The current price of the Gilead stock is $77 per share. Consider an option strategy, which...

The current price of the Gilead stock is $77 per share. Consider an option strategy, which consists of following positions:

- Selling one put option on the Gilead stock with the strike price of $75. The price of this put option is $3.44.

- Buying one put option on the Gilead stock with the strike price of $72. The price of this option is $2.24.

- Buying one call option on the Gilead stock with the strike price of $81. The price of this option is $3.10.

- Selling one call option on the Gilead stock with the strike price of $79. The price of this option is $3.90

All options expire in 3 months.

- Construct the payoff table for this strategy at expiration;

- Construct the graph, which illustrates the payoff of this strategy at expiration. The payoff table should help you to construct this graph.

- What is the cost of this strategy?

- Draw the graph, showing profit/loss of this strategy at expiration (you can disregard the time value of money);

- In your opinion, what is the rationale for constructing this strategy?

Homework Answers

Belos is the data table:

- Put option is the right to sell at the strike price

- It is exercised when the spot price < strike price

- Payoff for Long is Strike - Spot

- Payoff for Short is Spot - Strike

- Long will Profit = Payoff - Premium

- Short will Profit = Payoff + Premium

- Call option is the right to buy at the strike price

- It is exercised when the spot price > strike price

- Payoff for Short is Strike - Spot

- Payoff for Long is Spot - Strike

- Long will Profit = Payoff - Premium

- Short will Profit = Payoff + Premium

- Based on all these points the above table is calculated.

- Total Payoff is the sum of all payoffs for all the options

- Total Profit is the sum of all profit for all the options

Using this we can create the payoff or profit diagram.

Total payoff of the strategy is as follows:

The cost of this strategy is the premiums paid-premiums received

The cost of this strategy is the 2.24+3.1-3.44-3.9 = -2 which implies that the cost is negative or in fact $2 premium is pocketed.

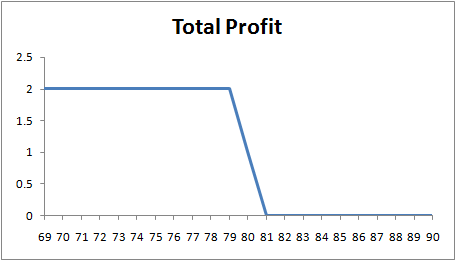

Total profit is as follows:

Reason for this strategy:

- The investor believes that the price will fall. But he cant be sure of it so he buys a call option of a higher strike price and sells a call option of a lower strike price. As the lower strike price is more profitable from long's perspective, it costs more and because the investor believes that the options will never be exercised, he will pocket the net premium on these two options

- Further, as the investor believes that the price will fall, but he cant be sure of it so he buys a put option of a lower strike price and sells a put option of a higher strike price. As the higher strike price is more profitable from long's perspective, it costs more and because the investor believes that the options will never be exercised, he will pocket the net premium on these two options

- This is seen in the total cost being negative.

- Also, it limits the negative payoff at -2 but the profit cant got lower than 0 and can get stable at 2 if price remain at 79 or fall below. So investor has secured upper and lower limit of his profit.

Add Answer to:

The current price of the Gilead stock is $77 per share. Consider

an option strategy, which...

A call option on a stock with a strike price of $60 costs $8. A put...

A call option on a stock with a strike price of $60 costs $8. A put option on the same stock with the same strike price costs $6. They both expire in 1 year. (a) How can these two options be used to create a straddle? (b) What is the initial investment? (c) Construct a table showing how the payoff and profit varies with ST in 1 year, for the straddle that you constructed. Whenever you need to refer to...

5. Suppose the current price of a stock is $35, and one associated six-month call option...

5. Suppose the current price of a stock is $35, and one associated six-month call option with a strike price of $36 currently sell for $3.5. Rachel Heyhoe-Flint, an amateur investor, feels that the price of the stock will increase and so she comes up with the following two possible strategies: (i) purchase 100 shares and (ii) buying 1,000 call options. Both strategies involve an investment of $3,500. How much the stock has to rise after six months for the...

5. Suppose the current price of a stock is $35, and one associated six-month call option with a strike price of $36 currently sell for $3.5. Rachel Heyhoe-Flint, an amateur investor, feels that the price of the stock will increase and so she comes up with the following two possible strategies: (i) purchase 100 shares and (ii) buying 1,000 call options. Both strategies involve an investment of $3,500. How much the stock has to rise after six months for the...

The goal of this project is to examine option trading strategies. The project requires you to...

The goal of this project is to examine option trading strategies. The project requires you to work in Excel with the provided spreadsheet. A) Bull Spread Payoff Long call option K1 = Short call option K2 = Stock Price (ST) Total Payoff $0.00 $5.00 $10.00 $15.00 $20.00 $25.00 $30.00 $35.00 $40.00 $45.00 $50.00 $55.00 $60.00 A) Consider buying a call option with a strike of $20 and a selling call option with strike of $30. Fill in the table for...

You own a put option on Ford stock with a strike price of $14. The option...

You own a put option on Ford stock with a strike price of $14. The option will expire in exactly six months' time. When you bought the put, its cost to you was $2. The option will expire in exacly six months' time. a. If the stock is trading at $10 in six months, what will be the payoff of the put? What will be the profit of the put? b. If the stock is trading at $25 in six...

You own a put option on Ford stock with a strike price of $14. The option will expire in exactly six months' time. When you bought the put, its cost to you was $2. The option will expire in exacly six months' time. a. If the stock is trading at $10 in six months, what will be the payoff of the put? What will be the profit of the put? b. If the stock is trading at $25 in six...

You own a put option on Ford stock with a strike price of $11. The option...

You own a put option on Ford stock with a strike price of $11. The option will expire in exactly six months' time. When you bought the put, its oost to you was $2. The option will expire in exactly six months' time. a. If the stock is trading at $7 in six months, what will be the payoff of the put? What will be the profit of the put? b. If the stock is trading at $20 in six...

You own a put option on Ford stock with a strike price of $11. The option will expire in exactly six months' time. When you bought the put, its oost to you was $2. The option will expire in exactly six months' time. a. If the stock is trading at $7 in six months, what will be the payoff of the put? What will be the profit of the put? b. If the stock is trading at $20 in six...

5. A call option on Company B common stock is worth $8 with 7 months before...

5. A call option on Company B common stock is worth $8 with 7 months before expiration. The strike price on the call is $40 and the price per share is currently trading at $44 per share. The put option at the same exercise price is worth $1.50. a. Is the call option in or out or the money? b. Is the put option in or out of the money? c. At what extra above expiration value is the call...

g) European call with a strike price of $40 costs $7. European put with the same...

g) European call with a strike price of $40 costs $7. European put with the same strike price and expiration date costs $6. Assume that you buy two calls and one put (strap strategy). Sketch the graph and write down functions of payoff and profit h) Consider a stock with a price of $50 and there is European put option on that stock with the strike of $55 and premium of $4. Assume that you buy 1/3 of a stock...

g) European call with a strike price of $40 costs $7. European put with the same strike price and expiration date costs $6. Assume that you buy two calls and one put (strap strategy). Sketch the graph and write down functions of payoff and profit h) Consider a stock with a price of $50 and there is European put option on that stock with the strike of $55 and premium of $4. Assume that you buy 1/3 of a stock...

You own a call option on Intuit stock with a strike price of $41. When you...

You own a call option on Intuit stock with a strike price of $41. When you purchased the option, it cost you $5. The option will expire in exactly three months' time. a. If the stock is trading at $46 in three months, what will be the payoff of the call? What will be the profit of the call? b. If the stock is trading at $36 in three months, what will be the payoff of the call? What will...

You own a call option on Intuit stock with a strike price of $41. When you purchased the option, it cost you $5. The option will expire in exactly three months' time. a. If the stock is trading at $46 in three months, what will be the payoff of the call? What will be the profit of the call? b. If the stock is trading at $36 in three months, what will be the payoff of the call? What will...

Open Buying a Call Stock Option Open Buying a Put Stock Option Number Strike Stock Call...

Open Buying a Call Stock Option Open Buying a Put Stock Option Number Strike Stock Call Number Strike Stock Put of Contracts Price Price Premium of Contracts Price Price Premium 1 36 35 1.25 1 36 35 1.45 Intrinsic Value Intrinsic Value Time Value Time Value Cost Cost Close Close Number Strike Stock Call Number Strike Stock Put of Contracts Price Price Premium of Contracts Price Price Premium 1 36 40 4.25 1 36 40 0.05 Intrinsic Value Intrinsic Value...

A 6-month European call option with a strike price of $25

A 6-month European call option with a strike price of $25 costs $2.24. A 6-month European put option with a strike price of $20 costs $1.31. a. Explain how a strangle can be created from these two options. b. Construct a table that shows the profit from the strategy. c. For what range of stock prices would the strategy lead to a profit.

5. Suppose the current price of a stock is $35, and one associated six-month call option with a strike price of $36 currently sell for $3.5. Rachel Heyhoe-Flint, an amateur investor, feels that the price of the stock will increase and so she comes up with the following two possible strategies: (i) purchase 100 shares and (ii) buying 1,000 call options. Both strategies involve an investment of $3,500. How much the stock has to rise after six months for the...

5. Suppose the current price of a stock is $35, and one associated six-month call option with a strike price of $36 currently sell for $3.5. Rachel Heyhoe-Flint, an amateur investor, feels that the price of the stock will increase and so she comes up with the following two possible strategies: (i) purchase 100 shares and (ii) buying 1,000 call options. Both strategies involve an investment of $3,500. How much the stock has to rise after six months for the...

You own a put option on Ford stock with a strike price of $14. The option will expire in exactly six months' time. When you bought the put, its cost to you was $2. The option will expire in exacly six months' time. a. If the stock is trading at $10 in six months, what will be the payoff of the put? What will be the profit of the put? b. If the stock is trading at $25 in six...

You own a put option on Ford stock with a strike price of $14. The option will expire in exactly six months' time. When you bought the put, its cost to you was $2. The option will expire in exacly six months' time. a. If the stock is trading at $10 in six months, what will be the payoff of the put? What will be the profit of the put? b. If the stock is trading at $25 in six...

You own a put option on Ford stock with a strike price of $11. The option will expire in exactly six months' time. When you bought the put, its oost to you was $2. The option will expire in exactly six months' time. a. If the stock is trading at $7 in six months, what will be the payoff of the put? What will be the profit of the put? b. If the stock is trading at $20 in six...

You own a put option on Ford stock with a strike price of $11. The option will expire in exactly six months' time. When you bought the put, its oost to you was $2. The option will expire in exactly six months' time. a. If the stock is trading at $7 in six months, what will be the payoff of the put? What will be the profit of the put? b. If the stock is trading at $20 in six...

g) European call with a strike price of $40 costs $7. European put with the same strike price and expiration date costs $6. Assume that you buy two calls and one put (strap strategy). Sketch the graph and write down functions of payoff and profit h) Consider a stock with a price of $50 and there is European put option on that stock with the strike of $55 and premium of $4. Assume that you buy 1/3 of a stock...

g) European call with a strike price of $40 costs $7. European put with the same strike price and expiration date costs $6. Assume that you buy two calls and one put (strap strategy). Sketch the graph and write down functions of payoff and profit h) Consider a stock with a price of $50 and there is European put option on that stock with the strike of $55 and premium of $4. Assume that you buy 1/3 of a stock...

You own a call option on Intuit stock with a strike price of $41. When you purchased the option, it cost you $5. The option will expire in exactly three months' time. a. If the stock is trading at $46 in three months, what will be the payoff of the call? What will be the profit of the call? b. If the stock is trading at $36 in three months, what will be the payoff of the call? What will...

You own a call option on Intuit stock with a strike price of $41. When you purchased the option, it cost you $5. The option will expire in exactly three months' time. a. If the stock is trading at $46 in three months, what will be the payoff of the call? What will be the profit of the call? b. If the stock is trading at $36 in three months, what will be the payoff of the call? What will...

Most questions answered within 3 hours.

-

The charge to the left in the figure above has a

magnitude of 2.90 nC, and...

asked 39 minutes ago -

Verify the MIRR is 9.29% given cash flows in years 1 and 2 of

$1,000 each,...

asked 1 hour ago -

Calculate the pH of a 5.7 M solution of aniline (C6H5NH2; Kb =

3.8 x 10^-10)

asked 3 hours ago -

LSL R3, R3, R12

Memory

Address

Orig.

Data

Updated

Data

Register

Orig.

Data

Updated

Data

0x84F0...

asked 3 hours ago -

Air at 100 kPa and density of 1.2 kg/m3 flows upward through a

5-cm diameter inclined...

asked 3 hours ago -

Define the following concepts in your own words: (a) stiffness,

(b) strength, (c) strain,

(d) ductility,...

asked 4 hours ago -

In C++

In this homework, you will be tasked with creating functions to

manipulate strings that...

asked 5 hours ago -

An isolated colony represents a pure culture. one rare occasions

, however , a colony can...

asked 5 hours ago -

*****DO NOT ANSWER THIS QUESTION IF YOU DON'T

KNOW*******Rights and Duties of Auditors; Minimum 4000

words...

asked 6 hours ago -

The probability that Janie is wearing sunglasses is 1/4. The

probability that she is wearing sunglasses...

asked 6 hours ago -

Do you believe social media is more of a help or a hindrance in

controlling crises...

asked 7 hours ago -

Two long, parallel wires separated by 2.85 cm carry currents in

opposite directions. The current in...

asked 6 hours ago