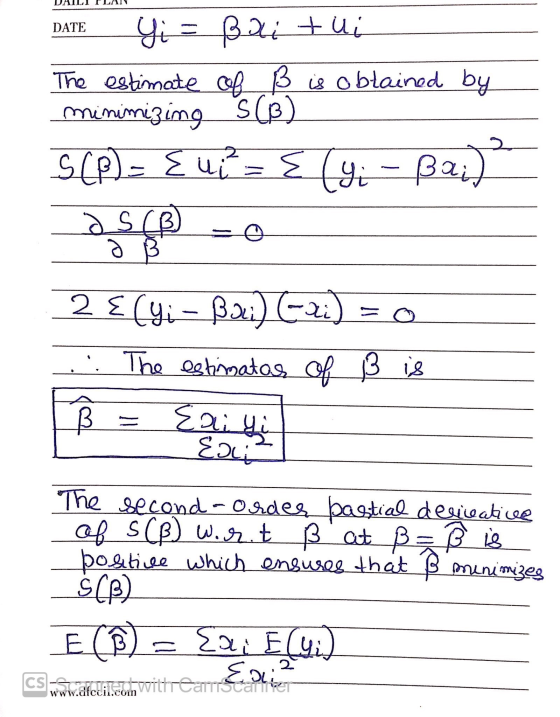

![Question 1 Consider the following model Yi = Bx; +ui (a) Derive the OLS estimator of B, ß. (6 marks] (b) Show that B is unbia](http://img.homeworklib.com/questions/dd14fcd0-08cf-11eb-a977-cb695d045e55.png?x-oss-process=image/resize,w_560)

Homework Answers

Add Answer to:

Question 1 Consider the following model Yi = Bx; +ui (a) Derive the OLS estimator of...

Question 1 Consider the following model Yi = B.z; + u (a) Derive the OLS estimator...

Question 1 Consider the following model Yi = B.z; + u (a) Derive the OLS estimator of B, B. (6 marks] (b) Show that is unbiased. [9 marks] (c) Find the variance of B. [7 marks]

Question 1 Consider the following model Yi = B.z; + u (a) Derive the OLS estimator of B, B. (6 marks] (b) Show that is unbiased. [9 marks] (c) Find the variance of B. [7 marks]

Derive the OLS estimator β₀ in the regression model yi=β₀+ui.

Derive the OLS estimator \hat{β}₀ in the regression model yi=β₀+ui. Show all of the steps in your derivation.

Consider a simple linear regression model with nonstochastic regressor: Yi = β1 + β2Xi + ui....

Consider a simple linear regression model with nonstochastic regressor: Yi = β1 + β2Xi + ui. 1. [3 points] What are the assumptions of this model so that the OLS estimators are BLUE (best linear unbiased estimates)? 2. [4 points] Let βˆ and βˆ be the OLS estimators of β and β . Derive βˆ and βˆ. 12 1212 3. [2 points] Show that βˆ is an unbiased estimator of β .22

Consider the linear model: Yi = α0 + α1(Xi − X̄) + ui. Find the OLS...

Consider the linear model: Yi = α0 + α1(Xi − X̄) + ui.

Find the OLS estimators of α0 and α1. Compare with the OLS

estimators of β0 and β1 in the standard model discussed in class

(Yi = β0 + β1Xi + ui).

Consider the linear model: Yį = ao + Q1(X; - X) + Ui. Find the OLS estimators of do and a1. Compare with the OLS estimators of Bo and B1 in the standard model discussed in...

Consider the linear model: Yi = α0 + α1(Xi − X̄) + ui.

Find the OLS estimators of α0 and α1. Compare with the OLS

estimators of β0 and β1 in the standard model discussed in class

(Yi = β0 + β1Xi + ui).

Consider the linear model: Yį = ao + Q1(X; - X) + Ui. Find the OLS estimators of do and a1. Compare with the OLS estimators of Bo and B1 in the standard model discussed in...

4. Consider the model yi-β +82i + ei. Find the OLS estimator for β.

4. Consider the model yi-β +82i + ei. Find the OLS estimator for β.

4. Consider the model yi-β +82i + ei. Find the OLS estimator for β.

Prove that the OLS estimator As for β in the linear regression model is consistent Let's first sh...

Taking the yellow parts below as a model to solve the

question above. Thank you!!!!!!!!

Prove that the OLS estimator As for β in the linear regression model is consistent Let's first show that the OLS estimator is consistent Recall the result for β LS-(Lil Xix;厂E-1 xīYi Using Yi = X(B* + ui By the WLLN Assuming that E(X,X is non-negative definite (so that its inverse exists) and using Slutsky's theorem It follows In words: ßOLs converges in probability to...

Taking the yellow parts below as a model to solve the

question above. Thank you!!!!!!!!

Prove that the OLS estimator As for β in the linear regression model is consistent Let's first show that the OLS estimator is consistent Recall the result for β LS-(Lil Xix;厂E-1 xīYi Using Yi = X(B* + ui By the WLLN Assuming that E(X,X is non-negative definite (so that its inverse exists) and using Slutsky's theorem It follows In words: ßOLs converges in probability to...

Consider the following slope estimator: b=2i=1 Yi Suppose the true model is ki + Bo +...

Consider the following slope estimator: b=2i=1 Yi Suppose the true model is ki + Bo + Bicite and the model satisfies the Gauss-Markov conditions. Answer the following questions: (a) What assumption in addition to the Gauss-Markov assumptions is required to estimate the model? (b) Show that in general, b is a biased estimator of B1. (c) Outline the special condition(s) under which b is an unbiased estimator of B1.

Consider the following slope estimator: b=2i=1 Yi Suppose the true model is ki + Bo + Bicite and the model satisfies the Gauss-Markov conditions. Answer the following questions: (a) What assumption in addition to the Gauss-Markov assumptions is required to estimate the model? (b) Show that in general, b is a biased estimator of B1. (c) Outline the special condition(s) under which b is an unbiased estimator of B1.

Problem 3: Absence of Intercept Consider the regression model Y, = BX,+", where , and X,...

Problem 3: Absence of Intercept Consider the regression model Y, = BX,+", where , and X, satisfy Assumptions SLR1-SLR5. Y (i) Let B denote an estimator of B that is constructed as P where Y and X as are the sample means of Y,and X,, respectively. Show that B is conditionally unbiased. Derive the least squares estimator of B. Show that the estimator is conditionally unbiased. Derive the conditional variance of the estimator. (ii) (iii) (iv) 2

Problem 3: Absence of Intercept Consider the regression model Y, = BX,+", where , and X, satisfy Assumptions SLR1-SLR5. Y (i) Let B denote an estimator of B that is constructed as P where Y and X as are the sample means of Y,and X,, respectively. Show that B is conditionally unbiased. Derive the least squares estimator of B. Show that the estimator is conditionally unbiased. Derive the conditional variance of the estimator. (ii) (iii) (iv) 2

1. Consider a regression model Yi = x;ß +ei, i = 1,...,n. You estimate this model...

1. Consider a regression model Yi = x;ß +ei, i = 1,...,n. You estimate this model using the OLS estimator. (a) Present and discuss assumptions for the OLS estimation.

1. Consider a regression model Yi = x;ß +ei, i = 1,...,n. You estimate this model using the OLS estimator. (a) Present and discuss assumptions for the OLS estimation.

Problem 2. (Regression without intercept, 50 pts) Suppose you are given the model: Y; = BX;...

Problem 2. (Regression without intercept, 50 pts) Suppose you are given the model: Y; = BX; + Ui, E[u;|Xį] = 0. A) Derive the OLS estimator ß. B) After you estimate B, you can obtain the residual û; = Y; – ĢXį. Does 21-1 Ûi = 0? Explain why and show your derivation.

Problem 2. (Regression without intercept, 50 pts) Suppose you are given the model: Y; = BX; + Ui, E[u;|Xį] = 0. A) Derive the OLS estimator ß. B) After you estimate B, you can obtain the residual û; = Y; – ĢXį. Does 21-1 Ûi = 0? Explain why and show your derivation.

Question 1 Consider the following model Yi = B.z; + u (a) Derive the OLS estimator of B, B. (6 marks] (b) Show that is unbiased. [9 marks] (c) Find the variance of B. [7 marks]

Question 1 Consider the following model Yi = B.z; + u (a) Derive the OLS estimator of B, B. (6 marks] (b) Show that is unbiased. [9 marks] (c) Find the variance of B. [7 marks]

Consider the linear model: Yi = α0 + α1(Xi − X̄) + ui.

Find the OLS estimators of α0 and α1. Compare with the OLS

estimators of β0 and β1 in the standard model discussed in class

(Yi = β0 + β1Xi + ui).

Consider the linear model: Yį = ao + Q1(X; - X) + Ui. Find the OLS estimators of do and a1. Compare with the OLS estimators of Bo and B1 in the standard model discussed in...

Consider the linear model: Yi = α0 + α1(Xi − X̄) + ui.

Find the OLS estimators of α0 and α1. Compare with the OLS

estimators of β0 and β1 in the standard model discussed in class

(Yi = β0 + β1Xi + ui).

Consider the linear model: Yį = ao + Q1(X; - X) + Ui. Find the OLS estimators of do and a1. Compare with the OLS estimators of Bo and B1 in the standard model discussed in...

4. Consider the model yi-β +82i + ei. Find the OLS estimator for β.

4. Consider the model yi-β +82i + ei. Find the OLS estimator for β.

Taking the yellow parts below as a model to solve the

question above. Thank you!!!!!!!!

Prove that the OLS estimator As for β in the linear regression model is consistent Let's first show that the OLS estimator is consistent Recall the result for β LS-(Lil Xix;厂E-1 xīYi Using Yi = X(B* + ui By the WLLN Assuming that E(X,X is non-negative definite (so that its inverse exists) and using Slutsky's theorem It follows In words: ßOLs converges in probability to...

Taking the yellow parts below as a model to solve the

question above. Thank you!!!!!!!!

Prove that the OLS estimator As for β in the linear regression model is consistent Let's first show that the OLS estimator is consistent Recall the result for β LS-(Lil Xix;厂E-1 xīYi Using Yi = X(B* + ui By the WLLN Assuming that E(X,X is non-negative definite (so that its inverse exists) and using Slutsky's theorem It follows In words: ßOLs converges in probability to...

Consider the following slope estimator: b=2i=1 Yi Suppose the true model is ki + Bo + Bicite and the model satisfies the Gauss-Markov conditions. Answer the following questions: (a) What assumption in addition to the Gauss-Markov assumptions is required to estimate the model? (b) Show that in general, b is a biased estimator of B1. (c) Outline the special condition(s) under which b is an unbiased estimator of B1.

Consider the following slope estimator: b=2i=1 Yi Suppose the true model is ki + Bo + Bicite and the model satisfies the Gauss-Markov conditions. Answer the following questions: (a) What assumption in addition to the Gauss-Markov assumptions is required to estimate the model? (b) Show that in general, b is a biased estimator of B1. (c) Outline the special condition(s) under which b is an unbiased estimator of B1.

Problem 3: Absence of Intercept Consider the regression model Y, = BX,+", where , and X, satisfy Assumptions SLR1-SLR5. Y (i) Let B denote an estimator of B that is constructed as P where Y and X as are the sample means of Y,and X,, respectively. Show that B is conditionally unbiased. Derive the least squares estimator of B. Show that the estimator is conditionally unbiased. Derive the conditional variance of the estimator. (ii) (iii) (iv) 2

Problem 3: Absence of Intercept Consider the regression model Y, = BX,+", where , and X, satisfy Assumptions SLR1-SLR5. Y (i) Let B denote an estimator of B that is constructed as P where Y and X as are the sample means of Y,and X,, respectively. Show that B is conditionally unbiased. Derive the least squares estimator of B. Show that the estimator is conditionally unbiased. Derive the conditional variance of the estimator. (ii) (iii) (iv) 2

1. Consider a regression model Yi = x;ß +ei, i = 1,...,n. You estimate this model using the OLS estimator. (a) Present and discuss assumptions for the OLS estimation.

1. Consider a regression model Yi = x;ß +ei, i = 1,...,n. You estimate this model using the OLS estimator. (a) Present and discuss assumptions for the OLS estimation.

Problem 2. (Regression without intercept, 50 pts) Suppose you are given the model: Y; = BX; + Ui, E[u;|Xį] = 0. A) Derive the OLS estimator ß. B) After you estimate B, you can obtain the residual û; = Y; – ĢXį. Does 21-1 Ûi = 0? Explain why and show your derivation.

Problem 2. (Regression without intercept, 50 pts) Suppose you are given the model: Y; = BX; + Ui, E[u;|Xį] = 0. A) Derive the OLS estimator ß. B) After you estimate B, you can obtain the residual û; = Y; – ĢXį. Does 21-1 Ûi = 0? Explain why and show your derivation.

Most questions answered within 3 hours.

-

An economist wants to estimate the mean per capita income (in

thousands of dollars) for a...

asked 4 minutes ago -

What would be the input/output characteristic of a circuit

obtained by putting two of your 2's-complementers...

asked 3 minutes ago -

In Drosophila, the transition from the syncytial blastoderm

stage to the cellular blastoderm stage is a...

asked 31 minutes ago -

Project management question:

Name 3 different types of resources (hint: humans are one

type)

asked 44 minutes ago -

Consider the following reaction: C 2H 2( g) + 2H 2( g) C 2H 6(

g)...

asked 51 minutes ago -

Consider a 1.0 L buffer containing 0.092 mol L-1 HCOOH and 0.100

mol L-1 HCOO-. What...

asked 1 hour ago -

Koch Realty has owned a vacant land with a FMV of

$775,000 and an adjusted basis...

asked 1 hour ago -

It is estimated 29% of all adults in United States invest in

stocks and that 85%...

asked 1 hour ago -

What does a 2-sided p value of 0.04 mean? (I am not asking if it

is...

asked 1 hour ago -

A parallel-plate capacitor is made from two aluminum-foil

sheets, each 7.8 cmcm wide and 5.1 mmlong....

asked 1 hour ago -

1. why is toluene a stronger nucleophile than benzene?

2.why is phenol a stronger nucleophile than...

asked 1 hour ago -

4. How can you solve for the density of the liquid from the

slope? Please show...

asked 1 hour ago