As an intern at Hadlock & Fee Investments, you have been assigned to manage a $10...

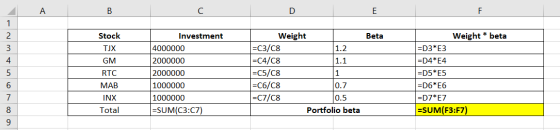

As an intern at Hadlock & Fee Investments, you have been assigned to manage a $10 million portfolio that is invested in five stocks. What is the portfolio's Beta?

Stock Amount Invested Beta

TJX $4 million 1.2

GM $2 million 1.1

RTC $2 million 1.0

MAB $1 million 0.7

INX $1 million 0.5

Homework Answers

EXCEL FORMULA:

FEEL FREE TO ASK DOUBTS... PLEASE RATE MY ANSWER

Add Answer to:

As an intern at Hadlock & Fee Investments, you have been

assigned to manage a $10...

please answer both parts 1)Quantitative Problem: You are holding a portfolio with the following investments and...

please answer both parts 1)Quantitative Problem: You are holding a portfolio with the following investments and betas: Stock Dollar investment Beta A $300,000 1.35 B 200,000 1.60 C 400,000 0.80 D 100,000 -0.35 Total investment $1,000,000 The market's required return is 11% and the risk-free rate is 4%. What is the portfolio's required return? Do not round intermediate calculations. Round your answer to three decimal places. ____ % 2)An individual has $35,000 invested in a stock with a beta of...

Problem 6-10 Portfolio Required Return Suppose you manage a $5.255 million fund that consists of four...

Problem 6-10 Portfolio Required Return Suppose you manage a $5.255 million fund that consists of four stocks with the following investments: Stock Investment Beta A $480,000 1.50 B 475,000 -0.50 C 1,500,000 1.25 D 2,800,000 0.75 If the market's required rate of return is 11% and the risk-free rate is 7%, what is the fund's required rate of return? Do not round intermediate calculations. Round your answer to two decimal places. %

Problem 6-10 Portfolio Required Return Suppose you manage a $5.375 million fund that consists of four...

Problem 6-10 Portfolio Required Return Suppose you manage a $5.375 million fund that consists of four stocks with the following investments: Stock Investment Beta A $480,000 1.50 B 675,000 -0.50 C 1,420,000 1.25 D 2,800,000 0.75 If the market's required rate of return is 8% and the risk-free rate is 6%, what is the fund's required rate of return? Do not round intermediate calculations. Round your answer to two decimal places.

Please show all work. Thanks! An optimal risky portfolio has been developed with investments in stocks...

Please show all work. Thanks!

An optimal risky portfolio has been developed with investments in stocks and bonds This optimal portfolio has 24% invested in bonds and the remainder invested in stocks The optimal portfolio mean return is 12.05% and its standard deviation is 18.45% The t-bill rate is 4.75%; what is the mean of the complete portfolio if 33% is invested in the optimal portfolio and theremainder is invested in T-bills? a What is the resulting allocation to stocks...

Please show all work. Thanks!

An optimal risky portfolio has been developed with investments in stocks and bonds This optimal portfolio has 24% invested in bonds and the remainder invested in stocks The optimal portfolio mean return is 12.05% and its standard deviation is 18.45% The t-bill rate is 4.75%; what is the mean of the complete portfolio if 33% is invested in the optimal portfolio and theremainder is invested in T-bills? a What is the resulting allocation to stocks...

Tom O'Brien has a 2-stock portfolio with a total value of $100,000 $47.500 is invested in Stock A with a beta...

Tom O'Brien has a 2-stock portfolio with a total value of $100,000 $47.500 is invested in Stock A with a beta of 0.75 and the remainder is invested in Stock B with a beta of 1.42. What is his portfolio's beta? Do not round your intermediate calculations. Round your final answer to 2 decimal places. a. 1.06 O b. 1.05 . c. 1.09 • O d. 1.10 OOO oooo.. o. Click here to read the eBook: The Relationship Between Risk...

Tom O'Brien has a 2-stock portfolio with a total value of $100,000 $47.500 is invested in Stock A with a beta of 0.75 and the remainder is invested in Stock B with a beta of 1.42. What is his portfolio's beta? Do not round your intermediate calculations. Round your final answer to 2 decimal places. a. 1.06 O b. 1.05 . c. 1.09 • O d. 1.10 OOO oooo.. o. Click here to read the eBook: The Relationship Between Risk...

You plan to invest in the Kish Hedge Fund, which has total capital of R500 million...

You plan to invest in the Kish Hedge Fund, which has total capital of R500 million invested in five stocks: Stock Investment Stock's Beta Coefficient A 160 million 0.5 B 120 million 1.2 C 80 million 1.8 D 80 million 1.0 E 60 million 1.6 Kish's beta coefficient can be found as a weighted average of its stocks' betas. The risk-free rate is 6%, and you believe the following probability distribution for future market returns is realistic: Probability Market Return...

3. Stocks A, B, C and D have the same standard deviation of 10% and the...

3. Stocks A, B, C and D have the same standard deviation of 10% and the same expected return of 5%. The following table shows the correlation coefficient between the returns on these stocks. (note that correlation with itself is always 1). Stock B Stock C Stock D Stock A Stock B Stock C Stock D Stock A 1.0 -0.4 0.9 -0.1 1.0 0.1 1.0 -0.5 -0.2 1.0 (a) Consider a portfolio P = 0 A+ B+ C, calculate the...

3. Stocks A, B, C and D have the same standard deviation of 10% and the same expected return of 5%. The following table shows the correlation coefficient between the returns on these stocks. (note that correlation with itself is always 1). Stock B Stock C Stock D Stock A Stock B Stock C Stock D Stock A 1.0 -0.4 0.9 -0.1 1.0 0.1 1.0 -0.5 -0.2 1.0 (a) Consider a portfolio P = 0 A+ B+ C, calculate the...

Problem #5 (12 Marks) You have a portfolio with a standard deviation of 30% and an...

Problem #5 (12 Marks) You have a portfolio with a standard deviation of 30% and an expected return of 18%. You are considering adding one of the two stocks in the table below to your portfolio. After adding the stock, you will have 20% of your money in the new stock and 80% of your money in your existing portfolio. A) Calculate the risk and return of a new portfolio with 20% invested in stock A and 80% in your...

Problem #5 (12 Marks) You have a portfolio with a standard deviation of 30% and an expected return of 18%. You are considering adding one of the two stocks in the table below to your portfolio. After adding the stock, you will have 20% of your money in the new stock and 80% of your money in your existing portfolio. A) Calculate the risk and return of a new portfolio with 20% invested in stock A and 80% in your...

ignore question 6 i forgot to crop the screenshot 5. You plan to invest in the...

ignore question 6 i forgot to crop the screenshot

5. You plan to invest in the Kish Hedge Fund, which has total capital of $500 million invested in five stocks: Stock Investment Beta А $160 million 0.5 B 120 million 1.2 с 80 million 1.8 D 80 million 1.0 60 million 1.6 Kish's beta coefficient can be found as a weighted average of its stocks" betas. The risk-free rate is 6% and you believe that following probability distribution for future...

ignore question 6 i forgot to crop the screenshot

5. You plan to invest in the Kish Hedge Fund, which has total capital of $500 million invested in five stocks: Stock Investment Beta А $160 million 0.5 B 120 million 1.2 с 80 million 1.8 D 80 million 1.0 60 million 1.6 Kish's beta coefficient can be found as a weighted average of its stocks" betas. The risk-free rate is 6% and you believe that following probability distribution for future...

1. Problem 6-10 Portfolio Required Return Suppose you manage a $3.8 million fund that consists of...

1. Problem 6-10 Portfolio Required Return Suppose you manage a $3.8 million fund that consists of four stocks with the following investments: Stock Investment Beta A $200,000 1.50 B 550,000 -0.50 C 900,000 1.25 D 2,150,000 0.75 If the market's required rate of return is 9% and the risk-free rate is 5%, what is the fund's required rate of return? Do not round intermediate calculations. Round your answer to two decimal places. % 2. Problem 9-2 After-Tax Cost of Debt...

Please show all work. Thanks!

An optimal risky portfolio has been developed with investments in stocks and bonds This optimal portfolio has 24% invested in bonds and the remainder invested in stocks The optimal portfolio mean return is 12.05% and its standard deviation is 18.45% The t-bill rate is 4.75%; what is the mean of the complete portfolio if 33% is invested in the optimal portfolio and theremainder is invested in T-bills? a What is the resulting allocation to stocks...

Please show all work. Thanks!

An optimal risky portfolio has been developed with investments in stocks and bonds This optimal portfolio has 24% invested in bonds and the remainder invested in stocks The optimal portfolio mean return is 12.05% and its standard deviation is 18.45% The t-bill rate is 4.75%; what is the mean of the complete portfolio if 33% is invested in the optimal portfolio and theremainder is invested in T-bills? a What is the resulting allocation to stocks...

Tom O'Brien has a 2-stock portfolio with a total value of $100,000 $47.500 is invested in Stock A with a beta of 0.75 and the remainder is invested in Stock B with a beta of 1.42. What is his portfolio's beta? Do not round your intermediate calculations. Round your final answer to 2 decimal places. a. 1.06 O b. 1.05 . c. 1.09 • O d. 1.10 OOO oooo.. o. Click here to read the eBook: The Relationship Between Risk...

Tom O'Brien has a 2-stock portfolio with a total value of $100,000 $47.500 is invested in Stock A with a beta of 0.75 and the remainder is invested in Stock B with a beta of 1.42. What is his portfolio's beta? Do not round your intermediate calculations. Round your final answer to 2 decimal places. a. 1.06 O b. 1.05 . c. 1.09 • O d. 1.10 OOO oooo.. o. Click here to read the eBook: The Relationship Between Risk...

3. Stocks A, B, C and D have the same standard deviation of 10% and the same expected return of 5%. The following table shows the correlation coefficient between the returns on these stocks. (note that correlation with itself is always 1). Stock B Stock C Stock D Stock A Stock B Stock C Stock D Stock A 1.0 -0.4 0.9 -0.1 1.0 0.1 1.0 -0.5 -0.2 1.0 (a) Consider a portfolio P = 0 A+ B+ C, calculate the...

3. Stocks A, B, C and D have the same standard deviation of 10% and the same expected return of 5%. The following table shows the correlation coefficient between the returns on these stocks. (note that correlation with itself is always 1). Stock B Stock C Stock D Stock A Stock B Stock C Stock D Stock A 1.0 -0.4 0.9 -0.1 1.0 0.1 1.0 -0.5 -0.2 1.0 (a) Consider a portfolio P = 0 A+ B+ C, calculate the...

Problem #5 (12 Marks) You have a portfolio with a standard deviation of 30% and an expected return of 18%. You are considering adding one of the two stocks in the table below to your portfolio. After adding the stock, you will have 20% of your money in the new stock and 80% of your money in your existing portfolio. A) Calculate the risk and return of a new portfolio with 20% invested in stock A and 80% in your...

Problem #5 (12 Marks) You have a portfolio with a standard deviation of 30% and an expected return of 18%. You are considering adding one of the two stocks in the table below to your portfolio. After adding the stock, you will have 20% of your money in the new stock and 80% of your money in your existing portfolio. A) Calculate the risk and return of a new portfolio with 20% invested in stock A and 80% in your...

ignore question 6 i forgot to crop the screenshot

5. You plan to invest in the Kish Hedge Fund, which has total capital of $500 million invested in five stocks: Stock Investment Beta А $160 million 0.5 B 120 million 1.2 с 80 million 1.8 D 80 million 1.0 60 million 1.6 Kish's beta coefficient can be found as a weighted average of its stocks" betas. The risk-free rate is 6% and you believe that following probability distribution for future...

ignore question 6 i forgot to crop the screenshot

5. You plan to invest in the Kish Hedge Fund, which has total capital of $500 million invested in five stocks: Stock Investment Beta А $160 million 0.5 B 120 million 1.2 с 80 million 1.8 D 80 million 1.0 60 million 1.6 Kish's beta coefficient can be found as a weighted average of its stocks" betas. The risk-free rate is 6% and you believe that following probability distribution for future...

Most questions answered within 3 hours.

-

Write a program to solve the Josephus problem, with the following

modification:

Sample Input:

./a.out n...

asked 59 minutes ago -

At the start of a CD it is spinning at a rate of 525 rpm

(revolutions...

asked 1 hour ago -

4. Without doing any calculations, predict whether the observed

∆T would increase, decrease or remain the...

asked 2 hours ago -

Based on the range, which of the following sets of scores has

the greatest variability? 3,...

asked 3 hours ago -

Ripples in a pond travel at a velocity of 3 m/s with one peak

passing a...

asked 3 hours ago -

A man stands on the roof of a building of height 13.0 mm and

throws a...

asked 3 hours ago -

The extent to which assets are financed by borrowed funds and

other liabilities is indicated by:...

asked 4 hours ago -

Explain in detail

Germany is the fifth largest economy

explain what goods and services Germany specializes...

asked 5 hours ago -

The density of platinum is 21.45 g/mL. If a cube of platinum

with a mass of...

asked 5 hours ago -

Accounts Receivable

Sales

A/R Posting

Extended Sales Invoice

Packing Slip

Compare invoice to packing slip 2...

asked 5 hours ago -

Michaella, age 23, is a full-time law student and is claimed by

her parents as a...

asked 5 hours ago -

Why are polymers not typically casted into products?

asked 5 hours ago