EC, an engineering company, produces tools and components to customers' specific requirements. EC uses absorption costing...

EC, an engineering company, produces tools and components to customers' specific requirements. EC uses absorption costing to absorb overheads into the cost of each customer order. Selling prices are usually determined by adding a 30% mark up to the costs incurred in completing the order. EC has recently been asked to provide a quotation for a new customer. The details of the work have been discussed at a meeting with the customer and the following resource requirements have been determined. The cost of these resources has been calculated using the company’s routine costing system.

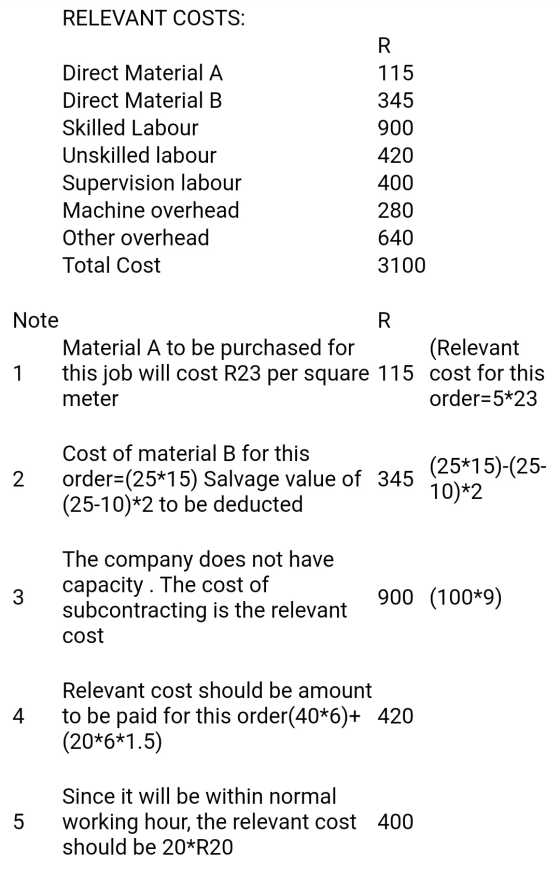

Direct material A 1 5 square metres @ R20 100 Direct material B 2 10 square metres @ R15 150 Skilled labour 3 100 hours @ R8 800 Unskilled labour 4 60 hours @ R6 360 Supervision labour 5 20 hours @ R20 400 Machine overhead 6 20 hours @ R12 240 Other overhead 7 160 labour hours @ R4 640 Total cost 2 690

Notes

Direct material A is currently held in inventory and is in regular use. The latest price paid for material A was R22 per square metre, but the replacement cost would be R23 per square metre. 2. Direct material B is currently not used by EC and would have to be bought if the work is undertaken. The minimum order from the supplier of material B is for 25 square metres. EC does not expect to be able to use this material on any other work, though it would be able to sell it as scrap for R2 per square metre.

3. The skilled labour that would be required is available within EC, but only if those employees are transferred from other work that they are currently doing. This other work could be done by sub-contractors who could be hired on an hourly basis at a cost of R7 per hour. Alternatively sub-contractors could be hired to work on this new customer’s order at a cost of R9 per hour. EC’s current skilled labour is paid R8 per hour. 4. The unskilled labour is paid an hourly rate of R6 but only for hours that they are actively working. There are only 40 hours of additional unskilled labour available within normal working hours. In order to complete the customer order on time they would have to work 20 hours of overtime. EC pays an overtime premium of 50%. 5. The work would be supervised by the existing supervisor as part of his normal activity. The supervisor is paid an annual salary which is equivalent to R20 per hour for a 40 hour working week. 6. The machines that would need to be used have a running cost of R12 per hour. Two different machines would be required: machine W for 12 hours and machine Z for 8 hours. Both machines are regularly used by EC. Machine W is very specialised and is used for only some of EC’s work. There is sufficient spare capacity on this machine. Machine Z is in constant use by EC and, if it is required for this customer order, EC would need to hire an additional machine at a hire cost of R5 per hour (excluding running costs) to fulfill its normal work. 7. EC’s non-machine related fixed overhead costs are absorbed into product costs using an absorption rate per labour hour.If this customer order is accepted it must be completed during the next 30 days. EC would like to win this order as it believes that it will probably win repeat orders from the customer. The directors have therefore decided to price this work on the basis of its relevant cost plus 10%

1.1 Prepare a schedule that shows the relevant cost of the new customer's order.

1.2 Explain, for each of the resource items numbered 1 to 7, the reason for each of the values you have included in your answer to 1.1 above.

Homework Answers

Please give positive rating your feedback is valuable to me.

In case , any problem please leave a comment.

Answer-

Add Answer to:

EC, an engineering company, produces tools and components to

customers' specific requirements. EC uses absorption costing...

QUESTION THREE [25] EC, an engineering company, produces tools and components to customers' specific requirements. EC...

QUESTION THREE [25] EC, an engineering company, produces tools and components to customers' specific requirements. EC uses absorption costing to absorb overheads into the cost of each customer order. Selling prices are usually determined by adding a 30% mark up to the costs incurred in completing the order. EC has recently been asked to provide a quotation for a new customer. The details of the work have been discussed at a meeting with the customer and the following resource requirements...

QUESTION ONE [20] EC, an engineering company, produces tools and components to customers' specific requirements. EC...

QUESTION ONE [20] EC, an engineering company, produces tools and components to customers' specific requirements. EC uses absorption costing to absorb overheads into the cost of each customer order. Selling prices are usually determined by adding a 30% mark up to the costs incurred in completing the order. EC has recently been asked to provide a quotation for a new customer. The details of the work have been discussed at a meeting with the customer and the following resource requirements...

9.2.2 ADVANCED MANAGERIAL ACCOUNTING [100] QUESTION ONE [20] EC, an engineering company, produces tools and components...

9.2.2 ADVANCED MANAGERIAL ACCOUNTING [100] QUESTION ONE [20] EC, an engineering company, produces tools and components to customers' specific requirements. EC uses absorption costing to absorb overheads into the cost of each customer order. Selling prices are usually determined by adding a 30% mark up to the costs incurred in completing the order. EC has recently been asked to provide a quotation for a new customer. The details of the work have been discussed at a meeting with the customer...

Laughing Strange Aussie Limited produces a single product -premium wool Ugg boots. Variable manufacturing overhead is...

Laughing Strange Aussie Limited produces a single product -premium wool Ugg boots. Variable manufacturing overhead is applied to products based on direct machine-hours. The standard costs for one unit of product are as follows: Direct Material: 16 metres at $3.25 per metre Direct Labour 6 hours at $19.00 per hour Variable Manufacturing Overhead: 4 machine-hours at $12.00 per hour Total Standard Variable Cost Per Unit $52.00 $114.00 $48.00 $214.00 During the month of May, 64,880 units were produced. The actual...

Laughing Strange Aussie Limited produces a single product -premium wool Ugg boots. Variable manufacturing overhead is applied to products based on direct machine-hours. The standard costs for one unit of product are as follows: Direct Material: 16 metres at $3.25 per metre Direct Labour 6 hours at $19.00 per hour Variable Manufacturing Overhead: 4 machine-hours at $12.00 per hour Total Standard Variable Cost Per Unit $52.00 $114.00 $48.00 $214.00 During the month of May, 64,880 units were produced. The actual...

Problem 7A-1 Activity-Based Costing Product Costs for External Reports [LO6] Data concerning Cranur Architects Corporation’s two...

Problem 7A-1 Activity-Based Costing Product Costs for External Reports [LO6] Data concerning Cranur Architects Corporation’s two major business lines are given below: Commercial Residential Direct materials per square metre $ 5.00 $ 3.50 Direct labour per square metre $ 47 $ 35.25 Direct labour-hours per square metre 0.1 DLHs 0.075 DLHs Estimated annual output 80,000 m2 560,000 m2 The company has a traditional costing system in which architecture department overhead is applied to units (square metres of architectural drawings) based...

Harrison Company makes two products and uses a conventional costing system in which a single plantwide,...

Harrison Company makes two products and uses a conventional costing system in which a single plantwide, predetermined overhead rate is computed based on direct labour-hours. Data for the two products for the upcoming year follow: Rascon 5 29.60 $ 14.70 70 29,000 Parcel $ 23.00 $ 4.20 Direct materials cost per unit Direct labour cost per unit Direct labour-hours per unit Number of units produced 40 120.000 These products are customized to some degree for specific customers. Required: 1. The...

Harrison Company makes two products and uses a conventional costing system in which a single plantwide, predetermined overhead rate is computed based on direct labour-hours. Data for the two products for the upcoming year follow: Rascon 5 29.60 $ 14.70 70 29,000 Parcel $ 23.00 $ 4.20 Direct materials cost per unit Direct labour cost per unit Direct labour-hours per unit Number of units produced 40 120.000 These products are customized to some degree for specific customers. Required: 1. The...

Harvey Ltd. Produces three products: Fridges, Dishwashers and Washing machines. The company uses a single plant-wide...

Harvey Ltd. Produces three products: Fridges, Dishwashers and Washing machines. The company uses a single plant-wide factory overhead rate to all three products based on direct labour hours. The company currently uses plant-wide factory overhead allocation based on direct labour hours. The company also adds a 20% mark-up on the cost of production to cover administration cost and gross margin. The selling price per unit for the three products are as follows: Fridge - $1043.85 Dishwasher ...

QUESTION 1 (12 marks; 22 minutes) Poullus Limited (PL). a high-tech electronics manufacturing company, is currently...

QUESTION 1 (12 marks; 22 minutes) Poullus Limited (PL). a high-tech electronics manufacturing company, is currently operating at 70% of its maximum capacity A new customer in lesotho has asked PL to provide a special order for 200 virtual reality headsets at R2.500 per unit. The potential customer is not a current customer of PL, but the directors of PL are keen to try and win the contract as they believe that this may lead to more contracts in the...

Vines Corporation produces custom machine parts on a job order basis. The company has two direct...

Vines Corporation produces custom machine parts on a job order

basis. The company has two direct product cost categories: direct

materials and direct labour. In the past, indirect

manufacturing costs were allocated to products using a single

indirect cost pool, allocated based on direct labour hours. The

indirect cost rate was $100 per direct labour hour.

The managers of Vines Corporation decided to switch from a

manual system to software programs that release materials and that

signal machines when to...

Vines Corporation produces custom machine parts on a job order

basis. The company has two direct product cost categories: direct

materials and direct labour. In the past, indirect

manufacturing costs were allocated to products using a single

indirect cost pool, allocated based on direct labour hours. The

indirect cost rate was $100 per direct labour hour.

The managers of Vines Corporation decided to switch from a

manual system to software programs that release materials and that

signal machines when to...

Nar Limited manufactures a range of cable products for the electronics industry. The company has been...

Nar Limited manufactures a range of cable products for the

electronics industry. The

company has been notified of an upcoming scarce availability

situation in relation to a raw

material called Rhond’, a metal used in the production of three of

the company’s cable

products. The maximum availability of this material will be

restricted to 15,000 metres in the

upcoming quarter.

You have been asked by the production manager to make appropriate

changes to the

production budget for these three cable...

Nar Limited manufactures a range of cable products for the

electronics industry. The

company has been notified of an upcoming scarce availability

situation in relation to a raw

material called Rhond’, a metal used in the production of three of

the company’s cable

products. The maximum availability of this material will be

restricted to 15,000 metres in the

upcoming quarter.

You have been asked by the production manager to make appropriate

changes to the

production budget for these three cable...

Laughing Strange Aussie Limited produces a single product -premium wool Ugg boots. Variable manufacturing overhead is applied to products based on direct machine-hours. The standard costs for one unit of product are as follows: Direct Material: 16 metres at $3.25 per metre Direct Labour 6 hours at $19.00 per hour Variable Manufacturing Overhead: 4 machine-hours at $12.00 per hour Total Standard Variable Cost Per Unit $52.00 $114.00 $48.00 $214.00 During the month of May, 64,880 units were produced. The actual...

Laughing Strange Aussie Limited produces a single product -premium wool Ugg boots. Variable manufacturing overhead is applied to products based on direct machine-hours. The standard costs for one unit of product are as follows: Direct Material: 16 metres at $3.25 per metre Direct Labour 6 hours at $19.00 per hour Variable Manufacturing Overhead: 4 machine-hours at $12.00 per hour Total Standard Variable Cost Per Unit $52.00 $114.00 $48.00 $214.00 During the month of May, 64,880 units were produced. The actual...

Harrison Company makes two products and uses a conventional costing system in which a single plantwide, predetermined overhead rate is computed based on direct labour-hours. Data for the two products for the upcoming year follow: Rascon 5 29.60 $ 14.70 70 29,000 Parcel $ 23.00 $ 4.20 Direct materials cost per unit Direct labour cost per unit Direct labour-hours per unit Number of units produced 40 120.000 These products are customized to some degree for specific customers. Required: 1. The...

Harrison Company makes two products and uses a conventional costing system in which a single plantwide, predetermined overhead rate is computed based on direct labour-hours. Data for the two products for the upcoming year follow: Rascon 5 29.60 $ 14.70 70 29,000 Parcel $ 23.00 $ 4.20 Direct materials cost per unit Direct labour cost per unit Direct labour-hours per unit Number of units produced 40 120.000 These products are customized to some degree for specific customers. Required: 1. The...

Vines Corporation produces custom machine parts on a job order

basis. The company has two direct product cost categories: direct

materials and direct labour. In the past, indirect

manufacturing costs were allocated to products using a single

indirect cost pool, allocated based on direct labour hours. The

indirect cost rate was $100 per direct labour hour.

The managers of Vines Corporation decided to switch from a

manual system to software programs that release materials and that

signal machines when to...

Vines Corporation produces custom machine parts on a job order

basis. The company has two direct product cost categories: direct

materials and direct labour. In the past, indirect

manufacturing costs were allocated to products using a single

indirect cost pool, allocated based on direct labour hours. The

indirect cost rate was $100 per direct labour hour.

The managers of Vines Corporation decided to switch from a

manual system to software programs that release materials and that

signal machines when to...

Nar Limited manufactures a range of cable products for the

electronics industry. The

company has been notified of an upcoming scarce availability

situation in relation to a raw

material called Rhond’, a metal used in the production of three of

the company’s cable

products. The maximum availability of this material will be

restricted to 15,000 metres in the

upcoming quarter.

You have been asked by the production manager to make appropriate

changes to the

production budget for these three cable...

Nar Limited manufactures a range of cable products for the

electronics industry. The

company has been notified of an upcoming scarce availability

situation in relation to a raw

material called Rhond’, a metal used in the production of three of

the company’s cable

products. The maximum availability of this material will be

restricted to 15,000 metres in the

upcoming quarter.

You have been asked by the production manager to make appropriate

changes to the

production budget for these three cable...

Most questions answered within 3 hours.

-

Kylie is a single mom with two dependent children,

Tanner, age 7 and Olivia, age 11....

asked 3 minutes ago -

Phosphorous + bromine = phosphorous tribromide. If 35.0 g of

bromine are reacted and 27.9 grams...

asked 1 hour ago -

Derive the long wavelength limit of the Planck energy density

distribution

asked 1 hour ago -

Calculate the pH of each of the following solutions.

0.50 M HBr

3.1×10−4 M KOH

4.2×10−5...

asked 4 hours ago -

For the year ended December 31, Depot Max’s cost of merchandise

sold was $85,600. Inventory at the...

asked 4 hours ago -

Week 10 - Professional Memo Assignment

Professional Memo Assignment

Your mission for this week, should you...

asked 5 hours ago -

Write a Python program that stores the data for each

player on the team, and it...

asked 5 hours ago -

In

the last 3 months, mike never knows when he is going to get his

allowance...

asked 5 hours ago -

Is Ca(OH)2 a Bronsted base, Lewis base, or both? Why?

asked 5 hours ago -

1A- Why don’t voters complain about U.S. tariffs on imported

sugar?

Because sugar is only a...

asked 5 hours ago -

Cash Payback Period

Primera Banco is evaluating two capital investment proposals for

a drive-up ATM kiosk,...

asked 5 hours ago -

Create a button in Swift (Xcode) that will create a charge,

create a charge using Stripe's...

asked 5 hours ago