A U.S. firm imports €10 million of goods from a German firm, and needs to pay...

Homework Answers

Add Answer to:

A U.S. firm imports €10 million of goods from a German firm,

and needs to pay...

A U.S. firm imports €10 million of goods from a German firm, and needs to pay...

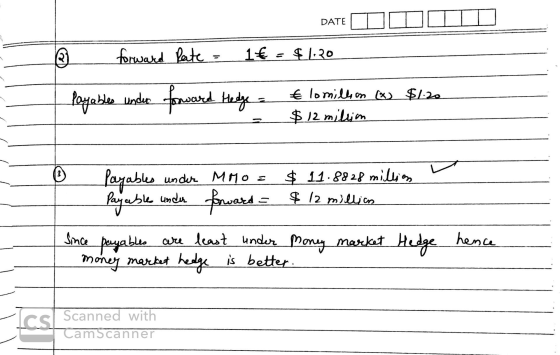

A U.S. firm imports €10 million of goods from a German firm, and needs to pay the full amount to the firm in 6 months. This U.S firm is engaging in the money market hedge in order to eliminate the transaction exposure. The following rates are available to the US firm: 6 month US interest rates = 3%, 6 month German interest rates = 5%, and the spot exchange rate (S$/€) = $1.20/€. a. Describe the money market hedging strategy...

A U.S. firm imports €10 million of goods from a German firm, and needs to pay...

A U.S. firm imports €10 million of goods from a German firm, and needs to pay the full amount to the firm in 6 months. This U.S firm is engaging in the money market hedge in order to eliminate the transaction exposure. The following rates are available to the US firm: 6 month US interest rates = 3%, 6 month German interest rates = 5%, and the spot exchange rate (S$/€) = $1.20/€. a. Describe the money market hedging strategy...

A U.S. firm imports €10 million of goods from a German firm, and needs to pay...

A U.S. firm imports €10 million of goods from a German firm, and needs to pay the full amount to the firm in 6 months. This U.S firm is engaging in the money market hedge in order to eliminate the transaction exposure. The following rates are available to the US firm: 6 month US interest rates = 3%, 6 month German interest rates = 5%, and the spot exchange rate (S$/€) = $1.20/€. a. Describe the money market hedging strategy...

) A U.S. firm imports €10 million of goods from a German firm, and needs to...

) A U.S. firm imports €10 million of goods from a German firm, and needs to pay the full amount to the firm in 6 months. This U.S firm is engaging in the money market hedge in order to eliminate the transaction exposure. The following rates are available to the US firm: 6 month US interest rates = 3%, 6 month German interest rates = 5%, and the spot exchange rate (S$/€) = $1.20/€. a. Describe the money market hedging...

A U.S. firm imports €10 million of goods from a German firm, and needs to pay...

A U.S. firm imports €10 million of goods from a German firm, and needs to pay the full amount to the firm in 6 months. This U.S firm is engaging in the money market hedge in order to eliminate the transaction exposure. The following rates are available to the US firm: 6 month US interest rates = 3%, 6 month German interest rates = 5%, and the spot exchange rate (S$/€) = $1.20/€. a. Describe the money market hedging strategy...

A U.S. firm imports €10 million of goods from a German firm, and needs to pay...

A U.S. firm imports €10 million of goods from a German firm, and needs to pay the full amount to the firm in 6 months. This U.S firm is engaging in the money market hedge in order to eliminate the transaction exposure. The following rates are available to the US firm: 6 month US interest rates = 3%, 6 month German interest rates = 5%, and the spot exchange rate (S$/€) = $1.20/€. a. Describe the money market hedging strategy...

A US firm imports £625,000 of goods from a UK firm, and need to pay in...

A US firm imports £625,000 of goods from a UK firm, and need to pay in six months. The US firm is considering to take the option hedging strategy. Assuming that a 6-month call option on pound is available at the exercise price of $1.20/£ and the call premium of $0.15/£. Answer the Following Questions: Show the formula that provides the value (per unit of pound) of this long call option hedge. Draw a figure that represents (per unit of...

1. Plains States Manufacturing has just signed a contract to sell agricultural equipment to Boschin, a...

1. Plains States Manufacturing has just signed a contract to sell agricultural equipment to Boschin, a German firm, for €1,250,000. The sale was made in June with payment due six months later in December. Because this is a sizable contract for the firm and because the contract is in Euros rather than dollars, Plains States is considering several hedging alternatives to reduce the exchange rate risk arising from the sale. To help the firm make a hedging decision you have...

Hedging Examples (pages 10-12) o buy) A US company will pay £10 million for imports from...

Hedging Examples (pages 10-12) o buy) A US company will pay £10 million for imports from Britain in 3 months and decides to hedge using a long position in a forward contract An investor owns 1,000 Microsoft shares currently worth $28 per share. A two-month put with a strike price of $27.50 costs $1. The investor decides to hedge by buying 10 contracts

Hedging Examples (pages 10-12) o buy) A US company will pay £10 million for imports from Britain in 3 months and decides to hedge using a long position in a forward contract An investor owns 1,000 Microsoft shares currently worth $28 per share. A two-month put with a strike price of $27.50 costs $1. The investor decides to hedge by buying 10 contracts

A U.S.-based importer, Zarb Inc., makes a purchase of crystal glassware from a firm in Switzerland...

A U.S.-based importer, Zarb Inc., makes a purchase of crystal glassware from a firm in Switzerland for 39,960 Swiss francs, or $24,000, at the spot rate of 1.665 francs per dollar. The terms of the purchase are net 90 days, and the U.S. firm wants to cover this trade payable with a forward market hedge to eliminate its exchange rate risk. Suppose the firm completes a forward hedge at the 90-day forward rate of 1.682 francs. If the spot rate...

Hedging Examples (pages 10-12) o buy) A US company will pay £10 million for imports from Britain in 3 months and decides to hedge using a long position in a forward contract An investor owns 1,000 Microsoft shares currently worth $28 per share. A two-month put with a strike price of $27.50 costs $1. The investor decides to hedge by buying 10 contracts

Hedging Examples (pages 10-12) o buy) A US company will pay £10 million for imports from Britain in 3 months and decides to hedge using a long position in a forward contract An investor owns 1,000 Microsoft shares currently worth $28 per share. A two-month put with a strike price of $27.50 costs $1. The investor decides to hedge by buying 10 contracts

Most questions answered within 3 hours.

-

An explosion breaks a 20.0-kg object into three parts. The

object is initially moving at a...

asked 38 minutes ago -

Calculate the approximate number of residues of Rubisco, which

is involved in carbon fixation in plants,...

asked 1 hour ago -

Other decisions about scientific claims can have a much broader

impact.ENERGYarrow-10x10.png, environment, health, security - all...

asked 2 hours ago -

I need to write a research paper and work cited about this

topic: The United States...

asked 2 hours ago -

Hello! I was wondering if I could have some help?

If the vapor pressure of carvone...

asked 3 hours ago -

An economist wants to estimate the mean per capita income (in

thousands of dollars) for a...

asked 3 hours ago -

What would be the input/output characteristic of a circuit

obtained by putting two of your 2's-complementers...

asked 3 hours ago -

In Drosophila, the transition from the syncytial blastoderm

stage to the cellular blastoderm stage is a...

asked 4 hours ago -

Project management question:

Name 3 different types of resources (hint: humans are one

type)

asked 4 hours ago -

Consider the following reaction: C 2H 2( g) + 2H 2( g) C 2H 6(

g)...

asked 4 hours ago -

Consider a 1.0 L buffer containing 0.092 mol L-1 HCOOH and 0.100

mol L-1 HCOO-. What...

asked 4 hours ago -

Koch Realty has owned a vacant land with a FMV of

$775,000 and an adjusted basis...

asked 4 hours ago