You Just a TD stock at $100 and a put option on the TD stock at $5....

| You Just a TD stock at $100 and a put option on the TD stock at $5. The put has exercise price of $108 and expiration date is 6 months from now. Assume that the spot price of the TD stock on expiration date turned to as follows (consider each case separately): |

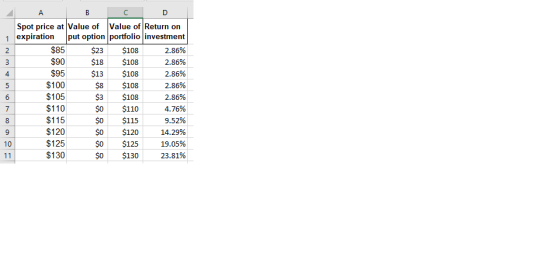

| Spot price at expiration |

| $85 |

| $90 |

| $95 |

| $100 |

| $105 |

| $110 |

| $115 |

| $120 |

| $125 |

| $130 |

| i. What will be value of put option expiration date under each scenario. |

| ii. What will be the value of your portfolio (a stock and a put option) at expiration under each case? |

| iii. What will be your return on investment (a stock and a put)? Compute holding period return for each case. |

| iv. Discuss how put option is helping you to reduce the downside risk of your investment. |

| Now assume that you rather short the TD stock today and buy a call option with a strike price of $105 |

| v. What will be value of call option expiration date under each scenario. |

| vi. Discuss how call option is helping to reduce the upside risk of your investment strategy. |

Homework Answers

(i)

Value of a long put option = Max[X-S, 0]

S = underlying price at expiry,

X = exercise price.

(ii)

Value of portfolio = Value of put option + value of stock

(iii)

Return on investment = (Value of portfolio at expiration - value of portfolio today) / value of portfolio today

value of portfolio today = purchase price of stock + purchase price of put option

value of portfolio today = $100 + $5 = $105

The formulas are below :

(iv)

The put option gains in value if the stock price at expiration is below the option exercise price. Thus, if the stock price falls, the gains on the put option offset the losses on the stock. In this way, the put option is helping you to reduce the downside risk of your investment.

Value of value of portfolio Return on investment Spot price at put expiration option $85 $15 $90 $10 $95 $100 $105 $110 $115 $120 $125 $130 $100 $100 $100 $100 $105 $110 $115 $120 $125 $130 -4.76% -4.76% -4.76% -4.76% 0.00% 4.76% 9.52% 14.29% 19.05% 23.81%

Value of put option Spot price at 1 expiration 2 85 3 90 4 95 5 100 6 105 7 110 8 115 9 120 10 125 11 130 =MAX(100-A2,0) =MAX(100-A3,0) =MAX(100-A4,0) =MAX(100-A5,0) =MAX(100-A6,0) =MAX(100-A7,0) =MAX(100-A8,0) =MAX(100-A9,0) =MAX(100-A10,0) =MAX(100-A11,0) Value of portfolio =A2+B2 =A3+B3 =A4+B4 =A5+B5 =A6+B6 =A7+B7 =A8+B8 =A9+B9 =A10+B10 =A11+B11 Return on investment =(C2-105)/105 =(C3-105)/105 =(C4-105)/105 = (C5-105)/105 = (C6-105)/105 =(C7-105)/105 = (C8-105)/105 =(C9-105)/105 =(C10-105)/105 =(C11-105)/105

Add Answer to:

You Just a TD stock at $100 and a put option on the

TD stock at $5....

9. Put-call parity and the value of a put option Aa Aa E Consider two portfolios...

9. Put-call parity and the value of a put option Aa Aa E Consider two portfolios A and B. At the expiration date, t, both portfolios have identical payoffs. Portfolio A consists of a put option and one share of stock. Portfolio B has a call option (with the same strike price and expiration date as the put option) and cash in the amount equal to the present value (PV) of the strike price discounted at the continuously compounded risk-free...

9. Put-call parity and the value of a put option Aa Aa E Consider two portfolios A and B. At the expiration date, t, both portfolios have identical payoffs. Portfolio A consists of a put option and one share of stock. Portfolio B has a call option (with the same strike price and expiration date as the put option) and cash in the amount equal to the present value (PV) of the strike price discounted at the continuously compounded risk-free...

You bought Stock A at a purchase price of: Put option strike price: $25 $15 Option...

You bought Stock A at a purchase price of: Put option strike price: $25 $15 Option expiration date: Price of put option: June 30, 2020 $5 Stock goes up to $50 Stock goes down to $5 Profit/Loss on stock if sell now Profit/Loss on call option if sell now

You bought Stock A at a purchase price of: Put option strike price: $25 $15 Option expiration date: Price of put option: June 30, 2020 $5 Stock goes up to $50 Stock goes down to $5 Profit/Loss on stock if sell now Profit/Loss on call option if sell now

13. The premium on a pound put option is $.03 per unit. The exercise price is...

13. The premium on a pound put option is $.03 per unit. The exercise price is s1.60. The break-even point for the buyer and seller is? (Assume put option are speculators.) zero transactions costs and that the buyer and seller of the 14. You purchase a call option on pounds for a premium of $.03 per unit, with an exercise price of $1.64; the option will not be exercised until the expiration date, if at all. If the spot rate...

13. The premium on a pound put option is $.03 per unit. The exercise price is s1.60. The break-even point for the buyer and seller is? (Assume put option are speculators.) zero transactions costs and that the buyer and seller of the 14. You purchase a call option on pounds for a premium of $.03 per unit, with an exercise price of $1.64; the option will not be exercised until the expiration date, if at all. If the spot rate...

A call option on XYZ stock has a delta of 0.4483, and a put option on...

A call option on XYZ stock has a delta of 0.4483, and a put option on XYZ stock with same strike and date to expiration has a delta of −0.5517. The stock is currently trading for $48.00. The gamma for both the call and put is 0.07. What is the price of the call option?

. Assume the following for a stock and a call and a put option written on...

. Assume the following for a stock and a call and a put option written on the stock. EXERCISE PRICE = $20 CURRENT STOCK PRICE = $22 VARIANCE = .25 Standard Deviation = .50 TIME TO EXPIRATION = 4 MONTHS T = .33 RISK FREE RATE = 3% Use the Black Scholes procedure to determine the value of the call option and the value of a put.

4. Assume the following for a stock and a call and a put option written on...

4. Assume the following for a stock and a call and a put option written on the stock. EXERCISE PRICE = $20 CURRENT STOCK PRICE = $22 VARIANCE = .25 TIME TO EXPIRATION = 4 MONTHS RISK FREE RATE = 3% B) Use the Black Scholes procedure to determine the value of the call option and the value of a put.

Buying a put option and selling a call option are both considered a way of expressing...

Buying a put option and selling a call option are both considered a way of expressing a bearish view on a stock (i.e., that its price will decline). Draw the hockey-sticks for both buying a put and selling a call in terms of the stock price at expiry S(T), the strike (X), and the premium (C/P). Be sure to label the graphs including breakeven points and upside/downside

Consider a stock with a price with S = 100 and pays no dividends. The annual...

Consider a stock with a price with S = 100 and pays no dividends. The annual risk-free is 10%. A European put option on the stock with a strike price 90 and an expiration date three months from now has a price of 10. What is the price of a European call option on this stock with the same strike price and expiration date?

A European call option and put option on a stock both have a strike price of...

A European call option and put option on a stock both have a strike price of $45 and an expiration date in six months. Both sell for $2. The risk-free interest rate is 5% p.a. The current stock price is $43. There is no dividend expected for the next six months. a) If the stock price in three months is $48, which option is in the money and which one is out of the money? b) As an arbitrageur, can...

Put-Call Parity The current price of a stock is $35, and the annual risk-free rate is...

Put-Call Parity The current price of a stock is $35, and the annual risk-free rate is 3%. A call option with a strike price of $31 and with 1 year until expiration has a current value of $6.60. What is the value of a put option written on the stock with the same exercise price and expiration date as the call option? Do not round intermediate calculations. Round your answer to the nearest cent. How do you calculate the negative...

9. Put-call parity and the value of a put option Aa Aa E Consider two portfolios A and B. At the expiration date, t, both portfolios have identical payoffs. Portfolio A consists of a put option and one share of stock. Portfolio B has a call option (with the same strike price and expiration date as the put option) and cash in the amount equal to the present value (PV) of the strike price discounted at the continuously compounded risk-free...

9. Put-call parity and the value of a put option Aa Aa E Consider two portfolios A and B. At the expiration date, t, both portfolios have identical payoffs. Portfolio A consists of a put option and one share of stock. Portfolio B has a call option (with the same strike price and expiration date as the put option) and cash in the amount equal to the present value (PV) of the strike price discounted at the continuously compounded risk-free...

You bought Stock A at a purchase price of: Put option strike price: $25 $15 Option expiration date: Price of put option: June 30, 2020 $5 Stock goes up to $50 Stock goes down to $5 Profit/Loss on stock if sell now Profit/Loss on call option if sell now

You bought Stock A at a purchase price of: Put option strike price: $25 $15 Option expiration date: Price of put option: June 30, 2020 $5 Stock goes up to $50 Stock goes down to $5 Profit/Loss on stock if sell now Profit/Loss on call option if sell now

13. The premium on a pound put option is $.03 per unit. The exercise price is s1.60. The break-even point for the buyer and seller is? (Assume put option are speculators.) zero transactions costs and that the buyer and seller of the 14. You purchase a call option on pounds for a premium of $.03 per unit, with an exercise price of $1.64; the option will not be exercised until the expiration date, if at all. If the spot rate...

13. The premium on a pound put option is $.03 per unit. The exercise price is s1.60. The break-even point for the buyer and seller is? (Assume put option are speculators.) zero transactions costs and that the buyer and seller of the 14. You purchase a call option on pounds for a premium of $.03 per unit, with an exercise price of $1.64; the option will not be exercised until the expiration date, if at all. If the spot rate...

Most questions answered within 3 hours.

-

(Expected rate of return and risk) Carter Inc. is evaluating a

security. Calculate the investment’s expected...

asked 30 minutes ago -

What specific indicators can point to lack of progress for

African Americans in American society?

asked 1 hour ago -

1-The Electrons in a beam are moving at 2.7×108 m/s in an

electric field of 15000...

asked 1 hour ago -

A gas tank is a vertical cylinder. It has a radius of 1m, a

height of...

asked 2 hours ago -

Accent Software faces the following conditions. All of these

support Accent’s use of a market-penetration pricing...

asked 3 hours ago -

A mathematically inclined friend emails you the following

instructions: "Meet me in the cafeteria the first...

asked 3 hours ago -

A monopoly sells in two countries . The demand curves in the two

countries are p1...

asked 4 hours ago -

A .15kg rubber ball is bounced off a wall. Before hitting the

wall, the ball moves...

asked 4 hours ago -

A manufacturing company preparing to build a new plant is

considering three potential locations for it....

asked 4 hours ago -

B. If compound Y has approximately the same values of solubility

in toluene as compound X,...

asked 5 hours ago -

Oscar Inc. has inventory in Japan valued at 39,051,000 Yen one

year ago. One year ago...

asked 5 hours ago -

If Canada suffered from "fundamental disequilibrium," and its

government choose not to devalue its currency, a...

asked 5 hours ago