer to the graph above depicting a perfectly competitive firm. When maximizing profit, the total profit earned by the firm represented is: A. $220. B. $275. C. $330 D. $605, 26. Refer to the graph above of a monopolistically competitive firm. If the firm maximizes profit, it will earn: A. zero economic profit this year. B. $320,000 economic profit this year. C. 584,000 economic profit this year. D. $56,000 economic profit this year. ATC AVC - 01 02 03...

8. Refer to the graph above depicting a perfectly competitive firm. When maximizing profit, the total profit earned by the firm represented is: A. $220. B. $275. C. $330 D. $605, 26. Refer to the graph above of a monopolistically competitive firm. If the firm maximizes profit, it will earn: A. zero economic profit this year. B. $320,000 economic profit this year. C. 584,000 economic profit this year. D. $56,000 economic profit this year. ATC AVC - 01 02 03...

In a perfectly competitive market, a firm profit maximizes by choosing to produce the level of...

In a perfectly competitive market, a firm profit maximizes by choosing to produce the level of output for which a. marginal revenue equals marginal cost. b. total revenue equals marginal costs. c. externalities are minimized. d. net social benefits are greatest. e. marginal costs are minimized. . if economic profits are positive for firms in a perfectly competitive market, then a. market supply will shift to the left. b. each firm will decrease production. c. new firms will enter the...

The monopolist chooses to produce: O at an inefficient outcome. where marginal cost equals marginal revenue. at a lower quantity than the perfectly competitive firm. O All of these statements are true. In the short run, monopolistically competitive firms: will earn zero economic profits by acting like a monopolist. O can earn positive economic profits by acting like a perfectly competitive firm. will earn zero economic profits by acting like a perfectly competitive firm. can earn positive economic profits by...

The monopolist chooses to produce: O at an inefficient outcome. where marginal cost equals marginal revenue. at a lower quantity than the perfectly competitive firm. O All of these statements are true. In the short run, monopolistically competitive firms: will earn zero economic profits by acting like a monopolist. O can earn positive economic profits by acting like a perfectly competitive firm. will earn zero economic profits by acting like a perfectly competitive firm. can earn positive economic profits by...

15. When marginal cost is less than average total cost, a. marginal cost must be falling. b. average variable cost must be falling. c. average total cost is falling. d. average total cost is rising. 16. Which of the following is not a characteristic of a competitive market? a. Buyers and sellers are price takers. b. Each firm sells a virtually identical product. c. Entry is limited d. Each firm chooses an output level that maximizes profits. 17. If a...

15. When marginal cost is less than average total cost, a. marginal cost must be falling. b. average variable cost must be falling. c. average total cost is falling. d. average total cost is rising. 16. Which of the following is not a characteristic of a competitive market? a. Buyers and sellers are price takers. b. Each firm sells a virtually identical product. c. Entry is limited d. Each firm chooses an output level that maximizes profits. 17. If a...

1l. If a monopolistically competitive firm is incurring losses, then at the profit-max a price is above the average total cost curve. b. price is below the average total cost curve c. price is equal to marginal revenue. d. price is less than marginal revenue. e. average total cost equals marginal cost. Both competitive and monopolistically competitive firms a. can maximize profit by raising price. b. cannot control or set their own price c. can maximize profit by producing to...

1l. If a monopolistically competitive firm is incurring losses, then at the profit-max a price is above the average total cost curve. b. price is below the average total cost curve c. price is equal to marginal revenue. d. price is less than marginal revenue. e. average total cost equals marginal cost. Both competitive and monopolistically competitive firms a. can maximize profit by raising price. b. cannot control or set their own price c. can maximize profit by producing to...

8. Refer to the graph above depicting a perfectly competitive firm. When maximizing profit, the total profit earned by the firm represented is: A. $220. B. $275. C. $330 D. $605, 26. Refer to the graph above of a monopolistically competitive firm. If the firm maximizes profit, it will earn: A. zero economic profit this year. B. $320,000 economic profit this year. C. 584,000 economic profit this year. D. $56,000 economic profit this year. ATC AVC - 01 02 03...

8. Refer to the graph above depicting a perfectly competitive firm. When maximizing profit, the total profit earned by the firm represented is: A. $220. B. $275. C. $330 D. $605, 26. Refer to the graph above of a monopolistically competitive firm. If the firm maximizes profit, it will earn: A. zero economic profit this year. B. $320,000 economic profit this year. C. 584,000 economic profit this year. D. $56,000 economic profit this year. ATC AVC - 01 02 03...

Most questions answered within 3 hours.

-

An FM modulator is tested using

single-tone baseband signal with frequency of 50kHz and a sprectrum...

asked 3 minutes ago -

Write the ionic equations for the first stage of salts

hydrolysis.

Anion, Cation?

Na2S

NiSO4

K2SO4...

asked 1 hour ago -

suppose there is a normally distributed population with a mean of

250 and a standard deviation...

asked 2 hours ago -

Question Three

Suppose you as project manager are using the Waterfall

development methodology on a large...

asked 3 hours ago -

Which statement is not true about welfare in Canada?

A.Benefits typically vary based on one's ability...

asked 3 hours ago -

Please help me with FLOWCHART and UML diagram for class,

thank you!

#include <iostream>

#include <fstream>...

asked 4 hours ago -

3. Describe the “logic circuit” of the Lac operon. Which

proteins are bound or not to...

asked 4 hours ago -

Ayesha’s adjusted gross income is $60,000 in 2019. She donated a

piece of artwork with a...

asked 4 hours ago -

For Dijkstra’s shortest path algorithm:

a. Give the Big-O time for Dijkstra’s shortest path algorithm

and...

asked 4 hours ago -

Phosphorus violates the 'octet rule' in biological molecules,

forming more covalent bonds than expected based on...

asked 4 hours ago -

A 1.3 eV electron has a 10-4 probability of tunneling

through a 2.4 eV potential barrier....

asked 5 hours ago -

What is the one ingredient that is common to being successful

with all stakeholders?

profit

trust...

asked 5 hours ago