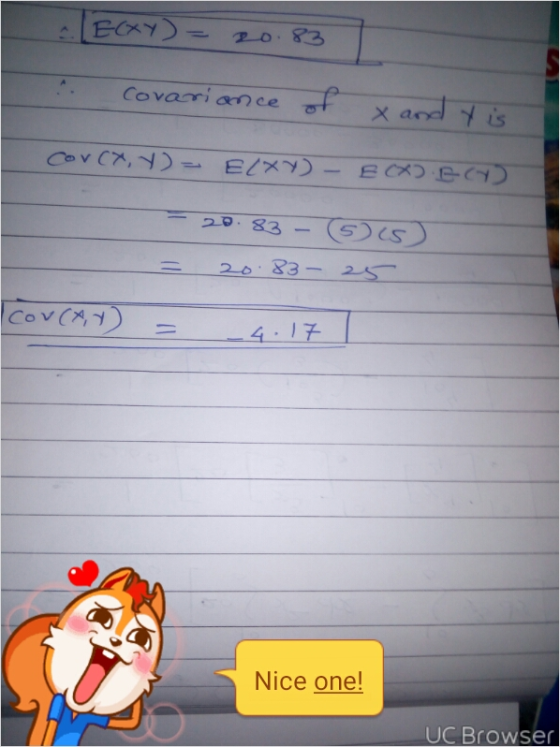

Annual windstorm losses, X and Y , in two different geographical regions are independent, and each...

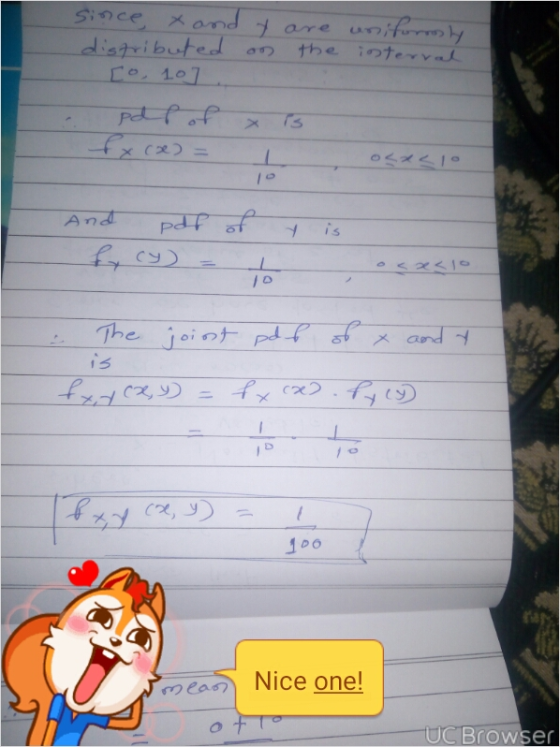

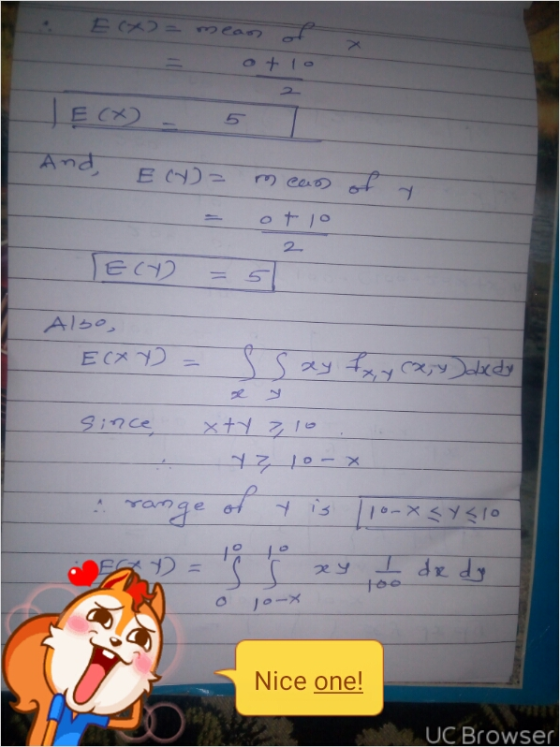

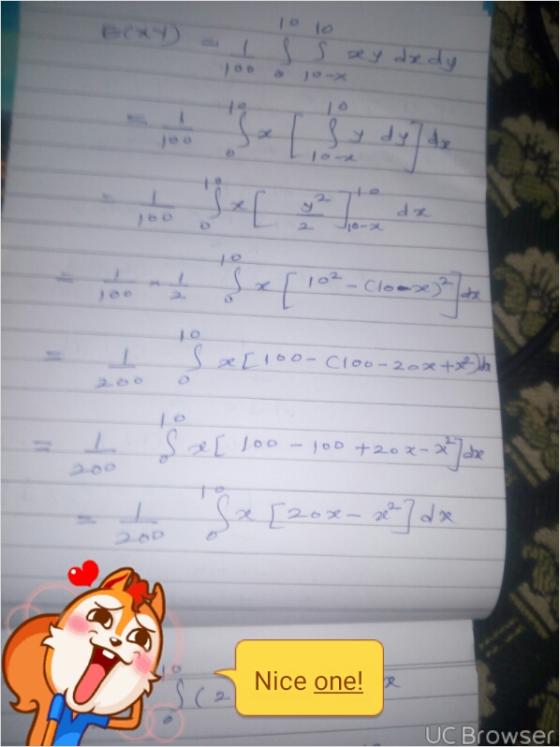

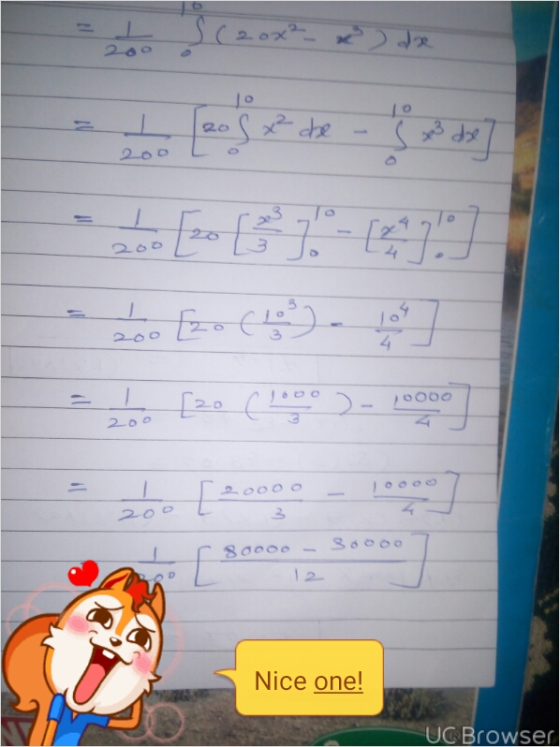

Annual windstorm losses, X and Y , in two different geographical regions are independent, and each is uniformly distributed on the interval [0, 10]. Calculate the covariance of X and Y , given that X + Y ≥ 10

Homework Answers

Add Answer to:

Annual windstorm losses, X and Y , in two different geographical

regions are independent, and each...

Problem 6: 10 points Assume that X and Y are independent random variables uniformly distributed over...

Problem 6: 10 points Assume that X and Y are independent random variables uniformly distributed over the unit interval (0,1) 1. Define Z-max (X, Y) as the larger of the two. Derive the C.D.F. and density function for Z. 2. Define Wmin (X, Y) as the smaller of the two. Derive the C.D.F. and density function for W 3. Derive the joint density of the pair (W, Z). Specify where the density if positive and where it takes a zero...

Problem 6: 10 points Assume that X and Y are independent random variables uniformly distributed over the unit interval (0,1) 1. Define Z-max (X, Y) as the larger of the two. Derive the C.D.F. and density function for Z. 2. Define Wmin (X, Y) as the smaller of the two. Derive the C.D.F. and density function for W 3. Derive the joint density of the pair (W, Z). Specify where the density if positive and where it takes a zero...

Problem 6: 10 points Assume that X and Y are independent random variables uniformly distributed over...

Problem 6: 10 points Assume that X and Y are independent random variables uniformly distributed over the unit interval (0,1) 1. Define Z max (X. Y) as the larger of the two, Derive the C.DF. and density function for Z. 2. Define W min(X,Y) as the smaller of the two. Derive the C.D.F.and density function for W 3. Derive the joint density of the pair (W. Z). Specify where the density if positive and where it takes a zero value....

Problem 6: 10 points Assume that X and Y are independent random variables uniformly distributed over the unit interval (0,1) 1. Define Z max (X. Y) as the larger of the two, Derive the C.DF. and density function for Z. 2. Define W min(X,Y) as the smaller of the two. Derive the C.D.F.and density function for W 3. Derive the joint density of the pair (W. Z). Specify where the density if positive and where it takes a zero value....

Let X and Y be independent random variables uniformly distributed on the interval [1,2]. What is ...

Let X and Y be independent random variables uniformly distributed on the interval [1,2]. What is the moment generating function of X + 2Y?

Let X and Y be independent random variables uniformly distributed on the interval [1,2]. What is the moment generating function of X + 2Y?

Let X and Y be independent random variables uniformly distributed on the interval [1,2]. What is the moment generating function of X + 2Y?

Let X and Y be independent random variables uniformly distributed on the interval [1,2]. What is the moment generating function of X + 2Y?

10. What is the probability density of the sum of two independent random variables, each of...

10. What is the probability density of the sum of two independent random variables, each of which is uniformly distributed over the interval 0, 1]?

10. What is the probability density of the sum of two independent random variables, each of which is uniformly distributed over the interval 0, 1]?

3. Suppose that X and Y are independent exponentially distributed random variables with parameter λ, and...

3. Suppose that X and Y are independent exponentially distributed random variables with parameter λ, and further suppose that U is a uniformly distributed random variable between 0 and 1 that is independent from X and Y. Calculate Pr(X<U< Y) and estimate numerically (based on a visual plot, for example) the value of λ that maximizes this probability.

3. Suppose that X and Y are independent exponentially distributed random variables with parameter λ, and further suppose that U is a uniformly distributed random variable between 0 and 1 that is independent from X and Y. Calculate Pr(X<U< Y) and estimate numerically (based on a visual plot, for example) the value of λ that maximizes this probability.

Show the random variables X and Y are independent, or not independent Find the joint cdf given the joint pdf below Suppose that (X, Y) is uniformly distributed over the region defined by 0 sys1-x2 a...

Show the random variables X and Y are independent, or not

independent

Find the joint cdf given the joint pdf below

Suppose that (X, Y) is uniformly distributed over the region defined by 0 sys1-x2 and -1sx 4 Therefore, the joint probability density function is, 0; Otherwise

Suppose that (X, Y) is uniformly distributed over the region defined by 0 sys1-x2 and -1sx 4

Therefore, the joint probability density function is, 0; Otherwise

Show the random variables X and Y are independent, or not

independent

Find the joint cdf given the joint pdf below

Suppose that (X, Y) is uniformly distributed over the region defined by 0 sys1-x2 and -1sx 4 Therefore, the joint probability density function is, 0; Otherwise

Suppose that (X, Y) is uniformly distributed over the region defined by 0 sys1-x2 and -1sx 4

Therefore, the joint probability density function is, 0; Otherwise

2) Two statistically-independent random variables, (X,Y), each have marginal probability density,...

2) Two statistically-independent random variables, (X,Y), each have marginal probability density, N(0,1) (e.g., zero-mean, unit-variance Gaussian). Let V-3X-Y, Z = X-Y Find the covariance matrix of the vector,

2) Two statistically-independent random variables, (X,Y), each have marginal probability density, N(0,1) (e.g., zero-mean, unit-variance Gaussian). Let V-3X-Y, Z = X-Y Find the covariance matrix of the vector,

2) Two statistically-independent random variables, (X,Y), each have marginal probability density, N(0,1) (e.g., zero-mean, unit-variance Gaussian). Let V-3X-Y, Z = X-Y Find the covariance matrix of the vector,

2) Two statistically-independent random variables, (X,Y), each have marginal probability density, N(0,1) (e.g., zero-mean, unit-variance Gaussian). Let V-3X-Y, Z = X-Y Find the covariance matrix of the vector,

Q4) Let X and Y be two independent N(0,1) random variable and 10 ei Find the covariance of Z and W.WE3-Y Q4) Let X and Y be two independent N(0,1) random variable and 10 ei Find the covarian...

Q4) Let X and Y be two independent N(0,1) random variable and 10 ei Find the covariance of Z and W.WE3-Y

Q4) Let X and Y be two independent N(0,1) random variable and 10 ei Find the covariance of Z and W.WE3-Y

Q4) Let X and Y be two independent N(0,1) random variable and 10 ei Find the covariance of Z and W.WE3-Y

Q4) Let X and Y be two independent N(0,1) random variable and 10 ei Find the covariance of Z and W.WE3-Y

Need only parts 5 and 6 Problem 6: 10 points Assume that X and Y are...

Need only parts 5 and 6

Problem 6: 10 points Assume that X and Y are independent random variables uniformly distributed over the unit interval (0, 1) 1. Define Z = max (X, Y) as the larger of the two. Derive the CD. F. and density function for Z 2. Define W- min (X, Y) as the smaller of the two. Derive the C.D.F. and density function for W. 3. Derive the joint density of the pair (W, Z). Specify...

Need only parts 5 and 6

Problem 6: 10 points Assume that X and Y are independent random variables uniformly distributed over the unit interval (0, 1) 1. Define Z = max (X, Y) as the larger of the two. Derive the CD. F. and density function for Z 2. Define W- min (X, Y) as the smaller of the two. Derive the C.D.F. and density function for W. 3. Derive the joint density of the pair (W, Z). Specify...

A subscription service stated that preference for different national magazines is independent of the geographical location...

A subscription service stated that preference for different national magazines is independent of the geographical location of the subscribers. A survey was conducted in which 300 persons randomly selected from two areas were given a choice of three different magazines. Each person expressed their favorite. The following results were obtained: Region Magazine A Magazine B Magazine C New England 75 50 175 Middle Atlantic 120 85 95 The critical value of chi square obtained from the table for a 5%...

Problem 6: 10 points Assume that X and Y are independent random variables uniformly distributed over the unit interval (0,1) 1. Define Z-max (X, Y) as the larger of the two. Derive the C.D.F. and density function for Z. 2. Define Wmin (X, Y) as the smaller of the two. Derive the C.D.F. and density function for W 3. Derive the joint density of the pair (W, Z). Specify where the density if positive and where it takes a zero...

Problem 6: 10 points Assume that X and Y are independent random variables uniformly distributed over the unit interval (0,1) 1. Define Z-max (X, Y) as the larger of the two. Derive the C.D.F. and density function for Z. 2. Define Wmin (X, Y) as the smaller of the two. Derive the C.D.F. and density function for W 3. Derive the joint density of the pair (W, Z). Specify where the density if positive and where it takes a zero...

Problem 6: 10 points Assume that X and Y are independent random variables uniformly distributed over the unit interval (0,1) 1. Define Z max (X. Y) as the larger of the two, Derive the C.DF. and density function for Z. 2. Define W min(X,Y) as the smaller of the two. Derive the C.D.F.and density function for W 3. Derive the joint density of the pair (W. Z). Specify where the density if positive and where it takes a zero value....

Problem 6: 10 points Assume that X and Y are independent random variables uniformly distributed over the unit interval (0,1) 1. Define Z max (X. Y) as the larger of the two, Derive the C.DF. and density function for Z. 2. Define W min(X,Y) as the smaller of the two. Derive the C.D.F.and density function for W 3. Derive the joint density of the pair (W. Z). Specify where the density if positive and where it takes a zero value....

Let X and Y be independent random variables uniformly distributed on the interval [1,2]. What is the moment generating function of X + 2Y?

Let X and Y be independent random variables uniformly distributed on the interval [1,2]. What is the moment generating function of X + 2Y?

Let X and Y be independent random variables uniformly distributed on the interval [1,2]. What is the moment generating function of X + 2Y?

Let X and Y be independent random variables uniformly distributed on the interval [1,2]. What is the moment generating function of X + 2Y?

10. What is the probability density of the sum of two independent random variables, each of which is uniformly distributed over the interval 0, 1]?

10. What is the probability density of the sum of two independent random variables, each of which is uniformly distributed over the interval 0, 1]?

3. Suppose that X and Y are independent exponentially distributed random variables with parameter λ, and further suppose that U is a uniformly distributed random variable between 0 and 1 that is independent from X and Y. Calculate Pr(X<U< Y) and estimate numerically (based on a visual plot, for example) the value of λ that maximizes this probability.

3. Suppose that X and Y are independent exponentially distributed random variables with parameter λ, and further suppose that U is a uniformly distributed random variable between 0 and 1 that is independent from X and Y. Calculate Pr(X<U< Y) and estimate numerically (based on a visual plot, for example) the value of λ that maximizes this probability.

Show the random variables X and Y are independent, or not

independent

Find the joint cdf given the joint pdf below

Suppose that (X, Y) is uniformly distributed over the region defined by 0 sys1-x2 and -1sx 4 Therefore, the joint probability density function is, 0; Otherwise

Suppose that (X, Y) is uniformly distributed over the region defined by 0 sys1-x2 and -1sx 4

Therefore, the joint probability density function is, 0; Otherwise

Show the random variables X and Y are independent, or not

independent

Find the joint cdf given the joint pdf below

Suppose that (X, Y) is uniformly distributed over the region defined by 0 sys1-x2 and -1sx 4 Therefore, the joint probability density function is, 0; Otherwise

Suppose that (X, Y) is uniformly distributed over the region defined by 0 sys1-x2 and -1sx 4

Therefore, the joint probability density function is, 0; Otherwise

2) Two statistically-independent random variables, (X,Y), each have marginal probability density, N(0,1) (e.g., zero-mean, unit-variance Gaussian). Let V-3X-Y, Z = X-Y Find the covariance matrix of the vector,

2) Two statistically-independent random variables, (X,Y), each have marginal probability density, N(0,1) (e.g., zero-mean, unit-variance Gaussian). Let V-3X-Y, Z = X-Y Find the covariance matrix of the vector,

2) Two statistically-independent random variables, (X,Y), each have marginal probability density, N(0,1) (e.g., zero-mean, unit-variance Gaussian). Let V-3X-Y, Z = X-Y Find the covariance matrix of the vector,

2) Two statistically-independent random variables, (X,Y), each have marginal probability density, N(0,1) (e.g., zero-mean, unit-variance Gaussian). Let V-3X-Y, Z = X-Y Find the covariance matrix of the vector,

Q4) Let X and Y be two independent N(0,1) random variable and 10 ei Find the covariance of Z and W.WE3-Y

Q4) Let X and Y be two independent N(0,1) random variable and 10 ei Find the covariance of Z and W.WE3-Y

Q4) Let X and Y be two independent N(0,1) random variable and 10 ei Find the covariance of Z and W.WE3-Y

Q4) Let X and Y be two independent N(0,1) random variable and 10 ei Find the covariance of Z and W.WE3-Y

Need only parts 5 and 6

Problem 6: 10 points Assume that X and Y are independent random variables uniformly distributed over the unit interval (0, 1) 1. Define Z = max (X, Y) as the larger of the two. Derive the CD. F. and density function for Z 2. Define W- min (X, Y) as the smaller of the two. Derive the C.D.F. and density function for W. 3. Derive the joint density of the pair (W, Z). Specify...

Need only parts 5 and 6

Problem 6: 10 points Assume that X and Y are independent random variables uniformly distributed over the unit interval (0, 1) 1. Define Z = max (X, Y) as the larger of the two. Derive the CD. F. and density function for Z 2. Define W- min (X, Y) as the smaller of the two. Derive the C.D.F. and density function for W. 3. Derive the joint density of the pair (W, Z). Specify...

Most questions answered within 3 hours.

-

The Baily Corporation has developed a specialized software

program that improves inventory control capability. The following...

asked 17 seconds ago -

Problem 5-4A (Part Level Submission) Wolford Department Store is

located in midtown Metropolis. During the past...

asked 24 seconds ago -

Preparation of Benzoic Acid using a Grignard Reagent URGENT

1. During your Grignard formation, a small...

asked 23 minutes ago -

A uniform magnetic field is perpendicular to the plane of a wire

loop. If the loop...

asked 22 minutes ago -

At the peak of your career, your were earning $120,000 and

holding a top level position....

asked 25 minutes ago -

. A permanent magnet is dropped south-end-down through a horizontal

circular coil with a radius of...

asked 27 minutes ago -

Bernie's Beverages purchased some fixed assets classified as

5-year property for MACRS. The assets cost $28,000....

asked 41 minutes ago -

How many ATPs are produced from the catabolism of a 10-C

molecule of fatty acid under...

asked 46 minutes ago -

Before practicing a routine on the rings, a 64.8 kg gymnast

hangs motionless, with one hand...

asked 47 minutes ago -

If the K b of a weak base is 6.3 × 10 − 6 , what...

asked 54 minutes ago -

Which of the following is the minimum amount of moles of NaOH

that must be added...

asked 57 minutes ago -

Stories about organizational ________ provide important clues

about cultural values and norms.

a. myths

b. heroes...

asked 59 minutes ago