Can you please show calculations.

Homework Answers

To calculate alpha, we have to perform regression of Portfolio return (dependent variable) with S&P returns (independent variable)

R-square = 0.95

Alpha = 0.11%

Beta = 0.92

| Average return difference (with signs) | 0.09% |

| Average return difference (without signs) | 0.51% |

Add Answer to:

Can you please show calculations.

Given the monthly returns that follow, find the R', alpha, and...

Problem 4-07 Given the monthly returns that follow, find the R2, alpha, and beta of the...

Problem 4-07 Given the monthly returns that follow, find the R2, alpha, and beta of the portfolio. Compute the average return differential with and without sign. Do not round intermediate calculations. Round your answers to two decimal places. Month Portfolio Return 5.3% -2.7 -1.6 S&P 500 Return 5.6% -3.2 -1.0 1.7 0.1 -0.6 0.9 January February March April May June July August September October November December 2.3 1.8 0.7 -1.2 0.5 1.5 -0.3 -3.2 2.8 0.3 -0.1 -3.7 2.0 0.0...

Problem 4-07 Given the monthly returns that follow, find the R2, alpha, and beta of the portfolio. Compute the average return differential with and without sign. Do not round intermediate calculations. Round your answers to two decimal places. Month Portfolio Return 5.3% -2.7 -1.6 S&P 500 Return 5.6% -3.2 -1.0 1.7 0.1 -0.6 0.9 January February March April May June July August September October November December 2.3 1.8 0.7 -1.2 0.5 1.5 -0.3 -3.2 2.8 0.3 -0.1 -3.7 2.0 0.0...

Problem 4-07 Given the monthly returns that follow, find the R2, alpha, and beta of the...

Problem 4-07 Given the monthly returns that follow, find the R2, alpha, and beta of the portfolio. Compute the average return differential with and without sign. Do not round intermediate calculations. Round your answers to two decimal places. Portfolio Return 5.8% S&P 500 Return 6.2% -2.3 -2.7 Month January February March April May -1.8 -0.9 2.6 2.0 0.4 -0.2 June -0.8 -0.3 0.4 0.7 1.4 1.1 -0.4 -0.1 July August September October November December -3.1 -3.4 1.7 2.6 0.6 0.3...

Problem 4-07 Given the monthly returns that follow, find the R2, alpha, and beta of the portfolio. Compute the average return differential with and without sign. Do not round intermediate calculations. Round your answers to two decimal places. Portfolio Return 5.8% S&P 500 Return 6.2% -2.3 -2.7 Month January February March April May -1.8 -0.9 2.6 2.0 0.4 -0.2 June -0.8 -0.3 0.4 0.7 1.4 1.1 -0.4 -0.1 July August September October November December -3.1 -3.4 1.7 2.6 0.6 0.3...

Given the monthly returns that follow, find the R2, alpha, and beta of the portfolio. Compute...

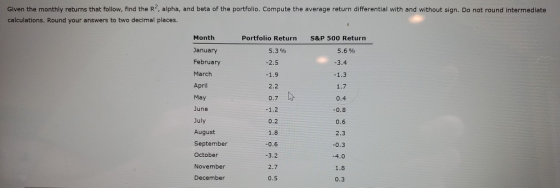

Given the monthly returns that follow, find the R2, alpha, and beta of the portfolio. Compute the average return differential with and without sign. Do not round intermediate calculations. Round your answers to two decimal places. MonthPortfolio ReturnS&P 500 Return January5.1%5.5% February-2.5-3.2 March-1.6-1.4 April2.72.3 May0.4-0.1 June-1.0-0.4 July0.00.5 August1.21.3 September-0.6-0.2 October-3.4-4.1 November2.21.4 December0.60.5 R2: Alpha: % Beta: Average return difference (with signs): % Average return difference (without signs) %

Coding in C++ Write a program using structures to store the following weather information: - Month...

Coding in C++ Write a program using structures to store the following weather information: - Month name - Day of month (Monday, Tuesday, etc) - High Temperature - Low Temperature - Rainfall for the day Use an the input.txt file to load the data into weather structures. Once the data for all the days is entered, the program should calculate and display the: - Total rainfall for the data - Average daily temperatures. (note: you'll need to calculate the days...

On Blackboard under "Course Content / Homeworks and Practice Tests" there is an Excel file titled...

On Blackboard under "Course Content / Homeworks and Practice Tests" there is an Excel file titled "HW 6 Data" with monthly stock return data to be used for this question: What is Deckers Outdoor Corporation's [DECK] beta? Round to two decimal places. [Hint: Take S&P 500 as a proxy for the market, and use the beta formula from the book. You will need to use two Excel functions: STDEV.S and CORREL] Numeric Answer S&PS00 DECK NKE SBUX -1.5% Ос-19 7.4%...

On Blackboard under "Course Content / Homeworks and Practice Tests" there is an Excel file titled "HW 6 Data" with monthly stock return data to be used for this question: What is Deckers Outdoor Corporation's [DECK] beta? Round to two decimal places. [Hint: Take S&P 500 as a proxy for the market, and use the beta formula from the book. You will need to use two Excel functions: STDEV.S and CORREL] Numeric Answer S&PS00 DECK NKE SBUX -1.5% Ос-19 7.4%...

Please show me how to use R to solve this problem. For data CIR, regress involact on race and int...

Please show me how to use R to solve this problem. For data CIR, regress involact on race and interpret the coefficient. Test the hypothesis to determine the claim that homeowners in zip codes with high percent minority are being denied insurance at higher rate than other zip codes. What can regression analysis tell you about the insurance companies claim that the discrepancy is due to greater risks in some zip codes?zip race fire theft age volact involact income 60626...

CASE 7.1 Tires for You, Inc Tires for You, Inc. (TFY), founded in 1987, is an automotive repair shop specializing in re...

CASE 7.1 Tires for You, Inc Tires for You, Inc. (TFY), founded in 1987, is an automotive repair shop specializing in replacement tires. Located in Altoona, Pennsylvania, TFY has grown successfully over the past few years because of the addition of a new general manager, Ian Overbaugh. Since tire replacement is a major portion of TFY's business (it also performs oil changes, small mechanical repairs, etc.), Ian was surprised at the lack of forecasts for tire consumption for the company....

CASE 7.1 Tires for You, Inc Tires for You, Inc. (TFY), founded in 1987, is an automotive repair shop specializing in replacement tires. Located in Altoona, Pennsylvania, TFY has grown successfully over the past few years because of the addition of a new general manager, Ian Overbaugh. Since tire replacement is a major portion of TFY's business (it also performs oil changes, small mechanical repairs, etc.), Ian was surprised at the lack of forecasts for tire consumption for the company....

QUESTION 10 Consider the monthly data, including the estimates for March 2020, and the information in...

QUESTION 10

Consider the monthly data, including the estimates for March

2020, and the information in the articles. Which of the following

is the best analysis of and prediction for the money market in the

U.S. economy for the next few months?

a.

Shortages are causing panic buying by households, which has

increased money demand. Lenders are increasing their lending to

keep up with the needs of households and businesses. Money demand

is increasing more than money supply.

b.

Shortages...

QUESTION 10

Consider the monthly data, including the estimates for March

2020, and the information in the articles. Which of the following

is the best analysis of and prediction for the money market in the

U.S. economy for the next few months?

a.

Shortages are causing panic buying by households, which has

increased money demand. Lenders are increasing their lending to

keep up with the needs of households and businesses. Money demand

is increasing more than money supply.

b.

Shortages...

CASE 1-5 Financial Statement Ratio Computation Refer to Campbell Soup Company's financial Campbell Soup statements in...

CASE 1-5 Financial Statement Ratio Computation Refer to Campbell Soup Company's financial Campbell Soup statements in Appendix A. Required: Compute the following ratios for Year 11. Liquidity ratios: Asset utilization ratios:* a. Current ratio n. Cash turnover b. Acid-test ratio 0. Accounts receivable turnover c. Days to sell inventory p. Inventory turnover d. Collection period 4. Working capital turnover Capital structure and solvency ratios: 1. Fixed assets turnover e. Total debt to total equity s. Total assets turnover f. Long-term...

CASE 1-5 Financial Statement Ratio Computation Refer to Campbell Soup Company's financial Campbell Soup statements in Appendix A. Required: Compute the following ratios for Year 11. Liquidity ratios: Asset utilization ratios:* a. Current ratio n. Cash turnover b. Acid-test ratio 0. Accounts receivable turnover c. Days to sell inventory p. Inventory turnover d. Collection period 4. Working capital turnover Capital structure and solvency ratios: 1. Fixed assets turnover e. Total debt to total equity s. Total assets turnover f. Long-term...

Problem 4-07 Given the monthly returns that follow, find the R2, alpha, and beta of the portfolio. Compute the average return differential with and without sign. Do not round intermediate calculations. Round your answers to two decimal places. Month Portfolio Return 5.3% -2.7 -1.6 S&P 500 Return 5.6% -3.2 -1.0 1.7 0.1 -0.6 0.9 January February March April May June July August September October November December 2.3 1.8 0.7 -1.2 0.5 1.5 -0.3 -3.2 2.8 0.3 -0.1 -3.7 2.0 0.0...

Problem 4-07 Given the monthly returns that follow, find the R2, alpha, and beta of the portfolio. Compute the average return differential with and without sign. Do not round intermediate calculations. Round your answers to two decimal places. Month Portfolio Return 5.3% -2.7 -1.6 S&P 500 Return 5.6% -3.2 -1.0 1.7 0.1 -0.6 0.9 January February March April May June July August September October November December 2.3 1.8 0.7 -1.2 0.5 1.5 -0.3 -3.2 2.8 0.3 -0.1 -3.7 2.0 0.0...

Problem 4-07 Given the monthly returns that follow, find the R2, alpha, and beta of the portfolio. Compute the average return differential with and without sign. Do not round intermediate calculations. Round your answers to two decimal places. Portfolio Return 5.8% S&P 500 Return 6.2% -2.3 -2.7 Month January February March April May -1.8 -0.9 2.6 2.0 0.4 -0.2 June -0.8 -0.3 0.4 0.7 1.4 1.1 -0.4 -0.1 July August September October November December -3.1 -3.4 1.7 2.6 0.6 0.3...

Problem 4-07 Given the monthly returns that follow, find the R2, alpha, and beta of the portfolio. Compute the average return differential with and without sign. Do not round intermediate calculations. Round your answers to two decimal places. Portfolio Return 5.8% S&P 500 Return 6.2% -2.3 -2.7 Month January February March April May -1.8 -0.9 2.6 2.0 0.4 -0.2 June -0.8 -0.3 0.4 0.7 1.4 1.1 -0.4 -0.1 July August September October November December -3.1 -3.4 1.7 2.6 0.6 0.3...

On Blackboard under "Course Content / Homeworks and Practice Tests" there is an Excel file titled "HW 6 Data" with monthly stock return data to be used for this question: What is Deckers Outdoor Corporation's [DECK] beta? Round to two decimal places. [Hint: Take S&P 500 as a proxy for the market, and use the beta formula from the book. You will need to use two Excel functions: STDEV.S and CORREL] Numeric Answer S&PS00 DECK NKE SBUX -1.5% Ос-19 7.4%...

On Blackboard under "Course Content / Homeworks and Practice Tests" there is an Excel file titled "HW 6 Data" with monthly stock return data to be used for this question: What is Deckers Outdoor Corporation's [DECK] beta? Round to two decimal places. [Hint: Take S&P 500 as a proxy for the market, and use the beta formula from the book. You will need to use two Excel functions: STDEV.S and CORREL] Numeric Answer S&PS00 DECK NKE SBUX -1.5% Ос-19 7.4%...

CASE 7.1 Tires for You, Inc Tires for You, Inc. (TFY), founded in 1987, is an automotive repair shop specializing in replacement tires. Located in Altoona, Pennsylvania, TFY has grown successfully over the past few years because of the addition of a new general manager, Ian Overbaugh. Since tire replacement is a major portion of TFY's business (it also performs oil changes, small mechanical repairs, etc.), Ian was surprised at the lack of forecasts for tire consumption for the company....

CASE 7.1 Tires for You, Inc Tires for You, Inc. (TFY), founded in 1987, is an automotive repair shop specializing in replacement tires. Located in Altoona, Pennsylvania, TFY has grown successfully over the past few years because of the addition of a new general manager, Ian Overbaugh. Since tire replacement is a major portion of TFY's business (it also performs oil changes, small mechanical repairs, etc.), Ian was surprised at the lack of forecasts for tire consumption for the company....

QUESTION 10

Consider the monthly data, including the estimates for March

2020, and the information in the articles. Which of the following

is the best analysis of and prediction for the money market in the

U.S. economy for the next few months?

a.

Shortages are causing panic buying by households, which has

increased money demand. Lenders are increasing their lending to

keep up with the needs of households and businesses. Money demand

is increasing more than money supply.

b.

Shortages...

QUESTION 10

Consider the monthly data, including the estimates for March

2020, and the information in the articles. Which of the following

is the best analysis of and prediction for the money market in the

U.S. economy for the next few months?

a.

Shortages are causing panic buying by households, which has

increased money demand. Lenders are increasing their lending to

keep up with the needs of households and businesses. Money demand

is increasing more than money supply.

b.

Shortages...

CASE 1-5 Financial Statement Ratio Computation Refer to Campbell Soup Company's financial Campbell Soup statements in Appendix A. Required: Compute the following ratios for Year 11. Liquidity ratios: Asset utilization ratios:* a. Current ratio n. Cash turnover b. Acid-test ratio 0. Accounts receivable turnover c. Days to sell inventory p. Inventory turnover d. Collection period 4. Working capital turnover Capital structure and solvency ratios: 1. Fixed assets turnover e. Total debt to total equity s. Total assets turnover f. Long-term...

CASE 1-5 Financial Statement Ratio Computation Refer to Campbell Soup Company's financial Campbell Soup statements in Appendix A. Required: Compute the following ratios for Year 11. Liquidity ratios: Asset utilization ratios:* a. Current ratio n. Cash turnover b. Acid-test ratio 0. Accounts receivable turnover c. Days to sell inventory p. Inventory turnover d. Collection period 4. Working capital turnover Capital structure and solvency ratios: 1. Fixed assets turnover e. Total debt to total equity s. Total assets turnover f. Long-term...

Most questions answered within 3 hours.

-

What specific indicators can point to lack of progress for

African Americans in American society?

asked 47 minutes ago -

1-The Electrons in a beam are moving at 2.7×108 m/s in an

electric field of 15000...

asked 1 hour ago -

A gas tank is a vertical cylinder. It has a radius of 1m, a

height of...

asked 1 hour ago -

Accent Software faces the following conditions. All of these

support Accent’s use of a market-penetration pricing...

asked 2 hours ago -

A mathematically inclined friend emails you the following

instructions: "Meet me in the cafeteria the first...

asked 2 hours ago -

A monopoly sells in two countries . The demand curves in the two

countries are p1...

asked 3 hours ago -

A .15kg rubber ball is bounced off a wall. Before hitting the

wall, the ball moves...

asked 4 hours ago -

A manufacturing company preparing to build a new plant is

considering three potential locations for it....

asked 4 hours ago -

B. If compound Y has approximately the same values of solubility

in toluene as compound X,...

asked 4 hours ago -

Oscar Inc. has inventory in Japan valued at 39,051,000 Yen one

year ago. One year ago...

asked 5 hours ago -

If Canada suffered from "fundamental disequilibrium," and its

government choose not to devalue its currency, a...

asked 5 hours ago -

4. How many input & output Key Value Pairs are passed into,

and emitted out of...

asked 5 hours ago