Homework Answers

a) The risk that are non-diversifiable is the risk which is common across all the securities and the market, also known as the systematic risk. This is measured in terms of beta. Some of the examples of systematic risk are interest rate change, natural disaster, Civil war within the country impacting the daily activities.

b) The asset that would have the greatest impact with the change in the market return is the one which has the highest beta because in CAPM model beta is the measure of risk hence asset 2will have the highest impact.

c) The expected return according to CAPM model is

Risk free rate + beta *(market return – risk free rate)

= 2.5 + 1.25*(10 – 2.5)

=11.875%

Add Answer to:

(a) In CAPM framework, there are risks that are diversifiable. What are the non-diversifiable risks? (2...

Part D and E please 2. Consider the information in Table 1. Table 1 Correlation with...

Part D and E please

2. Consider the information in Table 1. Table 1 Correlation with market portfolio 0.20 0.80 1.00 0.00 Standard deviation Return Beta Stock 1 Stock 2 Market portfolio Risk-free asset 5% 12% 8% 0% 16% 2% 0 (a) Consider Table 1. Calculate betas for stock I and stock 2 (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for stocks 1 and 2 (c) Consider Table 1 and the equilibrium expected returns...

Part D and E please

2. Consider the information in Table 1. Table 1 Correlation with market portfolio 0.20 0.80 1.00 0.00 Standard deviation Return Beta Stock 1 Stock 2 Market portfolio Risk-free asset 5% 12% 8% 0% 16% 2% 0 (a) Consider Table 1. Calculate betas for stock I and stock 2 (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for stocks 1 and 2 (c) Consider Table 1 and the equilibrium expected returns...

I would like part d and e answered please 2. Consider the information in Table 1...

I would like part d and e answered please

2. Consider the information in Table 1 Table 1 Correlation with market portfolio 0.20 0.80 1.00 0.00 Standard deviation Return Beta Stock 1 Stock 2 Market portfolio 6% 12% 8% 0% 16% 2% Risk-free asset 0 (a) Consider Table 1. Calculate betas for stock 1 and stock 2. (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for stocks 1 and 2. (c) Consider Table 1 and...

I would like part d and e answered please

2. Consider the information in Table 1 Table 1 Correlation with market portfolio 0.20 0.80 1.00 0.00 Standard deviation Return Beta Stock 1 Stock 2 Market portfolio 6% 12% 8% 0% 16% 2% Risk-free asset 0 (a) Consider Table 1. Calculate betas for stock 1 and stock 2. (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for stocks 1 and 2. (c) Consider Table 1 and...

please provide assistance with the following as well as step by step instruction question 4 your...

please provide assistance with the following as well as step by

step instruction

question 4

your portfolio is invested 30% each in A and C, and 40% in B

what us the expected return if the portfolio? Also what is the

variance of this portfolio? the standard deviation. pleas give

steps and calculation

3. Returns and Variances [LOI] Consider the following information: Rate of Return If Probability of State of State of State Occurs Economy Economy Stock Stock Stock A...

please provide assistance with the following as well as step by

step instruction

question 4

your portfolio is invested 30% each in A and C, and 40% in B

what us the expected return if the portfolio? Also what is the

variance of this portfolio? the standard deviation. pleas give

steps and calculation

3. Returns and Variances [LOI] Consider the following information: Rate of Return If Probability of State of State of State Occurs Economy Economy Stock Stock Stock A...

2. Consider the information in Table1. Table 1 Standard Deviation of Stock Stock Correlation with Market...

2. Consider the information in Table1. Table 1 Standard Deviation of Stock Stock Correlation with Market Portfolio 0.75 0.20 Stock 20% 15% 14% 0% 49% ected Market Return Risk Free Rate Return (a) Consider Table 1 . Calculate betas for Stock 1, Stock 2, and a portfolio consisting of 75% invested in Stock 1 and (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for Stock 1, Stock 2, and the (c) Consider Table 1 and...

2. Consider the information in Table1. Table 1 Standard Deviation of Stock Stock Correlation with Market Portfolio 0.75 0.20 Stock 20% 15% 14% 0% 49% ected Market Return Risk Free Rate Return (a) Consider Table 1 . Calculate betas for Stock 1, Stock 2, and a portfolio consisting of 75% invested in Stock 1 and (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for Stock 1, Stock 2, and the (c) Consider Table 1 and...

Consider the following information about three stocks: State of Economy Probability of State Rate of Return...

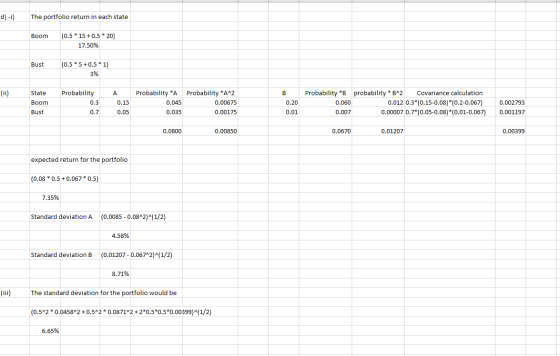

Consider the following information about three stocks: State of Economy Probability of State Rate of Return if State Occurs Stock A Stock B 0.24 0.36 0.17 0.13 0.00 -0.28 Boom Normal Bust 0.35 0.50 0.15 Stock C 0.55 0.09 -0.45 a. What is the expected return of Stock A? The standard deviation? (6 points) b. If your portfolio is invested 40% each in A and B and 20% in C, what is the portfolio expected return? The standard deviation? (13...

Consider the following information about three stocks: State of Economy Probability of State Rate of Return if State Occurs Stock A Stock B 0.24 0.36 0.17 0.13 0.00 -0.28 Boom Normal Bust 0.35 0.50 0.15 Stock C 0.55 0.09 -0.45 a. What is the expected return of Stock A? The standard deviation? (6 points) b. If your portfolio is invested 40% each in A and B and 20% in C, what is the portfolio expected return? The standard deviation? (13...

Consider the following information about three stocks: Probability of Rate of Return if State of Economy...

Consider the following information about three stocks: Probability of Rate of Return if State of Economy State State Occurs Stock A Stock B Stock C 0.24 Boom 0.35 0.36 0.55 0.13 Normal 0.50 0.17 0.09 -0.28 Bust 0.15 0.00 -0.45 a. What is the expected return of Stock A? The standard deviation? (6 points) b. If your portfolio is invested 40% each in A and B and 20% in C, what is the portfolio expected return? The standard deviation? (13...

Consider the following information about three stocks: Probability of Rate of Return if State of Economy State State Occurs Stock A Stock B Stock C 0.24 Boom 0.35 0.36 0.55 0.13 Normal 0.50 0.17 0.09 -0.28 Bust 0.15 0.00 -0.45 a. What is the expected return of Stock A? The standard deviation? (6 points) b. If your portfolio is invested 40% each in A and B and 20% in C, what is the portfolio expected return? The standard deviation? (13...

Home assignment 4 Consider following information Probability of the state of economy Rate of return if state occurs StockA StockB boom normal a. b. c. 0.2 0.8 0.4 0.2 0.05 Calculate the expected...

Home assignment 4 Consider following information Probability of the state of economy Rate of return if state occurs StockA StockB boom normal a. b. c. 0.2 0.8 0.4 0.2 0.05 Calculate the expected return of Calculate the variance and standard deviation of each stock. Calculate the covariance between stock A and B returns and the correlation coefficient. Calculate the expected return of the portfolio (Portfolio!) consisting 40% of stock A and 60% of stock B. Calculate the variance and standard...

Home assignment 4 Consider following information Probability of the state of economy Rate of return if state occurs StockA StockB boom normal a. b. c. 0.2 0.8 0.4 0.2 0.05 Calculate the expected return of Calculate the variance and standard deviation of each stock. Calculate the covariance between stock A and B returns and the correlation coefficient. Calculate the expected return of the portfolio (Portfolio!) consisting 40% of stock A and 60% of stock B. Calculate the variance and standard...

Assume that the assumptions of the CAPM hold. The expected return and the standard deviation of...

Assume that the assumptions of the CAPM hold. The expected return and the standard deviation of the market portfolio are 7% and 14%, respectively. There are two individual stocks A and B: Mean Return A: 4% Standard Deviation A: 18% Mean Return B: 12% Standard Deviation B: 36% Stock A has a correlation of 0.2 with the market portfolio. A.What is the beta of stock A? B.What is the risk free rate? C.What is the beta of a portfolio with...

Ravi, a fund manager working for a private equity firm, is considering including the following stocks...

Ravi, a fund manager working for a private equity firm, is

considering including the following stocks in the firm’s

portfolio:

He plans to invest 40% of the portfolio funds in stock RST and

the balance equally between VVR and BAB. Beta of stock VVR is 0.15

higher than RST.

The firm’s in-house economist anticipates the probability of

boom, normal and recession to be 25%, 40% and 35% respectively. The

yield on long term government securities is 3% per year.

(a)...

Ravi, a fund manager working for a private equity firm, is

considering including the following stocks in the firm’s

portfolio:

He plans to invest 40% of the portfolio funds in stock RST and

the balance equally between VVR and BAB. Beta of stock VVR is 0.15

higher than RST.

The firm’s in-house economist anticipates the probability of

boom, normal and recession to be 25%, 40% and 35% respectively. The

yield on long term government securities is 3% per year.

(a)...

2. Company A's stock has a beta of BA 1.5, and Company B's stock has a beta of βΒ-2.5. Expected r...

2. Company A's stock has a beta of BA 1.5, and Company B's stock has a beta of βΒ-2.5. Expected returns on this two stocks are E [rA]-9.5 and E rB 14.5. Assume CAPM holds. At age 30, you decide to allocate ALL your financial wealth of $100k between stock A and stock B, with portfolio weights wA + wB1. You would like this portfolio to be risky such that Bp- 3 (a) Solve for wA and wB- (b) State...

2. Company A's stock has a beta of BA 1.5, and Company B's stock has a beta of βΒ-2.5. Expected returns on this two stocks are E [rA]-9.5 and E rB 14.5. Assume CAPM holds. At age 30, you decide to allocate ALL your financial wealth of $100k between stock A and stock B, with portfolio weights wA + wB1. You would like this portfolio to be risky such that Bp- 3 (a) Solve for wA and wB- (b) State...

Part D and E please

2. Consider the information in Table 1. Table 1 Correlation with market portfolio 0.20 0.80 1.00 0.00 Standard deviation Return Beta Stock 1 Stock 2 Market portfolio Risk-free asset 5% 12% 8% 0% 16% 2% 0 (a) Consider Table 1. Calculate betas for stock I and stock 2 (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for stocks 1 and 2 (c) Consider Table 1 and the equilibrium expected returns...

Part D and E please

2. Consider the information in Table 1. Table 1 Correlation with market portfolio 0.20 0.80 1.00 0.00 Standard deviation Return Beta Stock 1 Stock 2 Market portfolio Risk-free asset 5% 12% 8% 0% 16% 2% 0 (a) Consider Table 1. Calculate betas for stock I and stock 2 (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for stocks 1 and 2 (c) Consider Table 1 and the equilibrium expected returns...

I would like part d and e answered please

2. Consider the information in Table 1 Table 1 Correlation with market portfolio 0.20 0.80 1.00 0.00 Standard deviation Return Beta Stock 1 Stock 2 Market portfolio 6% 12% 8% 0% 16% 2% Risk-free asset 0 (a) Consider Table 1. Calculate betas for stock 1 and stock 2. (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for stocks 1 and 2. (c) Consider Table 1 and...

I would like part d and e answered please

2. Consider the information in Table 1 Table 1 Correlation with market portfolio 0.20 0.80 1.00 0.00 Standard deviation Return Beta Stock 1 Stock 2 Market portfolio 6% 12% 8% 0% 16% 2% Risk-free asset 0 (a) Consider Table 1. Calculate betas for stock 1 and stock 2. (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for stocks 1 and 2. (c) Consider Table 1 and...

please provide assistance with the following as well as step by

step instruction

question 4

your portfolio is invested 30% each in A and C, and 40% in B

what us the expected return if the portfolio? Also what is the

variance of this portfolio? the standard deviation. pleas give

steps and calculation

3. Returns and Variances [LOI] Consider the following information: Rate of Return If Probability of State of State of State Occurs Economy Economy Stock Stock Stock A...

please provide assistance with the following as well as step by

step instruction

question 4

your portfolio is invested 30% each in A and C, and 40% in B

what us the expected return if the portfolio? Also what is the

variance of this portfolio? the standard deviation. pleas give

steps and calculation

3. Returns and Variances [LOI] Consider the following information: Rate of Return If Probability of State of State of State Occurs Economy Economy Stock Stock Stock A...

2. Consider the information in Table1. Table 1 Standard Deviation of Stock Stock Correlation with Market Portfolio 0.75 0.20 Stock 20% 15% 14% 0% 49% ected Market Return Risk Free Rate Return (a) Consider Table 1 . Calculate betas for Stock 1, Stock 2, and a portfolio consisting of 75% invested in Stock 1 and (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for Stock 1, Stock 2, and the (c) Consider Table 1 and...

2. Consider the information in Table1. Table 1 Standard Deviation of Stock Stock Correlation with Market Portfolio 0.75 0.20 Stock 20% 15% 14% 0% 49% ected Market Return Risk Free Rate Return (a) Consider Table 1 . Calculate betas for Stock 1, Stock 2, and a portfolio consisting of 75% invested in Stock 1 and (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for Stock 1, Stock 2, and the (c) Consider Table 1 and...

Consider the following information about three stocks: State of Economy Probability of State Rate of Return if State Occurs Stock A Stock B 0.24 0.36 0.17 0.13 0.00 -0.28 Boom Normal Bust 0.35 0.50 0.15 Stock C 0.55 0.09 -0.45 a. What is the expected return of Stock A? The standard deviation? (6 points) b. If your portfolio is invested 40% each in A and B and 20% in C, what is the portfolio expected return? The standard deviation? (13...

Consider the following information about three stocks: State of Economy Probability of State Rate of Return if State Occurs Stock A Stock B 0.24 0.36 0.17 0.13 0.00 -0.28 Boom Normal Bust 0.35 0.50 0.15 Stock C 0.55 0.09 -0.45 a. What is the expected return of Stock A? The standard deviation? (6 points) b. If your portfolio is invested 40% each in A and B and 20% in C, what is the portfolio expected return? The standard deviation? (13...

Consider the following information about three stocks: Probability of Rate of Return if State of Economy State State Occurs Stock A Stock B Stock C 0.24 Boom 0.35 0.36 0.55 0.13 Normal 0.50 0.17 0.09 -0.28 Bust 0.15 0.00 -0.45 a. What is the expected return of Stock A? The standard deviation? (6 points) b. If your portfolio is invested 40% each in A and B and 20% in C, what is the portfolio expected return? The standard deviation? (13...

Consider the following information about three stocks: Probability of Rate of Return if State of Economy State State Occurs Stock A Stock B Stock C 0.24 Boom 0.35 0.36 0.55 0.13 Normal 0.50 0.17 0.09 -0.28 Bust 0.15 0.00 -0.45 a. What is the expected return of Stock A? The standard deviation? (6 points) b. If your portfolio is invested 40% each in A and B and 20% in C, what is the portfolio expected return? The standard deviation? (13...

Home assignment 4 Consider following information Probability of the state of economy Rate of return if state occurs StockA StockB boom normal a. b. c. 0.2 0.8 0.4 0.2 0.05 Calculate the expected return of Calculate the variance and standard deviation of each stock. Calculate the covariance between stock A and B returns and the correlation coefficient. Calculate the expected return of the portfolio (Portfolio!) consisting 40% of stock A and 60% of stock B. Calculate the variance and standard...

Home assignment 4 Consider following information Probability of the state of economy Rate of return if state occurs StockA StockB boom normal a. b. c. 0.2 0.8 0.4 0.2 0.05 Calculate the expected return of Calculate the variance and standard deviation of each stock. Calculate the covariance between stock A and B returns and the correlation coefficient. Calculate the expected return of the portfolio (Portfolio!) consisting 40% of stock A and 60% of stock B. Calculate the variance and standard...

Ravi, a fund manager working for a private equity firm, is

considering including the following stocks in the firm’s

portfolio:

He plans to invest 40% of the portfolio funds in stock RST and

the balance equally between VVR and BAB. Beta of stock VVR is 0.15

higher than RST.

The firm’s in-house economist anticipates the probability of

boom, normal and recession to be 25%, 40% and 35% respectively. The

yield on long term government securities is 3% per year.

(a)...

Ravi, a fund manager working for a private equity firm, is

considering including the following stocks in the firm’s

portfolio:

He plans to invest 40% of the portfolio funds in stock RST and

the balance equally between VVR and BAB. Beta of stock VVR is 0.15

higher than RST.

The firm’s in-house economist anticipates the probability of

boom, normal and recession to be 25%, 40% and 35% respectively. The

yield on long term government securities is 3% per year.

(a)...

2. Company A's stock has a beta of BA 1.5, and Company B's stock has a beta of βΒ-2.5. Expected returns on this two stocks are E [rA]-9.5 and E rB 14.5. Assume CAPM holds. At age 30, you decide to allocate ALL your financial wealth of $100k between stock A and stock B, with portfolio weights wA + wB1. You would like this portfolio to be risky such that Bp- 3 (a) Solve for wA and wB- (b) State...

2. Company A's stock has a beta of BA 1.5, and Company B's stock has a beta of βΒ-2.5. Expected returns on this two stocks are E [rA]-9.5 and E rB 14.5. Assume CAPM holds. At age 30, you decide to allocate ALL your financial wealth of $100k between stock A and stock B, with portfolio weights wA + wB1. You would like this portfolio to be risky such that Bp- 3 (a) Solve for wA and wB- (b) State...

Most questions answered within 3 hours.

-

#10

Calculate the solubility ( in moles per liter) of Al(OH)3 (

Ksp=2*10^-32) in each of...

asked 1 minute ago -

Micro bio

For the tetanus vaccine, what is the antigen?

we have learned the tetanus part...

asked 3 minutes ago -

What is the scope of work for replacing a toilet with a

urinal

asked 5 minutes ago -

A random sample of 40 videos posted to youtube was selected. A

month later, the number...

asked 6 minutes ago -

Find the optimum strategies for player A and player B in the

game represented by the...

asked 17 minutes ago -

*SHOW YOUR WORK*

(Boyle's Law):

1. What is the final volume (in mL) or argon gas...

asked 17 minutes ago -

What is the purpose of adding a fluorescent dye to a cleaning

product?

asked 22 minutes ago -

The number of tornadoes in an unspecified year follows a Poisson

distribution with mean 3. Calculate...

asked 23 minutes ago -

If a benzene ring has one methyl group as a substituent, will

the next substituent add...

asked 27 minutes ago -

A current of 5.91 A is passed through a Fe(NO3)2 solution for

1.80 h. How much...

asked 41 minutes ago -

A transmission line carries an 800-A current from east to west.

The earth's magnetic field is...

asked 42 minutes ago -

How do Public sectors innovate?

By concentrating on their history and examining the ways these

sectors...

asked 44 minutes ago