Homework Answers

Add Answer to:

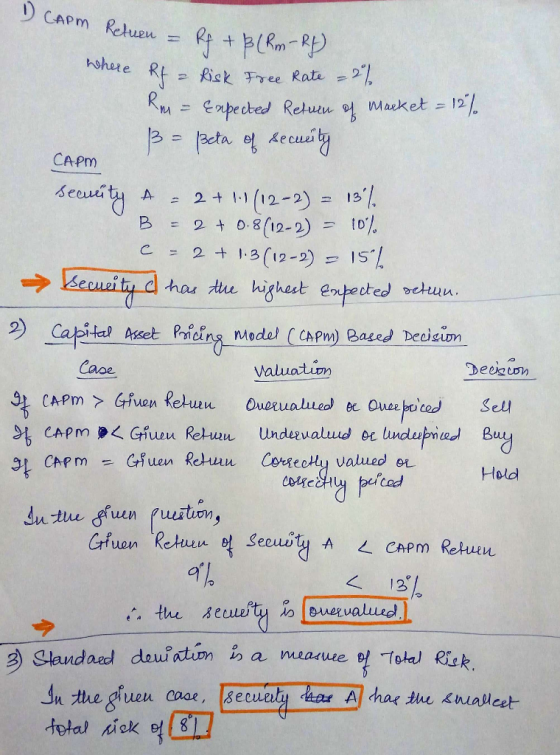

Use the following information to answer the question below Analysts Estimated Return Standard Deviation 8% Security...

CAPM Question Problem 1 (15pts). Given the following data: Security Beta Expected Return 1.3 20% 0.8...

CAPM Question

Problem 1 (15pts). Given the following data: Security Beta Expected Return 1.3 20% 0.8 14% 18% 1.2 (a) (10pts). Assume Securities 1 and 2 are correctly priced. Based on the CAPM, what is the expected return on the market? What is the risk-free rate? (b) (5pts). Would you recommend buying Security 3 according to CAPM? Why or why not?

CAPM Question

Problem 1 (15pts). Given the following data: Security Beta Expected Return 1.3 20% 0.8 14% 18% 1.2 (a) (10pts). Assume Securities 1 and 2 are correctly priced. Based on the CAPM, what is the expected return on the market? What is the risk-free rate? (b) (5pts). Would you recommend buying Security 3 according to CAPM? Why or why not?

Suppose you observe the following situation: Security Beta Expected Return Peat Co. 1.15 10.0 Re-Peat Co....

Suppose you observe the following situation: Security Beta Expected Return Peat Co. 1.15 10.0 Re-Peat Co. 0.90 9.0 Assume these securities are correctly priced. Based on the CAPM, what is the expected return on the market? What is the risk-free rate? (Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places.) Expected return on market % Risk-free rate %

Please show work/equations. Risk and Return Porfolio Weights and the Security Market Line Do not round...

Please show

work/equations.

Risk and Return Porfolio Weights and the Security Market Line Do not round any calculations From the Topic "Application of the SML"pp. 240-242 An investor wants to build a 2-stock portfolio of the following stocks: Stock Beta 1.3 0.85 Expected Return 7.80% 5.80% 14 If the investor wants the Portfolio Beta to be 1.1, what should the weights of each stock be in the portfolio? 16 sub-calc area Desired Portfolio beta: Weight of Stock A: Weight of...

Please show

work/equations.

Risk and Return Porfolio Weights and the Security Market Line Do not round any calculations From the Topic "Application of the SML"pp. 240-242 An investor wants to build a 2-stock portfolio of the following stocks: Stock Beta 1.3 0.85 Expected Return 7.80% 5.80% 14 If the investor wants the Portfolio Beta to be 1.1, what should the weights of each stock be in the portfolio? 16 sub-calc area Desired Portfolio beta: Weight of Stock A: Weight of...

Given the following information for the two stocks: Stock Expected Return Standard Deviation Investment Beta 16%...

Given the following information for the two stocks: Stock Expected Return Standard Deviation Investment Beta 16% 15% 300 10% $30,000 $20,000 0.8 You construct a portfolio composing of stocks A and B according to the above information. Assume that the risk free rate is 6% and the market risk premium (MRP) is 9%. Use the CAPM analysis to numerically determine whether this 2- stock portfolio is fairly priced? What is your investment recommendation on this portfolio? Why? ?E(Re) = 15.6%...

Given the following information for the two stocks: Stock Expected Return Standard Deviation Investment Beta 16% 15% 300 10% $30,000 $20,000 0.8 You construct a portfolio composing of stocks A and B according to the above information. Assume that the risk free rate is 6% and the market risk premium (MRP) is 9%. Use the CAPM analysis to numerically determine whether this 2- stock portfolio is fairly priced? What is your investment recommendation on this portfolio? Why? ?E(Re) = 15.6%...

4. Stock A has the expected return of 12%, the standard deviation of 15%, and the...

4. Stock A has the expected return of 12%, the standard deviation of 15%, and the CAPM beta of 0.5. Stock B has the expected return of 18%, the standard deviation of 20% and the CAPM beta of 1.1. The risk-free rate is 3%. If you have no other wealth could invest in some combination of the risk-free asset and only one of these two stocks, which of the stocks A and B will you choose and why? (1 point)

4. Stock A has the expected return of 12%, the standard deviation of 15%, and the CAPM beta of 0.5. Stock B has the expected return of 18%, the standard deviation of 20% and the CAPM beta of 1.1. The risk-free rate is 3%. If you have no other wealth could invest in some combination of the risk-free asset and only one of these two stocks, which of the stocks A and B will you choose and why? (1 point)

Problem 8-13 CAPM, portfolio risk, and return Consider the following information for three stocks, Stocks A, B, and...

Problem 8-13 CAPM, portfolio risk, and return Consider the following information for three stocks, Stocks A, B, and C. The returns on the three stocks are positively correlated, but they are not perfectly correlated. (That is, each of the correlation coefficients is between 0 and 1.) Stock Expected Return Standard Deviation Beta 14 8.78 % 14 % 0.8 10.83 1.3 11.65 1.5 Fund P has one-third of its funds invested in each of the three stocks. The risk-free rate is...

Problem 8-13 CAPM, portfolio risk, and return Consider the following information for three stocks, Stocks A, B, and C. The returns on the three stocks are positively correlated, but they are not perfectly correlated. (That is, each of the correlation coefficients is between 0 and 1.) Stock Expected Return Standard Deviation Beta 14 8.78 % 14 % 0.8 10.83 1.3 11.65 1.5 Fund P has one-third of its funds invested in each of the three stocks. The risk-free rate is...

Consider the following information Expected Standard Portfolio Return Deviation Risk-free 10% 1.0 Market 18 A 16...

Consider the following information Expected Standard Portfolio Return Deviation Risk-free 10% 1.0 Market 18 A 16 1.5 a. Calculate the return predicted by CAPM for a portfolio with a beta of 1.5 Return b. What is the alpha of portfolio A. (Negatlve value should be Indicated by a minus sign.) Alpha c. If the simple CAPM is valid, is the situation above possible? O Yes O No

Consider the following information Expected Standard Portfolio Return Deviation Risk-free 10% 1.0 Market 18 A 16 1.5 a. Calculate the return predicted by CAPM for a portfolio with a beta of 1.5 Return b. What is the alpha of portfolio A. (Negatlve value should be Indicated by a minus sign.) Alpha c. If the simple CAPM is valid, is the situation above possible? O Yes O No

Problem 8-13 CAPM, portfolio risk, and return Consider the following information for three stocks, Stocks A, B, and C....

Problem 8-13 CAPM, portfolio risk, and return Consider the following information for three stocks, Stocks A, B, and C. The returns on the three stocks are positively correlated, but they are not perfectly correlated. (That is, each of the correlation coefficients is between 0 and 1.) 1.3 Stock Expected Return Standard Deviation Beta 9.28 % 14 % 0.8 11.33 14 12.15 14 1.5 Fund P has one-third of its funds invested in each of the three stocks. The risk-free rate...

Problem 8-13 CAPM, portfolio risk, and return Consider the following information for three stocks, Stocks A, B, and C. The returns on the three stocks are positively correlated, but they are not perfectly correlated. (That is, each of the correlation coefficients is between 0 and 1.) 1.3 Stock Expected Return Standard Deviation Beta 9.28 % 14 % 0.8 11.33 14 12.15 14 1.5 Fund P has one-third of its funds invested in each of the three stocks. The risk-free rate...

Question 5 (8 points) a. The expected rates of return for stocks A and B are...

Question 5 (8 points) a. The expected rates of return for stocks A and B are 16% and 20% respectively. The beta of stock A is 0.7 while that of stock B is 0.8. The T-bill rate is 4% and the expected rate of return on S&P 500 index is 24%. The standard deviation of stock A is 20% while that of B is 32%. If you could invest only in T-bills plus one of these stocks, which stock would...

Question 5 (8 points) a. The expected rates of return for stocks A and B are 16% and 20% respectively. The beta of stock A is 0.7 while that of stock B is 0.8. The T-bill rate is 4% and the expected rate of return on S&P 500 index is 24%. The standard deviation of stock A is 20% while that of B is 32%. If you could invest only in T-bills plus one of these stocks, which stock would...

Assume that the assumptions of the CAPM hold. The expected return and the standard deviation of...

Assume that the assumptions of the CAPM hold. The expected return and the standard deviation of the market portfolio are 7% and 14%, respectively. There are two individual stocks A and B: Mean Return A: 4% Standard Deviation A: 18% Mean Return B: 12% Standard Deviation B: 36% Stock A has a correlation of 0.2 with the market portfolio. A.What is the beta of stock A? B.What is the risk free rate? C.What is the beta of a portfolio with...

CAPM Question

Problem 1 (15pts). Given the following data: Security Beta Expected Return 1.3 20% 0.8 14% 18% 1.2 (a) (10pts). Assume Securities 1 and 2 are correctly priced. Based on the CAPM, what is the expected return on the market? What is the risk-free rate? (b) (5pts). Would you recommend buying Security 3 according to CAPM? Why or why not?

CAPM Question

Problem 1 (15pts). Given the following data: Security Beta Expected Return 1.3 20% 0.8 14% 18% 1.2 (a) (10pts). Assume Securities 1 and 2 are correctly priced. Based on the CAPM, what is the expected return on the market? What is the risk-free rate? (b) (5pts). Would you recommend buying Security 3 according to CAPM? Why or why not?

Please show

work/equations.

Risk and Return Porfolio Weights and the Security Market Line Do not round any calculations From the Topic "Application of the SML"pp. 240-242 An investor wants to build a 2-stock portfolio of the following stocks: Stock Beta 1.3 0.85 Expected Return 7.80% 5.80% 14 If the investor wants the Portfolio Beta to be 1.1, what should the weights of each stock be in the portfolio? 16 sub-calc area Desired Portfolio beta: Weight of Stock A: Weight of...

Please show

work/equations.

Risk and Return Porfolio Weights and the Security Market Line Do not round any calculations From the Topic "Application of the SML"pp. 240-242 An investor wants to build a 2-stock portfolio of the following stocks: Stock Beta 1.3 0.85 Expected Return 7.80% 5.80% 14 If the investor wants the Portfolio Beta to be 1.1, what should the weights of each stock be in the portfolio? 16 sub-calc area Desired Portfolio beta: Weight of Stock A: Weight of...

Given the following information for the two stocks: Stock Expected Return Standard Deviation Investment Beta 16% 15% 300 10% $30,000 $20,000 0.8 You construct a portfolio composing of stocks A and B according to the above information. Assume that the risk free rate is 6% and the market risk premium (MRP) is 9%. Use the CAPM analysis to numerically determine whether this 2- stock portfolio is fairly priced? What is your investment recommendation on this portfolio? Why? ?E(Re) = 15.6%...

Given the following information for the two stocks: Stock Expected Return Standard Deviation Investment Beta 16% 15% 300 10% $30,000 $20,000 0.8 You construct a portfolio composing of stocks A and B according to the above information. Assume that the risk free rate is 6% and the market risk premium (MRP) is 9%. Use the CAPM analysis to numerically determine whether this 2- stock portfolio is fairly priced? What is your investment recommendation on this portfolio? Why? ?E(Re) = 15.6%...

4. Stock A has the expected return of 12%, the standard deviation of 15%, and the CAPM beta of 0.5. Stock B has the expected return of 18%, the standard deviation of 20% and the CAPM beta of 1.1. The risk-free rate is 3%. If you have no other wealth could invest in some combination of the risk-free asset and only one of these two stocks, which of the stocks A and B will you choose and why? (1 point)

4. Stock A has the expected return of 12%, the standard deviation of 15%, and the CAPM beta of 0.5. Stock B has the expected return of 18%, the standard deviation of 20% and the CAPM beta of 1.1. The risk-free rate is 3%. If you have no other wealth could invest in some combination of the risk-free asset and only one of these two stocks, which of the stocks A and B will you choose and why? (1 point)

Problem 8-13 CAPM, portfolio risk, and return Consider the following information for three stocks, Stocks A, B, and C. The returns on the three stocks are positively correlated, but they are not perfectly correlated. (That is, each of the correlation coefficients is between 0 and 1.) Stock Expected Return Standard Deviation Beta 14 8.78 % 14 % 0.8 10.83 1.3 11.65 1.5 Fund P has one-third of its funds invested in each of the three stocks. The risk-free rate is...

Problem 8-13 CAPM, portfolio risk, and return Consider the following information for three stocks, Stocks A, B, and C. The returns on the three stocks are positively correlated, but they are not perfectly correlated. (That is, each of the correlation coefficients is between 0 and 1.) Stock Expected Return Standard Deviation Beta 14 8.78 % 14 % 0.8 10.83 1.3 11.65 1.5 Fund P has one-third of its funds invested in each of the three stocks. The risk-free rate is...

Consider the following information Expected Standard Portfolio Return Deviation Risk-free 10% 1.0 Market 18 A 16 1.5 a. Calculate the return predicted by CAPM for a portfolio with a beta of 1.5 Return b. What is the alpha of portfolio A. (Negatlve value should be Indicated by a minus sign.) Alpha c. If the simple CAPM is valid, is the situation above possible? O Yes O No

Consider the following information Expected Standard Portfolio Return Deviation Risk-free 10% 1.0 Market 18 A 16 1.5 a. Calculate the return predicted by CAPM for a portfolio with a beta of 1.5 Return b. What is the alpha of portfolio A. (Negatlve value should be Indicated by a minus sign.) Alpha c. If the simple CAPM is valid, is the situation above possible? O Yes O No

Problem 8-13 CAPM, portfolio risk, and return Consider the following information for three stocks, Stocks A, B, and C. The returns on the three stocks are positively correlated, but they are not perfectly correlated. (That is, each of the correlation coefficients is between 0 and 1.) 1.3 Stock Expected Return Standard Deviation Beta 9.28 % 14 % 0.8 11.33 14 12.15 14 1.5 Fund P has one-third of its funds invested in each of the three stocks. The risk-free rate...

Problem 8-13 CAPM, portfolio risk, and return Consider the following information for three stocks, Stocks A, B, and C. The returns on the three stocks are positively correlated, but they are not perfectly correlated. (That is, each of the correlation coefficients is between 0 and 1.) 1.3 Stock Expected Return Standard Deviation Beta 9.28 % 14 % 0.8 11.33 14 12.15 14 1.5 Fund P has one-third of its funds invested in each of the three stocks. The risk-free rate...

Question 5 (8 points) a. The expected rates of return for stocks A and B are 16% and 20% respectively. The beta of stock A is 0.7 while that of stock B is 0.8. The T-bill rate is 4% and the expected rate of return on S&P 500 index is 24%. The standard deviation of stock A is 20% while that of B is 32%. If you could invest only in T-bills plus one of these stocks, which stock would...

Question 5 (8 points) a. The expected rates of return for stocks A and B are 16% and 20% respectively. The beta of stock A is 0.7 while that of stock B is 0.8. The T-bill rate is 4% and the expected rate of return on S&P 500 index is 24%. The standard deviation of stock A is 20% while that of B is 32%. If you could invest only in T-bills plus one of these stocks, which stock would...

Most questions answered within 3 hours.

-

Company A is assigned $200,000 of goodwill arising from a recent

business combination. The current carrying...

asked 31 seconds ago -

Write any individual Class A IP address below. It cannot be

non-routable address. Include the subnet...

asked 1 minute ago -

Coronado Industries had January 1 inventory of $301000 when it

adopted dollar-value LIFO. During the year,...

asked 10 minutes ago -

The cable supporting a 2145-kg elevator has a maximum strength

of 2.18×104 N.

a) What maximum...

asked 20 minutes ago -

Find the critical value(s) and rejection region(s) for a

two-tailed chi-square test with a sample size...

asked 24 minutes ago -

One of your experts gave me an answer of $7.36 but there are

many different answers...

asked 30 minutes ago -

Petrus Framing's cost formula for its supplies cost is $1,790

per month plus $10 per frame....

asked 43 minutes ago -

Introduction

Information design is a field that studies the way information

should be displayed, which is...

asked 40 minutes ago -

1.The main product of the reaction between p-cresol and Br2 /

FeBr3 is:

3-Bromo-4-methyl phenol

2-Bromo-4-methyl...

asked 44 minutes ago -

At present, concentration

of 92235U in naturally

occurring uranium deposits is approximately 0.74 %. What will the...

asked 47 minutes ago -

Question 1:

For the following reaction, 8.72 grams of nitrogen gas are

allowed to react with...

asked 49 minutes ago -

Discuss the benefits and detriments of hard water, and your

opinion on using water softeners.

asked 1 hour ago