x

xHomework Answers

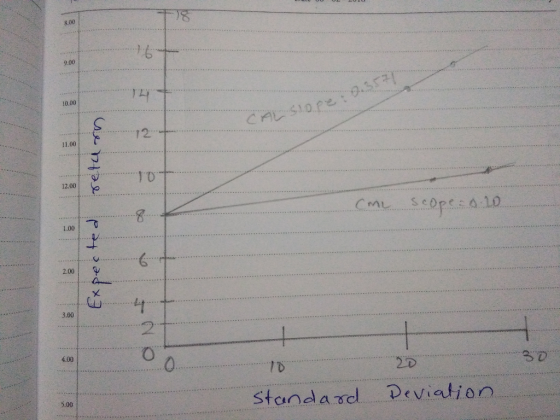

| Part A | Scal = (18% - 8%)/28% = 0.3771 |

| Scml = (13%-8%)/25%=0.2 | |

| Part B | in chart Diagram |

| Part C | My fund allows an investor to achieve a higher mean for any given standard deviationthan would a a passive strategy i.e. higher expected for any given level of risk. |

| Part D | With 70% of the funds invested in my portfolio, the clients expected return is 15% per year and standard deviation is 19.6%per year. If he shifts that money to the passive portfolio (which has an expected rate of return of 13% and standard deviation of 25%) his overall expetected return becomes: |

| E(rC) = rF + 0.7[E(rM)-rf] = 8+ [0.7*(13-8) = 11.5% | |

| The Standard Deviation of the complete portfoilio using the passive portfolio would be: | |

| 0.7 *25% = 17.5% | |

| So the shift entails a decrease in mean from 15 to 11.5 % and a standard decrease in standard deviation from 19.6% to 17.5%. Since both return and deviation decrease, thus the move is not beneficial. |

Add Answer to:

x

You estimate that a passive portfolio, that is, one invested in a risky portfolio that...

You manage a risky portfolio with an expected rate of return of 18% and a standard...

You manage a risky portfolio with an expected rate of return of 18% and a standard deviation of 28%. The T-bill rate is 8%. Your client's degree of risk aversion is A= 3.5, assuming a utility function U=EU - VAо. a. What proportion, y, of the total investment should be invested in your fund? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Investment proportion y b. What is the expected value and standard deviation of the...

You manage a risky portfolio with an expected rate of return of 18% and a standard deviation of 28%. The T-bill rate is 8%. Your client's degree of risk aversion is A= 3.5, assuming a utility function U=EU - VAо. a. What proportion, y, of the total investment should be invested in your fund? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Investment proportion y b. What is the expected value and standard deviation of the...

You manage a risky portfolio with an expected rate of return of 20% and a standard...

You manage a risky portfolio with an expected rate of return of 20% and a standard deviation of 37%. The T-bill rate is 7%. Your client's degree of risk aversion is A2.5, assuming a utility function U = E) - VAO? a. What proportion, y. of the total investment should be invested in your fund? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Investment proportion y 1% b. What is the expected value and standard deviation...

You manage a risky portfolio with an expected rate of return of 20% and a standard deviation of 37%. The T-bill rate is 7%. Your client's degree of risk aversion is A2.5, assuming a utility function U = E) - VAO? a. What proportion, y. of the total investment should be invested in your fund? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Investment proportion y 1% b. What is the expected value and standard deviation...

Assume that you manage a risky portfolio with an expected rate of return of 15% and...

Assume that you manage a risky portfolio with an expected rate of return of 15% and a standard deviation of 40%. The T-bill rate is 5%. Your risky portfolio includes the following investments in the given proportions: Stock A 24 % Stock B 33 Stock C 43 Your client decides to invest in your risky portfolio a proportion (y) of his total investment budget with the remainder in a T-bill money market fund so that his overall portfolio will have...

4 Assume that you manage a risky portfolio with an expected rate of return of 20%...

4 Assume that you manage a risky portfolio with an expected rate of return of 20% and a standard deviation of 42. The T-bill rate is 4% Your risky portfolio includes the following investments in the given proportions: points 268 Stock Stock Skipped Your client decides to invest in your risky portfolio a proportion (1) of his total investment budget with the remainder in a T-bill money market fund so that his overall portfolio will have an expected rate of...

4 Assume that you manage a risky portfolio with an expected rate of return of 20% and a standard deviation of 42. The T-bill rate is 4% Your risky portfolio includes the following investments in the given proportions: points 268 Stock Stock Skipped Your client decides to invest in your risky portfolio a proportion (1) of his total investment budget with the remainder in a T-bill money market fund so that his overall portfolio will have an expected rate of...

Check Assume that you manage a risky portfolio with an expected rate of return of 15%...

Check Assume that you manage a risky portfolio with an expected rate of return of 15% and a standard deviation of 31%. The T-bill rate is 5% Your risky portfolio includes the following investments in the given proportions: 125 points Stock A Stock 8 Stock C Your client decides to invest in your risky portfolio a proportion of his total investment budget with the remainder in a T-bill money market fund so that his overall portfolio will have an expected...

Check Assume that you manage a risky portfolio with an expected rate of return of 15% and a standard deviation of 31%. The T-bill rate is 5% Your risky portfolio includes the following investments in the given proportions: 125 points Stock A Stock 8 Stock C Your client decides to invest in your risky portfolio a proportion of his total investment budget with the remainder in a T-bill money market fund so that his overall portfolio will have an expected...

3) Assume that you manage a risky portfolio with an expected rate of return of 14%...

3) Assume that you manage a risky portfolio with an expected rate of return of 14% and standard deviation of 19%. The risk-free rate rate on a Treasury-bill is 6%. a. Your client chooses to invest 60% of a portfolio in your fund and 40% in a risk-free T-bill money market fund. What is the expected return and standard deviation of your client's portfolio? b. Suppose another investor decides to invest in your risky portfolio a proportion (w) of his...

3) Assume that you manage a risky portfolio with an expected rate of return of 14% and standard deviation of 19%. The risk-free rate rate on a Treasury-bill is 6%. a. Your client chooses to invest 60% of a portfolio in your fund and 40% in a risk-free T-bill money market fund. What is the expected return and standard deviation of your client's portfolio? b. Suppose another investor decides to invest in your risky portfolio a proportion (w) of his...

You manage a risky portfolio with an expected rate of return of 18% and a standard...

You manage a risky portfolio with an expected rate of return of 18% and a standard deviation of 36%. The T-bill rate is 6%. Your risky portfolio includes the following investments in the given proportions: Stock A Stock B Stock C 279 358 388 Suppose that your client decides to invest in your portfolio a proportion y of the total investment budget so that the overall portfolio will have an expected rate of return of 15%. a. What is the...

You manage a risky portfolio with an expected rate of return of 18% and a standard deviation of 36%. The T-bill rate is 6%. Your risky portfolio includes the following investments in the given proportions: Stock A Stock B Stock C 279 358 388 Suppose that your client decides to invest in your portfolio a proportion y of the total investment budget so that the overall portfolio will have an expected rate of return of 15%. a. What is the...

Problem 5-13 Assume that you manage a risky portfolio with an expected rate of return of...

Problem 5-13 Assume that you manage a risky portfolio with an expected rate of return of 15% and a standard deviation of 40%. The T-bill rate is 5% Your risky portfolio includes the following investments in the given proportions: Stock A Stock B Stock Your client decides to invest in your risky portfolio a proportion of his total investment budget with the remainder in a T-bil money market fund so that his overall portfolio will have an expected rate of...

Problem 5-13 Assume that you manage a risky portfolio with an expected rate of return of 15% and a standard deviation of 40%. The T-bill rate is 5% Your risky portfolio includes the following investments in the given proportions: Stock A Stock B Stock Your client decides to invest in your risky portfolio a proportion of his total investment budget with the remainder in a T-bil money market fund so that his overall portfolio will have an expected rate of...

Assume that you manage a risky portfolio with an expected rate of return of 17% and...

Assume that you manage a risky portfolio with an expected rate of return of 17% and a standard deviation of 27%. The T-bill rate is 7%. Your risky portfolio includes the following investments in the given proportions: Stock A 27% Stock B 33% Stock C 40% Your client decides to invest in your risky portfolio a proportion (y) of his total investment budget with the remainder in a T-bill money market fund so that his overall portfolio will have an...

Assume that you manage a risky portfolio with an expected rate of return of 14% and...

Assume that you manage a risky portfolio with an expected rate of return of 14% and a standard deviation of 30%. The T-bill rate is 6%. Your risky portfolio includes the following investments in the given proportions: Stock A Stock B Stock C 24% 32 44 Your client decides to invest in your risky portfolio a proportion (1) of his total investment budget with the remainder in a T-bill money market fund so that his overall portfolio will have an...

Assume that you manage a risky portfolio with an expected rate of return of 14% and a standard deviation of 30%. The T-bill rate is 6%. Your risky portfolio includes the following investments in the given proportions: Stock A Stock B Stock C 24% 32 44 Your client decides to invest in your risky portfolio a proportion (1) of his total investment budget with the remainder in a T-bill money market fund so that his overall portfolio will have an...

You manage a risky portfolio with an expected rate of return of 18% and a standard deviation of 28%. The T-bill rate is 8%. Your client's degree of risk aversion is A= 3.5, assuming a utility function U=EU - VAо. a. What proportion, y, of the total investment should be invested in your fund? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Investment proportion y b. What is the expected value and standard deviation of the...

You manage a risky portfolio with an expected rate of return of 18% and a standard deviation of 28%. The T-bill rate is 8%. Your client's degree of risk aversion is A= 3.5, assuming a utility function U=EU - VAо. a. What proportion, y, of the total investment should be invested in your fund? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Investment proportion y b. What is the expected value and standard deviation of the...

You manage a risky portfolio with an expected rate of return of 20% and a standard deviation of 37%. The T-bill rate is 7%. Your client's degree of risk aversion is A2.5, assuming a utility function U = E) - VAO? a. What proportion, y. of the total investment should be invested in your fund? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Investment proportion y 1% b. What is the expected value and standard deviation...

You manage a risky portfolio with an expected rate of return of 20% and a standard deviation of 37%. The T-bill rate is 7%. Your client's degree of risk aversion is A2.5, assuming a utility function U = E) - VAO? a. What proportion, y. of the total investment should be invested in your fund? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Investment proportion y 1% b. What is the expected value and standard deviation...

4 Assume that you manage a risky portfolio with an expected rate of return of 20% and a standard deviation of 42. The T-bill rate is 4% Your risky portfolio includes the following investments in the given proportions: points 268 Stock Stock Skipped Your client decides to invest in your risky portfolio a proportion (1) of his total investment budget with the remainder in a T-bill money market fund so that his overall portfolio will have an expected rate of...

4 Assume that you manage a risky portfolio with an expected rate of return of 20% and a standard deviation of 42. The T-bill rate is 4% Your risky portfolio includes the following investments in the given proportions: points 268 Stock Stock Skipped Your client decides to invest in your risky portfolio a proportion (1) of his total investment budget with the remainder in a T-bill money market fund so that his overall portfolio will have an expected rate of...

Check Assume that you manage a risky portfolio with an expected rate of return of 15% and a standard deviation of 31%. The T-bill rate is 5% Your risky portfolio includes the following investments in the given proportions: 125 points Stock A Stock 8 Stock C Your client decides to invest in your risky portfolio a proportion of his total investment budget with the remainder in a T-bill money market fund so that his overall portfolio will have an expected...

Check Assume that you manage a risky portfolio with an expected rate of return of 15% and a standard deviation of 31%. The T-bill rate is 5% Your risky portfolio includes the following investments in the given proportions: 125 points Stock A Stock 8 Stock C Your client decides to invest in your risky portfolio a proportion of his total investment budget with the remainder in a T-bill money market fund so that his overall portfolio will have an expected...

3) Assume that you manage a risky portfolio with an expected rate of return of 14% and standard deviation of 19%. The risk-free rate rate on a Treasury-bill is 6%. a. Your client chooses to invest 60% of a portfolio in your fund and 40% in a risk-free T-bill money market fund. What is the expected return and standard deviation of your client's portfolio? b. Suppose another investor decides to invest in your risky portfolio a proportion (w) of his...

3) Assume that you manage a risky portfolio with an expected rate of return of 14% and standard deviation of 19%. The risk-free rate rate on a Treasury-bill is 6%. a. Your client chooses to invest 60% of a portfolio in your fund and 40% in a risk-free T-bill money market fund. What is the expected return and standard deviation of your client's portfolio? b. Suppose another investor decides to invest in your risky portfolio a proportion (w) of his...

You manage a risky portfolio with an expected rate of return of 18% and a standard deviation of 36%. The T-bill rate is 6%. Your risky portfolio includes the following investments in the given proportions: Stock A Stock B Stock C 279 358 388 Suppose that your client decides to invest in your portfolio a proportion y of the total investment budget so that the overall portfolio will have an expected rate of return of 15%. a. What is the...

You manage a risky portfolio with an expected rate of return of 18% and a standard deviation of 36%. The T-bill rate is 6%. Your risky portfolio includes the following investments in the given proportions: Stock A Stock B Stock C 279 358 388 Suppose that your client decides to invest in your portfolio a proportion y of the total investment budget so that the overall portfolio will have an expected rate of return of 15%. a. What is the...

Problem 5-13 Assume that you manage a risky portfolio with an expected rate of return of 15% and a standard deviation of 40%. The T-bill rate is 5% Your risky portfolio includes the following investments in the given proportions: Stock A Stock B Stock Your client decides to invest in your risky portfolio a proportion of his total investment budget with the remainder in a T-bil money market fund so that his overall portfolio will have an expected rate of...

Problem 5-13 Assume that you manage a risky portfolio with an expected rate of return of 15% and a standard deviation of 40%. The T-bill rate is 5% Your risky portfolio includes the following investments in the given proportions: Stock A Stock B Stock Your client decides to invest in your risky portfolio a proportion of his total investment budget with the remainder in a T-bil money market fund so that his overall portfolio will have an expected rate of...

Assume that you manage a risky portfolio with an expected rate of return of 14% and a standard deviation of 30%. The T-bill rate is 6%. Your risky portfolio includes the following investments in the given proportions: Stock A Stock B Stock C 24% 32 44 Your client decides to invest in your risky portfolio a proportion (1) of his total investment budget with the remainder in a T-bill money market fund so that his overall portfolio will have an...

Assume that you manage a risky portfolio with an expected rate of return of 14% and a standard deviation of 30%. The T-bill rate is 6%. Your risky portfolio includes the following investments in the given proportions: Stock A Stock B Stock C 24% 32 44 Your client decides to invest in your risky portfolio a proportion (1) of his total investment budget with the remainder in a T-bill money market fund so that his overall portfolio will have an...

Most questions answered within 3 hours.

-

1. Why are the advantages and disadvantages of object-oriented

databases? 2. What are data marts? How...

asked 8 minutes ago -

A Porsche challenges a Honda to a 4.00×102m race. Because the

Porsche's acceleration of 3.30 m/s2...

asked 9 minutes ago -

A sample of C3H8 has 1.60×1024 H atoms.

How many carbon atoms does the sample contain?...

asked 1 hour ago -

How many unique codes are possibly formed from two characters,

where the first character can be...

asked 31 minutes ago -

A concentration cell is built based on the reaction:

2H+ + 2e- ----> H2

The pH...

asked 27 minutes ago -

what is the ph of the following solutions?

150 g NH4CI dissolved into 10.0 mL of...

asked 39 minutes ago -

A projectile is launched with an initial speed of 40 m/s at an

angle of 25°...

asked 21 minutes ago -

1. Using a function, display the customer who has the highest

credit limit. Display the customer...

asked 30 minutes ago -

A spatially uniform electric field varies in time according

to E = Eo + 3000 t,...

asked 56 minutes ago -

An electric power station that operates at 25 kV and uses a 20:1

step-up ideal transformer...

asked 49 minutes ago -

1. If 0.02% of a 0.6 M weak acid ionizes in a solution, what is

the...

asked 35 minutes ago -

The College of Business at Northeast College is accumulating

data as a first step in the...

asked 41 minutes ago