Why do deferred tax assets or deferred tax liabilities arise

Why do deferred tax assets or deferred tax liabilities arise? Explain your answer with suitable example. The reason for the deferred tax assets and liabilities have been explained with suitable example. Explain The concepts of temporary difference, taxable temporary difference, deductible temporary differences have been linked to DTA and DTL.

Homework Answers

Step 1 What Is a Deferred Tax Asset?How Deferred Tax Assets Arise? suitable example?

Meaning

Items on a company's balance sheet that may be used to reduce taxable income in the future are called deferred tax assets. The situation can happen when a business overpaid taxes or paid taxes in advance on its balance sheet. These taxes are eventually returned to the business in the form of tax relief. Therefore, an overpayment is considered an asset to the company. A deferred tax asset is the opposite of a deferred tax liability, which can increase the amount of income tax owed by a company.

A deferred tax asset is an item on the balance sheet that results from an overpayment or advance payment of taxes.

It is the opposite of a deferred tax liability, which represents income taxes owed.

A deferred tax asset can arise when there are differences in tax rules and accounting rules or when there is a carryover of tax losses.

How Deferred Tax Assets Arise?

The simplest example of a deferred tax asset is the carryover of losses. If a business incurs a loss in a financial year, it usually is entitled to use that loss in order to lower its taxable income in the following years.2 In that sense, the loss is an asset.

Another scenario where deferred tax assets arise is when there is a difference between accounting rules and tax rules. For example, deferred taxes exist when expenses are recognized in the income statement before they are required to be recognized by the tax authorities or when revenue is subject to taxes before it is taxable in the income statement. Essentially, whenever the tax base or tax rules for assets and/or liabilities are different, there is an opportunity for the creation of a deferred tax asset.

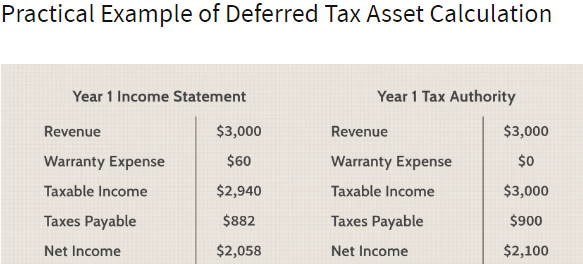

Example of Deferred Tax Asset

A computer manufacturing company estimates, based on previous experience, that the probability a computer may be sent back for warranty repairs in the next year is 2% of the total production. If the company's total revenue in year one is $3,000 and the warranty expense in its books is $60 (2% x $3,000), then the company's taxable income is $2,940. However, most tax authorities do not allow companies to deduct expenses based on expected warranties; thus the company is required to pay taxes on the full $3,000.

If the tax rate for the company is 30%, the difference of $18 ($60 x 30%) between the taxes payable in the income statement and the actual taxes paid to the tax authorities is a deferred tax asset.

Step 2What Is a Deferred Tax Liability?How Deferred Tax Liability Arise? suitable example?

Meaning

Deferred tax liability is a tax that is assessed or is due for the current period but has not yet been paid—meaning that it will eventually come due. The deferral comes from the difference in timing between when the tax is accrued and when the tax is paid. A deferred tax liability records the fact the company will, in the future, pay more income tax because of a transaction that took place during the current period, such as an instalment sale receivable.

A deferred tax liability represents an obligation to pay taxes in the future.

The obligation originates when a company or individual delays an event that would cause it to also recognize tax expenses in the current period.

For instance, earning returns in a qualified retirement plan, like a 401(k), represents a deferred tax liability since the retirement saver will eventually have to pay taxes on the saved income and gains upon withdrawal.

How Deferred Tax Liability Arise?

A common source of deferred tax liability is the difference in depreciation expense treatment by tax laws and accounting rules. The depreciation expense for long-lived assets for financial statement purposes is typically calculated using a straight-line method, while tax regulations allow companies to use an accelerated depreciation method. Since the straight-line method produces lower depreciation when compared to that of the under accelerated method, a company's accounting income is temporarily higher than its taxable income.

Another common source of deferred tax liability is an instalment sale, which is the revenue recognized when a company sells its products on credit to be paid off in equal amounts in the future. Under accounting rules, the company is allowed to recognize full income from the instalment sale of general merchandise, while tax laws require companies to recognize the income when instalment payments are made. This creates a temporary positive difference between the company's accounting earnings and taxable income, as well as a deferred tax liability.

Example of Deferred Tax Liability

Consider a company that sold a $1,000 piece of furniture with a 20% tax rate, which is paid for in monthly installments by the customer. The customer will pay this over two years ($500 + $500). For financial purposes, the company will record a sale of $1,000. Meanwhile, for tax purposes, they will record it as $500. As a result, the deferred tax liability would be $500 x 20% = $100.

temporary difference, taxable temporary difference, deductible temporary difference

The company derives its book profits from the financial statements prepared in accordance with the rules of the Companies Act and calculates its taxable profit based on the provision of the Income Tax Act. There is a difference between the book profit and taxable profit because of certain items which are specifically allowed or disallowed each year for tax purposes. This difference between the book and the taxable income or expense is known as timing difference and it can be either of the following:

Temporary Difference – Differences between book income and tax income that is capable of being reversed in the subsequent period.

Permanent Difference – Differences between book income and tax income which is not capable of being reversed in the subsequent period.

3. Deferred tax assets and deferred tax liabilities arise from: a. Permanent differences between book and...

3. Deferred tax assets and deferred tax liabilities arise from: a. Permanent differences between book and tax income. b. Agreements between companies and the Internal Revenue Service to pay taxes currently owed on the installment basis. c. Future taxable and future deductible items, respectively. d. Future deductible and future taxable items, respectively. e. All of the above. 4. Kobo Roger Corp.'s taxable income differed from its accounting income computed for this past year. An item that would create a permanent...

3. Deferred tax assets and deferred tax liabilities arise from: a. Permanent differences between book and tax income. b. Agreements between companies and the Internal Revenue Service to pay taxes currently owed on the installment basis. c. Future taxable and future deductible items, respectively. d. Future deductible and future taxable items, respectively. e. All of the above. 4. Kobo Roger Corp.'s taxable income differed from its accounting income computed for this past year. An item that would create a permanent...

15. Which of the following statements is correct? a. All current deferred tax liabilities and assets...

15. Which of the following statements is correct? a. All current deferred tax liabilities and assets shall be offset and presented as a single amount on the balance sheet. b. Deferred tax assets related to carryforwards shall be classified as current or noncurrent on the balance sheet based on their expected date of reversal. c. All current and noncurrent deferred taxes shall be offset and presented as a single amount on the balance sheet. d. Deferred tax liabilities and assets...

Permanent differences (between revenues and expenses for accounting and tax purposes): can cause Deferred Tax Liabilities...

Permanent differences (between revenues and expenses for accounting and tax purposes): can cause Deferred Tax Liabilities but not Deferred Tax Liabilities to arise can cause neither Deferred Tax Assets nor Deferred Tax Liabilities to arise can cause both Deferred Tax Assets and Deferred Tax Liabilities to arise can cause Deferred Tax Assets but not Deferred Tax Liabilities to arise

Why is this called deferred tax liability instead of deferred tax asset? Alvis Corporation reports pretax...

Why is this called deferred tax liability instead of

deferred tax asset?

Alvis Corporation reports pretax accounting income of $400,000, but due to a single temporary difference, taxable income is only $250.000. At the beginning of the year, no temporary differences existed Required: 1. Assuming a tax rate of 35%, what will be Alvis's net income? 2. What will Alvis report in the balance sheet pertaining to income taxes? Step-by-step solution Step 1 of 2 A Requirement 1 Since taxable...

Why is this called deferred tax liability instead of

deferred tax asset?

Alvis Corporation reports pretax accounting income of $400,000, but due to a single temporary difference, taxable income is only $250.000. At the beginning of the year, no temporary differences existed Required: 1. Assuming a tax rate of 35%, what will be Alvis's net income? 2. What will Alvis report in the balance sheet pertaining to income taxes? Step-by-step solution Step 1 of 2 A Requirement 1 Since taxable...

At the end of 2018, Smith Corporation had no book-tax differences and no deferred income tax...

At the end of 2018, Smith Corporation had no book-tax differences and no deferred income tax assets or deferred income tax liabilities. During the year 2019, two book-tax differences occurred. One was a $10,000 permanent difference that caused taxable income to be larger than financial income. The other was a $110,000 temporary difference that caused taxable income to be smaller than financial income. That $110,000 temporary difference will reverse over the years 2020 and 2021, causing future taxable amounts of...

P4. Temporary Differences, Deferred Tax Assets and Liabilities, Realizability of Deferred Assets, Change in Tax Rate....

P4. Temporary Differences, Deferred Tax Assets and Liabilities, Realizability of Deferred Assets, Change in Tax Rate. The following information is available for the first 4 years of operations for Shooting Star Corporation: Taxable Income (incorporates all information presented) Enacted Tax Rate (%) Year $200,000 2018 40% 2019 132,000 40 110,000 2020 40 2021 120,000 40 On January 2, 2018, the firm acquired heavy equipment costing $200,000 in a cash transaction. The equip- ment had a useful life of 5 years...

P4. Temporary Differences, Deferred Tax Assets and Liabilities, Realizability of Deferred Assets, Change in Tax Rate. The following information is available for the first 4 years of operations for Shooting Star Corporation: Taxable Income (incorporates all information presented) Enacted Tax Rate (%) Year $200,000 2018 40% 2019 132,000 40 110,000 2020 40 2021 120,000 40 On January 2, 2018, the firm acquired heavy equipment costing $200,000 in a cash transaction. The equip- ment had a useful life of 5 years...

Here’s an excerpt from one AF’s notes to its financial statements: Deferred taxes (in part) Deferred tax assets related...

Here’s an excerpt from one AF’s notes to its financial statements: Deferred taxes (in part) Deferred tax assets related to temporary differences and carryforwards are recognized only to the extent it is probable that a future taxable profit will be available against which the asset can be utilized at the tax entity level. Is this policy consistent with U.S. GAAP? Explain.

For financial reporting, income tax expense includes the following two components: Deferred income tax liabilities &...

For financial reporting, income tax expense includes the following two components: Deferred income tax liabilities & deferred income tax assets Current income tax & deferred income tax Income tax payable & income tax refunds Future deductible amounts & future taxable amounts

6) For reporting purposes, deferred tax assets and deferred tax labilities for the same company and...

6) For reporting purposes, deferred tax assets and deferred tax labilities for the same company and tax jurisdiction are: a. Reported separately in the balance sheet. b. Reflected only in the notes to the financial statements. C. Combined with noncurrent deferred tax assets and noncurrent deferred tax liabilities in the balance sheet to show a single net noncurrent among. d. Netted against one another and show as a net current asset or liability in the balance sheet. 7) of the...

6) For reporting purposes, deferred tax assets and deferred tax labilities for the same company and tax jurisdiction are: a. Reported separately in the balance sheet. b. Reflected only in the notes to the financial statements. C. Combined with noncurrent deferred tax assets and noncurrent deferred tax liabilities in the balance sheet to show a single net noncurrent among. d. Netted against one another and show as a net current asset or liability in the balance sheet. 7) of the...

(I dont know if the selected answers are correct) Lynch Company had a net deferred tax...

(I dont know if the selected answers are correct)

Lynch Company had a net deferred tax asset of $68,000 at the beginning of the year, representing a net deductible temporary difference of $200,000 (taxed at 34 percent). During the year, Lynch reported pretax book income of $800,000. Included in the computation were favorable temporary differences of $20,000 and unfavorable temporary differences of $50,000. At the beginning of the year, Congress reduced the corporate tax rate to 21 percent Lynch's deferred...

(I dont know if the selected answers are correct)

Lynch Company had a net deferred tax asset of $68,000 at the beginning of the year, representing a net deductible temporary difference of $200,000 (taxed at 34 percent). During the year, Lynch reported pretax book income of $800,000. Included in the computation were favorable temporary differences of $20,000 and unfavorable temporary differences of $50,000. At the beginning of the year, Congress reduced the corporate tax rate to 21 percent Lynch's deferred...

3. Deferred tax assets and deferred tax liabilities arise from: a. Permanent differences between book and tax income. b. Agreements between companies and the Internal Revenue Service to pay taxes currently owed on the installment basis. c. Future taxable and future deductible items, respectively. d. Future deductible and future taxable items, respectively. e. All of the above. 4. Kobo Roger Corp.'s taxable income differed from its accounting income computed for this past year. An item that would create a permanent...

3. Deferred tax assets and deferred tax liabilities arise from: a. Permanent differences between book and tax income. b. Agreements between companies and the Internal Revenue Service to pay taxes currently owed on the installment basis. c. Future taxable and future deductible items, respectively. d. Future deductible and future taxable items, respectively. e. All of the above. 4. Kobo Roger Corp.'s taxable income differed from its accounting income computed for this past year. An item that would create a permanent...

Why is this called deferred tax liability instead of

deferred tax asset?

Alvis Corporation reports pretax accounting income of $400,000, but due to a single temporary difference, taxable income is only $250.000. At the beginning of the year, no temporary differences existed Required: 1. Assuming a tax rate of 35%, what will be Alvis's net income? 2. What will Alvis report in the balance sheet pertaining to income taxes? Step-by-step solution Step 1 of 2 A Requirement 1 Since taxable...

Why is this called deferred tax liability instead of

deferred tax asset?

Alvis Corporation reports pretax accounting income of $400,000, but due to a single temporary difference, taxable income is only $250.000. At the beginning of the year, no temporary differences existed Required: 1. Assuming a tax rate of 35%, what will be Alvis's net income? 2. What will Alvis report in the balance sheet pertaining to income taxes? Step-by-step solution Step 1 of 2 A Requirement 1 Since taxable...

P4. Temporary Differences, Deferred Tax Assets and Liabilities, Realizability of Deferred Assets, Change in Tax Rate. The following information is available for the first 4 years of operations for Shooting Star Corporation: Taxable Income (incorporates all information presented) Enacted Tax Rate (%) Year $200,000 2018 40% 2019 132,000 40 110,000 2020 40 2021 120,000 40 On January 2, 2018, the firm acquired heavy equipment costing $200,000 in a cash transaction. The equip- ment had a useful life of 5 years...

P4. Temporary Differences, Deferred Tax Assets and Liabilities, Realizability of Deferred Assets, Change in Tax Rate. The following information is available for the first 4 years of operations for Shooting Star Corporation: Taxable Income (incorporates all information presented) Enacted Tax Rate (%) Year $200,000 2018 40% 2019 132,000 40 110,000 2020 40 2021 120,000 40 On January 2, 2018, the firm acquired heavy equipment costing $200,000 in a cash transaction. The equip- ment had a useful life of 5 years...

6) For reporting purposes, deferred tax assets and deferred tax labilities for the same company and tax jurisdiction are: a. Reported separately in the balance sheet. b. Reflected only in the notes to the financial statements. C. Combined with noncurrent deferred tax assets and noncurrent deferred tax liabilities in the balance sheet to show a single net noncurrent among. d. Netted against one another and show as a net current asset or liability in the balance sheet. 7) of the...

6) For reporting purposes, deferred tax assets and deferred tax labilities for the same company and tax jurisdiction are: a. Reported separately in the balance sheet. b. Reflected only in the notes to the financial statements. C. Combined with noncurrent deferred tax assets and noncurrent deferred tax liabilities in the balance sheet to show a single net noncurrent among. d. Netted against one another and show as a net current asset or liability in the balance sheet. 7) of the...

(I dont know if the selected answers are correct)

Lynch Company had a net deferred tax asset of $68,000 at the beginning of the year, representing a net deductible temporary difference of $200,000 (taxed at 34 percent). During the year, Lynch reported pretax book income of $800,000. Included in the computation were favorable temporary differences of $20,000 and unfavorable temporary differences of $50,000. At the beginning of the year, Congress reduced the corporate tax rate to 21 percent Lynch's deferred...

(I dont know if the selected answers are correct)

Lynch Company had a net deferred tax asset of $68,000 at the beginning of the year, representing a net deductible temporary difference of $200,000 (taxed at 34 percent). During the year, Lynch reported pretax book income of $800,000. Included in the computation were favorable temporary differences of $20,000 and unfavorable temporary differences of $50,000. At the beginning of the year, Congress reduced the corporate tax rate to 21 percent Lynch's deferred...

Most questions answered within 3 hours.

-

Calculate the number density of argon gas at a temperature of

24C and a pressure of...

asked 18 minutes ago -

Alternative

Classification

How to Estimate

Probabilities from Data? ( For continuous Attributes)

And How to generate...

asked 21 minutes ago -

An explosion breaks a 20.0-kg object into three parts. The

object is initially moving at a...

asked 1 hour ago -

Calculate the approximate number of residues of Rubisco, which

is involved in carbon fixation in plants,...

asked 2 hours ago -

Other decisions about scientific claims can have a much broader

impact.ENERGYarrow-10x10.png, environment, health, security - all...

asked 3 hours ago -

I need to write a research paper and work cited about this

topic: The United States...

asked 3 hours ago -

Hello! I was wondering if I could have some help?

If the vapor pressure of carvone...

asked 3 hours ago -

An economist wants to estimate the mean per capita income (in

thousands of dollars) for a...

asked 4 hours ago -

What would be the input/output characteristic of a circuit

obtained by putting two of your 2's-complementers...

asked 4 hours ago -

In Drosophila, the transition from the syncytial blastoderm

stage to the cellular blastoderm stage is a...

asked 4 hours ago -

Project management question:

Name 3 different types of resources (hint: humans are one

type)

asked 4 hours ago -

Consider the following reaction: C 2H 2( g) + 2H 2( g) C 2H 6(

g)...

asked 5 hours ago