Homework Answers

Add Answer to:

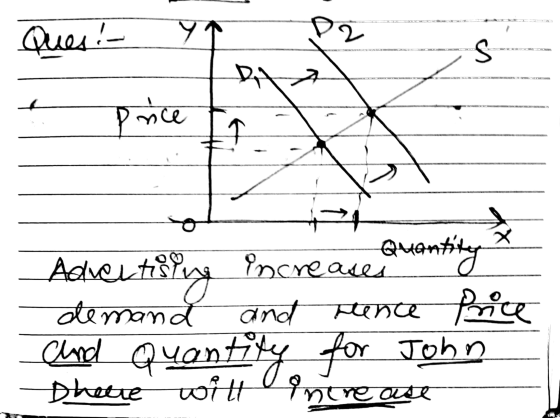

When both John Deere and Kubota increase their advertising simultaneously, we expect the equilibrium price for...

1- If the price of a good is below the equilibrium price, this will: a- Shift...

1- If the price of a good is below the equilibrium price, this will: a- Shift the demand curve down. b- Create a surplus. c- Create a shortage. d- Have no effect. How would an outward shift in demand affect the market equilibrium? Group of answer choices a- Equilibrium price and quantity would decrease. b- Equilibrium price and quantity would increase c- Equilibrium price would decrease; equilibrium quantity would increase. d- Equilibrium price would increase; equilibrium quantity would decrease. e-...

Question 5 1 pts If the demand for a product increases, then we would expect equilibrium...

Question 5 1 pts If the demand for a product increases, then we would expect equilibrium price 1. tincrease and equilibrium quantity to decrease. 2. to decrease and equilibrium quantity to increase. 3. and equilibrium quantity both to increase. 4. and equilibrium quantity both to decrease. to increase and equilibrium quantity to decrease. to decrease and equilibrium quantity to increase. and equilibrium quantity both to increase. o and equilibrium quantity both to decrease.

Question 5 1 pts If the demand for a product increases, then we would expect equilibrium price 1. tincrease and equilibrium quantity to decrease. 2. to decrease and equilibrium quantity to increase. 3. and equilibrium quantity both to increase. 4. and equilibrium quantity both to decrease. to increase and equilibrium quantity to decrease. to decrease and equilibrium quantity to increase. and equilibrium quantity both to increase. o and equilibrium quantity both to decrease.

3. Consider the market for oil. What do we expect to happen to the equilibrium price...

3. Consider the market for oil. What do we expect to happen to the equilibrium price and quantity in each of these situations? (a) New drilling technology makes oil extraction more economical at any given price (b) The economy improves more than expected and people drive more (c) Battery technology drives down the price of electric cars, while simultaneously major oil fields begin to decline in production (d) Engineers make gas using cars more efficient, while simultaneously the demand for...

QUESTION 35 We would expect the income elasticity of demand for steak to be positive, and...

QUESTION 35 We would expect the income elasticity of demand for steak to be positive, and that for hamburger to be negative. True False QUESTION 36 What will happen to the equilibrium quantity and price of salmon in a competitive market when there is an equal decrease in demand and supply? Equilibrium quantity and price will both decrease. Equilibrium quantity will decrease and equilibrium price will stay the same. Equilibrium quantity and price will both increase. Equilibrium quantity will stay...

QUESTION 35 We would expect the income elasticity of demand for steak to be positive, and that for hamburger to be negative. True False QUESTION 36 What will happen to the equilibrium quantity and price of salmon in a competitive market when there is an equal decrease in demand and supply? Equilibrium quantity and price will both decrease. Equilibrium quantity will decrease and equilibrium price will stay the same. Equilibrium quantity and price will both increase. Equilibrium quantity will stay...

would the answer be c? If the demand for a product decreases, then we would expect...

would the answer be c?

If the demand for a product decreases, then we would expect equilibrium price O a. to increase and equilibrium quantity to decrease. O b. and equilibrium quantity to both increase. C. and equilibrium quantity to both decrease. O d. to decrease and equilibrium quantity to increase.

would the answer be c?

If the demand for a product decreases, then we would expect equilibrium price O a. to increase and equilibrium quantity to decrease. O b. and equilibrium quantity to both increase. C. and equilibrium quantity to both decrease. O d. to decrease and equilibrium quantity to increase.

Question When we put supply and demand together, we have: equilibrium a market a surplus a...

Question When we put supply and demand together, we have: equilibrium a market a surplus a shortage Question Recall the video "Supply and Demand Shifts: Coffee Negative Supply Shock." The ice-storm causes the ______ curve to shift to the left. Price _______ and so manufacturers spend _______ trying to get everything out of their fields. demand; increases; more time and labor supply; increases; less time and labor supply; decreases; less time and labor supply; increases; more time and labor Question...

1. John is studying the effects of income on the demand for peppers. Which factors are...

1. John is studying the effects of income on the demand for peppers. Which factors are held constant when using the "ceteris paribus" assumption? income all factors affecting demand, except income all factors affecting demand, including income none of the above Only price could change the ceteris paribus. Change of income can affect demand. Do we disregard this in ceteris paribus? 2. If supply and demand shift simultaneously, the equilibrium price __________________. must decrease if the equilibrium quantity increases and...

When demand decreases in a graph of demand and supply: O equilibrium price will decrease, but...

When demand decreases in a graph of demand and supply: O equilibrium price will decrease, but equilibrium quantity will increase. o both equilibrium price and quantity will decrease. O equilibrium price will increase, but equilibrium quantity will decrease. O both equilibrium price and quantity will increase. When supply decreases in a graph of demand and supply: O equilibrium price will decrease, but equilibrium quantity will increase. O both equilibrium price and quantity will decrease. o equilibrium price will increase, but...

When demand decreases in a graph of demand and supply: O equilibrium price will decrease, but equilibrium quantity will increase. o both equilibrium price and quantity will decrease. O equilibrium price will increase, but equilibrium quantity will decrease. O both equilibrium price and quantity will increase. When supply decreases in a graph of demand and supply: O equilibrium price will decrease, but equilibrium quantity will increase. O both equilibrium price and quantity will decrease. o equilibrium price will increase, but...

23 minutes Save Progress Last Saved: 4.50 PM decrease Equilibrium price will decrease but equilibrium quantity...

23 minutes Save Progress Last Saved: 4.50 PM decrease Equilibrium price will decrease but equilibrium quantity will increase. O Equilibfium price and quantity will both decrease. Equilibriym price and quantity will both increase. 48) Ceteris paribuy equilibrium price and quantity would both increase at the same time as a (2 result of an increase in demand. a decrease in supply an jcrease in supply D decrease in demand. one of the other answers 1s orrect If supply and demand BOTH...

23 minutes Save Progress Last Saved: 4.50 PM decrease Equilibrium price will decrease but equilibrium quantity will increase. O Equilibfium price and quantity will both decrease. Equilibriym price and quantity will both increase. 48) Ceteris paribuy equilibrium price and quantity would both increase at the same time as a (2 result of an increase in demand. a decrease in supply an jcrease in supply D decrease in demand. one of the other answers 1s orrect If supply and demand BOTH...

Assume the following occurs in a market: consumers expect a lower price; there is an increase...

Assume the following occurs in a market: consumers expect a lower price; there is an increase in the price of a complement; there is an increase in the number of firms; and there is decrease in government regulation. Which of the following correctly summarizes the outcome? A. None of the choices shown is correct. B. No predictions can be made with the information. C. The equilibrium quantity will increase, but any change in the equilibrium price is uncertain. D. The...

Question 5 1 pts If the demand for a product increases, then we would expect equilibrium price 1. tincrease and equilibrium quantity to decrease. 2. to decrease and equilibrium quantity to increase. 3. and equilibrium quantity both to increase. 4. and equilibrium quantity both to decrease. to increase and equilibrium quantity to decrease. to decrease and equilibrium quantity to increase. and equilibrium quantity both to increase. o and equilibrium quantity both to decrease.

Question 5 1 pts If the demand for a product increases, then we would expect equilibrium price 1. tincrease and equilibrium quantity to decrease. 2. to decrease and equilibrium quantity to increase. 3. and equilibrium quantity both to increase. 4. and equilibrium quantity both to decrease. to increase and equilibrium quantity to decrease. to decrease and equilibrium quantity to increase. and equilibrium quantity both to increase. o and equilibrium quantity both to decrease.

QUESTION 35 We would expect the income elasticity of demand for steak to be positive, and that for hamburger to be negative. True False QUESTION 36 What will happen to the equilibrium quantity and price of salmon in a competitive market when there is an equal decrease in demand and supply? Equilibrium quantity and price will both decrease. Equilibrium quantity will decrease and equilibrium price will stay the same. Equilibrium quantity and price will both increase. Equilibrium quantity will stay...

QUESTION 35 We would expect the income elasticity of demand for steak to be positive, and that for hamburger to be negative. True False QUESTION 36 What will happen to the equilibrium quantity and price of salmon in a competitive market when there is an equal decrease in demand and supply? Equilibrium quantity and price will both decrease. Equilibrium quantity will decrease and equilibrium price will stay the same. Equilibrium quantity and price will both increase. Equilibrium quantity will stay...

would the answer be c?

If the demand for a product decreases, then we would expect equilibrium price O a. to increase and equilibrium quantity to decrease. O b. and equilibrium quantity to both increase. C. and equilibrium quantity to both decrease. O d. to decrease and equilibrium quantity to increase.

would the answer be c?

If the demand for a product decreases, then we would expect equilibrium price O a. to increase and equilibrium quantity to decrease. O b. and equilibrium quantity to both increase. C. and equilibrium quantity to both decrease. O d. to decrease and equilibrium quantity to increase.

When demand decreases in a graph of demand and supply: O equilibrium price will decrease, but equilibrium quantity will increase. o both equilibrium price and quantity will decrease. O equilibrium price will increase, but equilibrium quantity will decrease. O both equilibrium price and quantity will increase. When supply decreases in a graph of demand and supply: O equilibrium price will decrease, but equilibrium quantity will increase. O both equilibrium price and quantity will decrease. o equilibrium price will increase, but...

When demand decreases in a graph of demand and supply: O equilibrium price will decrease, but equilibrium quantity will increase. o both equilibrium price and quantity will decrease. O equilibrium price will increase, but equilibrium quantity will decrease. O both equilibrium price and quantity will increase. When supply decreases in a graph of demand and supply: O equilibrium price will decrease, but equilibrium quantity will increase. O both equilibrium price and quantity will decrease. o equilibrium price will increase, but...

23 minutes Save Progress Last Saved: 4.50 PM decrease Equilibrium price will decrease but equilibrium quantity will increase. O Equilibfium price and quantity will both decrease. Equilibriym price and quantity will both increase. 48) Ceteris paribuy equilibrium price and quantity would both increase at the same time as a (2 result of an increase in demand. a decrease in supply an jcrease in supply D decrease in demand. one of the other answers 1s orrect If supply and demand BOTH...

23 minutes Save Progress Last Saved: 4.50 PM decrease Equilibrium price will decrease but equilibrium quantity will increase. O Equilibfium price and quantity will both decrease. Equilibriym price and quantity will both increase. 48) Ceteris paribuy equilibrium price and quantity would both increase at the same time as a (2 result of an increase in demand. a decrease in supply an jcrease in supply D decrease in demand. one of the other answers 1s orrect If supply and demand BOTH...

Most questions answered within 3 hours.

-

Trace the following recursive methods:

a) isPal with the string “abccda”

b) isAnBn with the string...

asked 7 minutes ago -

1. Which of the following is false about photosynthesis?

A. ATP is the molecule used to...

asked 54 minutes ago -

A simple random sample of size n=64 is obtained from a

population with a mean of...

asked 1 hour ago -

(2 dimensions, 1 object, 2 accelerations)

1) A projectile is thrown with a wind. The wind...

asked 2 hours ago -

Brian makes $34,100 per year. How much can Brian expect to

contribute to FICA taxes in...

asked 3 hours ago -

To buy a new house you must borrow $155,000. To do this you take

out a...

asked 3 hours ago -

Spacely Sprockets is evaluating the construction of a new plant

on land the company purchased for...

asked 4 hours ago -

1. Consider a linear regression model of y on K regressors and

an intercept.

(i) Describe...

asked 4 hours ago -

Enter a balanced equation for the reaction between hydrochloric

acid and sodium sulfite.

Express your answer...

asked 4 hours ago -

Give a regular expression describing the language

{x | x ∈ Σ* and x does not...

asked 4 hours ago -

Masses of 1.0 kg, 2.0 kg, and 3.0 kg are each separately subject

to a net...

asked 4 hours ago -

The mode of philosophical argumentation and thought. How do

philosophers think and write? What is important...

asked 4 hours ago